Microsoft’s data-center shortages to persist longer than expected - Bloomberg

Introduction & Market Context

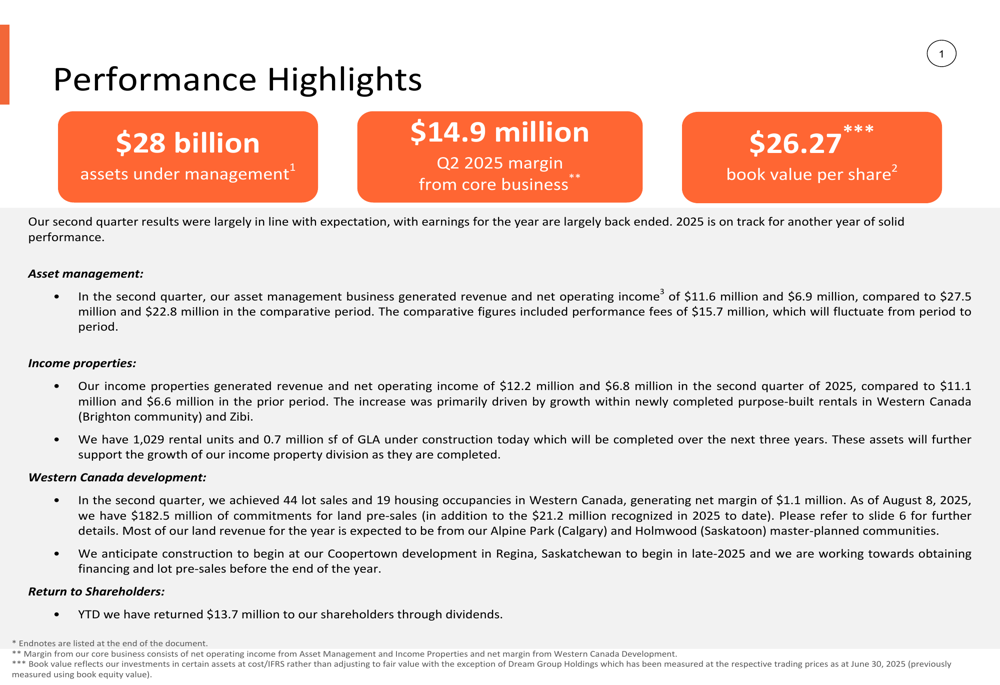

Dream Unlimited Corp (TSX:DRM) released its Q2 2025 supplemental information presentation on August 13, 2025, revealing a challenging quarter marked by significant earnings declines despite maintaining a substantial asset base. The Canadian real estate company, which operates across asset management, land development, and income properties segments, reported $28 billion in assets under management but faced headwinds in its core asset management business.

The company’s stock closed at $21.36 on August 12, 2025, trading at a substantial discount to its reported book value of $26.27 per share. This valuation gap highlights investor concerns about Dream’s near-term performance challenges, even as management suggests the company’s fair market value could be significantly higher.

Quarterly Performance Highlights

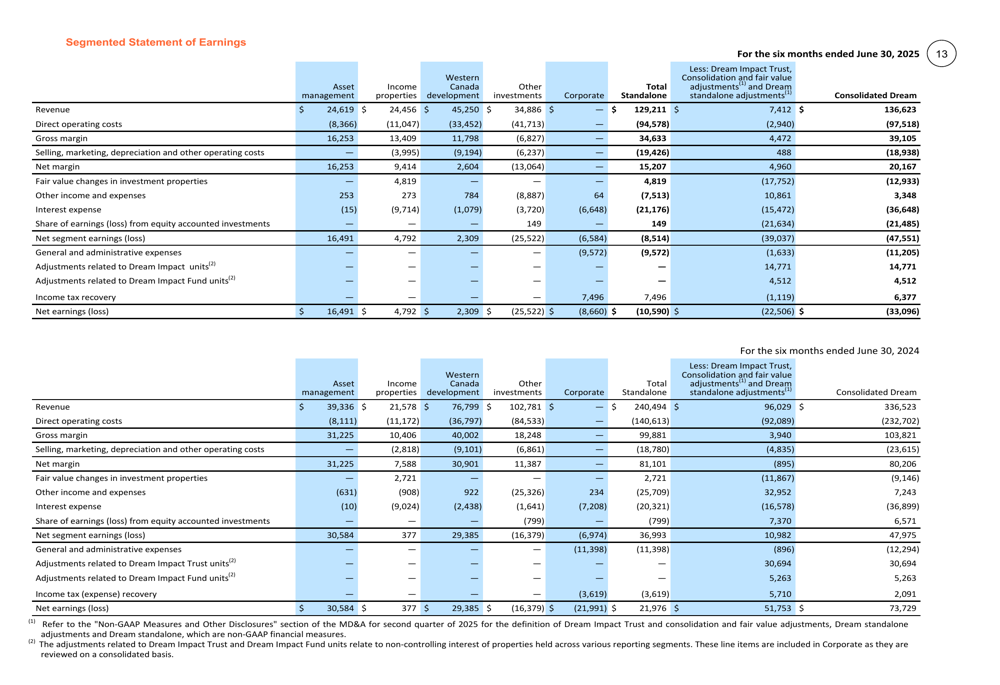

Dream Unlimited reported a $14.9 million margin from its core business in Q2 2025, but the company’s overall financial performance showed a marked deterioration compared to the prior year. For the six months ended June 30, 2025, Dream reported a net loss of $33.1 million, a stark contrast to the $73.7 million in net earnings reported for the same period in 2024.

As shown in the following performance highlights, the company maintained its $28 billion in assets under management while continuing to return capital to shareholders:

In the Western Canada development segment, Dream completed 44 lot sales and 19 housing occupancies in the second quarter, generating a net margin of $1.1 million. The company has secured $182.5 million in commitments for land pre-sales, in addition to the $21.2 million already recognized in 2025, indicating potential future revenue streams.

Segment Analysis

Asset Management

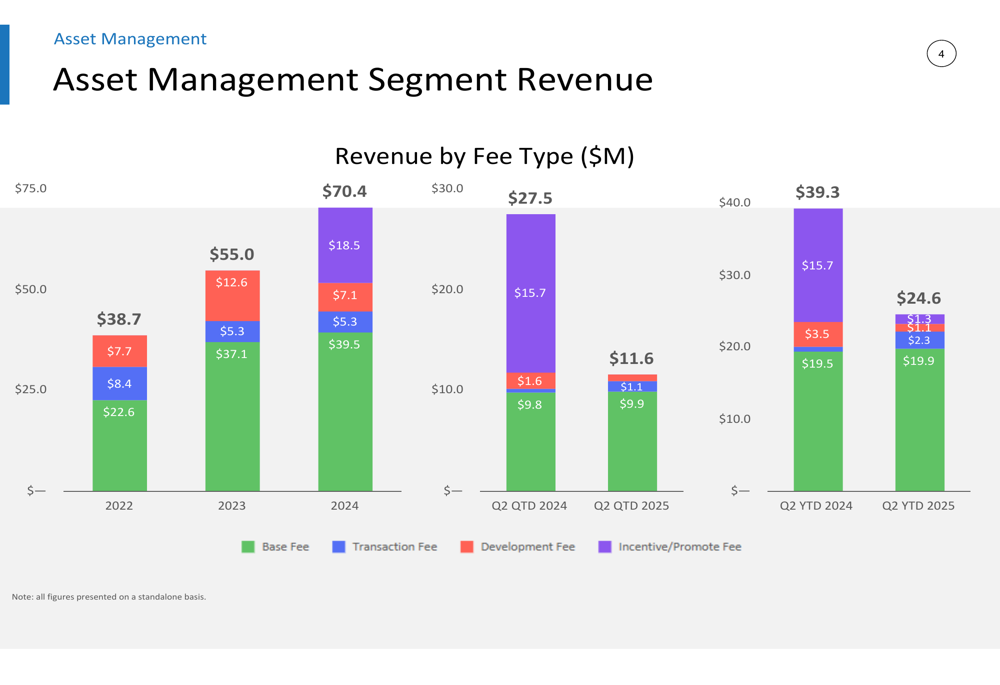

Dream’s asset management business experienced a significant decline in Q2 2025, generating revenue and net operating income of $11.6 million and $6.9 million respectively, compared to $27.5 million and $22.8 million in the comparative period. This represents a nearly 58% decrease in revenue and a 70% drop in operating income year-over-year.

The company’s asset management portfolio includes four publicly traded vehicles (Dream Impact Trust, Dream Office REIT, Dream Industrial REIT, and Dream Residential REIT) and six private investment vehicles focused on industrial, multi-family, and impact investments.

The following chart illustrates the breakdown of asset management revenue by fee type, highlighting the substantial decline in incentive/promote fees, which fell from $15.7 million in Q2 2024 to just $0.6 million in Q2 2025:

Western Canada Development

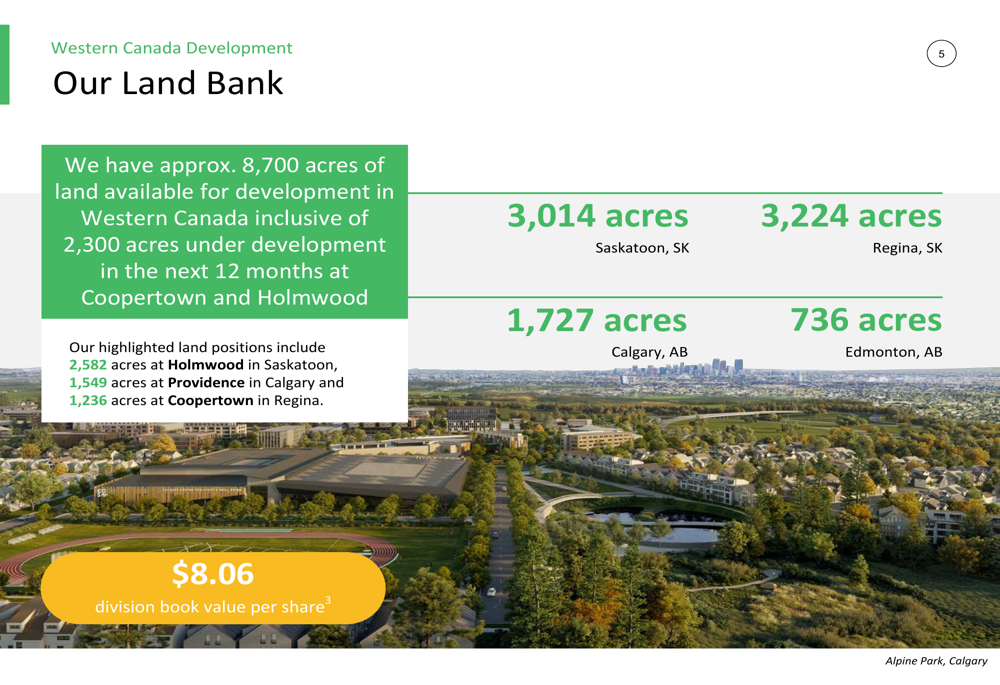

Dream maintains approximately 8,700 acres of land available for development across Western Canada, with holdings in Saskatoon (3,014 acres), Regina (3,224 acres), Calgary (1,727 acres), and Edmonton (736 acres). The company reports a division book value per share of $8.06 for this segment.

The land bank represents a significant future revenue opportunity, as illustrated in the following breakdown:

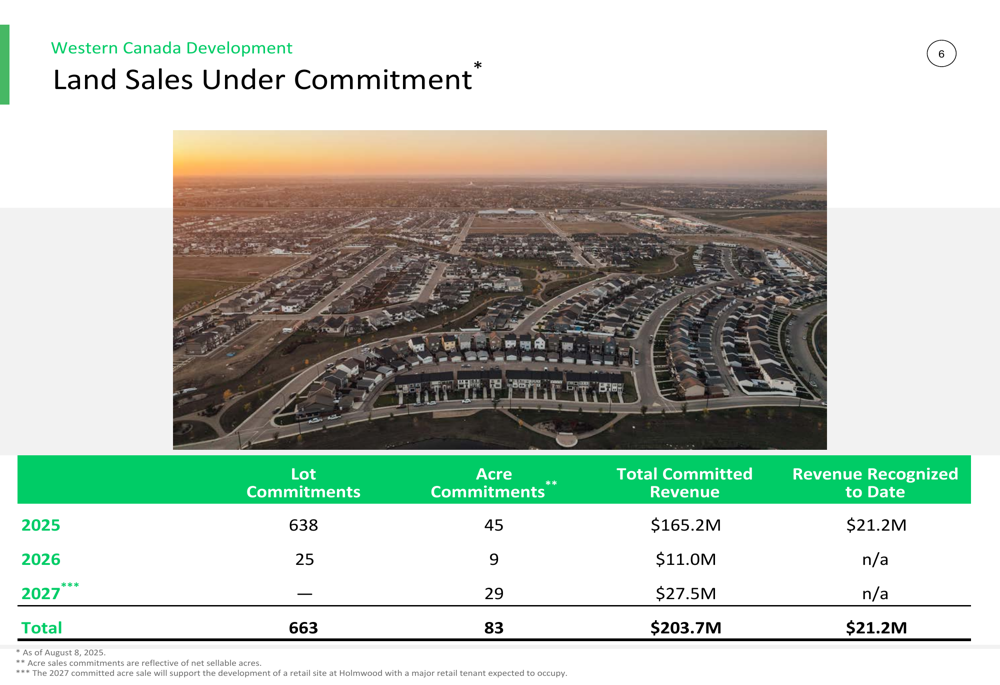

As of August 8, 2025, Dream has secured commitments for future land sales totaling $203.7 million, with only $21.2 million recognized to date. These commitments include 663 lot commitments and 83 acre commitments spanning from 2025 through 2027, providing visibility into future cash flows:

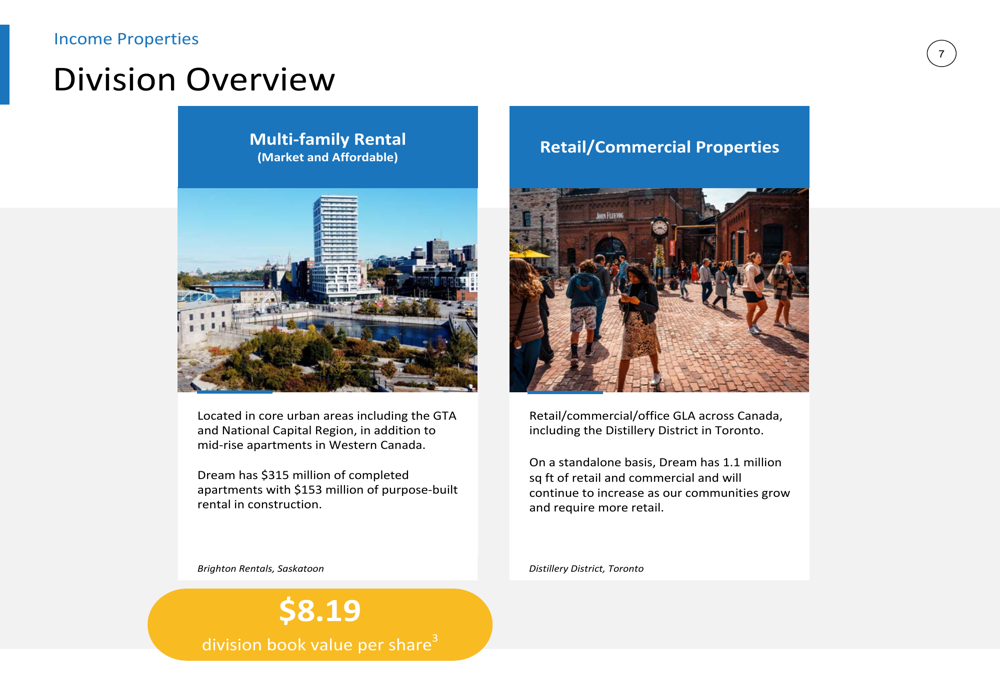

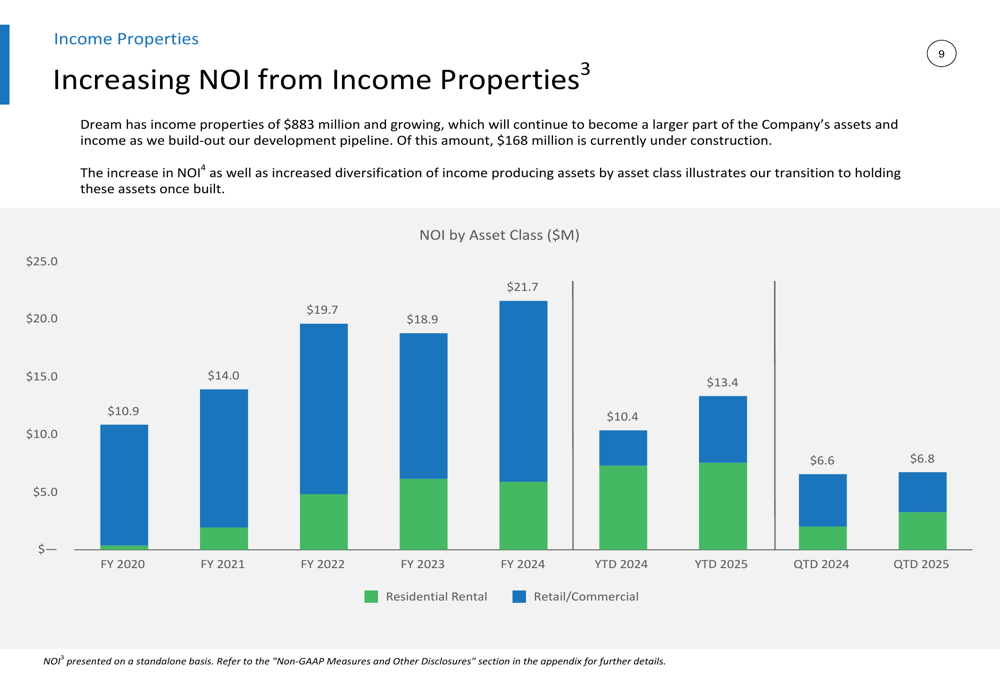

Income Properties

Dream’s income properties segment showed modest growth, generating revenue and net operating income of $12.2 million and $6.8 million in Q2 2025, compared to $11.1 million and $6.6 million in the prior period. This segment includes multi-family rentals and retail/commercial properties with a division book value per share of $8.19.

The company’s income properties portfolio is detailed in the following overview:

Dream is actively expanding its rental portfolio, with plans to add 1,029 apartment units comprising approximately 0.7 million square feet of residential space over the next three years. This expansion is expected to increase the net operating income from the income properties portfolio.

The company’s net operating income from income properties has shown growth over time, though recent quarters indicate some moderation:

Balance Sheet and Valuation

Dream Unlimited reported total assets of $2.62 billion as of June 30, 2025, with total liabilities of $1.51 billion and shareholders’ equity of $1.11 billion. This translates to a book value per share of $26.27, which is significantly higher than the current share price of $21.03, suggesting potential undervaluation.

Management provides an illustrative approach to balance sheet valuation that suggests even greater potential upside. By applying market value adjustments, particularly to the Western Canada development and asset management segments, Dream estimates a fair market value per share of $51.69, more than double the current trading price:

Forward-Looking Statements

Despite current challenges, Dream Unlimited continues to focus on its long-term growth strategy, particularly in land development and income properties. The company has returned $13.7 million to shareholders through dividends year-to-date and maintains a substantial pipeline of future revenue through land sale commitments and rental property development.

The company’s funds from operations (FFO) per share was $0.09 for the three months ended June 30, 2025, and $0.05 for the six-month period, reflecting the current operational challenges but providing a base for potential recovery as land sales commitments materialize and rental properties continue to develop.

While Dream faces significant headwinds in its asset management business, the company’s diversified business model and substantial land holdings provide potential pathways for future value creation. Investors will be watching closely to see if management can translate these assets into improved financial performance in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.