U.S. stocks rise on Fed cut bets; earnings continue to flow

Introduction & Market Context

Enento Group Plc (HEL:ENENTO) released its half-year financial report for Q2 2025 on July 15, revealing a slight revenue decline amid challenging economic conditions in its Nordic markets. The company, currently trading at €14.82 per share, reported mixed results across its business segments while continuing to launch new services and complete infrastructure improvements.

The presentation, delivered by Interim CEO and CFO Elina Stråhlman, highlighted that economic activity remained muted across Enento’s main markets, particularly affecting consumer credit information volumes in Sweden. Despite these headwinds, the company maintained stable performance in its Business Insight segment while focusing on strategic initiatives to drive future growth.

Quarterly Performance Highlights

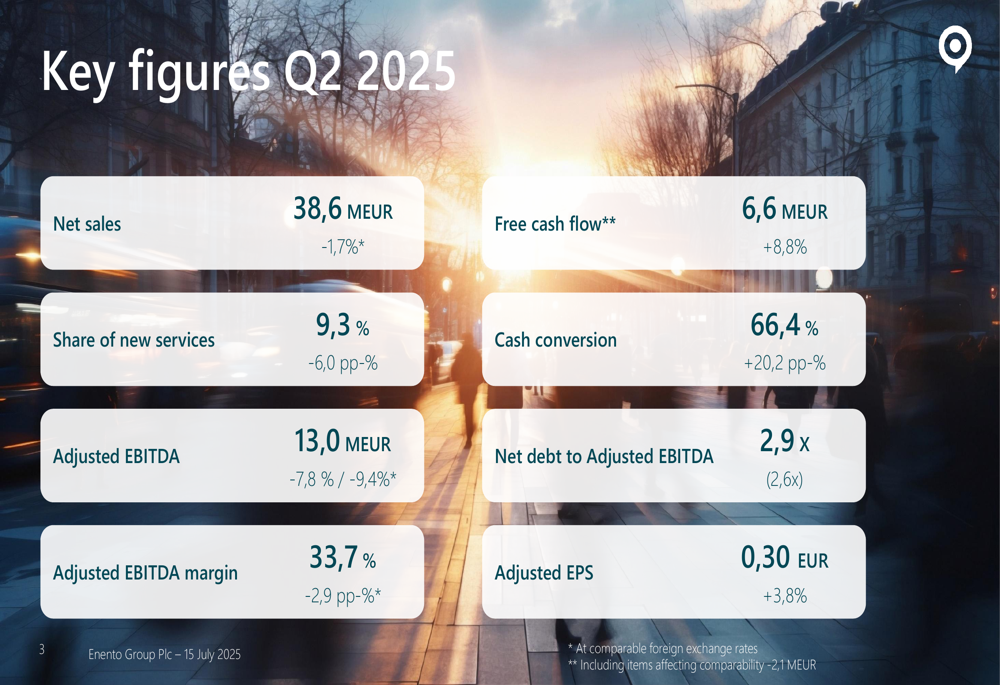

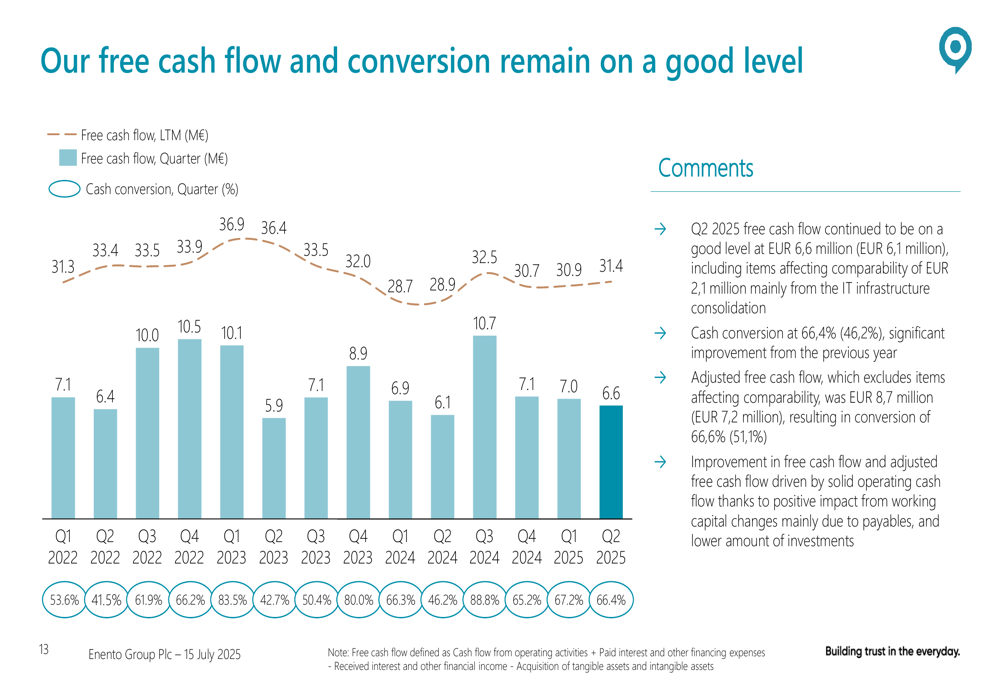

Enento reported Q2 2025 net sales of €38.6 million, representing a year-over-year decline of 1.7%. Despite the revenue dip, the company showed improvement in several key metrics, including free cash flow which increased by 8.8% to €6.6 million and adjusted earnings per share which rose 3.8% to €0.30.

As shown in the following key figures summary:

The adjusted EBITDA margin contracted to 33.7%, down 2.9 percentage points from the previous year, while adjusted EBITDA declined 7.8% to €13.0 million. The company’s net debt to adjusted EBITDA ratio increased slightly to 2.9x from 2.6x a year earlier, though still within the company’s long-term target of below 3x.

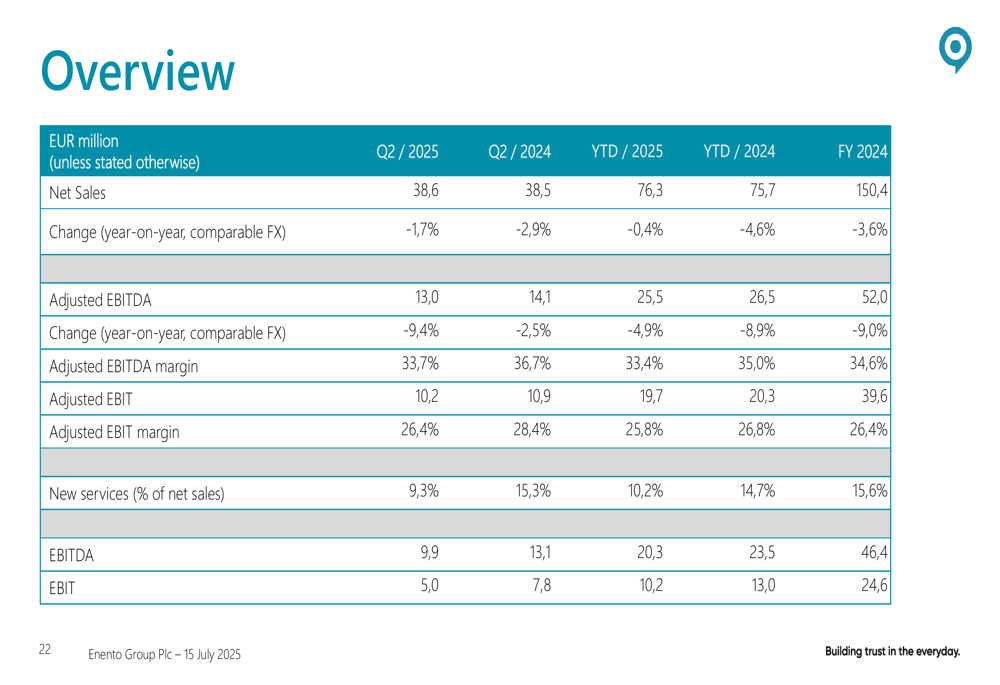

A more detailed view of the financial results shows the comparison with the previous year:

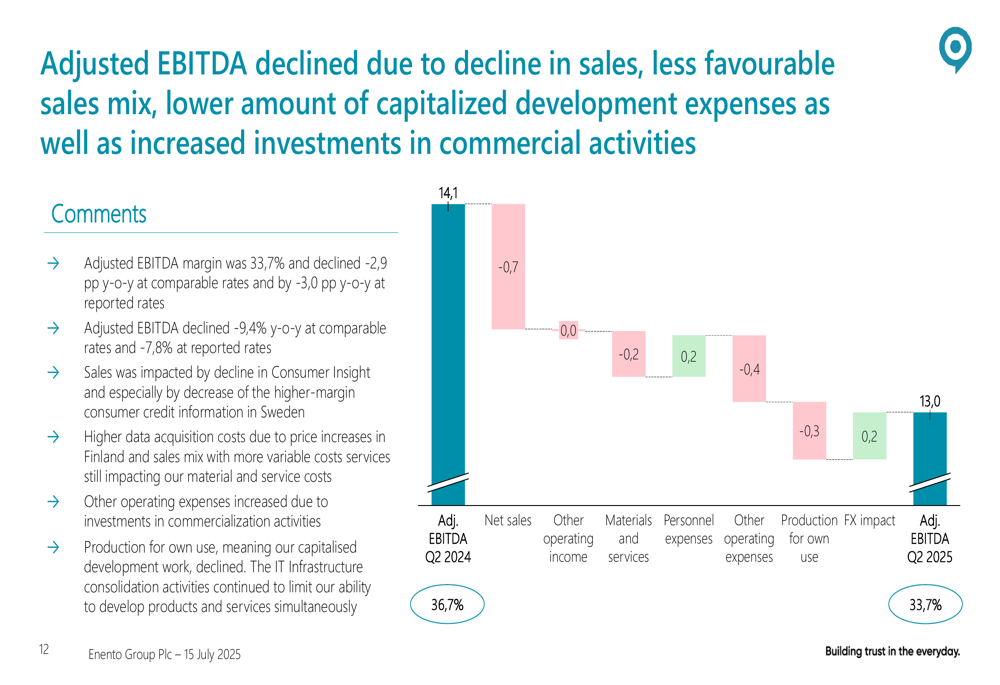

The decline in adjusted EBITDA was attributed to several factors, including lower sales volumes, a less favorable sales mix, and reduced capitalized development expenses:

Segment Performance Analysis

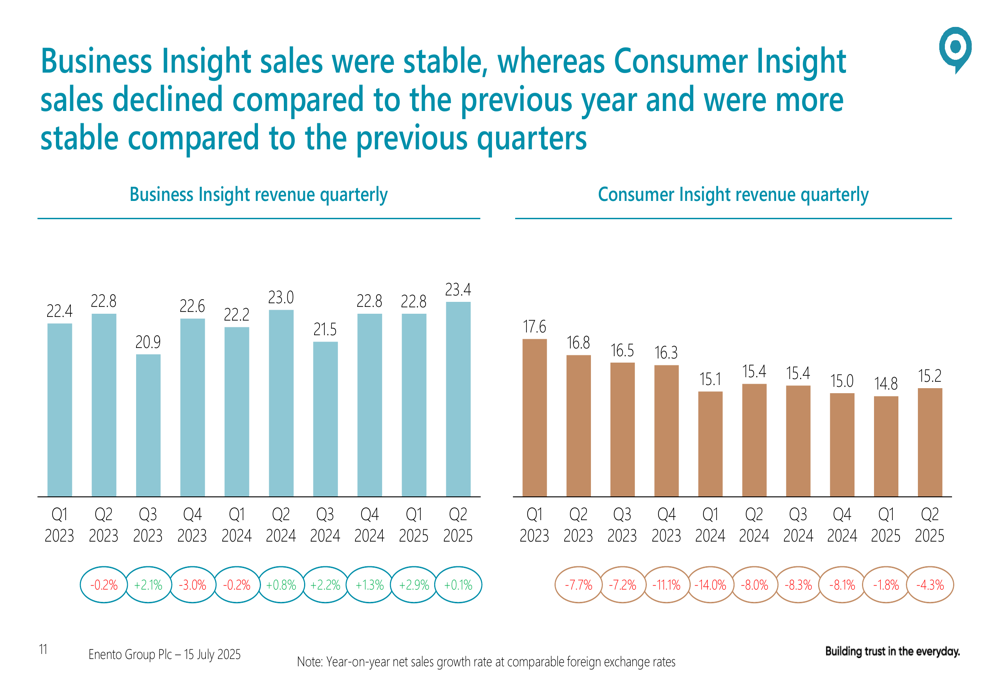

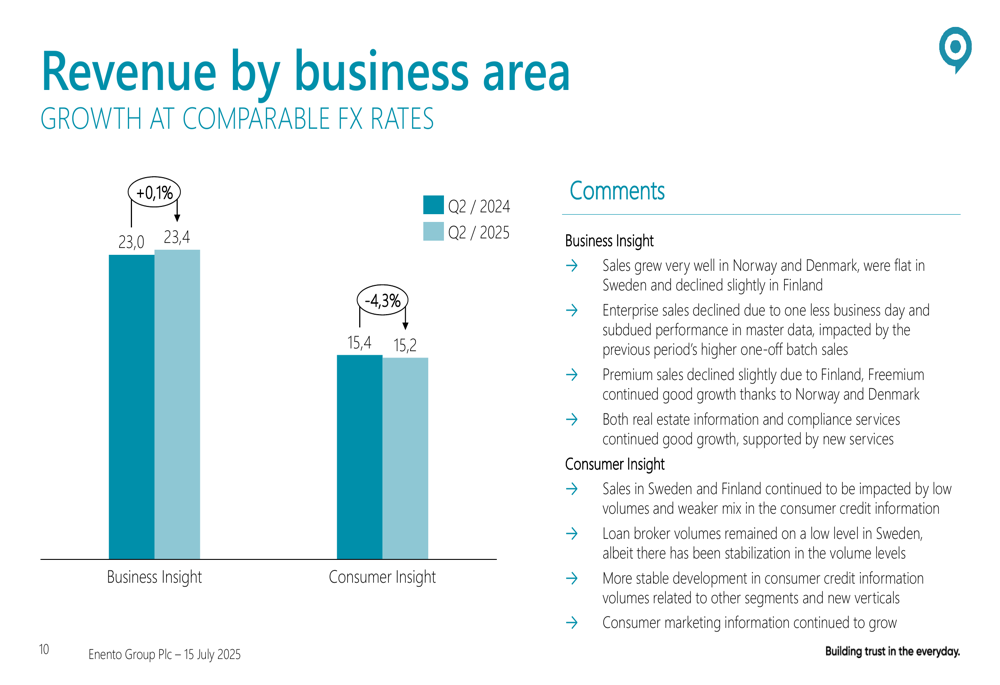

Enento’s business segments showed divergent performance in Q2 2025. The Business Insight segment, which accounts for 61% of total revenue, remained relatively stable with a marginal 0.1% increase in net sales to €23.4 million at comparable foreign exchange rates. This segment benefited from continued growth in compliance and real estate information services.

In contrast, the Consumer Insight segment experienced a 4.3% decline in net sales to €15.2 million, primarily due to low consumer credit information volumes, especially in the Swedish market. This segment continues to face challenges from structural changes and regulatory developments in the Swedish consumer credit market, including the parliament’s vote in favor of bank license requirements for loan brokers.

The quarterly revenue trend for both segments illustrates these divergent paths:

A breakdown of revenue by business area further highlights the performance difference:

Strategic Initiatives

Despite challenging market conditions, Enento continued to invest in strategic initiatives during Q2 2025. The company completed IT infrastructure server transitions in Finland and Sweden, launched innovative beneficial ownership and sanction screening services in Sweden, and introduced the Property ESG API in Finland.

A significant development was the launch of Proff PLUSS value-added services in Norway and Denmark, designed to provide more comprehensive company information and monitoring capabilities:

The company also reported initial success with its advanced credit rating service, Rating Odin, which gained its first orders during the quarter. These new service launches are part of Enento’s strategy to offset pressure in traditional markets by expanding into adjacent service areas.

Financial Outlook & Guidance

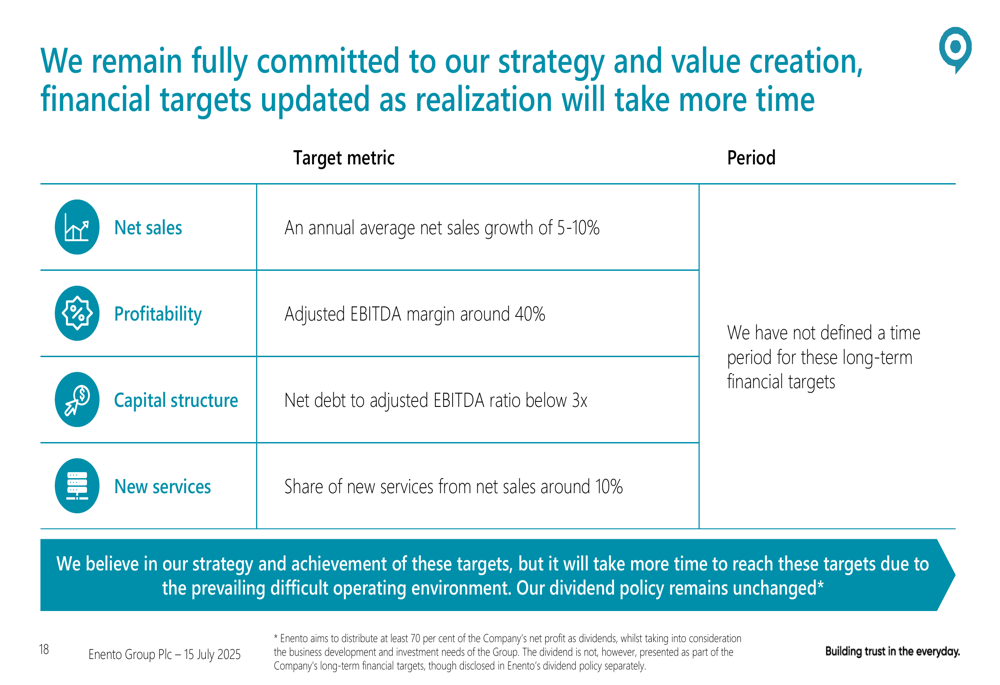

Enento maintained its full-year guidance for 2025, expecting net sales to be around €150-156 million and adjusted EBITDA to be around €50-55 million, assuming exchange rates remain at current levels. The company anticipates a gradually improving macroeconomic situation and stabilization in demand for information services.

The company also updated its long-term financial targets, which include:

For the remainder of 2025, Enento’s priorities include retaining and protecting core credit and business information services, advancing development and commercialization of new services, transforming the Swedish Premium business, and improving operational efficiency. Management acknowledged the continuing uncertainty in the macroeconomic environment and noted that consumer credit demand remains muted.

The company’s financial position remains solid, with strong cash conversion of 66.4% and free cash flow of €6.6 million for the quarter:

Overall, Enento’s Q2 2025 results reflect the challenges of operating in subdued Nordic markets, particularly in the consumer credit segment, while demonstrating the company’s ability to maintain profitability and cash generation through operational efficiency and strategic initiatives. The divergent performance of its business segments highlights both challenges and opportunities as the company continues to navigate an uncertain economic landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.