Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Duell Oyj (HEL:DUELL) presented its Q3 2025 financial results on July 3, 2025, revealing a significant slowdown in growth amid challenging market conditions. The powersports and bicycle parts distributor reported minimal sales growth and declining profitability, prompting a downward revision of its full-year guidance.

The company’s stock closed at €4.28 on July 2, down significantly from the €7.12 level seen after its more positive Q2 results, reflecting investor concerns about the deteriorating market environment. Duell’s presentation highlighted weakening consumer confidence, particularly in Nordic markets, and unfavorable weather conditions that impacted seasonal sales.

Quarterly Performance Highlights

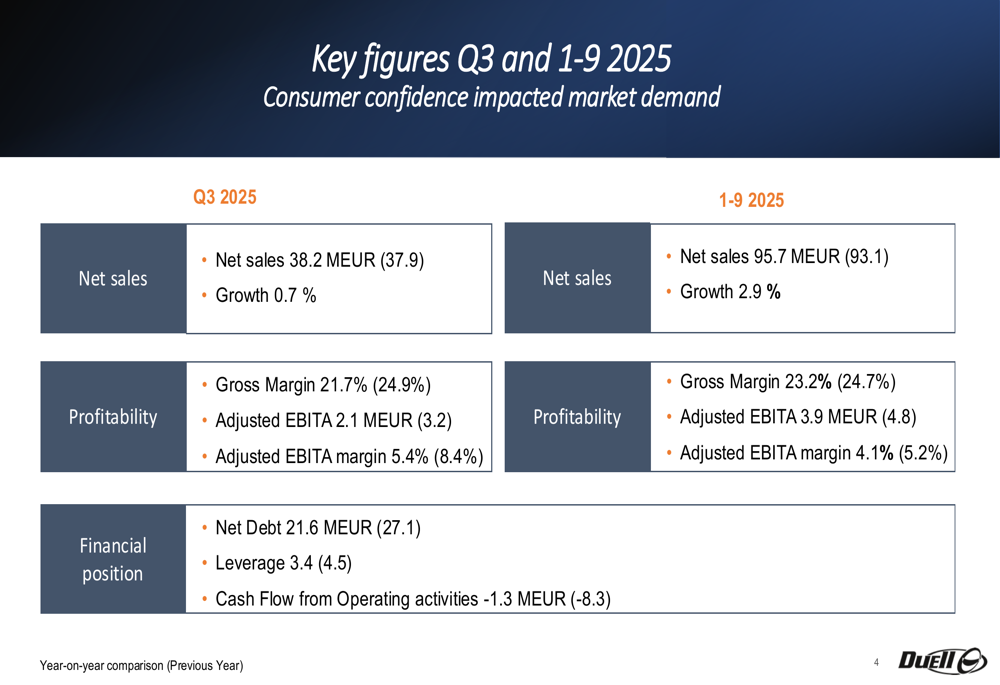

Duell reported Q3 2025 net sales of €38.2 million, representing a modest 0.7% increase compared to €37.9 million in the same period last year. However, when adjusted for comparable currencies, sales actually declined by 0.8%, indicating underlying weakness in core markets.

The company’s profitability metrics showed more pronounced deterioration. Q3 gross margin fell to 21.7% from 24.9% in the previous year, while adjusted EBITA dropped to €2.1 million from €3.2 million, resulting in an adjusted EBITA margin of 5.4% compared to 8.4% a year earlier.

As shown in the following financial summary chart:

For the first nine months of fiscal year 2025, Duell’s performance was somewhat better, with net sales reaching €95.7 million, up 2.9% from €93.1 million in the comparable period. However, profitability metrics for the nine-month period also showed declines, with gross margin falling to 23.2% from 24.7% and adjusted EBITA decreasing to €3.9 million from €4.8 million.

Detailed Financial Analysis

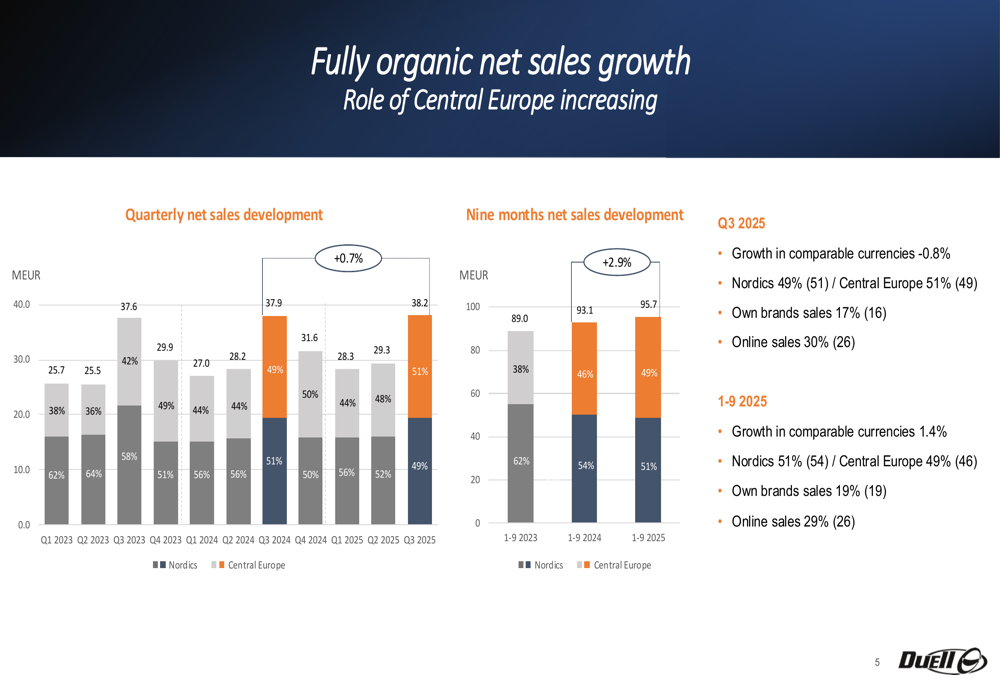

A notable shift in Duell’s business is the increasing importance of Central Europe, which now accounts for 51% of sales compared to 49% for Nordic markets. This represents a strategic pivot as the company faces headwinds in its traditional Nordic stronghold.

The company’s sales channels are also evolving, with online sales growing to 30% of total sales, up from 26% in the previous year. Own brand sales showed modest growth, increasing to 17% of total sales from 16% previously.

The following chart illustrates these regional and channel shifts:

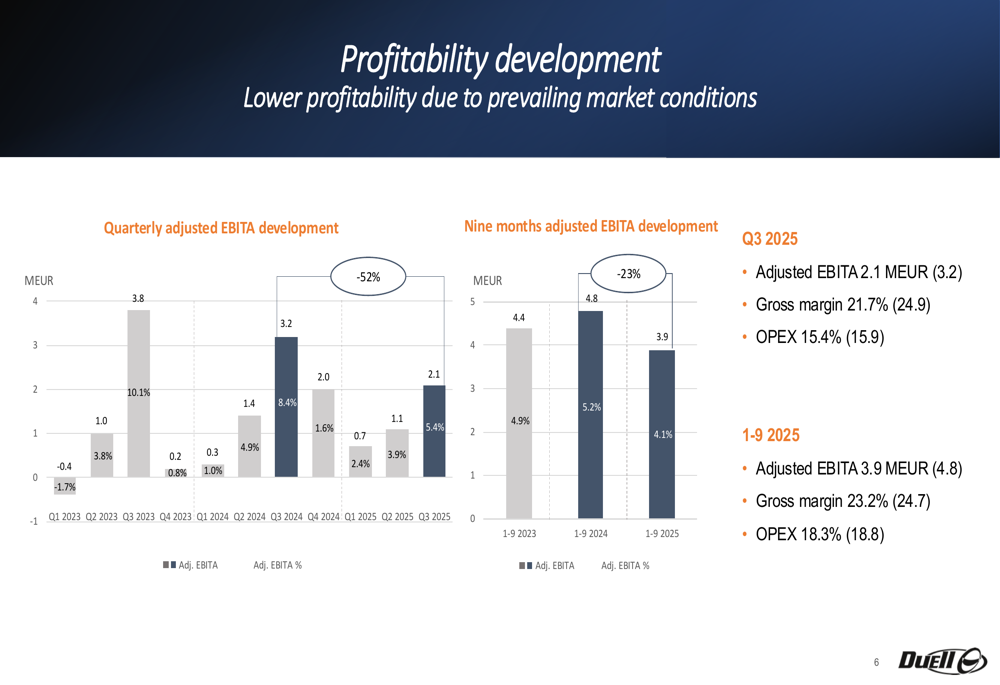

Profitability has been under pressure due to prevailing market conditions. The quarterly adjusted EBITA development shows a clear downward trend, with Q3 2025 marking one of the weakest quarters in recent periods:

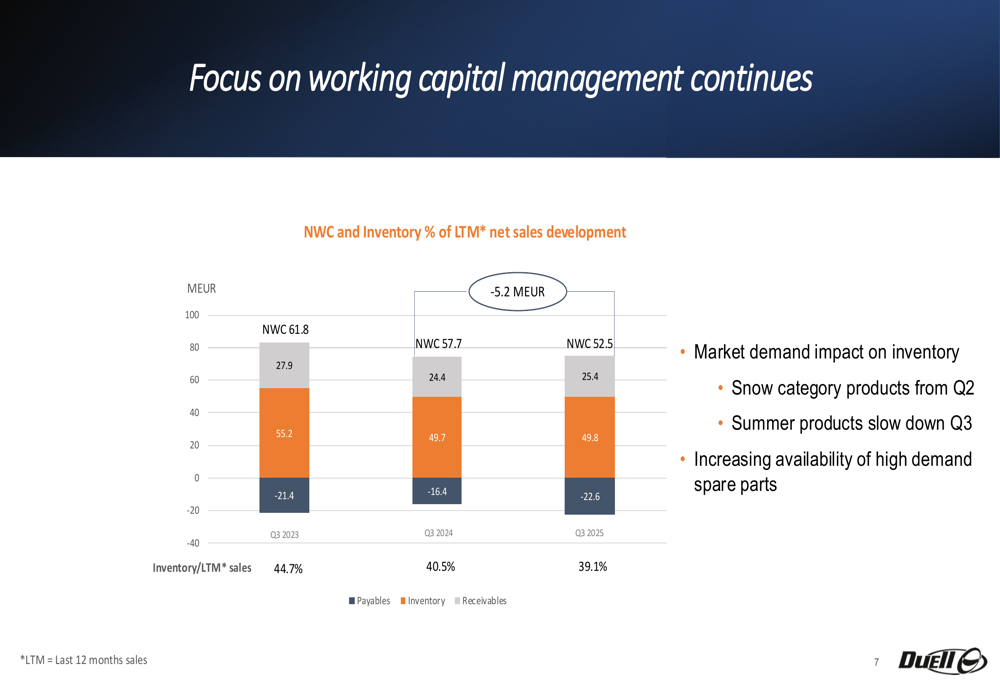

On a more positive note, Duell has made progress in working capital management. Net working capital decreased to €52.5 million in Q3 2025 from €57.7 million in Q3 2024, representing a €5.2 million improvement. Inventory as a percentage of last twelve months sales improved to 39.1% from 40.5% a year earlier.

The following chart shows the company’s working capital improvements:

Strategic Initiatives

Despite current challenges, Duell highlighted several operational bright spots. The company continues to see growth in Central Europe, supported by what it describes as "positive fundamentals." The bicycle category showed positive trends in Nordic countries, and the company reported solid performance in the tech category, where it boosted inventory on high-demand spare parts.

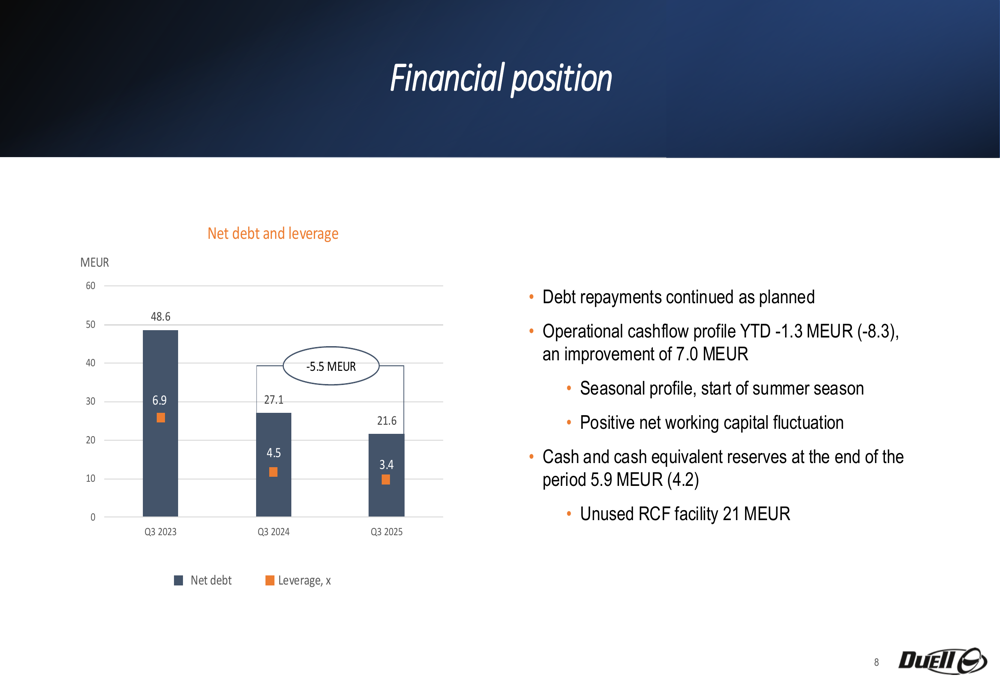

Duell’s financial position has improved in terms of debt metrics, with net debt decreasing to €21.6 million from €27.1 million a year earlier. This has resulted in an improved leverage ratio of 3.4 compared to 4.5 in the previous year. Cash flow from operating activities, while still negative at -€1.3 million, showed significant improvement from -€8.3 million in the previous year.

The following chart illustrates the company’s improving debt position:

Forward-Looking Statements

In a significant development, Duell lowered its guidance for the 2025 financial year on June 30, 2025. The company now expects organic net sales with comparable currencies to be at the same level or lower than the previous year, a downgrade from its earlier projection of sales being at the same level or higher. Similarly, adjusted EBITA is now expected to be below last year’s level, whereas previously the company had anticipated improvement.

The revised guidance reflects what Duell describes as a "more challenging" market environment that has impacted both sales and profitability. This represents a marked change from the optimistic outlook presented after Q2 results, when the company had anticipated a positive Q3 summer season.

Looking ahead, Duell outlined its strategic focus areas for the remainder of fiscal year 2025, emphasizing geographical expansion, partnerships for online sales, and product portfolio development. The company will prioritize profitability improvement, growth in selected markets, and efficient working capital management.

In summary, Duell’s Q3 2025 presentation revealed a company navigating significant market headwinds, particularly in its traditional Nordic markets. While making strategic progress in Central Europe and online channels, the overall financial performance has deteriorated, leading to lowered guidance. The company’s focus on debt reduction and working capital efficiency provides some financial flexibility as it works to address these challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.