Navitas stock soars as company advances 800V tech for NVIDIA AI platforms

Introduction & Market Context

Duluth Holdings Inc. (NASDAQ:DLTH) presented its second quarter 2025 financial results on September 4, 2025, revealing a return to profitability despite ongoing sales challenges. The workwear and casual clothing retailer reported net income of $1.3 million, a significant improvement from the $2.0 million loss in the same quarter last year, even as revenue continued to decline.

The company’s stock has faced significant pressure in recent months, trading at $2.36 as of September 3, 2025, well below its 52-week high of $4.20 and slightly above its 52-week low of $1.58. This presentation follows a challenging first quarter where the company reported a larger-than-expected loss, which triggered a sharp stock decline.

Quarterly Performance Highlights

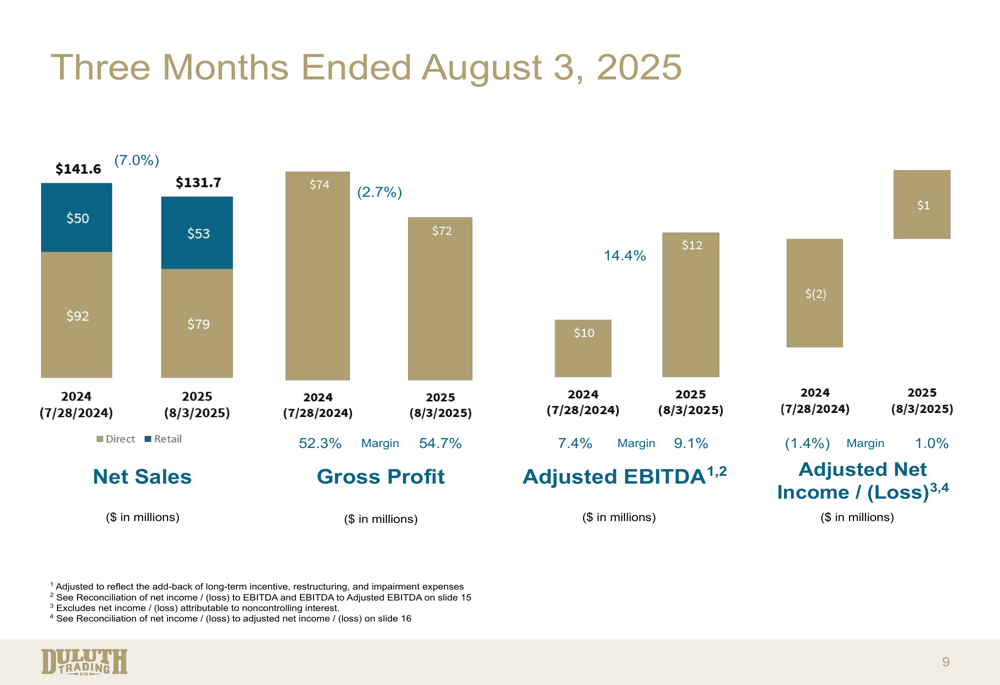

Duluth reported Q2 2025 net sales of $131.7 million, representing a 7.0% decrease compared to $141.6 million in the same period last year. Despite this revenue decline, the company achieved net income of $1.3 million, translating to reported earnings per share of $0.04 and adjusted EPS of $0.03.

As shown in the following chart of quarterly financial performance:

The company’s gross profit decreased slightly to $72 million, down 2.7% from the prior year, but gross margin improved significantly to 54.7% compared to 52.3% in Q2 2024. This margin expansion helped drive a $1.5 million increase in adjusted EBITDA to $12.0 million, representing 9.1% of net sales compared to 7.4% in the prior year.

A notable trend in the quarterly results was the divergence between sales channels. Direct sales (e-commerce and catalog) increased to $53 million from $50 million in the prior year, while retail store sales declined to $79 million from $92 million, reflecting changing consumer shopping preferences and possibly the impact of store optimization efforts.

Detailed Financial Analysis

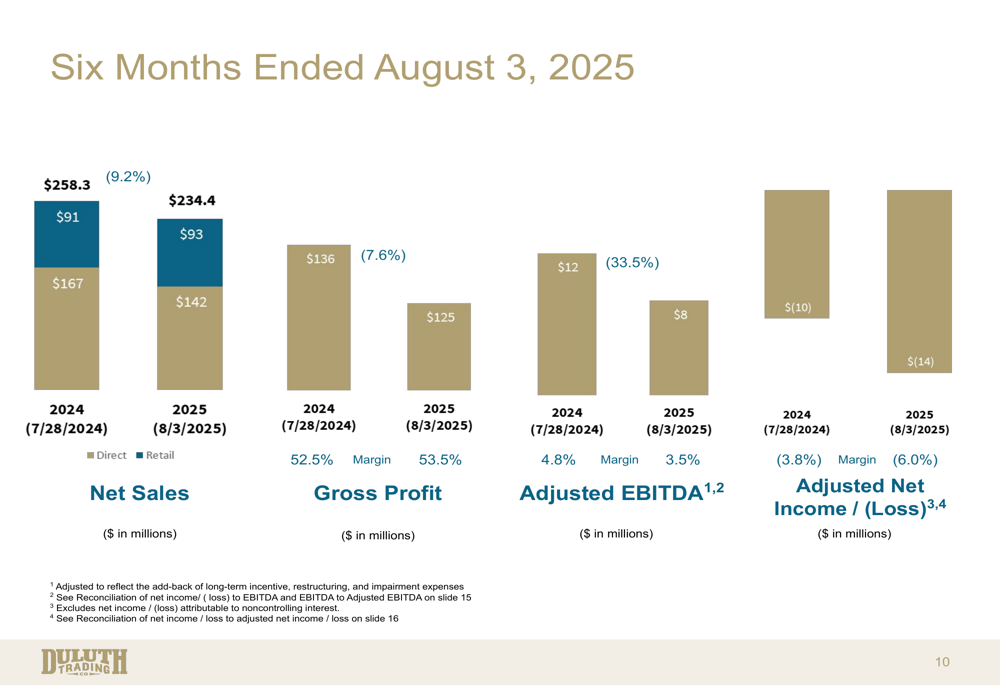

Looking at the six-month performance through August 3, 2025, Duluth’s results show more pronounced challenges:

For the first half of fiscal 2025, net sales decreased 9.2% to $234.4 million, with retail sales showing a significant decline of 15% while direct sales increased slightly. The company reported an adjusted net loss of $14 million for the six-month period, compared to a $10 million loss in the same period last year.

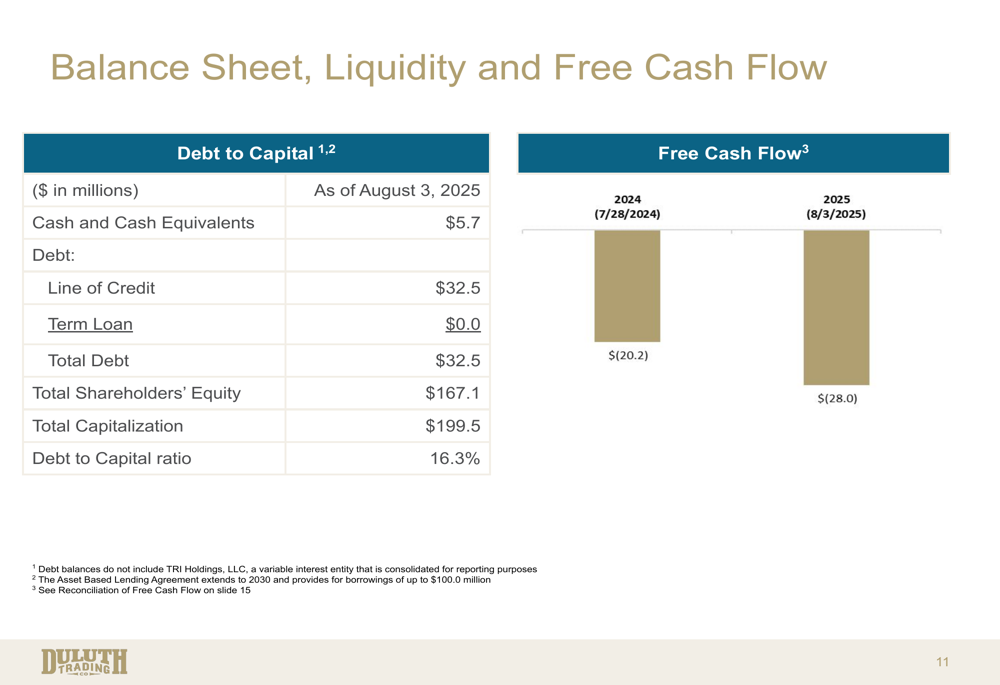

The company’s balance sheet and liquidity position as of August 3, 2025 showed:

Duluth maintained $5.7 million in cash and cash equivalents with $32.5 million drawn on its line of credit. The company’s debt-to-capital ratio stood at 16.3%, with total shareholders’ equity of $167.1 million. Free cash flow was negative at $(28.0) million for the three months ended August 3, 2025, deteriorating from $(20.2) million in the comparable period last year.

One positive development was inventory management, with inventory levels down $20.7 million or 12.2% compared to the previous year. This represents a significant improvement from Q1 2025, when inventory had increased by 29% year-over-year.

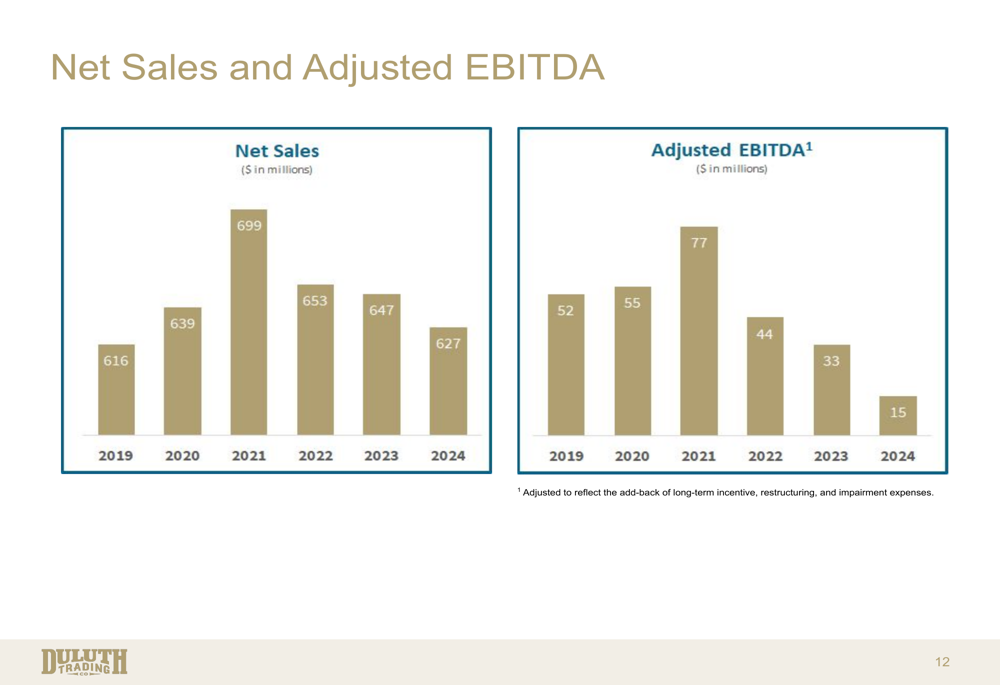

Looking at longer-term trends, Duluth’s financial performance has been challenging since its peak in 2021:

The historical data reveals that net sales have been gradually declining from a high of $699 million in 2021 to $627 million in 2024. More concerning is the sharp drop in adjusted EBITDA from $77 million in 2021 to just $15 million in 2024, reflecting significant margin pressure and operational challenges.

Strategic Initiatives & Outlook

Duluth Trading emphasizes its differentiation strategy through what it calls its "Secret Sauce":

The company’s strategic focus remains on product innovation, distinctive marketing, and customer experience. However, the financial presentation suggests a shift toward operational efficiency and cost management rather than growth initiatives.

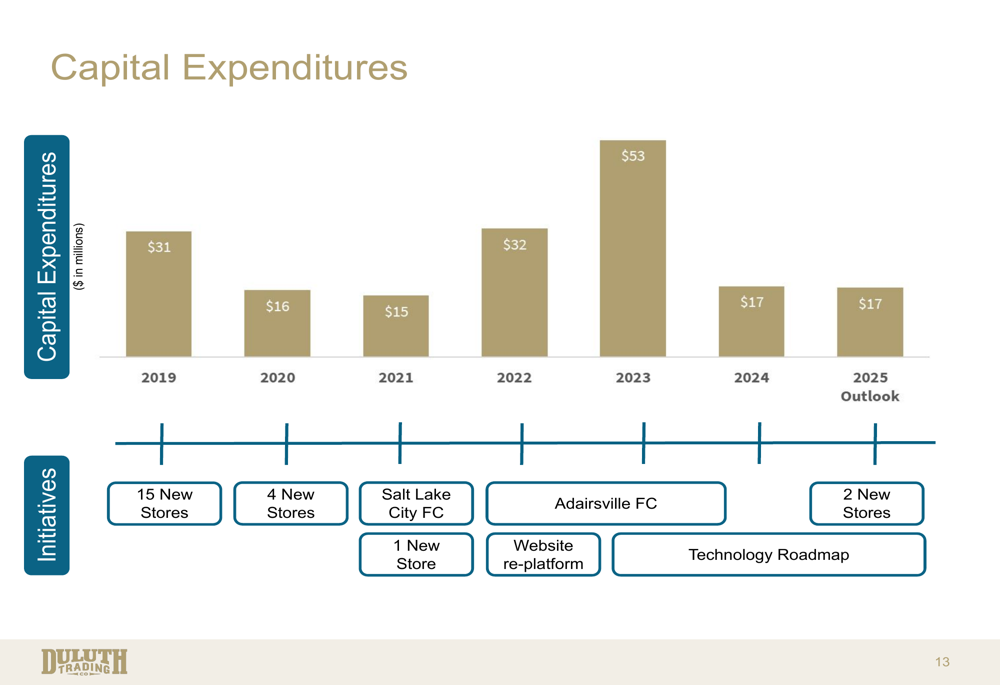

Capital expenditures have been significantly reduced in recent years, as shown in this chart:

After peaking at $53 million in 2023, capital expenditures decreased to $17 million in 2024, with the same amount projected for 2025. Recent initiatives have focused on technology investments including a website re-platform, rather than the aggressive store expansion seen in earlier years.

Despite the challenging first half, Duluth maintained its fiscal year 2025 guidance, projecting adjusted EBITDA in the range of $20 to $25 million. This implies a significant improvement in the second half of the year, as the company has achieved only $8 million in adjusted EBITDA through the first six months.

The maintained guidance contrasts with CEO Stephanie Pouliese’s comments from the Q1 earnings call, where she acknowledged the company was "taking decisive actions to get this great company and unique and powerful brand back on the path to profitability and growth." The Q2 results suggest these actions may be starting to yield results, though significant challenges remain.

As Duluth navigates this transition period, investors will be watching closely to see if the company can sustain its return to profitability while addressing the ongoing revenue challenges and evolving consumer preferences between direct and retail channels.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.