Anteris stock soars after enrolling first patients in pivotal heart valve trial

Dover Corporation (NYSE:DOV) reported strong third-quarter results on October 23, 2025, highlighting margin expansion across all five business segments despite mixed organic revenue growth. The industrial conglomerate raised its full-year earnings guidance while maintaining its revenue outlook, pointing to continued operational efficiency and strategic positioning in high-growth markets.

Quarterly Performance Highlights

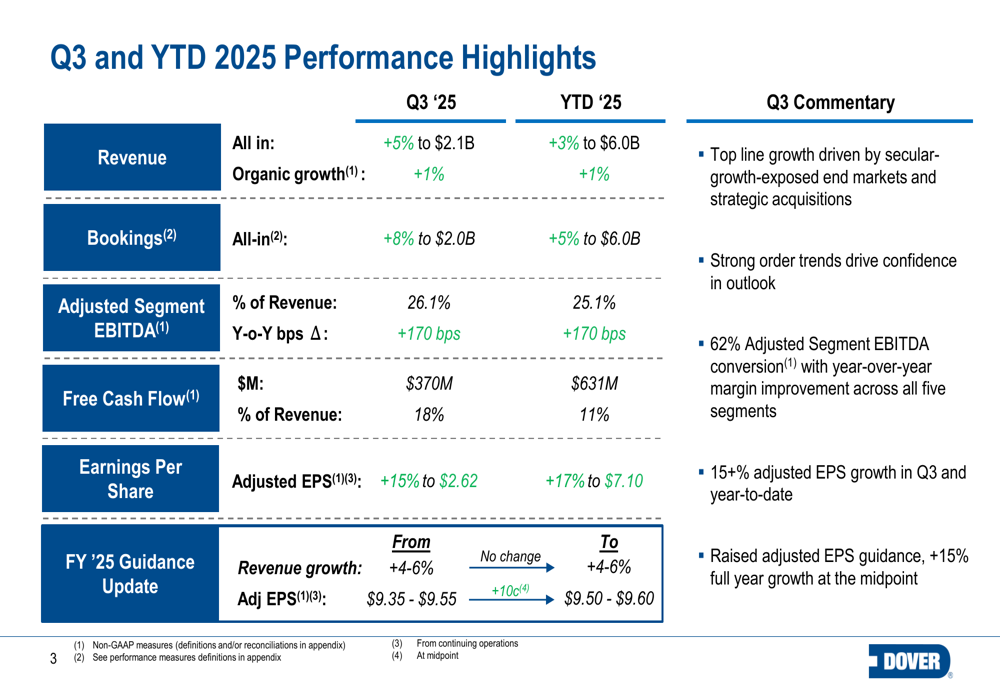

Dover delivered Q3 2025 revenue of $2.1 billion, representing 5% all-in growth and 1% organic growth compared to the prior year. The company reported adjusted earnings per share of $2.62, a 15% increase year-over-year, exceeding analyst expectations of $2.51. Notably, Dover achieved a 26.1% adjusted segment EBITDA margin, improving 170 basis points from Q3 2024.

As shown in the following performance summary, Dover’s free cash flow generation remained robust at $370 million in Q3, representing 18% of revenue:

The company’s stock responded positively to these results, rising 5.13% to $176.20 in regular trading following the announcement, with pre-market activity showing a 1.49% increase.

Segment Performance Analysis

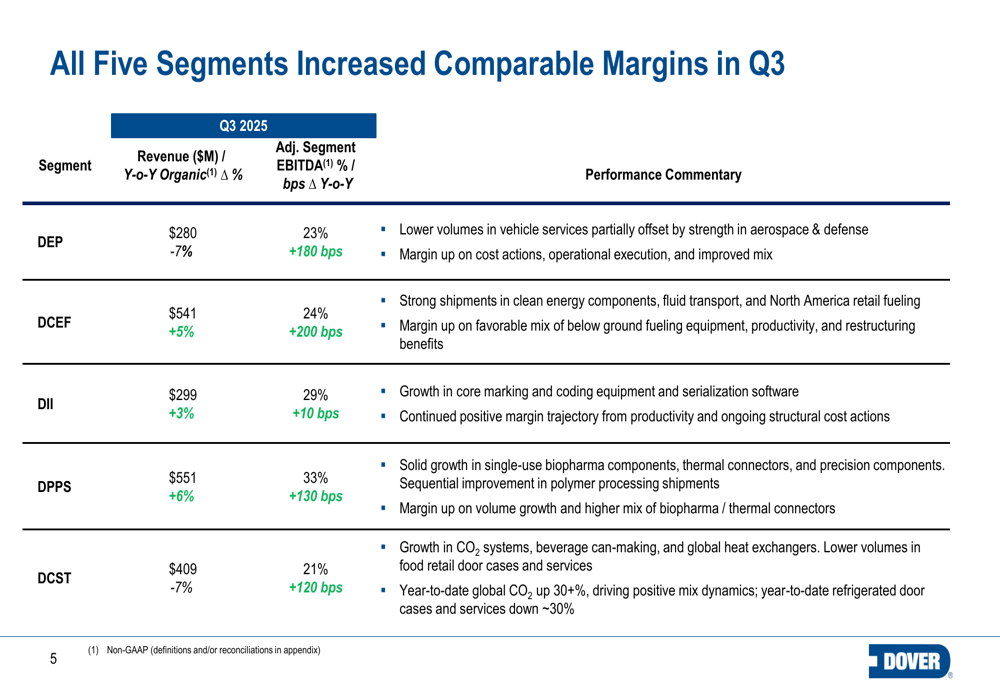

All five of Dover’s business segments achieved margin expansion in the third quarter, despite varying organic revenue growth rates. The Pumps & Process Solutions segment led performance with 33% adjusted segment EBITDA margin, while Clean Energy & Fueling delivered the strongest organic revenue growth at 5%.

The following segment breakdown illustrates the performance across Dover’s portfolio:

Brad Cerepak, Dover’s CFO, noted during the earnings call: "Our continued focus on operational excellence and cost discipline has enabled margin expansion across all segments, even in those facing temporary volume challenges."

The Climate & Sustainability Technologies and Engineered Products segments both experienced organic revenue declines of 7%, yet still managed to improve margins through cost actions and favorable mix. Meanwhile, Imaging & Identification achieved modest 3% organic growth while maintaining its strong margin trajectory.

Bookings Momentum and Cash Flow

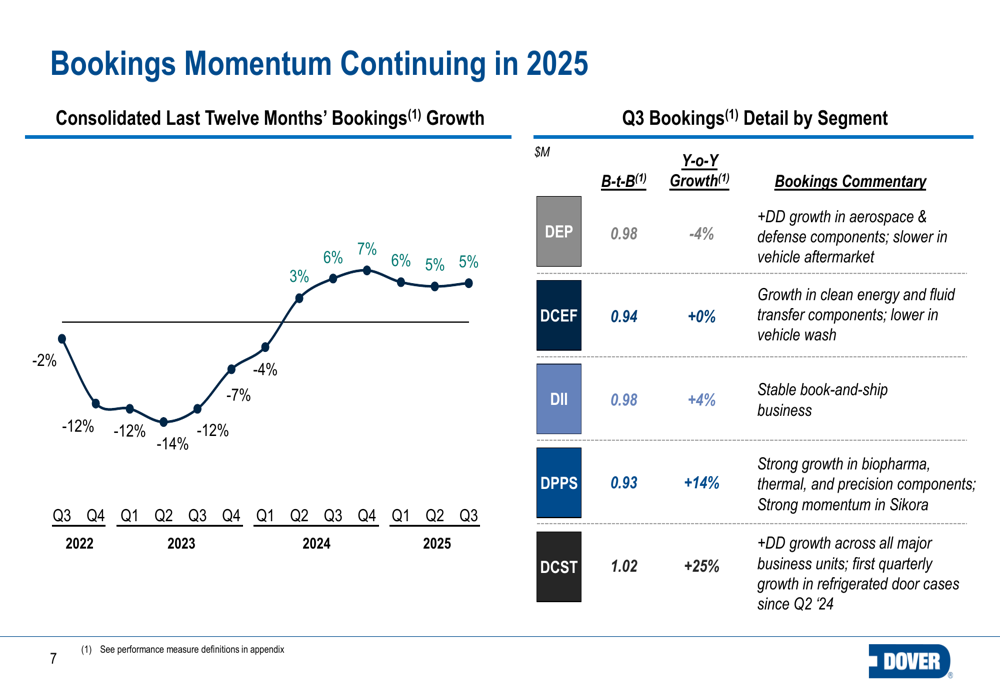

Dover’s bookings showed encouraging momentum, increasing 8% year-over-year to $2.0 billion in Q3 2025. The company has now achieved bookings growth in seven of the last eight quarters, providing visibility into future revenue streams.

The following chart illustrates Dover’s consistent bookings performance:

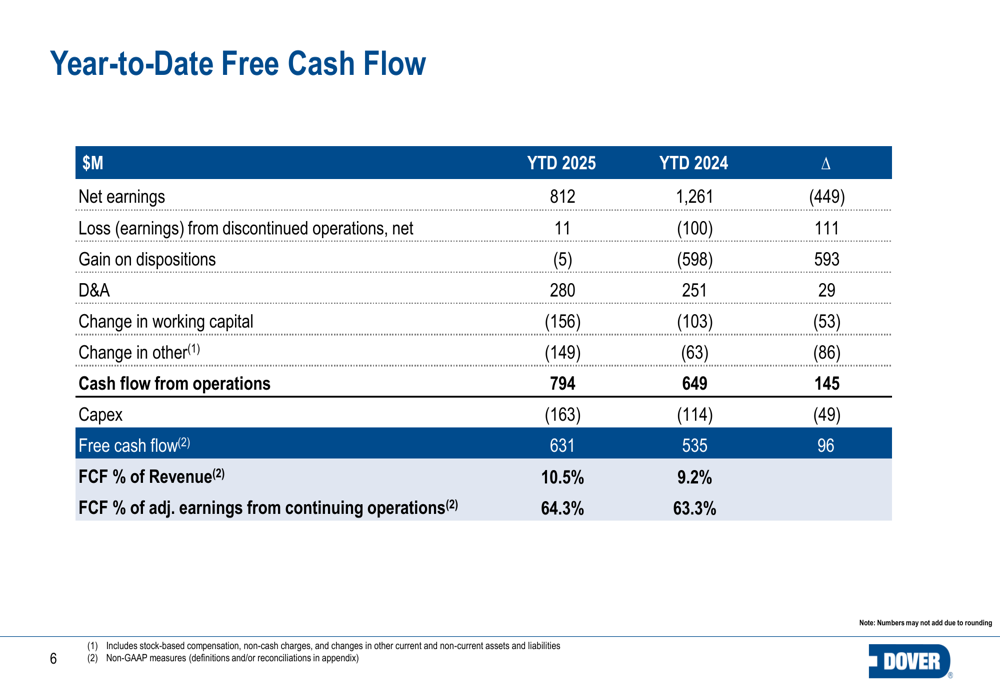

Free cash flow generation remained a strength, with year-to-date free cash flow reaching $631 million, representing 11% of revenue and 64.3% of adjusted earnings from continuing operations. This represents a significant improvement from the prior year.

As shown in the detailed cash flow reconciliation below:

Strategic Growth Initiatives

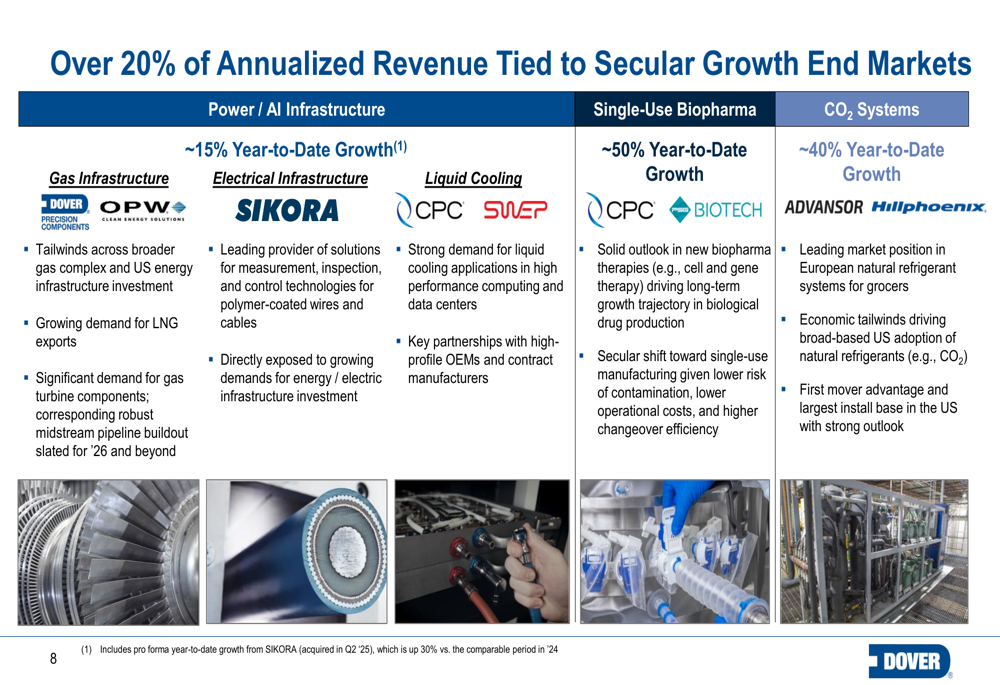

Dover highlighted that over 20% of its annualized revenue is tied to secular growth end markets, including gas infrastructure, power/AI infrastructure, electrical infrastructure, liquid cooling, single-use biopharma, and CO2 systems. These markets are expected to outpace general industrial growth rates in the coming years.

The following image details Dover’s positioning in these high-growth markets:

CEO Richard J. Tobin emphasized this strategic focus during the earnings call, stating: "We are well positioned as we begin to transition into 2026, and our advantaged balance sheet provides attractive optionality to selectively play offense to continue driving shareholder returns."

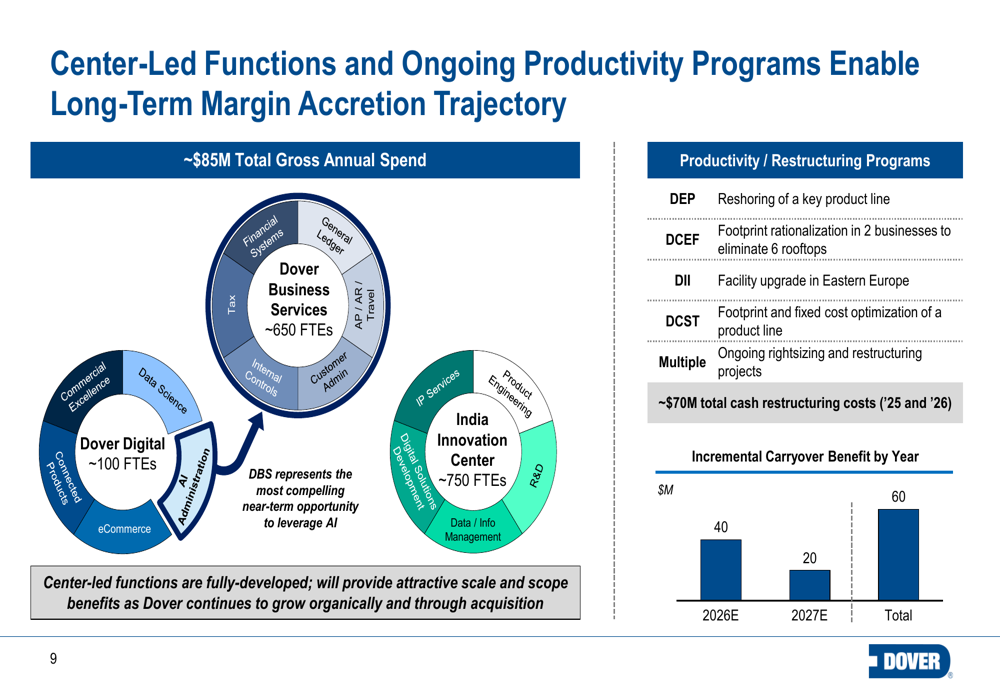

The company is also advancing productivity initiatives through center-led functions, with approximately $85 million in total gross annual spend on productivity and restructuring programs. These initiatives are expected to deliver incremental benefits in 2026 and 2027.

As illustrated in the productivity programs overview:

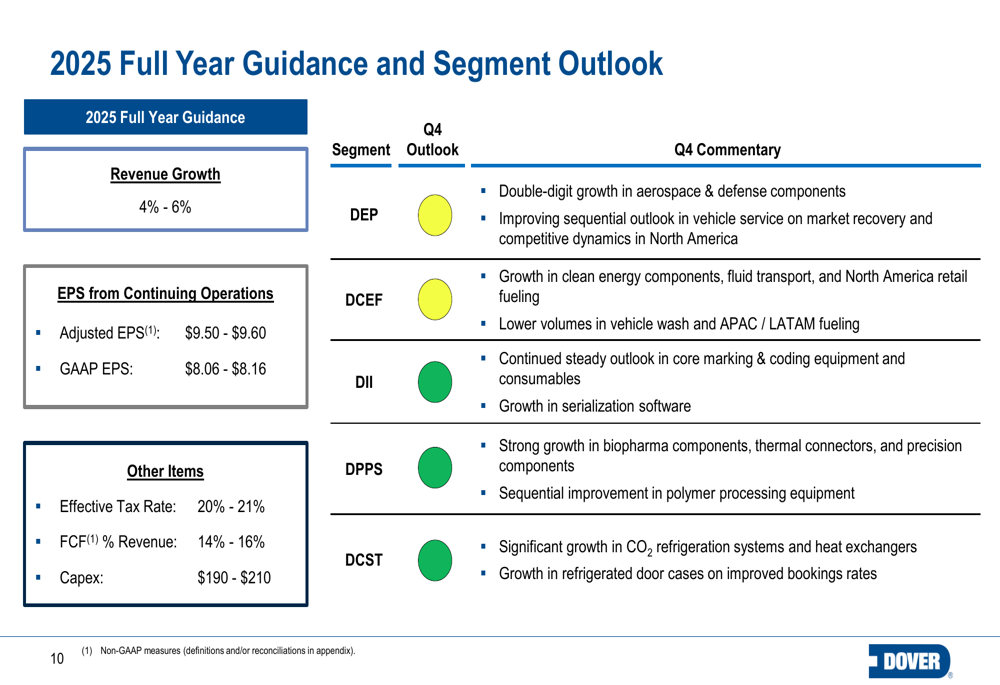

Forward Guidance & Outlook

Dover raised its full-year 2025 adjusted EPS guidance to $9.50-$9.60, up from the previous range of $9.35-$9.55, representing a $0.10 increase at the midpoint. The company maintained its revenue growth forecast of 4-6% for the full year.

The outlook for the fourth quarter varies by segment, with continued strength expected in Clean Energy & Fueling and Pumps & Process Solutions, while Climate & Sustainability Technologies and Engineered Products face ongoing market challenges.

As detailed in the guidance summary:

Looking ahead to 2026, Tobin noted, "I’m not aware of any business within the portfolio that’s forecasting down revenue for next year," suggesting continued growth despite macroeconomic uncertainties.

Dover’s diversified portfolio, margin expansion initiatives, and strategic positioning in secular growth markets appear to be resonating with investors, as evidenced by the stock’s positive reaction following the earnings announcement. With a strong balance sheet and consistent cash flow generation, the company remains well-positioned to navigate market challenges while pursuing selective growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.