Walmart halts H-1B visa offers amid Trump’s $100,000 fee increase - Bloomberg

Introduction & Market Context

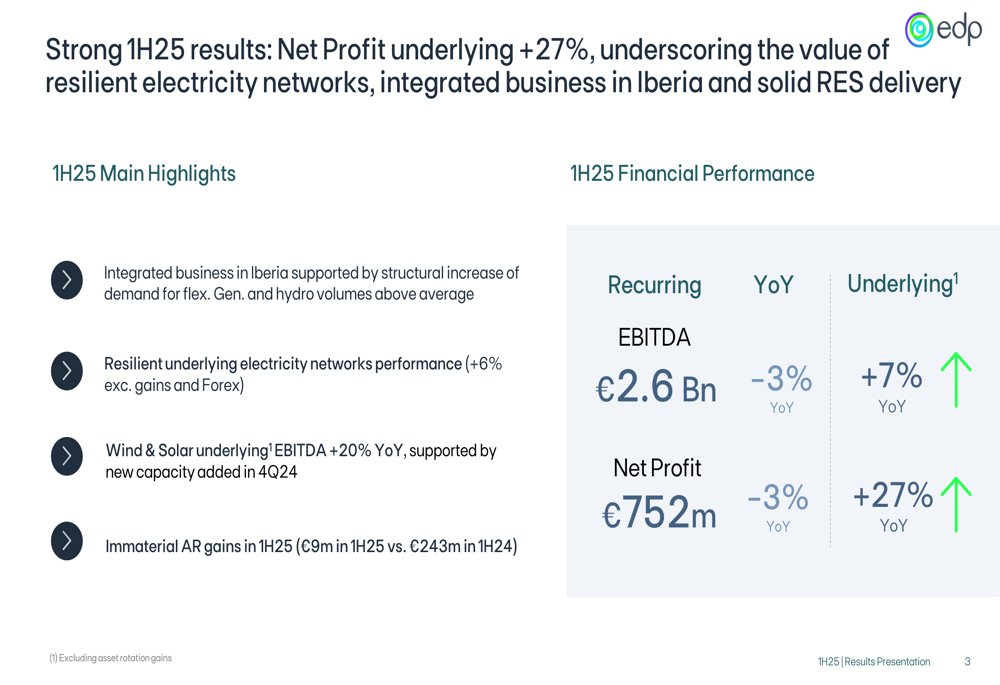

EDP Energias de Portugal SA (LISBON:EDP) presented its first-half 2025 results on July 31, highlighting strong underlying performance despite lower headline figures. The company’s results reflect the growing importance of renewable energy and flexible generation in its portfolio, alongside positive regulatory developments in key markets.

Trading at €3.70, EDP has demonstrated resilience in a challenging market environment, supported by its diversified business model across renewables, networks, and conventional generation. The company’s strategic focus on operational efficiency and capacity expansion continues to drive long-term growth.

Executive Summary

EDP reported recurring EBITDA of €2.6 billion for the first half of 2025, representing a 3% year-on-year decline. However, underlying EBITDA increased by 7% compared to the same period last year, demonstrating the company’s operational strength when excluding non-recurring items. Similarly, while reported net profit decreased by 3% to €752 million, underlying net profit surged by 27% year-on-year.

As shown in the following key highlights from the presentation:

This performance divergence is largely explained by significantly lower asset rotation gains in the first half of 2025 (€9 million compared to €243 million in 1H24), as the company’s asset rotation strategy execution is more heavily weighted toward the second half of the year.

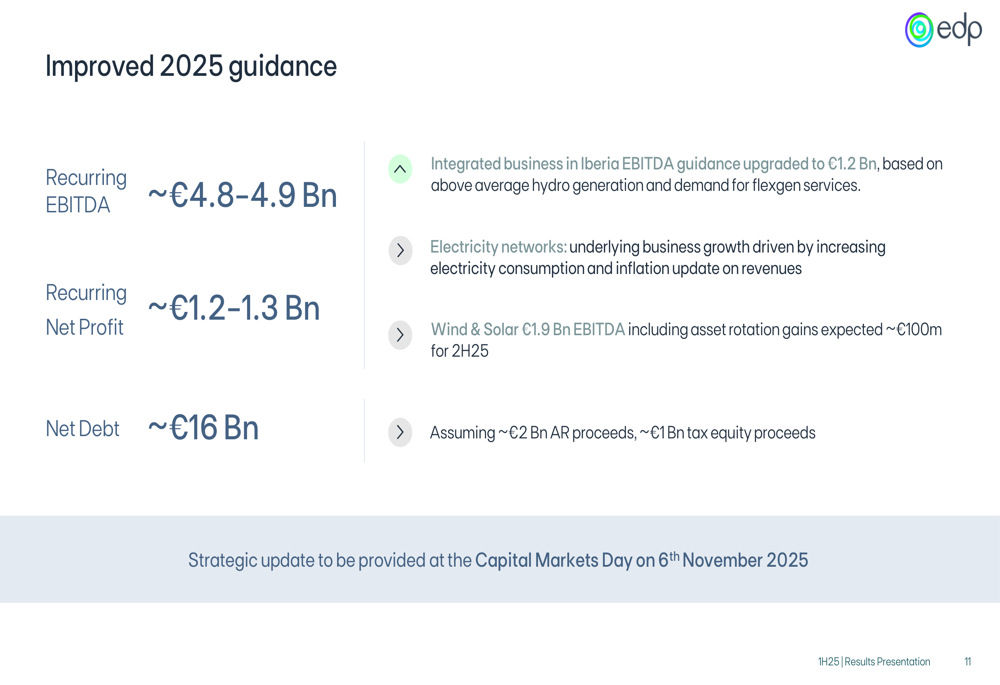

Based on these results, EDP has upgraded its full-year 2025 guidance, now projecting recurring EBITDA of approximately €4.8-4.9 billion and recurring net profit of €1.2-1.3 billion.

Detailed Financial Analysis

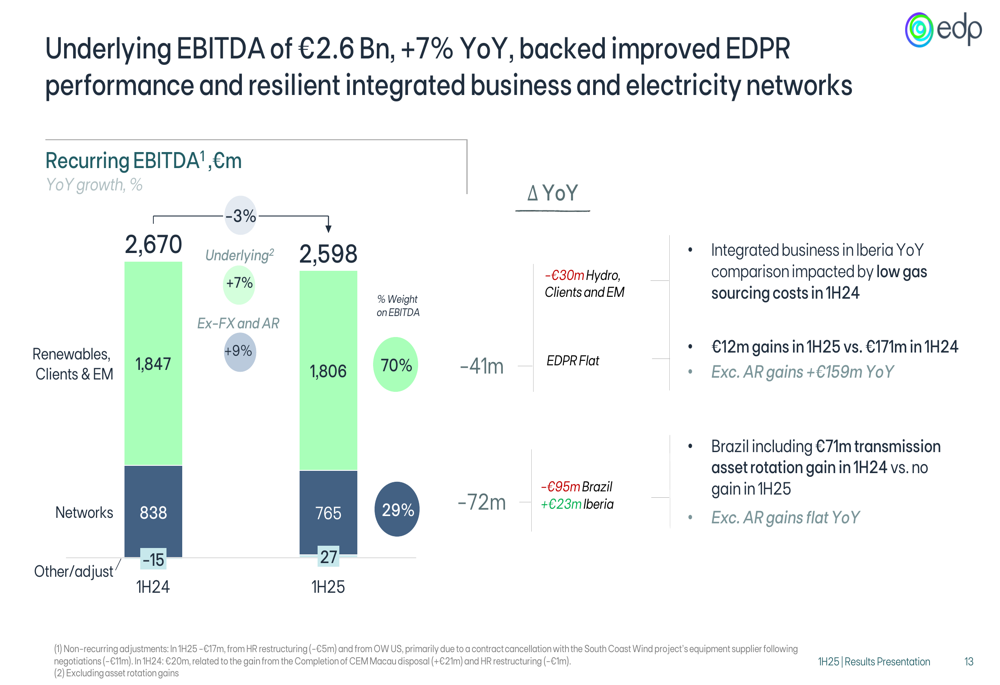

EDP’s underlying EBITDA growth of 7% was primarily driven by improved performance in its Wind & Solar segment, which saw a 20% increase in EBITDA year-on-year. This growth was supported by an 18% expansion in installed capacity to 19.6 GW and a 12% increase in electricity generation to 21.2 TWh, despite a slight 1% negative deviation from expected long-term gross capacity factor.

The following chart illustrates the components of EDP’s underlying EBITDA performance:

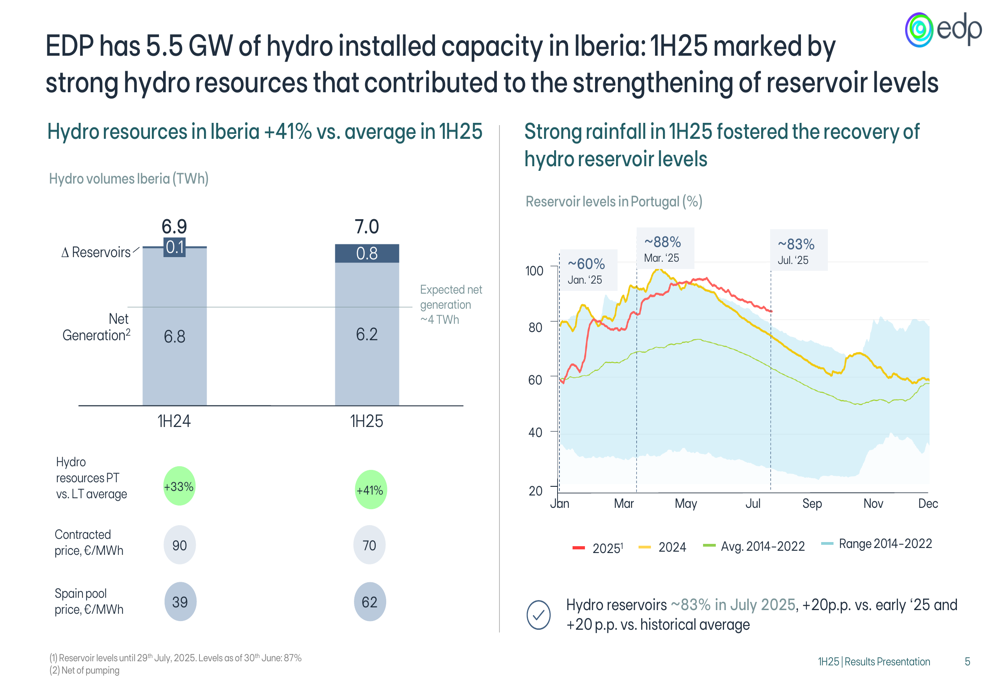

In the integrated generation and supply business in Iberia, EDP benefited from exceptional hydro resources, which were 41% above the long-term average in 1H25. This contributed to hydro reservoirs reaching approximately 83% capacity in July 2025, 20 percentage points above early 2025 levels and the historical average. The company’s hydro performance is illustrated in the following slide:

The electricity networks segment showed resilience with underlying EBITDA growing 6% year-on-year when excluding foreign exchange impacts and asset rotation gains. This growth reflects inflation updates, RAB growth in Iberia, and consumption growth in Brazil, where electricity distributed increased from 29.8 TWh to 30.7 TWh.

On the financial side, net financial costs increased by 6% to €470 million, primarily due to higher average debt, higher interest rates for Brazilian real-denominated debt, and lower capitalizations. Net debt rose to €17.2 billion in 1H25 from €15.6 billion at the end of 2024, reflecting annual dividend payments in Q2 and ongoing investment execution.

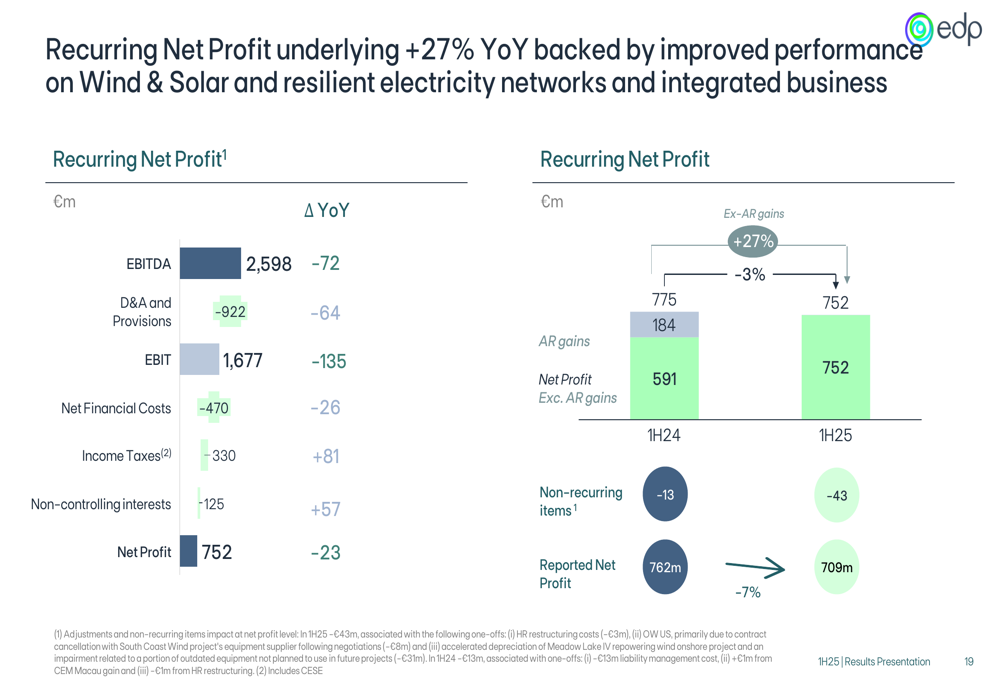

The components of EDP’s recurring net profit are detailed in the following chart:

Strategic Initiatives & Regulatory Developments

EDP continues to focus on operational efficiency, reducing its workforce by 8% from 13.3k to 12.3k employees between 1H23 and 1H25. This has contributed to a decline in recurring OPEX from €0.97 billion to €0.93 billion over the same period, with OPEX to gross profit ratio improving from 26% to 24%.

In terms of capacity expansion, EDP is on track to add approximately 2 GW of new renewable capacity in 2025, with 70% planned for the fourth quarter. The company also has high visibility for 2026, with up to 1.5 GW of capacity additions, approximately 65% of which is already secured.

Regulatory developments have been largely positive across EDP’s key markets. In Brazil, the company secured a 30-year concession extension for EDP ES (until July 2055), with a tariff review scheduled for August 2025. The regulatory return is expected to increase by 0.88 percentage points to 8.03%.

In Iberia, Spain is launching a public consultation proposing a 6.46% return for electricity networks and a shift of net RAB to the TOTEX model. Portugal is also expected to increase returns to support asset modernization. These regulatory changes are crucial as EDP sees increasing electricity demand, with e-mobility-related supply points growing 126% compared to 1H23.

Forward-Looking Statements

Based on its strong first-half performance, EDP has improved its 2025 guidance as shown in the following slide:

The company now expects recurring EBITDA of approximately €4.8-4.9 billion, recurring net profit of €1.2-1.3 billion, and net debt of around €16 billion by year-end. This improved outlook is supported by the strong performance of the integrated business in Iberia, resilient electricity networks, and continued growth in the wind and solar segment.

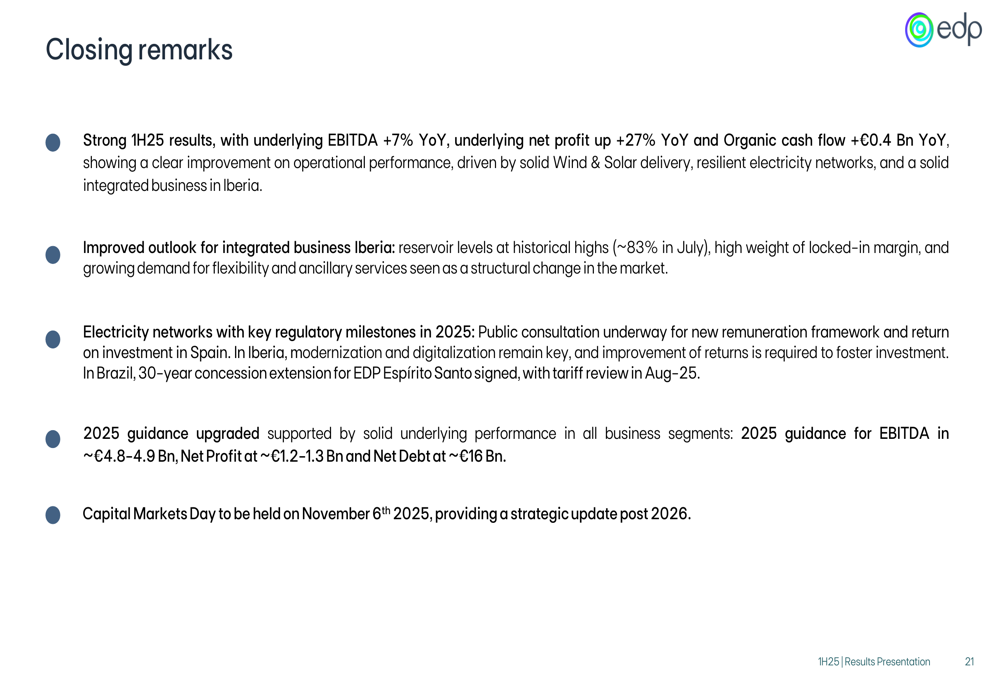

EDP’s closing remarks summarize the key achievements and outlook:

The company plans to provide a comprehensive strategic update at its Capital Markets Day scheduled for November 6, 2025, which will likely outline longer-term growth targets and capital allocation priorities.

While EDP faces challenges including higher financial costs and increased debt levels, its diversified business model, growing renewable portfolio, and favorable regulatory developments position it well for sustainable growth. The company’s focus on operational efficiency and strategic capacity expansion should continue to support its transition toward a cleaner energy mix while delivering value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.