Street Calls of the Week

Introduction & Market Context

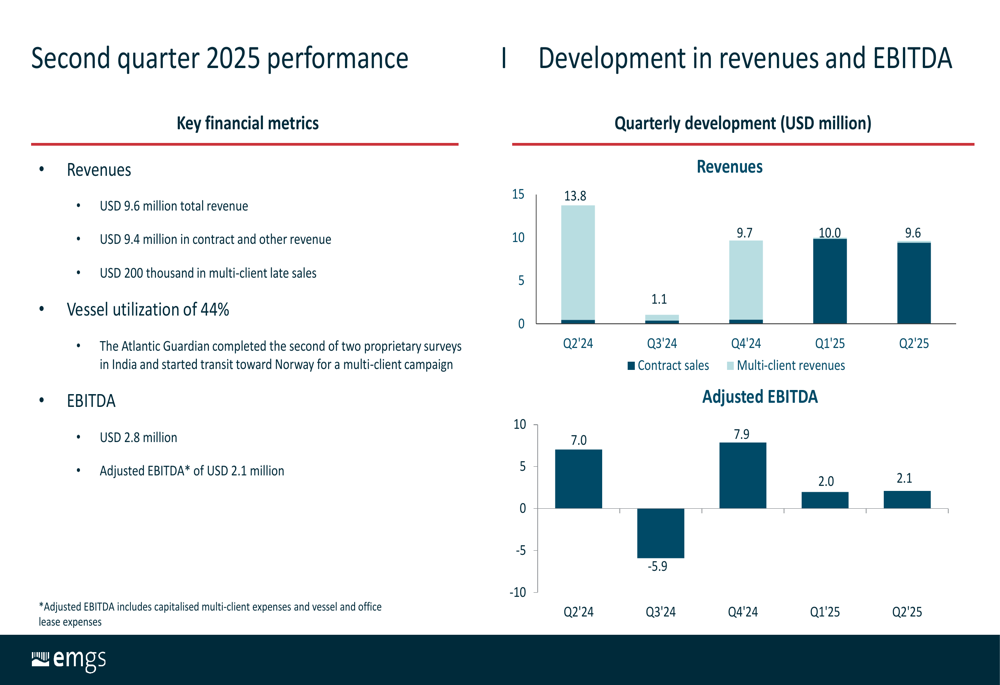

Electromagnetic Geoservices ASA (OB:EMGS) presented its second quarter 2025 results on August 13, 2025, revealing stable financial performance as the company continues to execute its strategic expansion plans. The offshore survey specialist reported revenues of USD 9.6 million, nearly matching the previous quarter’s USD 10 million, while slightly improving its adjusted EBITDA to USD 2.1 million.

EMGS shares closed at NOK 2.00 on August 12, 2025, down 1.5% for the day, and currently trade at a significant discount to their 52-week high of NOK 2.745.

Quarterly Performance Highlights

EMGS maintained relatively steady performance in Q2 2025, with total revenue of USD 9.6 million, comprising USD 9.4 million in contract revenue and USD 200,000 in multi-client late sales. The company achieved an EBITDA of USD 2.8 million and adjusted EBITDA of USD 2.1 million, showing a slight improvement from Q1’s USD 2.0 million.

Vessel utilization increased to 44% during the quarter, up from 37% in Q1, as the Atlantic Guardian completed its second proprietary survey in India before beginning transit to Norway for a multi-client campaign.

As shown in the following chart of quarterly revenue and adjusted EBITDA:

The company’s financial performance has stabilized after significant volatility in 2024, when adjusted EBITDA swung from USD 7.0 million in Q2 2024 to negative USD 5.9 million in Q3 2024, before recovering to USD 7.9 million in Q4 2024.

Detailed Financial Analysis

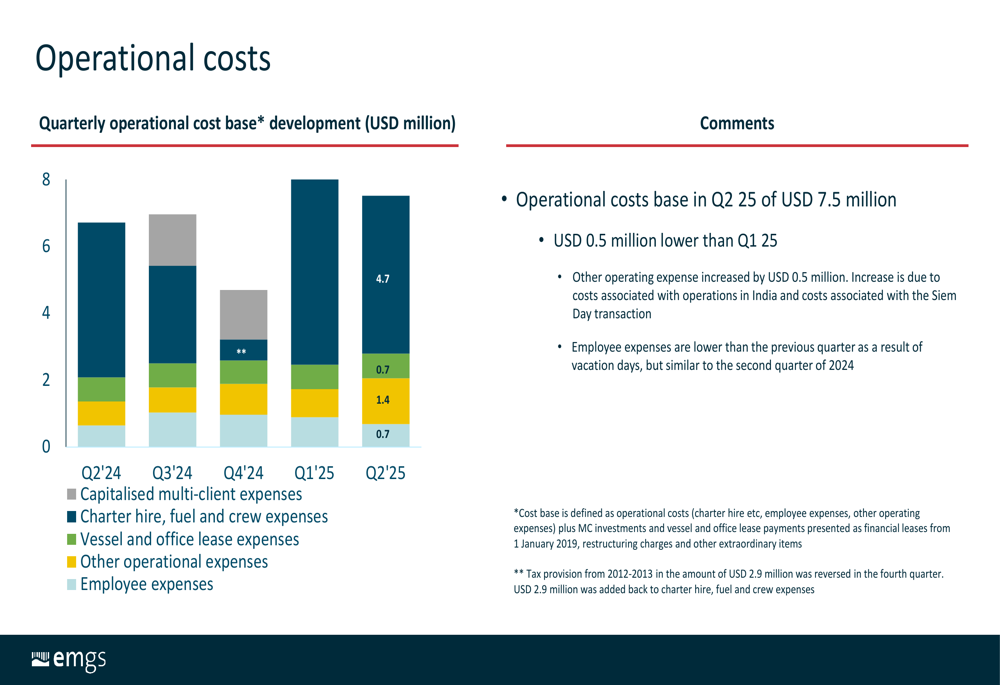

EMGS reported an operational cost base of USD 7.5 million in Q2 2025, representing a USD 0.5 million decrease from the previous quarter. The cost reduction came despite increased expenses related to operations in India and the ongoing Siem Day transaction.

The breakdown of operational costs reveals fluctuating employee expenses, which decreased compared to Q1 2025 due to vacation days but remained similar to Q2 2024 levels:

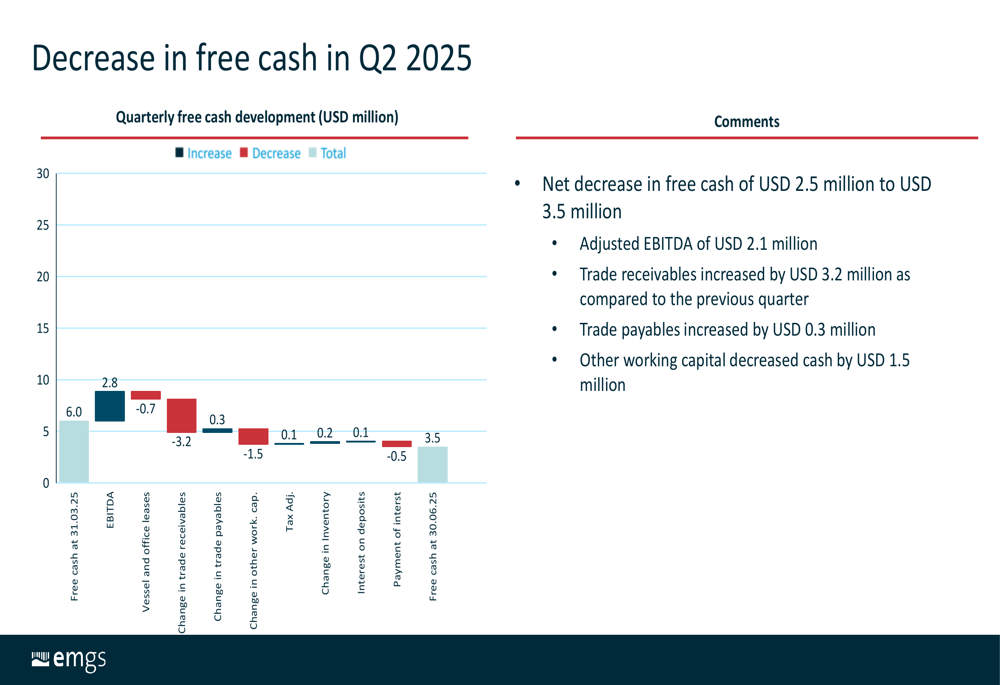

A concerning trend emerged in the company’s cash position, with free cash decreasing by USD 2.5 million to USD 3.5 million during the quarter. This decline was primarily driven by a USD 3.2 million increase in trade receivables, partially offset by positive EBITDA and other working capital changes.

The following chart illustrates the components affecting free cash flow:

On the debt front, EMGS successfully extended its USD 19.5 million convertible bond loan from a May 2025 maturity to November 2030, providing significant breathing room for its capital structure. The amended terms also include an option to issue up to USD 13.5 million in additional bonds through tap issues, enhancing the company’s financial flexibility.

Strategic Initiatives

EMGS continues to execute its international expansion strategy, highlighted by the successful completion of a 3D Controlled Source Electromagnetic (CSEM) survey for Cairn Oil & Gas in India’s Krishna-Godavari Basin. This deepwater project covered approximately 4,500 km² in water depths ranging from 500 to 2,500 meters.

The following image shows details of the completed India project:

Sam Algar of Cairn Oil & Gas praised the collaboration, noting that the acquired data "supports our exploration and development plans," while Hitesh Vaid emphasized the partnership’s role in fast-tracking deepwater block development to contribute to 50% of India’s oil and gas production.

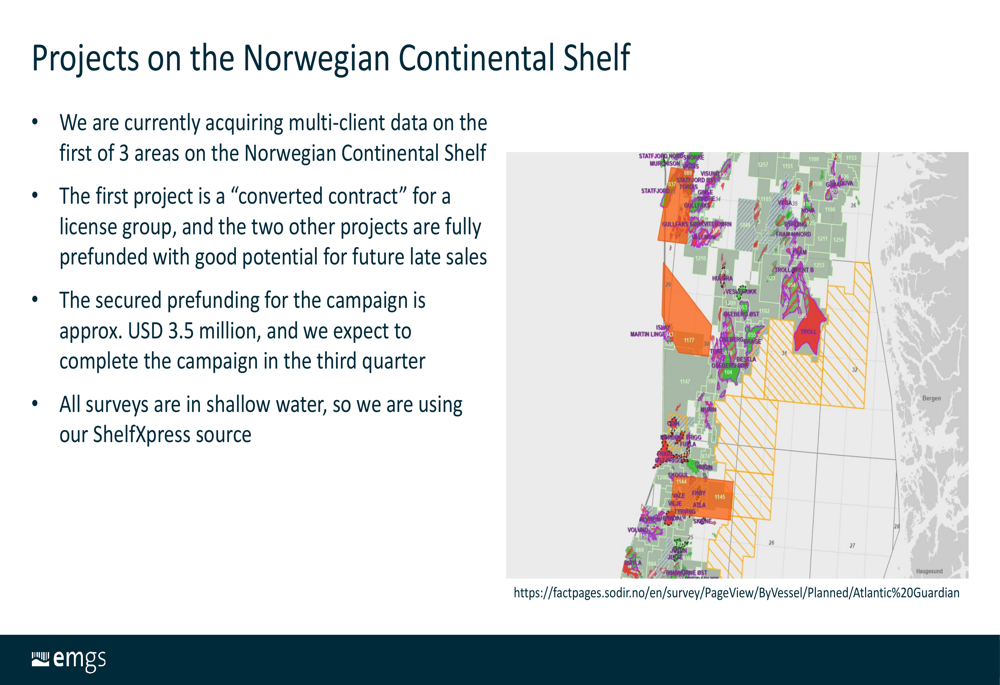

EMGS is now pivoting attention to the Norwegian Continental Shelf, where it has secured approximately USD 3.5 million in prefunding for a multi-client campaign spanning three areas. The company expects to complete this campaign in the third quarter of 2025.

The Norwegian Continental Shelf projects are illustrated in the following map:

The first project represents a "converted contract" for a license group, while the other two projects are fully prefunded with potential for future late sales. All surveys are being conducted in shallow water using the company’s ShallowXpress source.

Forward-Looking Statements

EMGS continues to work toward closing the Siem Day transaction, which was first mentioned in the company’s Q1 2025 presentation. While the Q1 report referenced a USD 109 million acquisition of a subsea construction vessel, the Q2 presentation provides limited additional details on this strategic move.

The company’s extension of its convertible bond loan maturity to 2030 suggests confidence in long-term business viability, while the option to issue additional bonds indicates potential capital needs for future growth initiatives.

With secured prefunding for Norwegian Continental Shelf projects and completed work in India, EMGS appears to be balancing its international portfolio while managing a challenging cash position. The increase in vessel utilization to 44% represents an improvement from Q1’s 37%, but still indicates significant unused capacity that could affect profitability in coming quarters.

As EMGS navigates these strategic initiatives, investors will be watching closely to see if the company can maintain its operational momentum while addressing the concerning trend in free cash reduction.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.