Pilgrim Global buys Sable Offshore (SOC) shares worth $14.7m

Introduction & Market Context

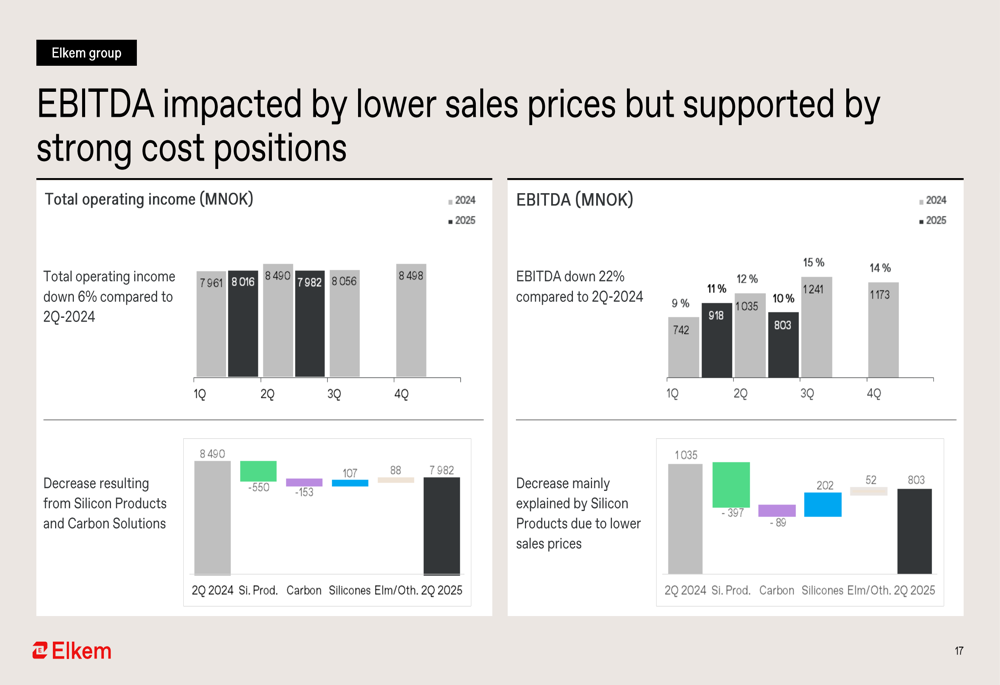

Elkem ASA (OB:ELK) released its second quarter 2025 results on July 11, revealing continued pressure from weak market conditions across its business segments. The Norwegian silicon, silicones and carbon solutions provider reported a total operating income of NOK 7,982 million and an EBITDA of NOK 803 million, resulting in an EBITDA margin of 10% - below the company’s long-term target of 15-20%.

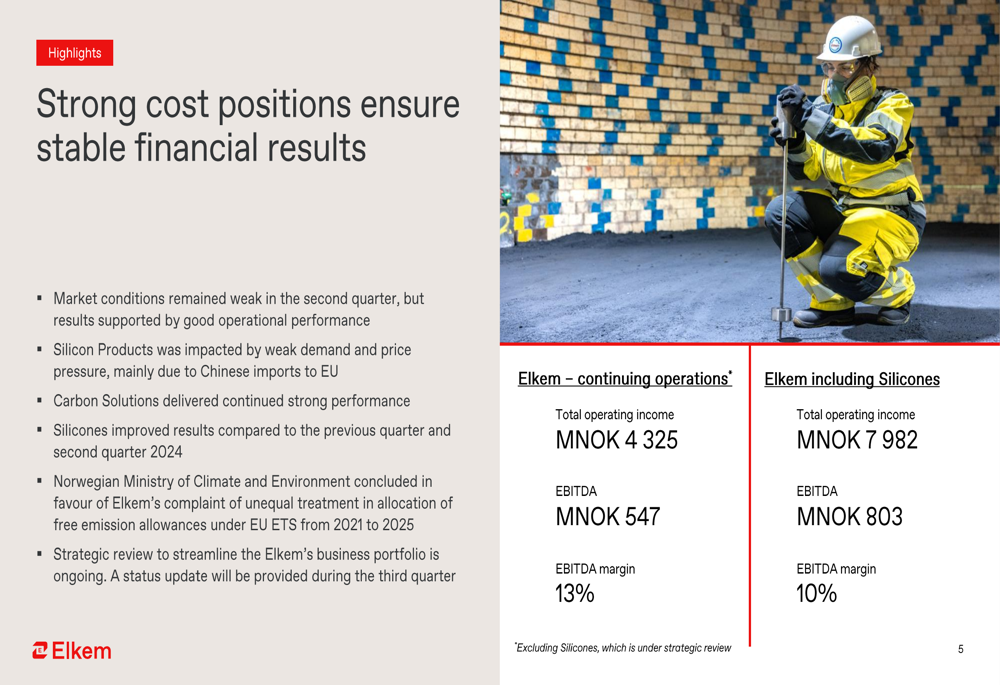

CEO Helge Aasen emphasized the company’s resilience despite challenging conditions: "Elkem continues to face weak market conditions. However, our strong cost position and solid operational performance ensures stable financial results."

The company’s stock closed at NOK 27.24 on October 14, 2025, down 0.8% for the session, reflecting ongoing investor concerns about market conditions despite management’s confidence in the company’s strategic positioning.

Quarterly Performance Highlights

Elkem’s financial performance showed significant pressure compared to the previous year, with EBITDA declining from NOK 1,035 million in Q2 2024 to NOK 803 million in Q2 2025. This decrease primarily stemmed from challenges in the Silicon Products division (-550 MNOK) and Carbon Solutions (-153 MNOK).

As shown in the following chart detailing EBITDA impacts:

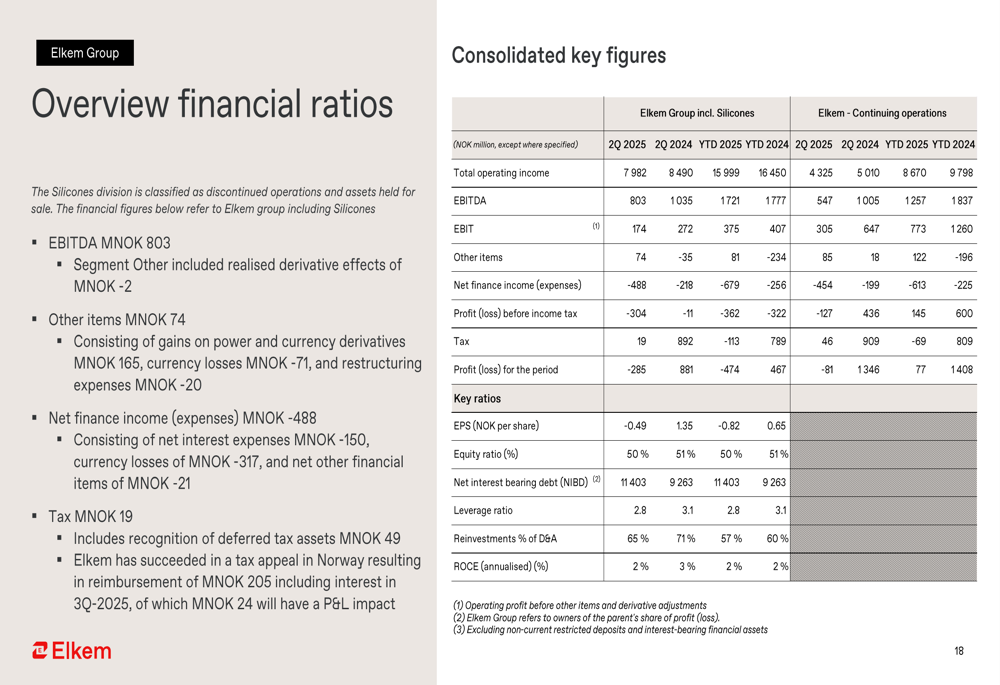

The company reported a negative earnings per share (EPS) of NOK 0.49 for the quarter, while maintaining an equity ratio of approximately 41%. Net interest-bearing debt stood at NOK 11.4 billion as of June 30, 2025, resulting in a leverage ratio of 2.8x - exceeding the company’s target range of 1-2x.

Cash flow from operations was NOK 308 million in Q2 2025, with investments excluding M&A totaling NOK 464 million. The following financial ratios provide a comprehensive overview of Elkem’s performance:

Segment Performance Analysis

Elkem’s three business segments showed varying performance during the quarter:

1. Silicon Products: This division continued to face significant challenges with lower sales prices being the primary factor affecting performance. Total operating income decreased to NOK 3,530 million, down from NOK 4,015 million in Q1 2024.

2. Carbon Solutions: Despite challenging market conditions, this segment delivered relatively strong performance, benefiting from good cost positions and a geographically diverse customer portfolio.

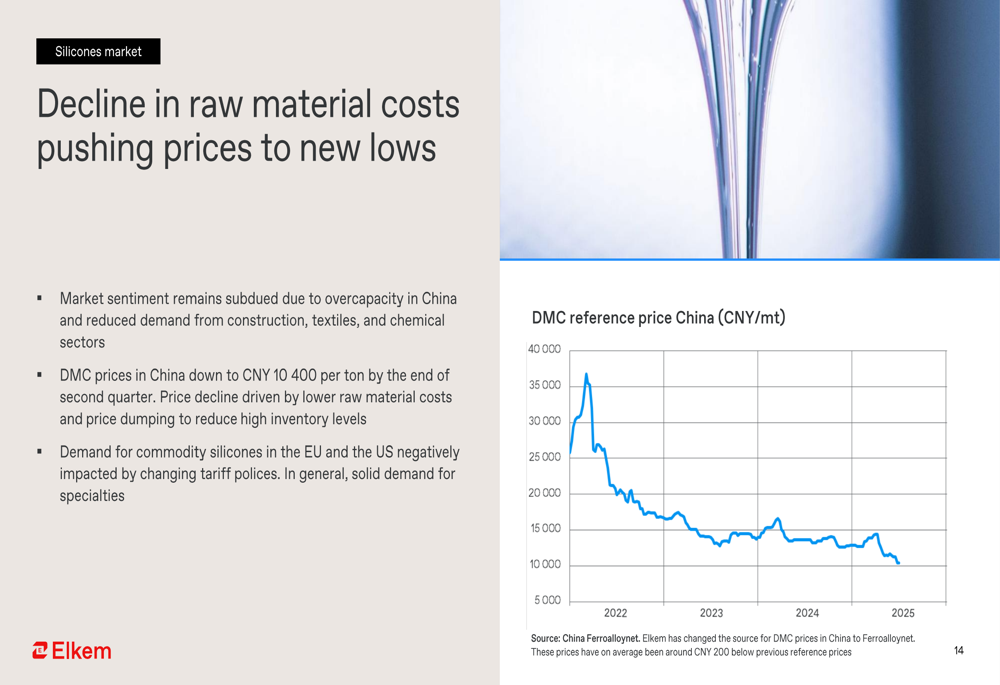

3. Silicones: This segment showed improved results with sales volume up 22% compared to Q2 2024, primarily due to higher commodity sales in the Asia Pacific region. However, market sentiment remains subdued due to overcapacity in China.

The following key highlights summarize the quarter’s performance across all segments:

Market Challenges and Positioning

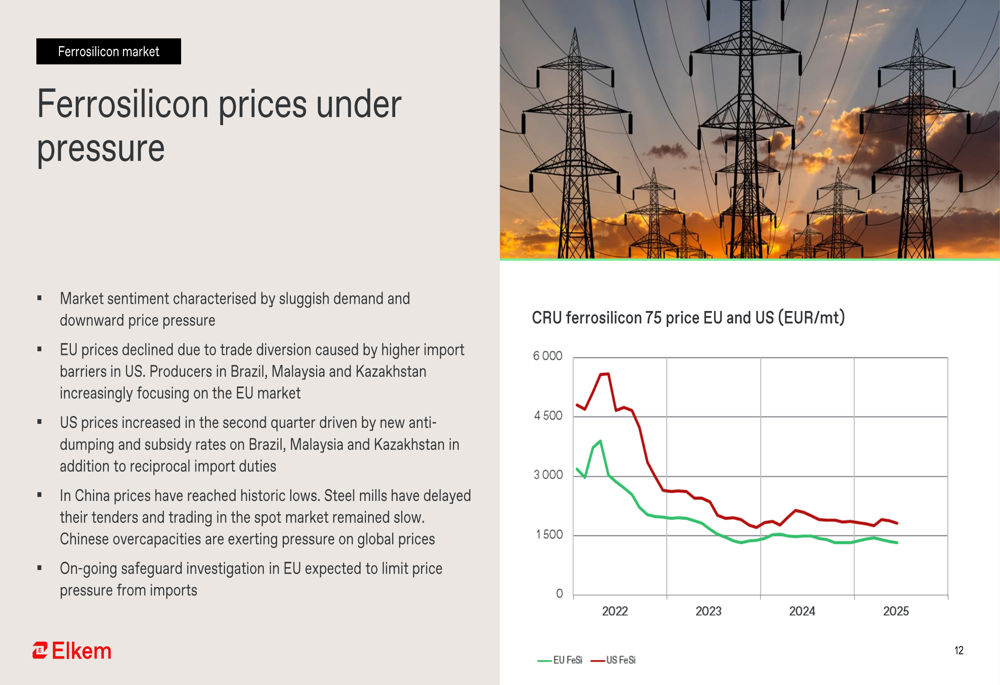

Elkem faces significant market headwinds across its product categories. In the silicon market, reference prices in the EU were reduced by approximately 20% at the end of June, while the US silicon market experienced continued downward pressure. Similarly, Chinese silicon prices continued to drop throughout the quarter.

The chart below illustrates the silicon price decline in the EU and US markets:

The ferrosilicon market showed similar weakness, characterized by sluggish demand. EU prices declined due to trade diversion, while US prices increased slightly in the second quarter. Chinese prices reached historic lows, putting additional pressure on global pricing.

In the silicones segment, market sentiment remained subdued due to overcapacity in China, with DMC prices in China falling to CNY 10,400 per ton. Demand for commodity silicones in the EU and US was negatively impacted by changing tariff policies.

The automotive sector, a key end market for Elkem, continues to show weakness, though the outlook is slightly improving. Light vehicle production remains at low levels with minor upward revisions, particularly in Europe and China.

Strategic Initiatives

Despite current market challenges, Elkem is implementing several strategic initiatives to strengthen its long-term position:

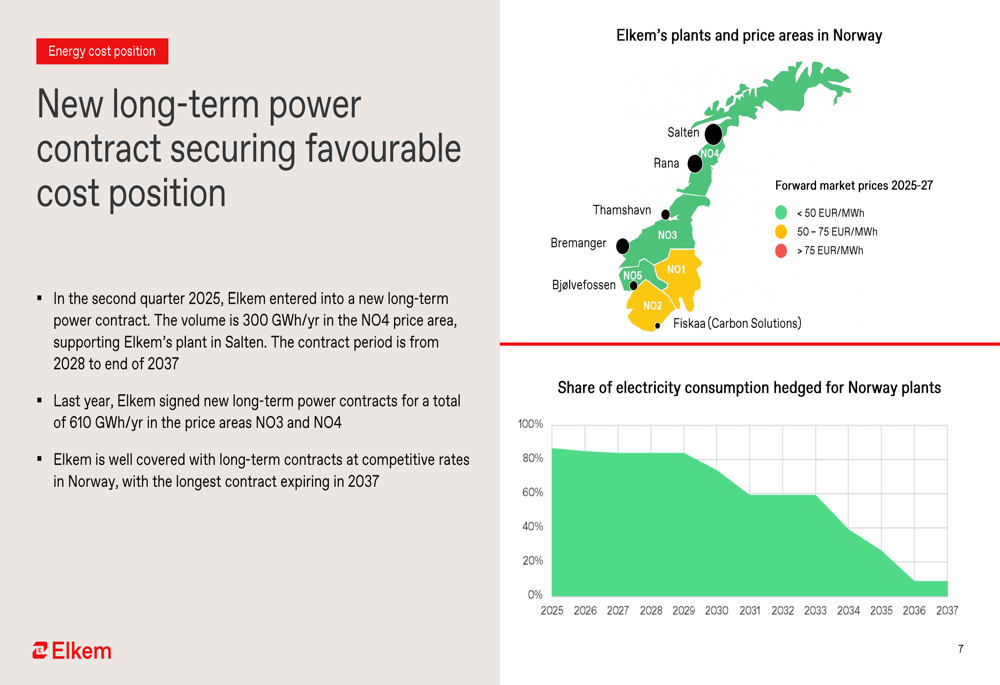

1. Energy Security: In Q2 2025, Elkem entered into a new long-term power contract of 300 GWh/yr in Norway’s NO4 price area. The contract runs from 2028 to 2037, securing favorable energy costs for the company’s Norwegian operations.

2. ESG Performance: Elkem maintains its commitment to sustainability with targets including a 25% reduction in CO2 emissions by 2030 and net-zero CO2 emissions by 2050. The company has received recognition through top ESG ratings, including EcoVadis Platinum for 2024 (top 1%) and placement in the 98th percentile by S&P Global CSA.

3. Strategic Review: The company is conducting a comprehensive review of its business portfolio, with a target to conclude before year-end. This review aims to streamline operations and potentially restructure the Silicones division.

4. Market Diversification: Elkem is pursuing opportunities in sustainable infrastructure, industrial AI applications, and defense technologies, leveraging its advanced silicon-based materials to enter growth markets.

Forward-Looking Statements

Looking ahead to Q3 2025, Elkem expects market conditions to remain subdued, though the company’s financial performance should continue to be supported by strong cost and market positions. The Silicon Products division will likely continue experiencing challenging markets, while Carbon Solutions is expected to benefit from good cost positions and a diverse customer portfolio. Silicones markets are anticipated to remain stable at low levels.

The company’s key takeaways and strategic focus areas are summarized below:

CFO Morten Wiega stated during the earnings call that "Today’s prices are not sustainable and there will be an adjustment upwards," suggesting potential relief in the medium term. Management emphasized that the ongoing safeguard investigation in the EU is expected to limit price pressure from imports, potentially providing some protection for European operations.

Elkem’s focus remains on cost improvement, maintaining high capacity utilization, and disciplined capital spending while navigating the current uncertain and volatile market environment. The conclusion of the strategic review before year-end could provide additional clarity on the company’s future direction and potential restructuring initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.