Paul Tudor Jones sees potential market rally after late October

Introduction & Market Context

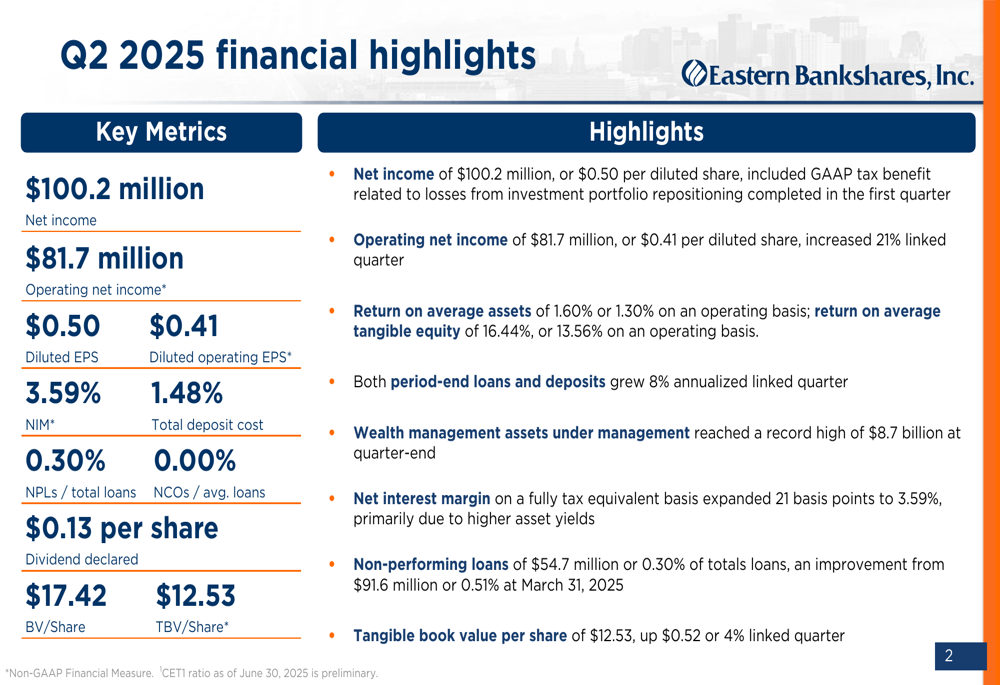

Eastern Bankshares Inc. (NASDAQ:EBC) released its second quarter 2025 earnings presentation on July 25, showcasing continued improvement across key performance metrics. The Boston-based financial institution reported net income of $100.2 million and operating net income of $81.7 million, demonstrating significant progress in its profitability journey while preparing for its planned merger with Harbor One.

The bank’s stock closed at $15.77 on July 25 and gained 2.35% in after-hours trading following the presentation, reflecting positive investor sentiment toward the results. With a 52-week range of $13.51 to $19.40, the stock appears to be recovering from the 5.22% decline it experienced after the previous quarter’s earnings release.

Quarterly Performance Highlights

Eastern Bankshares delivered strong financial results for Q2 2025, with diluted EPS of $0.50 and operating EPS of $0.41, marking a 21% increase from the previous quarter. The bank’s profitability metrics showed substantial improvement, with return on average assets reaching 1.60% and return on average tangible equity hitting 16.44%.

As shown in the following financial highlights chart, the bank achieved growth in both loans and deposits at an 8% annualized rate, while improving its net interest margin to 3.59%:

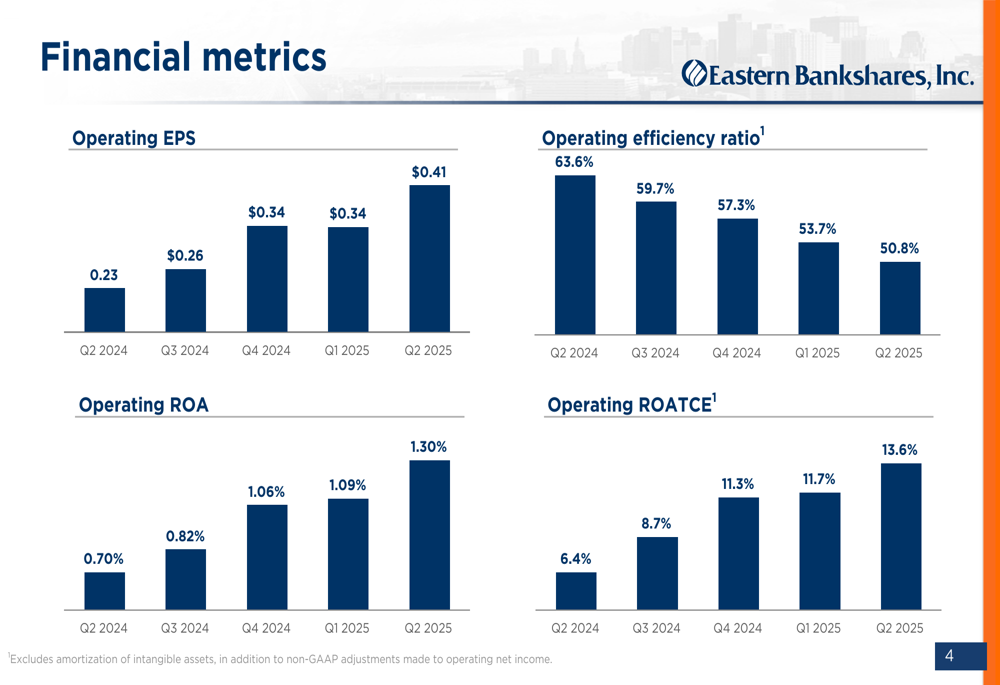

The bank’s operating metrics have shown consistent improvement over the past five quarters, with operating EPS growing from $0.23 in Q2 2024 to $0.41 in Q2 2025, representing a 78% increase year-over-year. Similarly, the operating efficiency ratio improved dramatically from 63.6% to 50.8% over the same period, demonstrating enhanced operational effectiveness.

The following chart illustrates the steady improvement in these key metrics:

Detailed Financial Analysis

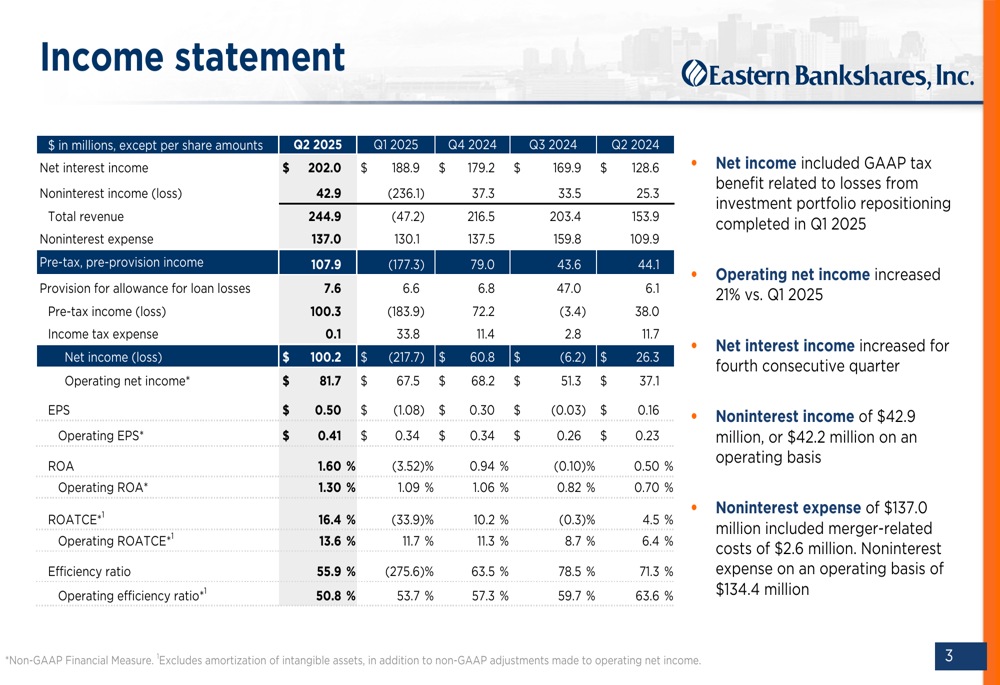

Eastern Bankshares’ income statement reveals that net interest income increased for the fourth consecutive quarter, reaching $202.0 million. Total (EPA:TTEF) revenue amounted to $244.9 million, while noninterest expense was $137.0 million, including $2.6 million in merger-related costs associated with the Harbor One transaction.

The detailed income statement shows the progression of key financial metrics over the past five quarters:

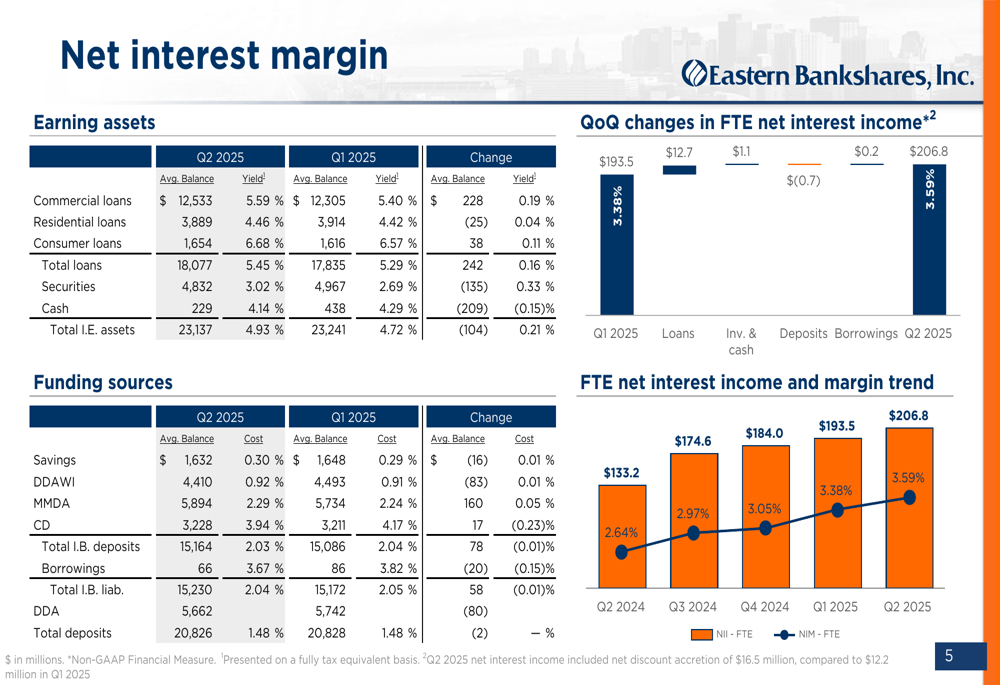

The bank’s net interest margin expanded by 21 basis points to 3.59%, driven by higher yields on loans and investments. This expansion has been a critical factor in the bank’s improved profitability, as illustrated in the following net interest margin analysis:

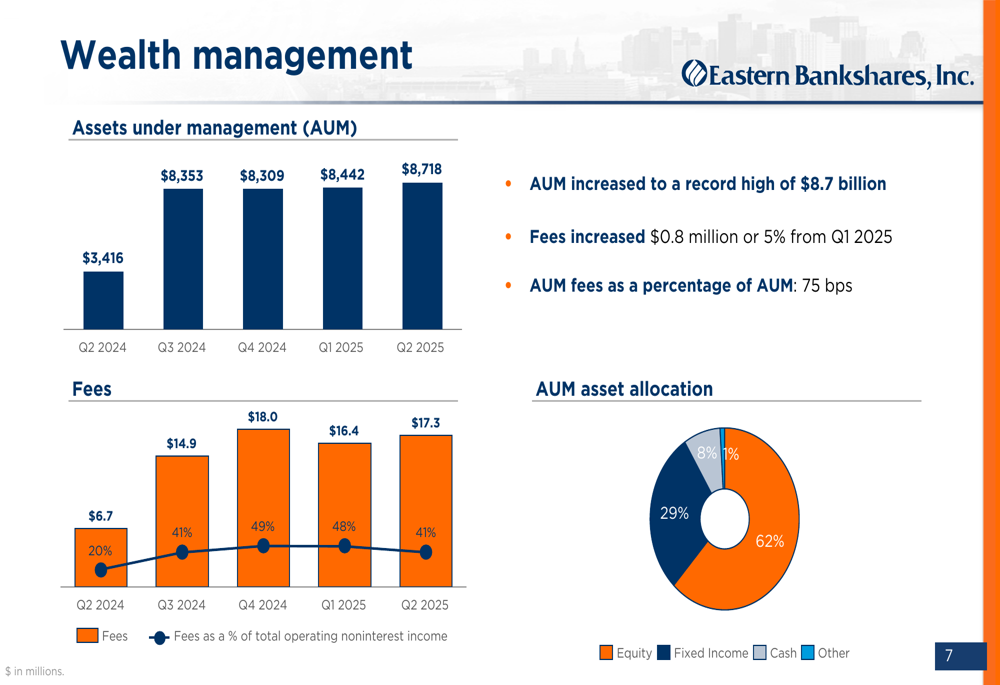

Noninterest income was $42.9 million for the quarter, with wealth management being a particular bright spot. The bank’s wealth management assets under management reached a record high of $8.7 billion, generating $17.3 million in investment advisory fees, up from $16.4 million in the previous quarter.

The following chart shows the growth in wealth management assets and fees:

Strategic Initiatives and Outlook

Eastern Bankshares updated its outlook for 2025, adjusting several key metrics. The bank now expects loan growth of 3-5% (up from 2-4%), while slightly reducing its deposit growth forecast to 0-1% (from 1-2%). Net interest income is projected at $810-820 million, slightly below the previous guidance of $815-840 million.

The bank maintained its net interest margin forecast at 3.45-3.55%, while improving its noninterest income outlook to $145-150 million (from $130-140 million) and reducing its noninterest expense projection to $530-540 million (from $535-555 million).

These adjustments suggest management’s confidence in continued loan growth and expense control, while acknowledging some pressure on deposit growth and net interest income in the current environment.

Capital and Asset Quality

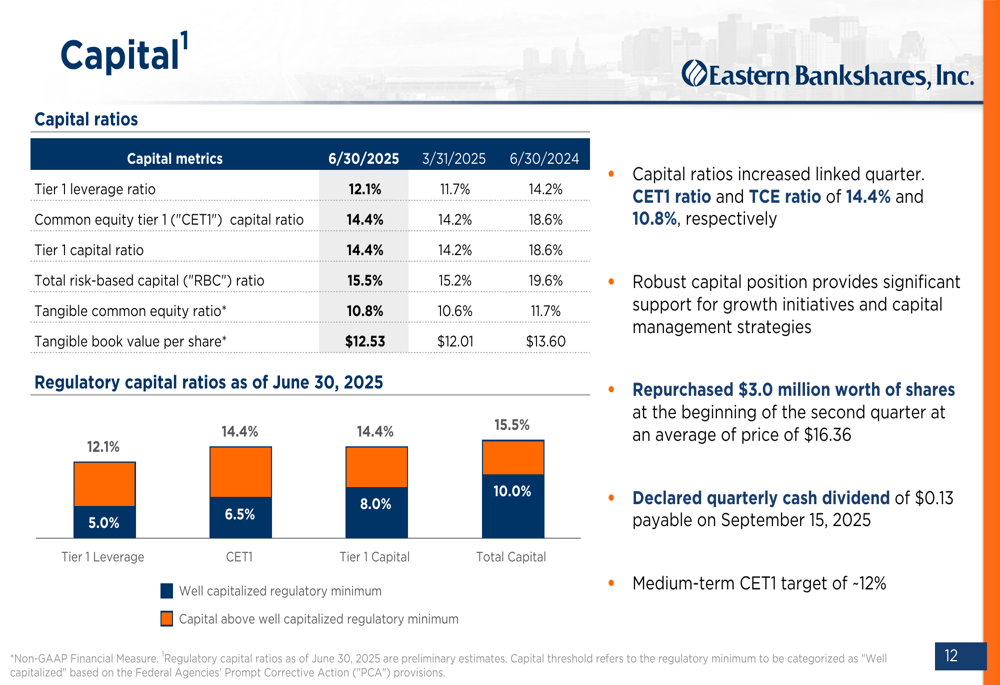

Eastern Bankshares maintained strong capital ratios, with a Common Equity Tier 1 ratio of 14.4% and a tangible common equity ratio of 10.8%. The bank’s tangible book value per share increased to $12.53, up $0.52 or 4% from the previous quarter.

The following chart illustrates the bank’s robust capital position:

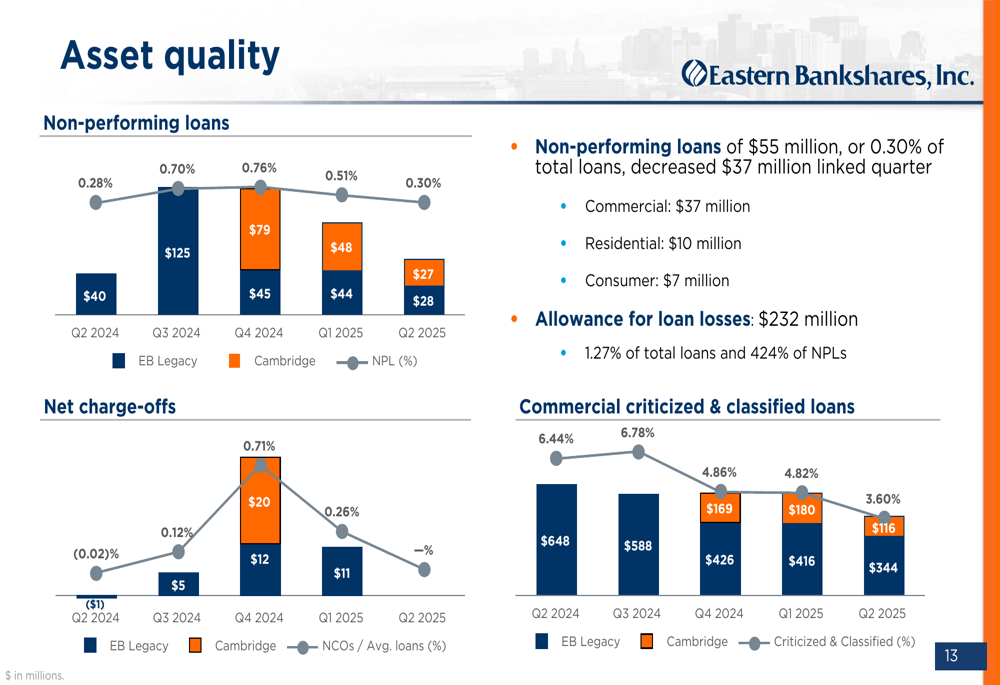

Asset quality remained excellent, with non-performing loans representing just 0.30% of total loans, down from previous quarters. The bank reported no net charge-offs for the quarter, reflecting strong credit quality across its loan portfolio.

The following chart shows the trend in non-performing loans:

Commercial real estate (CRE) exposure, a closely watched area for banks in the current environment, totaled $7.3 billion. The bank’s CRE investor office exposure was $828 million, with a diversified portfolio across property types and locations. The bank appears well-positioned to manage potential risks in this segment, with adequate reserves of $40 million against this exposure.

Forward-Looking Statements

Eastern Bankshares continues to make progress on its planned merger with Harbor One, which is expected to close between late Q4 2025 and Q1 2026. The merger is projected to create a $31 billion bank with enhanced scale and efficiency.

The bank’s Q2 2025 results demonstrate continued momentum in improving profitability metrics while maintaining strong asset quality. With its updated outlook for 2025, Eastern Bankshares appears well-positioned to navigate the current economic environment while preparing for its strategic merger with Harbor One.

Investors will likely focus on the bank’s ability to maintain its improved profitability metrics and successfully execute the Harbor One merger in the coming quarters, as these factors will be critical to the stock’s performance in the remainder of 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.