Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

ENAV SpA (BIT:ENAV) presented its first half 2025 results on July 31, revealing a mixed performance characterized by strong operational metrics but declining profitability. Despite reporting a 69.6% year-over-year decrease in net profit, the Italian air navigation service provider raised its full-year guidance, citing robust traffic trends and efficiency improvements. ENAV shares closed down 2.53% at €3.85 following the presentation, suggesting investors may have expected stronger results given the traffic growth.

The presentation follows a challenging first quarter when the company reported a €29.3 million loss, indicating a significant turnaround in Q2 that resulted in a positive, albeit reduced, half-year profit of €7 million.

Executive Summary

ENAV reported strong traffic growth in the first half of 2025, with en-route service units increasing by 7.3% compared to the same period last year, exceeding the company’s plan by 1.1 percentage points. Terminal traffic also showed solid growth of 4.4%. This operational strength, combined with efficiency measures, prompted management to upgrade its full-year 2025 targets across all key financial metrics.

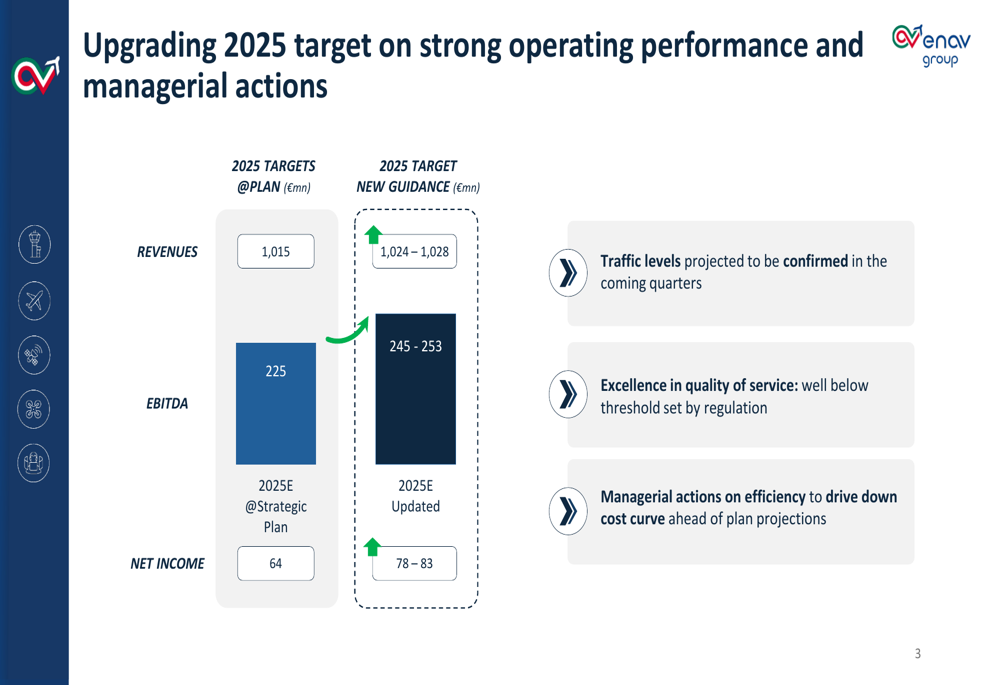

As shown in the following upgrade targets chart:

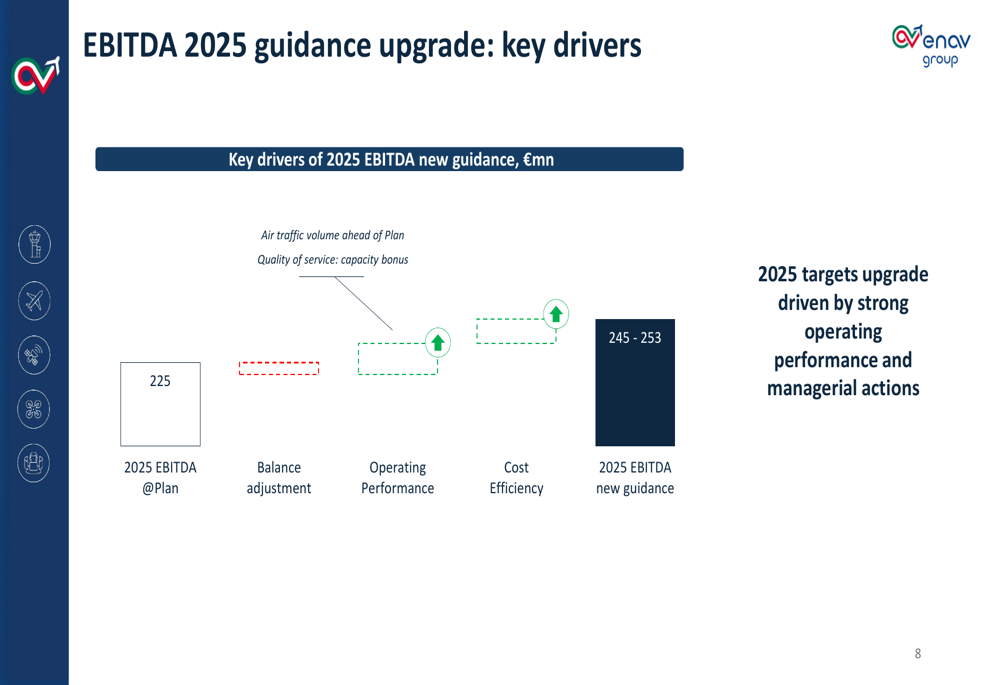

The company now expects revenues between €1,024-1,028 million (up from €1,015 million), EBITDA of €245-253 million (up from €225 million), and net income of €78-83 million (up from €64 million). These upgrades are supported by continued strong traffic levels, excellence in service quality, and efficiency measures that are driving down costs ahead of plan.

Quarterly Performance Highlights

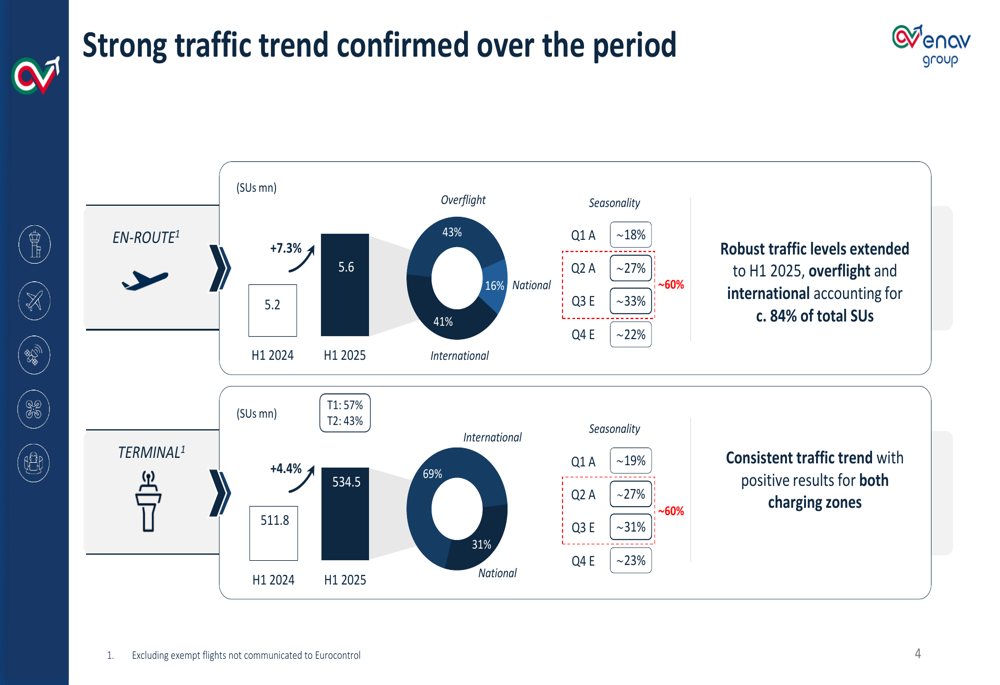

ENAV’s traffic performance remained robust throughout the first half of 2025, with both en-route and terminal segments showing significant growth. The traffic mix continues to favor international and overflight traffic, which together account for approximately 84% of total service units.

The following chart illustrates the traffic trends across both segments:

En-route traffic increased by 7.3% to 5.6 million service units, with overflight accounting for 43%, international for 41%, and national for 16% of the total. Terminal traffic grew by 4.4% to 534.5 million service units, with international flights representing 69% of the total.

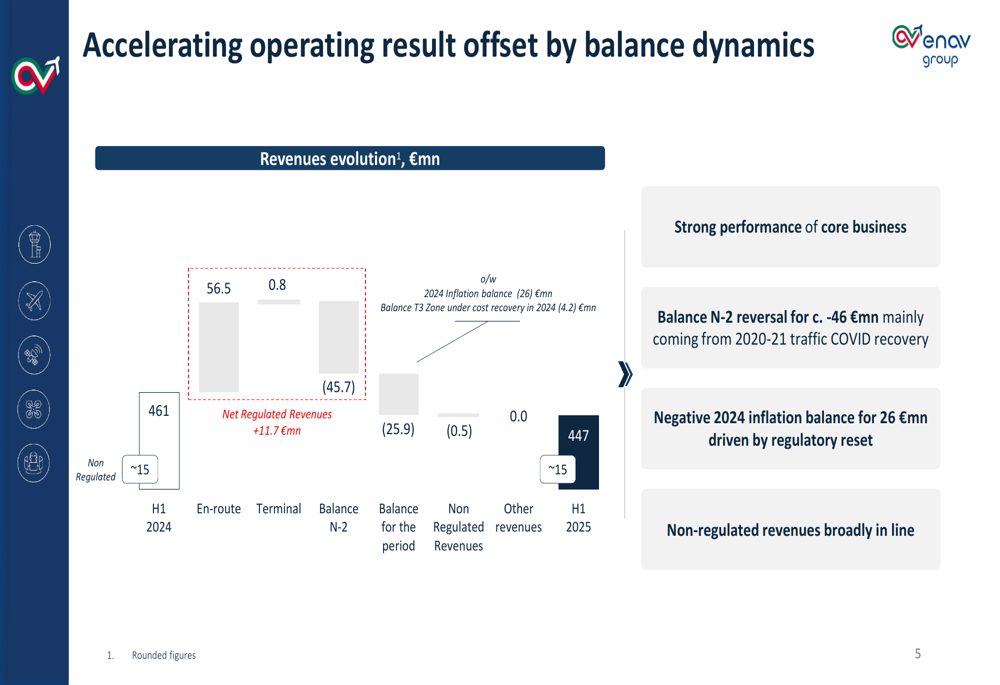

Despite this strong operational performance, ENAV’s financial results were negatively impacted by balance dynamics. Net regulated revenues increased by €11.7 million compared to H1 2024, but this was more than offset by negative balance impacts.

The following revenue evolution chart shows these dynamics:

Total (EPA:TTEF) revenues decreased from €461 million in H1 2024 to €447 million in H1 2025, primarily due to a €45.7 million negative impact from N-2 balance adjustments and a €25.9 million decrease in non-regulated revenues. The company noted a negative 2024 inflation balance of €26 million driven by regulatory reset.

Detailed Financial Analysis

ENAV’s operating costs increased in H1 2025, with personnel expenses rising by 4.5% to €309.7 million due to contractual salary inflation adjustments and variable components linked to traffic volume. Other costs grew by 4.9% to €68.1 million, primarily due to higher utility expenses.

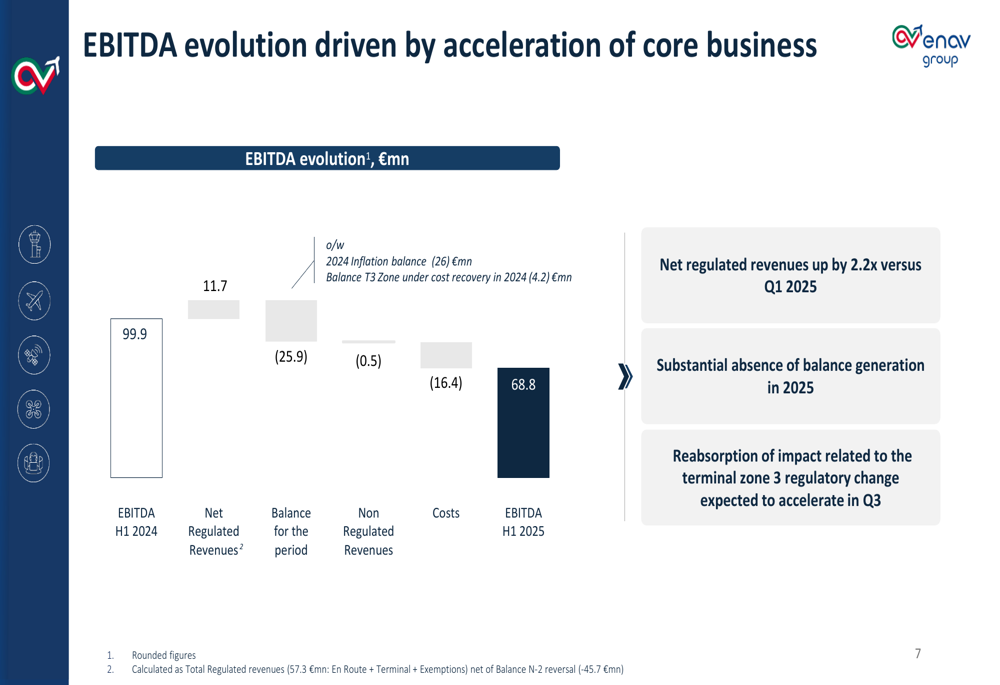

The combination of lower revenues and higher costs significantly impacted EBITDA, which fell by 31.1% year-over-year to €68.8 million. The following chart illustrates the EBITDA evolution:

Despite the substantial decline in EBITDA, management highlighted that net regulated revenues were 2.2 times higher than in Q1 2025, and they expect the reabsorption of impacts related to terminal zone 3 regulatory changes to accelerate in Q3.

The profit and loss summary reveals the extent of the financial performance decline:

EBIT decreased by 59.5% to €17.3 million, while net income fell by 69.6% to €7.0 million compared to H1 2024. Depreciation, amortization, and provisions decreased by 9.8% to €51.5 million, while financial expenses remained stable at €4.5 million.

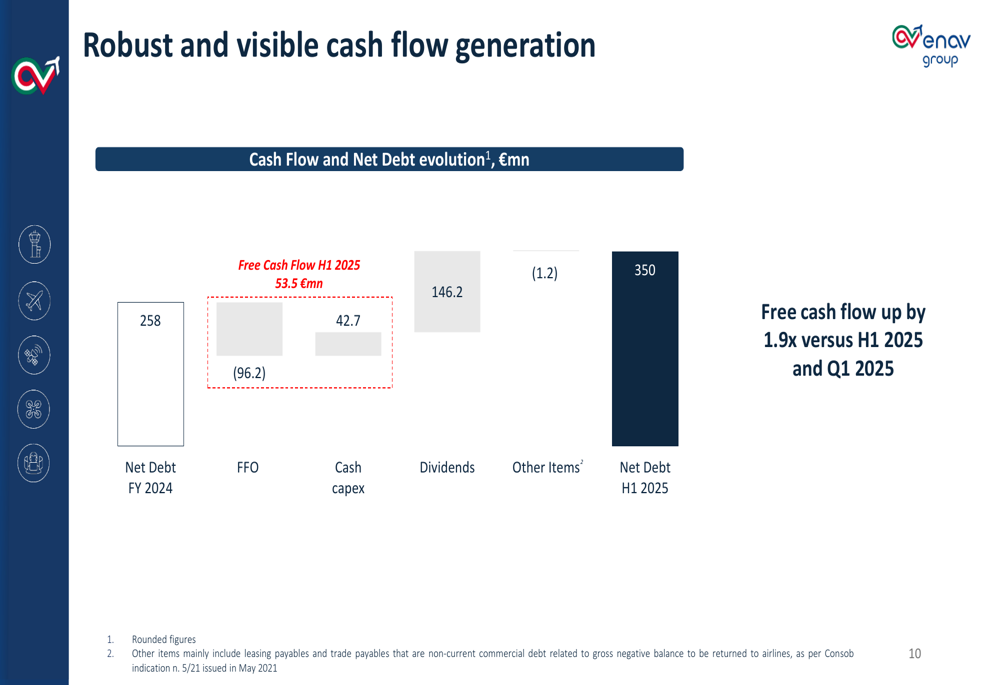

On a positive note, free cash flow generation improved significantly, nearly doubling compared to both Q1 2025 and H1 2024. However, net debt increased from €258 million at the end of 2024 to €350 million by the end of H1 2025, primarily due to dividend payments of €146.2 million.

Forward-Looking Statements

Despite the challenging first half results, ENAV’s management expressed confidence in achieving their upgraded 2025 targets. The company identified two key drivers for the EBITDA guidance upgrade:

Air traffic volume exceeding the original plan and quality of service bonuses are expected to drive EBITDA from the original target of €225 million to the new range of €245-253 million. Management emphasized their focus on efficiency measures to drive down the cost curve ahead of plan projections.

This optimistic outlook represents a significant improvement from the Q1 2025 results, when the company reported a €29.3 million loss. The presentation suggests that Q2 was substantially stronger and that management expects this positive momentum to continue through the second half of the year.

ENAV’s ability to deliver on these upgraded targets will depend on the continuation of strong traffic trends and the successful implementation of efficiency measures to offset rising costs. Investors will be watching closely to see if the company can translate its operational strength into improved financial performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.