Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Finnish telecommunications company Elisa Oyj (HEL:ELISA) released its Q2 2025 interim report on July 15, 2025, showing modest growth despite challenging market conditions. The company reported a 2.0% year-over-year revenue increase and 4.3% growth in comparable EBITDA. Despite these positive operational metrics, Elisa’s stock fell 3.13% following the announcement, trading at €45.22 as investors reacted to the results.

The telecom provider continues to execute its strategy focused on 5G expansion, fiber rollout, and growth in digital services, while maintaining its full-year guidance for 2025.

Quarterly Performance Highlights

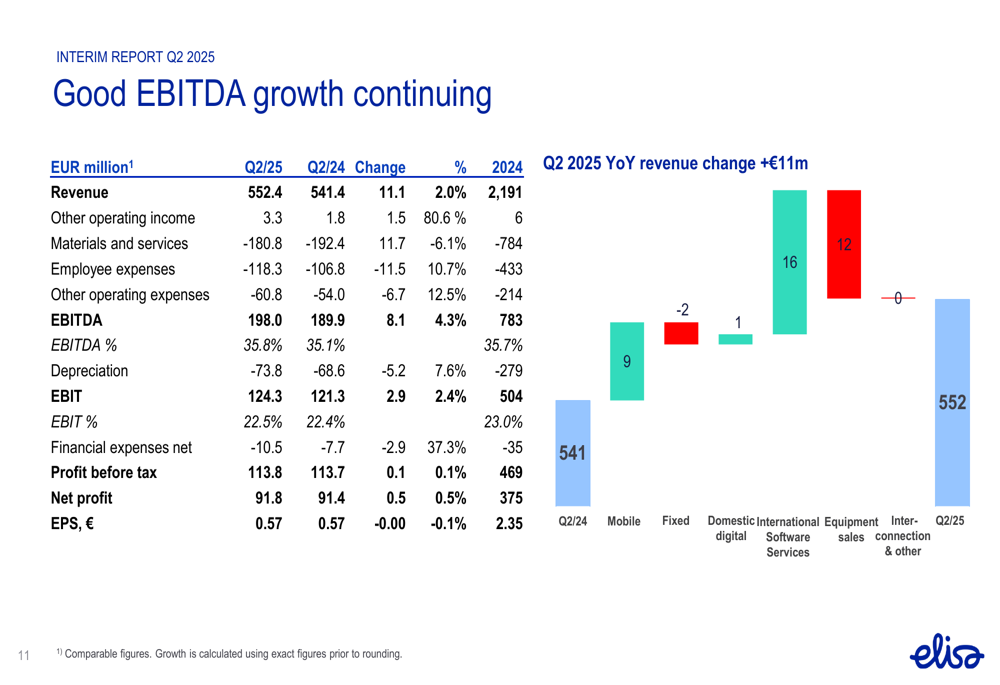

Elisa reported revenue of €552.4 million for Q2 2025, representing a 2.0% increase compared to the same period last year. This growth was primarily driven by international software services, which surged 70.7% (9.6% comparable growth), and mobile service revenue, which increased by 3.4%. However, equipment sales decreased by €12 million year-over-year, partially offsetting these gains.

The company’s comparable EBITDA rose 4.3% to €198.0 million, resulting in an EBITDA margin of 35.8%. Net profit reached €91.8 million with earnings per share of €0.57.

As shown in the following financial overview:

Operational metrics also showed improvement, with post-paid churn decreasing to 17.1% from 18.6% in Q1 2025. The company added 42,800 post-paid subscriptions, of which 14,100 were M2M and IoT subscriptions. The fixed broadband subscription base increased by 4,400.

Segment Performance

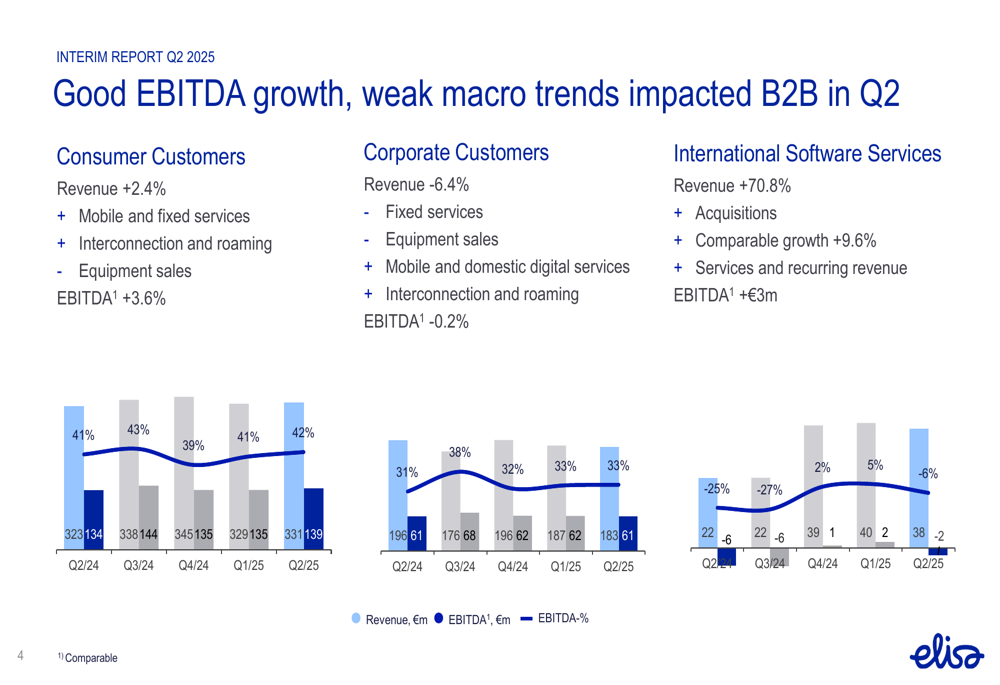

Elisa’s performance varied significantly across its three main business segments. The Consumer Customers segment showed solid growth with revenue increasing by 2.4% and EBITDA rising by 3.6% to €139 million. This segment maintained a strong EBITDA margin of 42%.

In contrast, the Corporate Customers segment faced challenges, with revenue declining by 6.4% due to decreases in fixed services and equipment sales. Despite this, the segment managed to limit EBITDA decline to just 0.2%, maintaining an EBITDA margin of 33%.

The International Software (ETR:SOWGn) Services segment demonstrated exceptional growth, with revenue increasing by 70.8%, largely driven by acquisitions. Comparable organic growth was 9.6%. However, this segment still recorded a negative EBITDA of €2 million, though this represents an improvement of €3 million compared to the previous year.

The following chart illustrates the performance across these segments:

Elisa’s Estonian operations showed improved profitability despite a revenue decline. Revenue decreased by 10% to €54.2 million, though excluding a one-time deal from the previous year, revenue actually increased by 2%. EBITDA in Estonia grew by 4% to €18.1 million, resulting in an improved EBITDA margin of 33.4%.

Strategic Initiatives

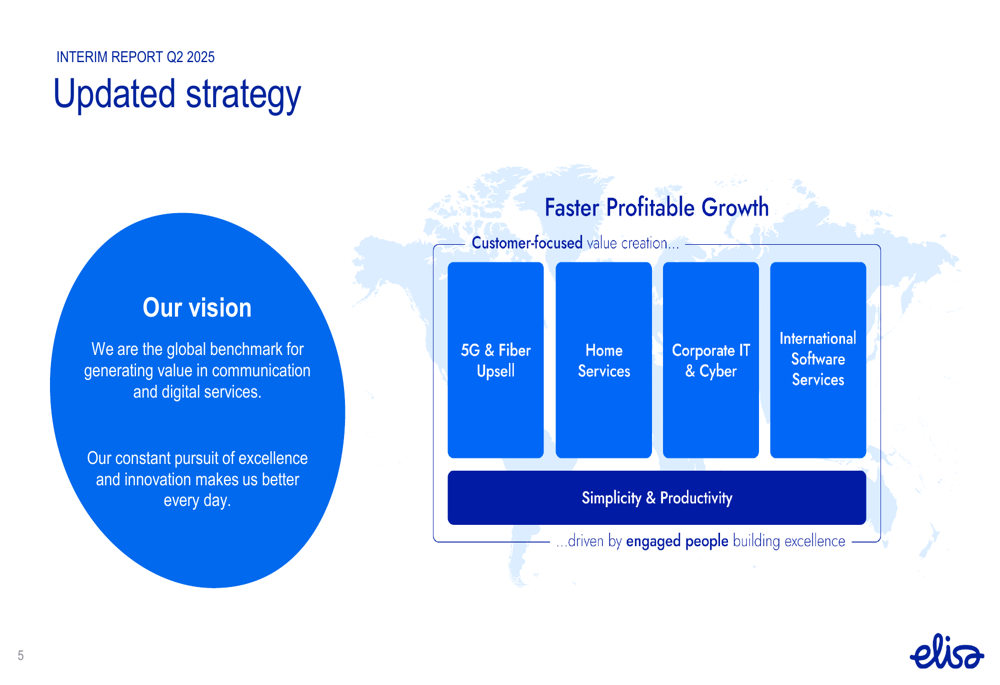

Elisa continues to execute its updated strategy centered around faster profitable growth through customer-focused value creation. The company’s strategic focus areas include 5G & Fiber Upsell, Home Services, Corporate IT & Cyber, and International Software Services.

The strategy is visually represented in this slide:

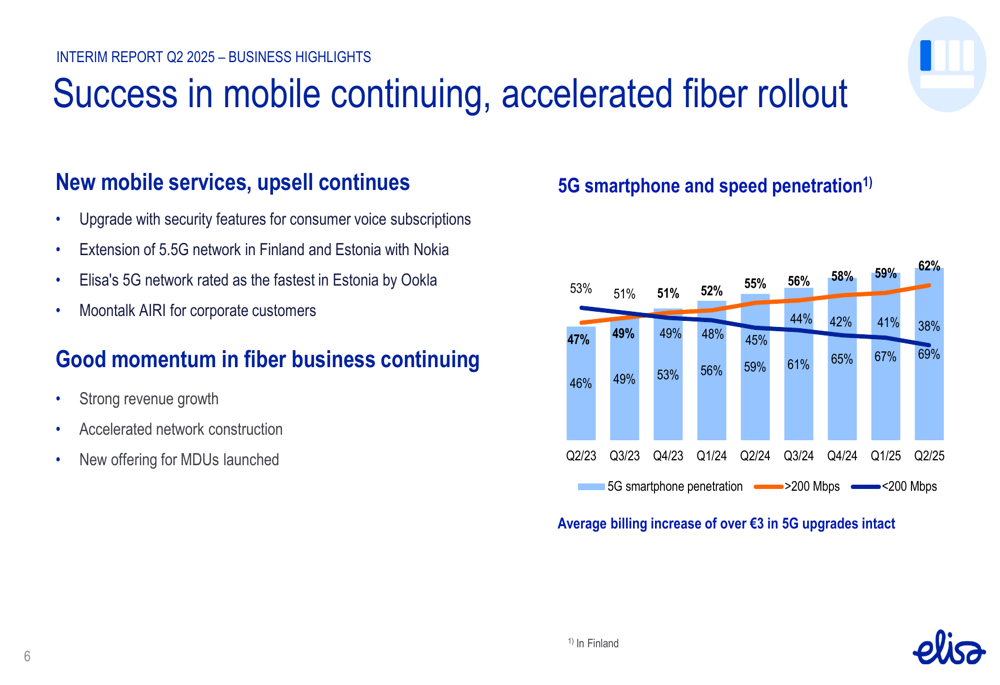

In mobile services, Elisa reported continued success with its 5G rollout and upselling efforts. The company extended its 5.5G network in Finland and Estonia with Nokia (HE:NOKIA), and Elisa’s 5G network was rated as the fastest in Estonia by Ookla. The company maintained its average billing increase of over €3 in 5G upgrades, with 5G smartphone penetration reaching 58% and high-speed (>200 Mbps) penetration at 62%.

The following chart shows the progression of 5G adoption:

Elisa also highlighted strong momentum in its fiber business, with accelerated network construction and a new offering for multi-dwelling units (MDUs). In digital services, the company launched a new season of its original series "The Man Who Died" on Elisa Viihde and introduced Elisa Kotiturva home security service.

The company’s sustainability efforts have gained recognition, with Elisa being named one of the world’s most sustainable companies by TIME (ranked 55th) and one of the 500 best employers in Europe by the Financial Times and Statista.

Financial Position

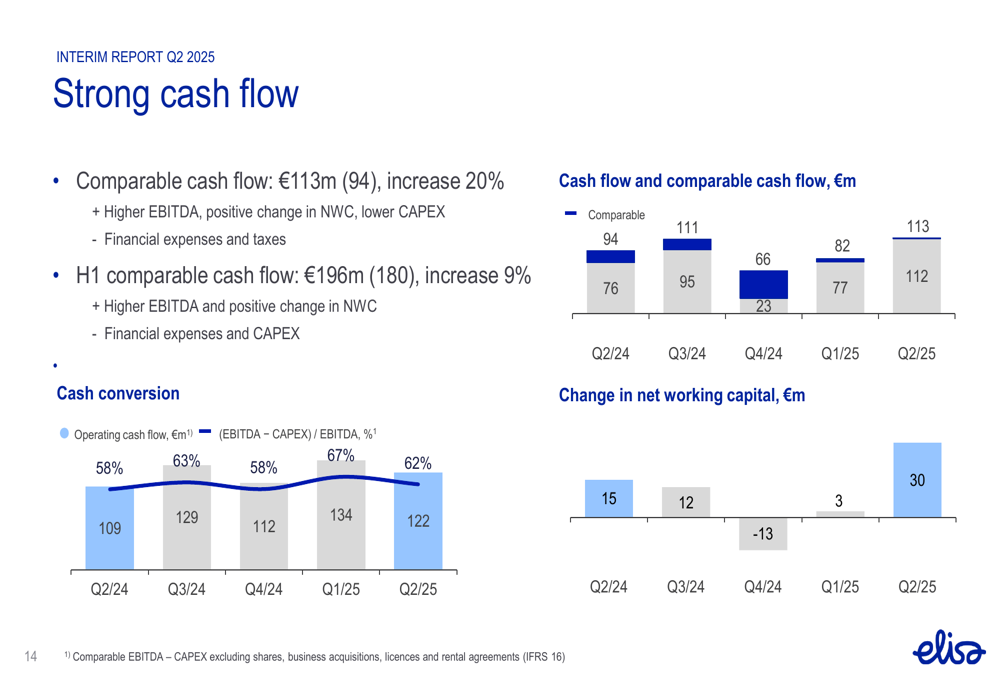

Elisa demonstrated strong cash flow performance in Q2 2025, with comparable cash flow increasing by 20% year-over-year to €113 million. For the first half of 2025, comparable cash flow grew by 9% to €196 million.

The following chart illustrates the company’s cash flow development:

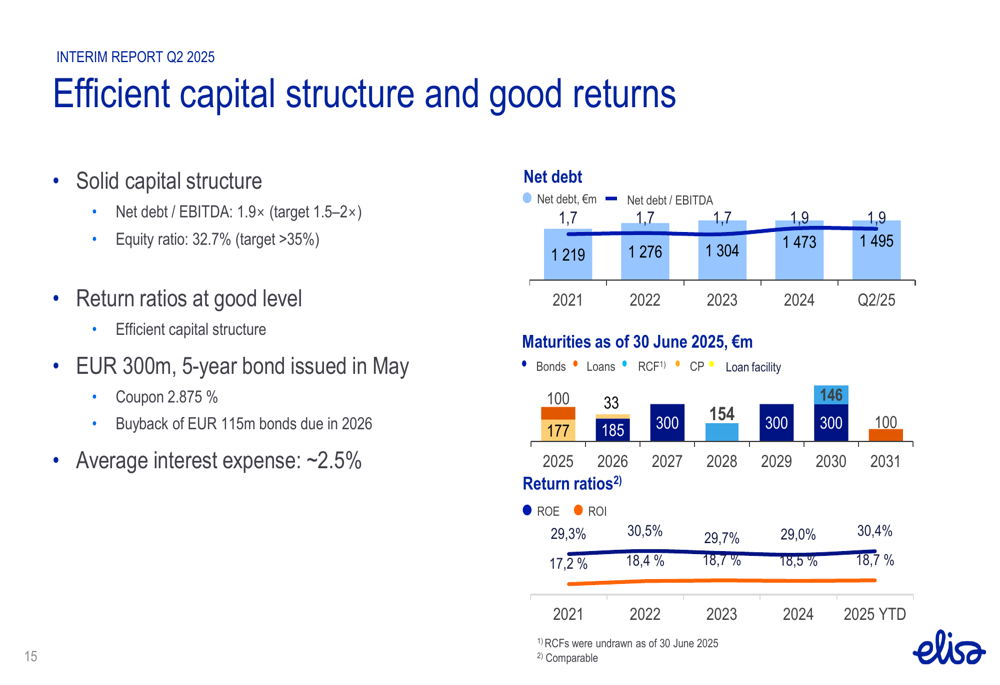

The company maintains a solid capital structure with a net debt to EBITDA ratio of 1.9×, within its target range of 1.5-2×. The equity ratio stands at 32.7%, slightly below the target of >35%. In May, Elisa issued a €300 million 5-year bond with a 2.875% coupon and bought back €115 million of bonds due in 2026. The average interest expense is approximately 2.5%.

Elisa’s debt maturity profile as of June 30, 2025, is well-distributed:

Capital expenditure (CAPEX) for Q2 2025 was €76 million, representing 14% of sales, with the full-year CAPEX guidance maintained at a maximum of 12% of revenue. The main CAPEX areas include 5G coverage expansion, fiber and other network investments, and IT infrastructure.

Outlook & Guidance

Elisa maintained its guidance for 2025, expecting revenue to be at the same level as or slightly higher than in 2024. Similarly, comparable EBITDA is projected to be at the same level or slightly higher than the previous year. The company reiterated its CAPEX guidance at a maximum of 12% of revenue.

The outlook acknowledges uncertainties in the general economy, particularly concerning the Finnish economy and global supply chains due to the Russia-Ukraine war. Competition in the telecommunications market remains intense.

In conclusion, Elisa’s Q2 2025 results demonstrate the company’s ability to generate modest growth and improve profitability in a challenging market environment. While the Consumer segment and International Software Services show promising momentum, the Corporate segment faces headwinds. The market reaction suggests investors may have expected stronger results or were concerned about the competitive landscape and economic uncertainties mentioned in the outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.