Paul Tudor Jones sees potential market rally after late October

Introduction & Market Context

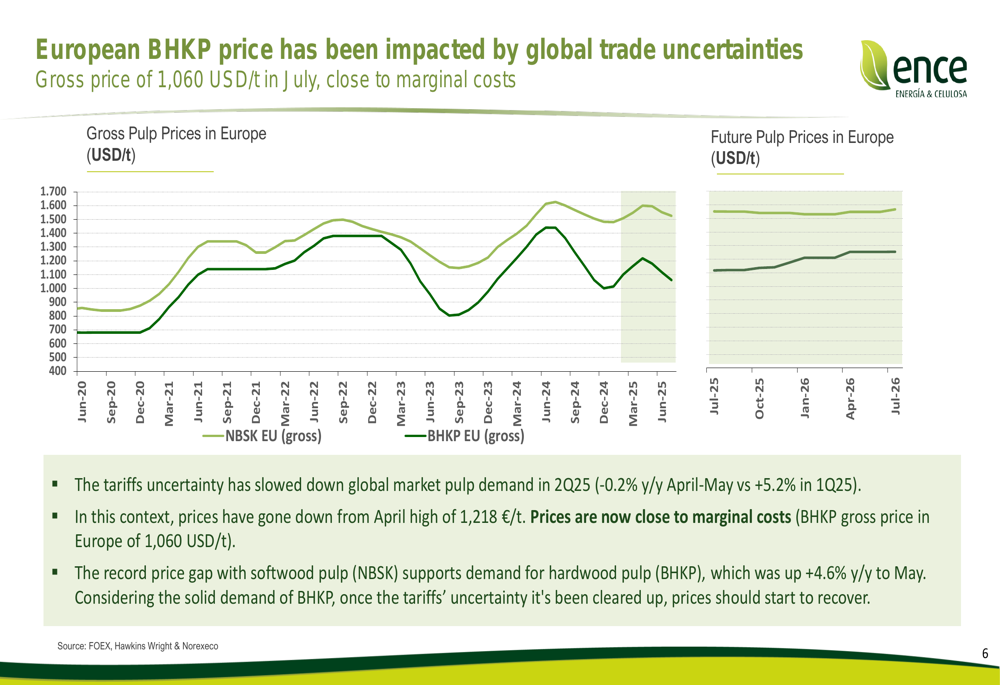

Ence Energia & Celulosa (BCBA:CELUm) presented its second quarter 2025 results on July 23, revealing a challenging period for the pulp producer as global trade uncertainties continued to impact market prices. The company reported that hardwood pulp (BHKP) prices have fallen to near marginal cost levels, reaching 1,060 USD/t in July, down from April’s high of 1,218 €/t.

Despite these headwinds, Ence has accelerated its strategic pivot toward higher-margin specialty products and diversification into renewable energy businesses. The company’s stock closed at €2.88 on the presentation day, down 0.28% and significantly below its 52-week high of €3.58, reflecting ongoing investor concerns about the pulp market outlook.

As shown in the following chart of European pulp price trends, tariff uncertainty has significantly impacted the market:

Quarterly Performance Highlights

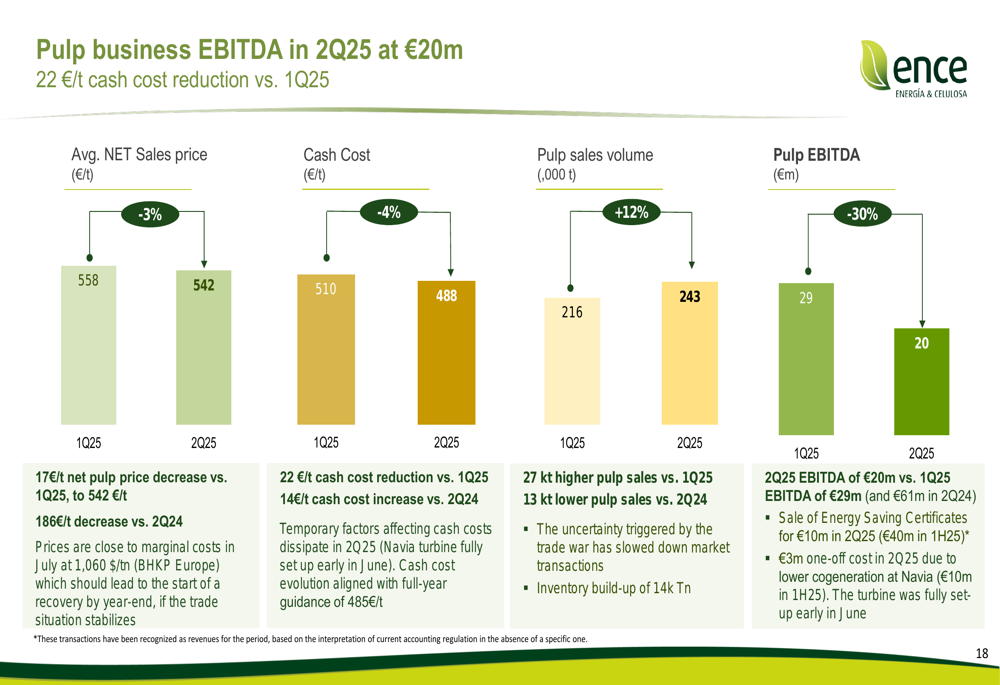

Ence reported a pulp business EBITDA of €20 million in Q2 2025, down from €28 million in the previous quarter. This decline occurred despite operational improvements, including a 22 €/t reduction in cash costs to 488 €/t and a 12% increase in pulp sales volume to 243,000 tons.

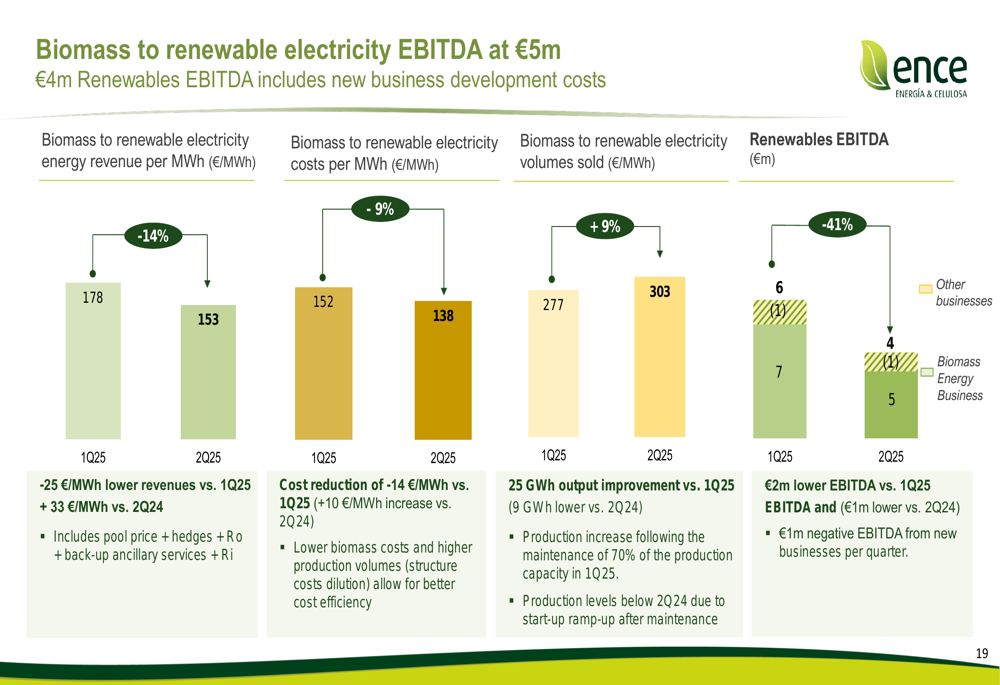

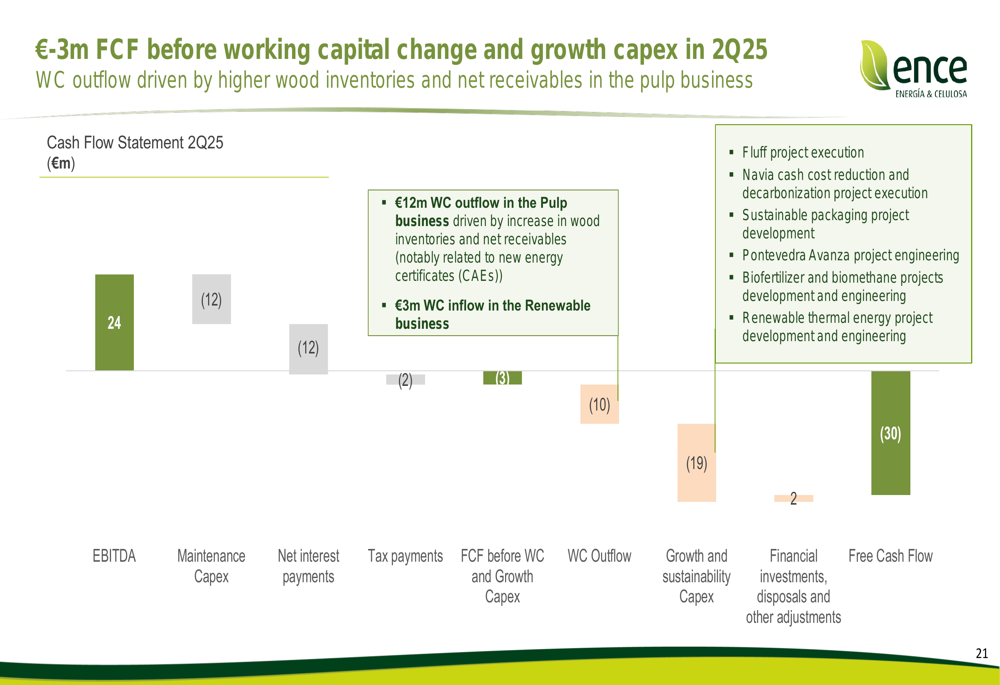

The company’s renewables business contributed €4 million to EBITDA, while energy saving certificates added €10 million in revenue during the quarter (€40 million year-to-date). Free cash flow before working capital changes and growth capex was negative at -€3 million, and consolidated net debt increased to €362 million, with a cash balance of €283 million.

The following chart illustrates the pulp business EBITDA performance:

The company’s biomass electricity business also showed mixed results, as shown in this breakdown:

Free cash flow was negatively impacted by several factors, as detailed in this chart:

Strategic Initiatives

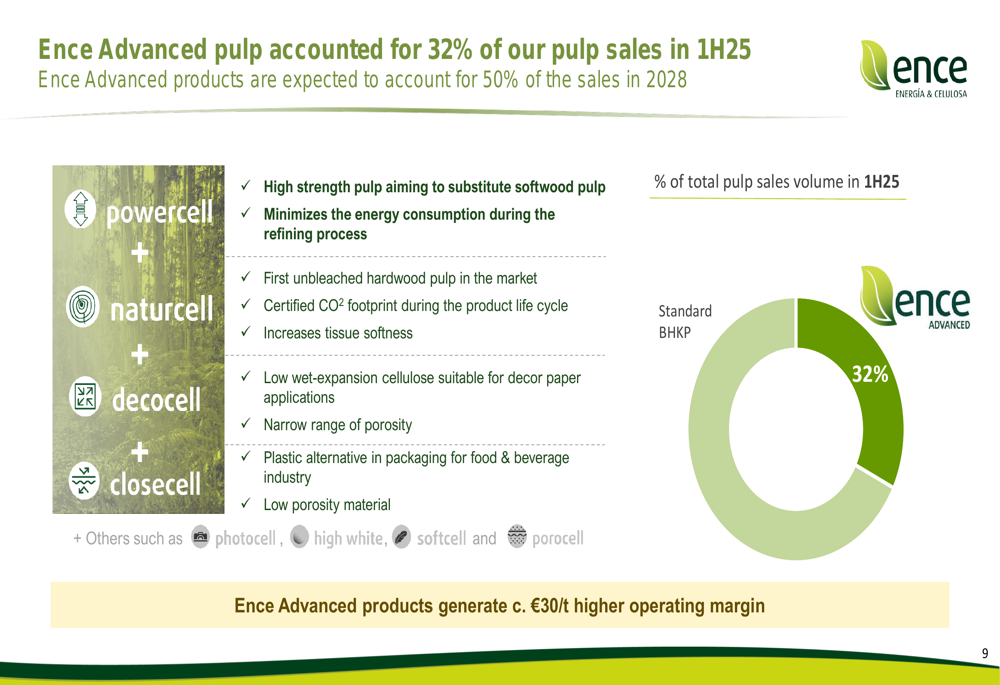

Ence is aggressively pursuing a strategic transformation to reduce its exposure to commodity pulp price volatility. The company’s "Ence Advanced" specialty pulp products now account for 32% of total pulp sales, with a higher operating margin of approximately €30/t compared to standard products. Management expects these premium offerings to reach 50% of sales by 2028.

The company’s product mix evolution is illustrated in the following chart:

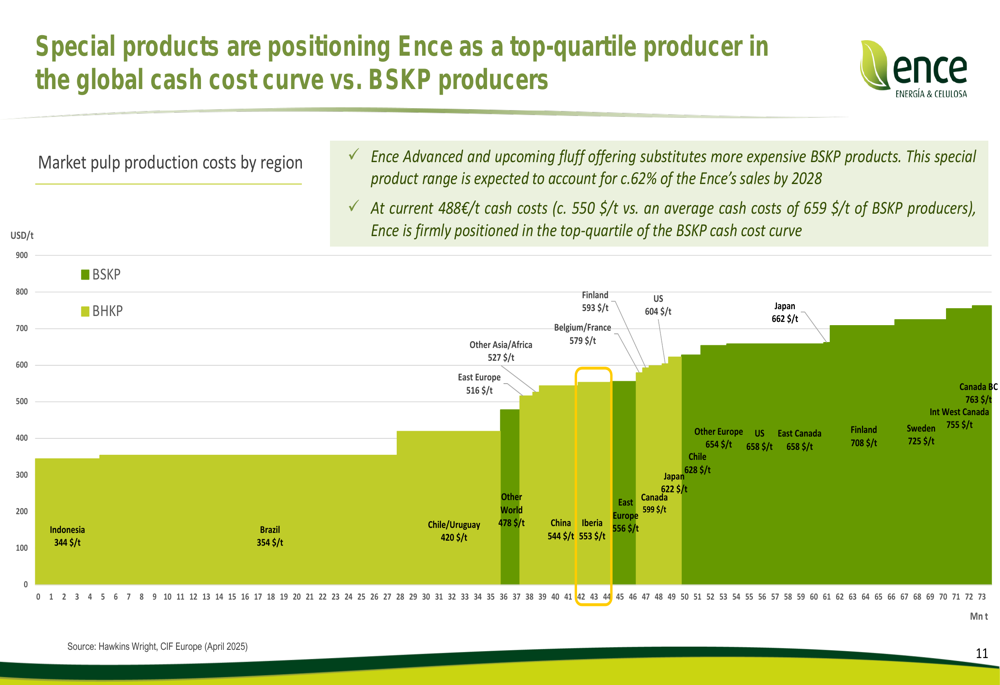

A key element of Ence’s strategy is its competitive positioning on the global cost curve. At current cash costs of 488€/t (approximately 550 $/t), the company ranks in the top quartile of global producers:

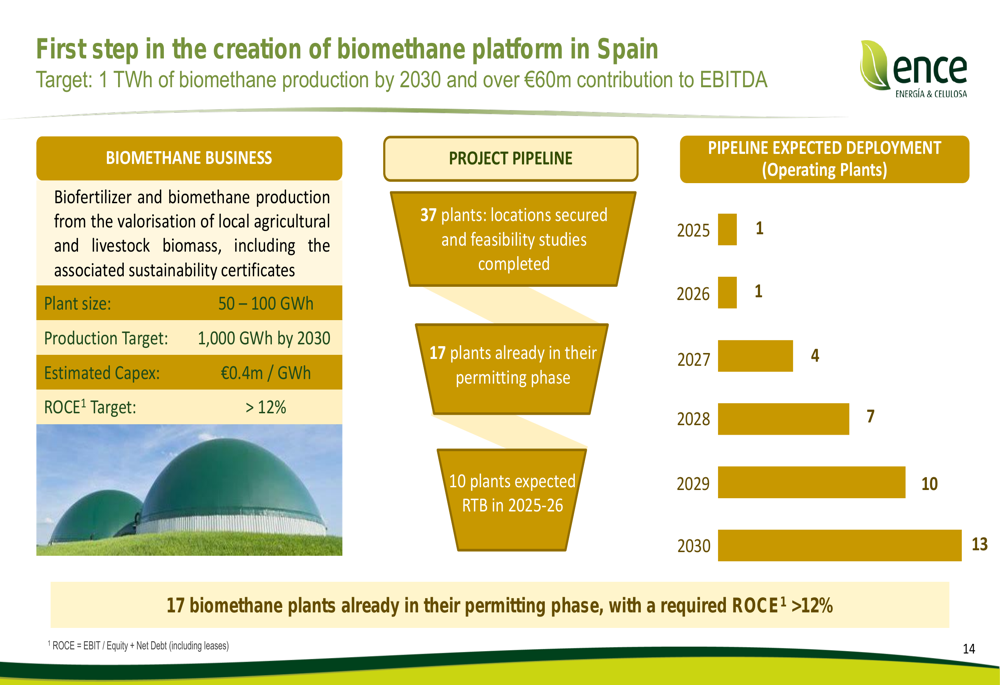

Beyond pulp products, Ence is diversifying into renewable energy businesses. The company is building a biomethane platform in Spain with a target of producing 1 TWh by 2030, expected to contribute over €60 million to EBITDA:

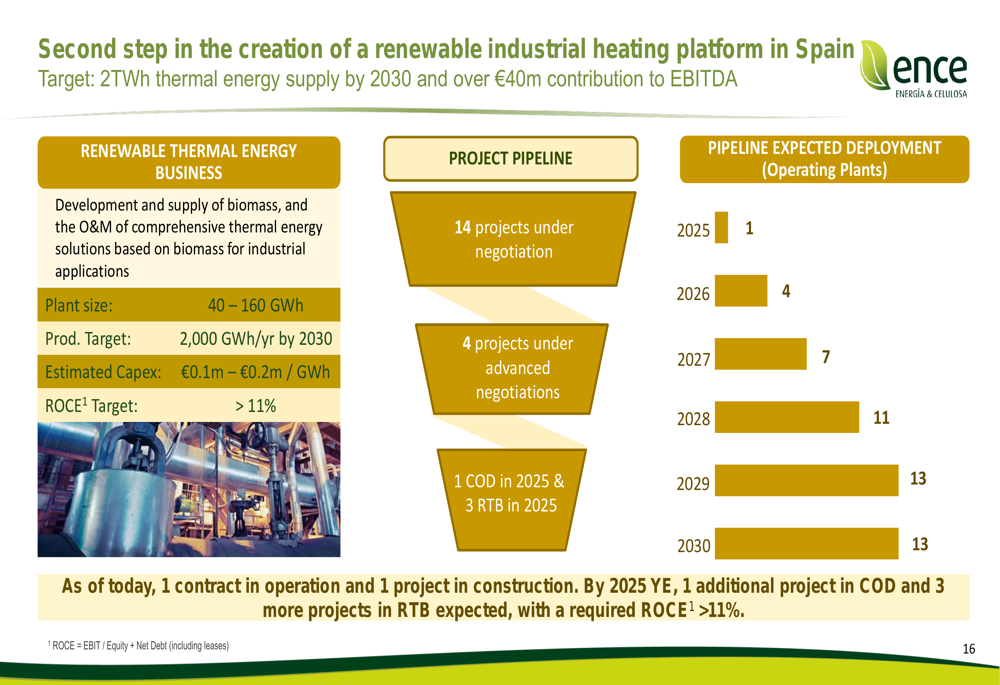

Additionally, Ence is developing a renewable industrial heating platform targeting 2 TWh of thermal energy supply by 2030, projected to add more than €40 million to EBITDA:

The company also emphasized its sustainability leadership, which supports its strategic positioning:

Forward-Looking Statements

Ence’s management expects pulp prices to recover by the end of 2025 as current prices are near marginal cost levels for many producers. A key milestone in the company’s transformation strategy is the commissioning of its first 125,000-ton fluff pulp line in Navia during Q4 2025, which is expected to generate an additional operating margin of €60/t compared to standard pulp.

By 2028, the company projects that special pulp sales will exceed 62% of total volume, significantly reducing its exposure to commodity price fluctuations. The renewable energy businesses are expected to provide substantial and stable cash flows, with biomethane and industrial heating platforms contributing over €100 million to EBITDA by 2030.

Market Response

Ence’s stock has been under pressure throughout 2025, trading near its 52-week low despite the company’s strategic initiatives. The Q2 presentation follows a disappointing Q1, when the company reported year-on-year declines in both revenues and profits, triggering a 4.5% stock drop.

Investors appear concerned about the short-term financial impact of global trade uncertainties on pulp prices, even as they evaluate the potential long-term benefits of Ence’s diversification strategy. The increase in net debt from €331 million in Q1 to €362 million in Q2 may also be contributing to market caution.

While management’s strategic vision focuses on transforming Ence into a more diversified and resilient company with higher-margin products, the market seems to be taking a wait-and-see approach until these initiatives translate into improved financial performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.