SoFi shares rise as record revenue, member growth drive strong Q3 results

Introduction & Market Context

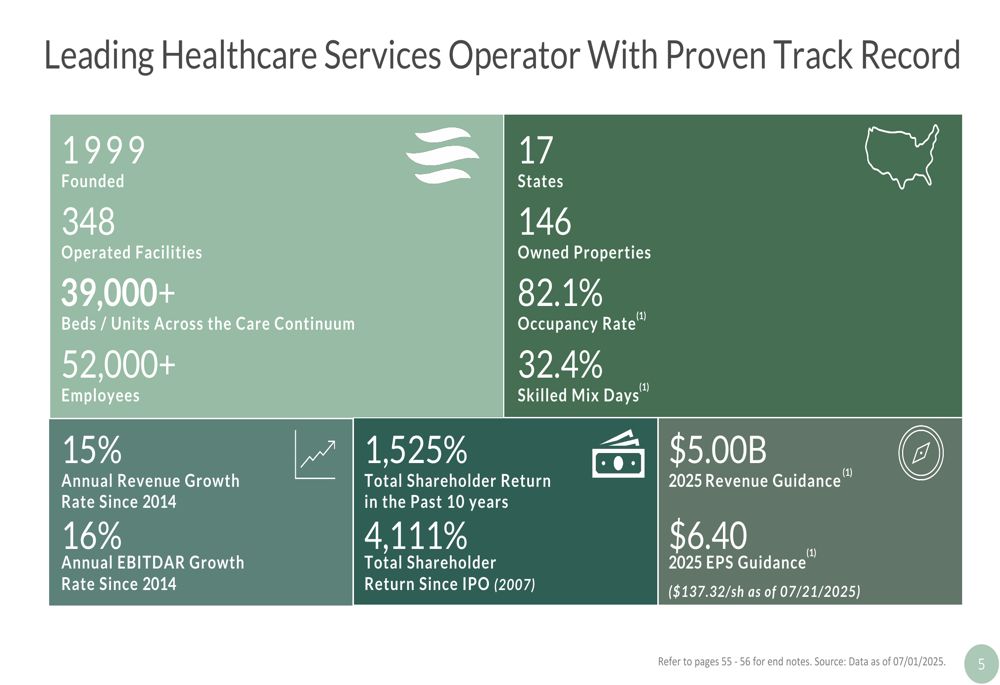

The Ensign Group (NASDAQ:ENSG), a leading provider of post-acute healthcare services, presented its Q2 2025 investor slides highlighting continued strong growth and operational improvements across its portfolio of 348 healthcare facilities. The company’s stock has performed exceptionally well, with a total shareholder return of 1,525% over the past decade and 4,111% since its 2007 IPO, significantly outperforming the broader healthcare sector.

Operating in a highly fragmented market where Ensign represents just 2.4% of the skilled nursing facility industry, the company continues to leverage favorable demographic trends, including an aging population that is projected to nearly double by 2060. This demographic shift supports Ensign’s long-term growth strategy as skilled nursing facilities currently receive 42% of Medicare post-acute dollars.

As shown in the following overview of key company metrics, Ensign has established itself as a leading healthcare services operator with a proven track record:

Quarterly Performance Highlights

Ensign Group reported impressive financial results for Q2 2025, with consolidated revenue reaching $1.23 billion, an 18.5% increase compared to Q2 2024. Consolidated adjusted net income rose to $93.3 million, representing a 22.1% year-over-year improvement. Same facility skilled nursing revenue increased by 6.5% compared to the prior year period.

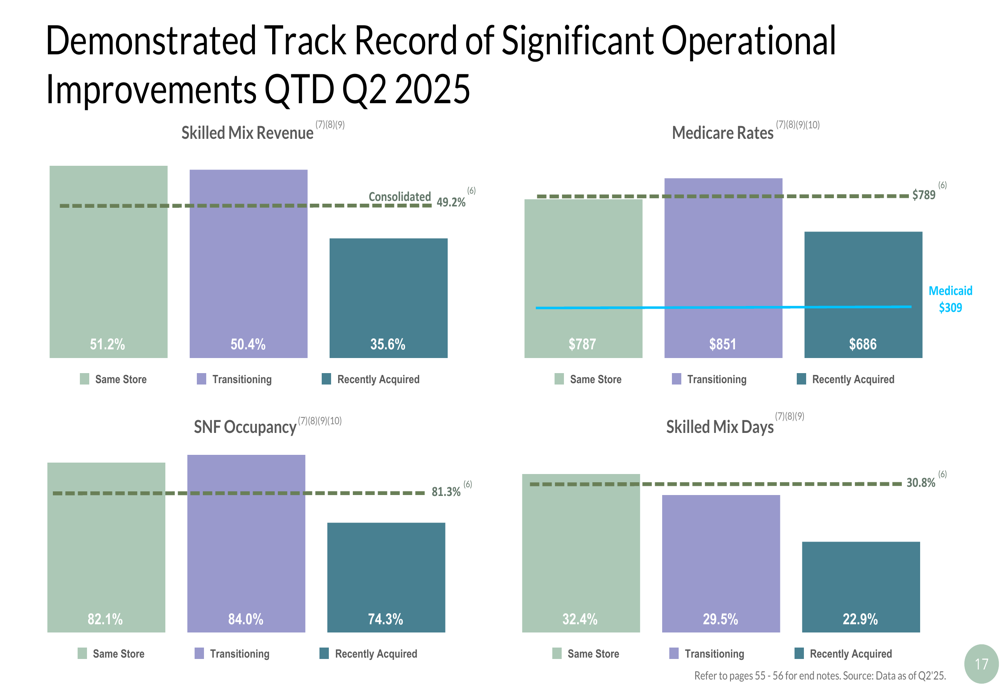

The company’s operational metrics also showed significant improvement, with same store skilled nursing occupancy rising to 82.1% and skilled mix days at 32.4%. These improvements reflect Ensign’s continued focus on clinical quality and operational excellence.

The following chart illustrates Ensign’s track record of operational improvements across its portfolio in Q2 2025:

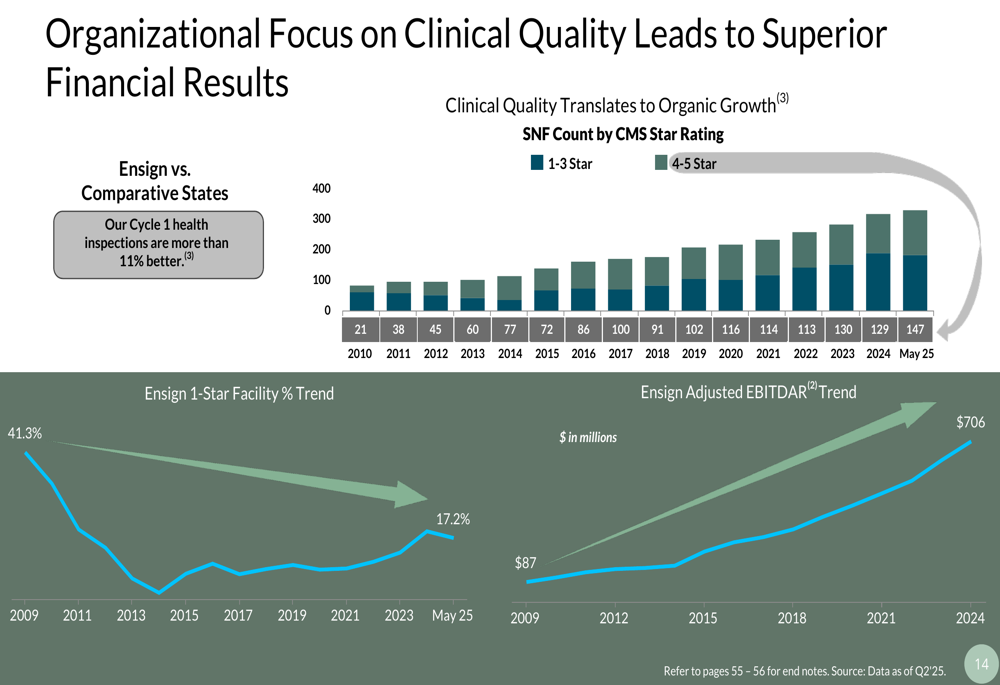

Ensign’s strong financial performance is underpinned by its focus on clinical quality, which has led to improved CMS star ratings across its portfolio. The company has reduced its percentage of 1-star facilities from 41.3% in 2009 to 17.2% in May 2025, while simultaneously growing its adjusted EBITDAR from $87 million to a projected $706 million over the same period.

This correlation between clinical quality and financial performance is clearly demonstrated in the following chart:

Acquisition Strategy and Operational Improvements

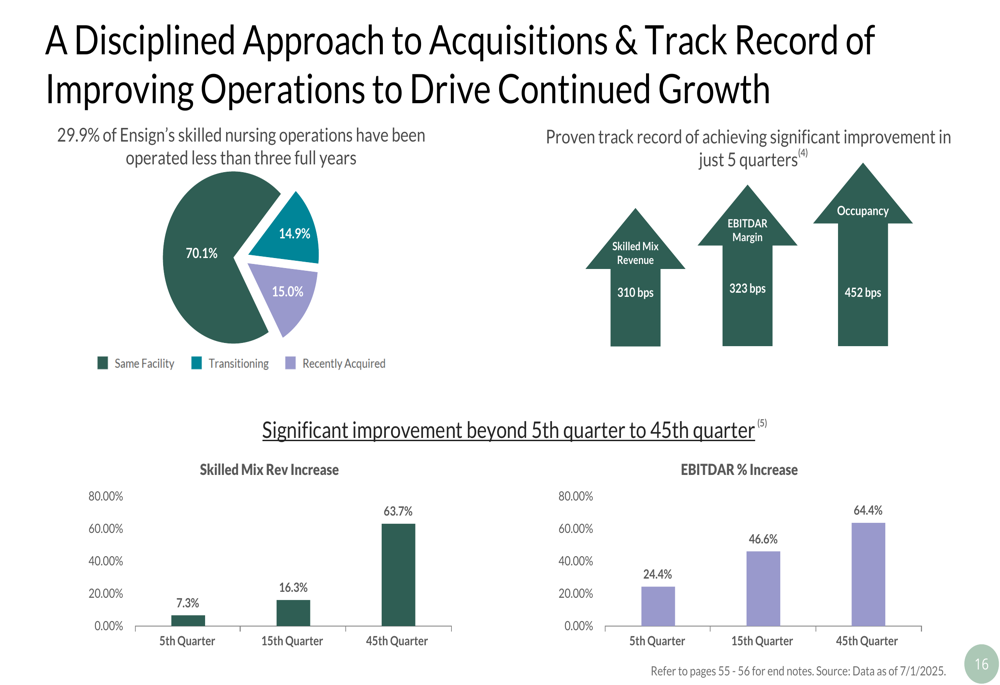

A key driver of Ensign’s growth has been its disciplined approach to acquisitions and subsequent operational improvements. The company has completed 78 acquisitions since 2023, with 29.9% of its skilled nursing operations having been operated for less than three years.

Ensign has demonstrated a consistent ability to improve newly acquired operations, with significant enhancements in skilled mix revenue, EBITDAR margins, and occupancy typically achieved within just five quarters of acquisition. This pattern of improvement continues well beyond the initial integration period, with operations showing continued growth through the 45th quarter.

The following chart illustrates Ensign’s disciplined approach to acquisitions and its track record of improving operations:

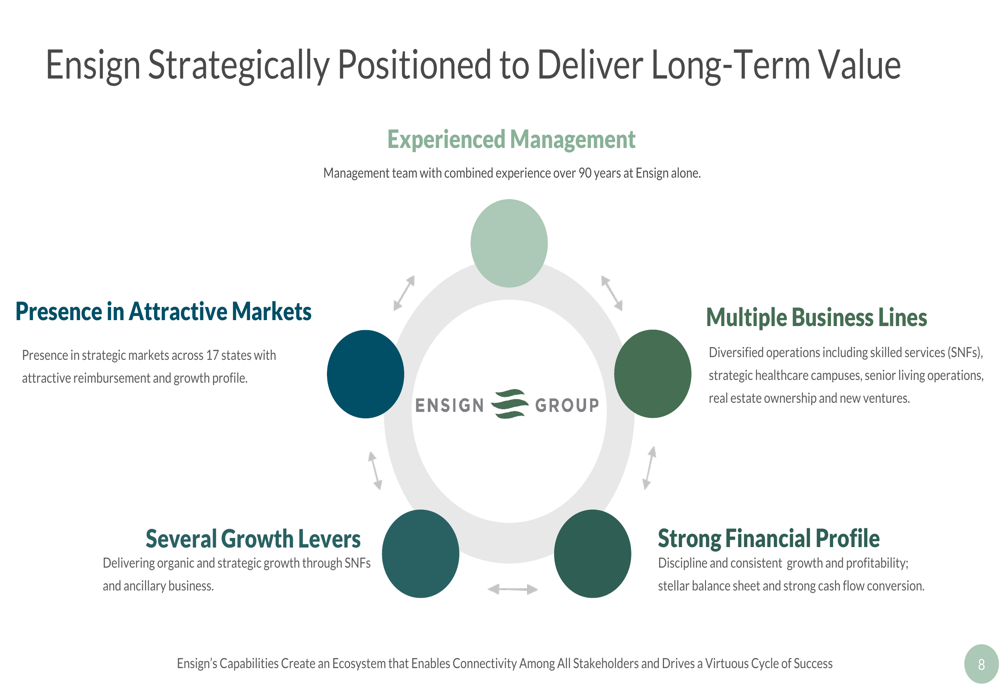

Central to Ensign’s operational success is its unique "cluster model," which empowers local leaders to make decisions based on the specific needs of their communities while benefiting from shared resources and best practices. This decentralized approach has enabled Ensign to maintain entrepreneurial agility despite its growing scale.

The company’s strategic positioning is designed to deliver long-term value through several key strengths, as illustrated below:

Standard Bearer REIT Performance

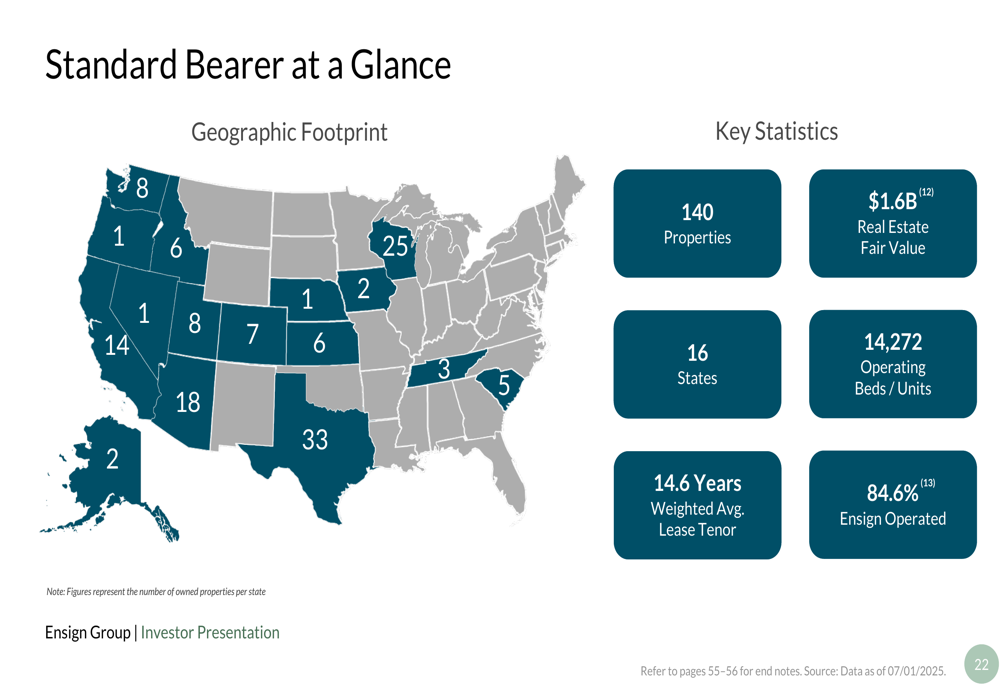

Ensign’s captive REIT, Standard Bearer, represents a significant component of the company’s overall strategy. As of July 2025, Standard Bearer owned 140 properties across 16 states with a real estate fair value of approximately $1.6 billion. The REIT structure provides increased visibility into embedded real estate value, expanded acquisition opportunities, and capital flexibility.

The following overview provides key statistics about Standard Bearer’s portfolio:

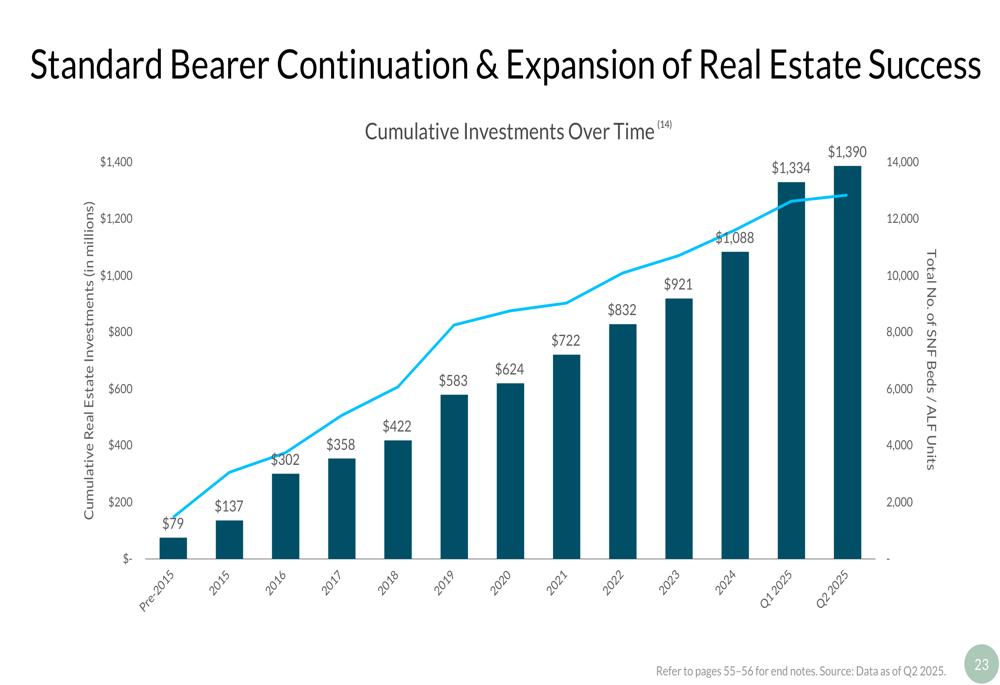

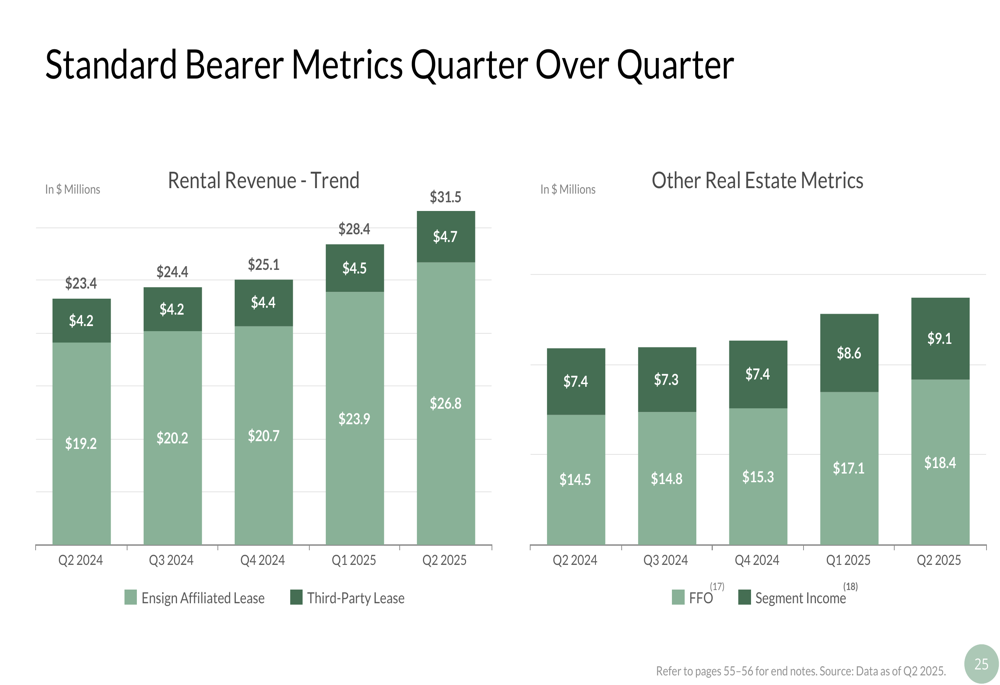

Standard Bearer has demonstrated consistent growth in both its property portfolio and financial performance. Cumulative investments have increased steadily over time, reaching $1.39 billion by Q2 2025. The REIT’s rental revenue has also shown strong quarter-over-quarter growth, with total rental revenue reaching $31.5 million in Q2 2025, compared to $23.4 million in Q2 2024.

The following chart illustrates Standard Bearer’s expansion of real estate investments over time:

Standard Bearer’s quarterly financial performance shows consistent improvement, with rental revenue, funds from operations (FFO), and segment income all trending upward:

Forward-Looking Guidance

Looking ahead, Ensign has provided guidance for 2025, projecting annual revenue between $4.99 billion and $5.02 billion and diluted adjusted earnings per share between $6.34 and $6.46. This EPS guidance represents a 16.4% increase over 2024 and a 34.2% increase over 2023, reflecting management’s confidence in continued growth.

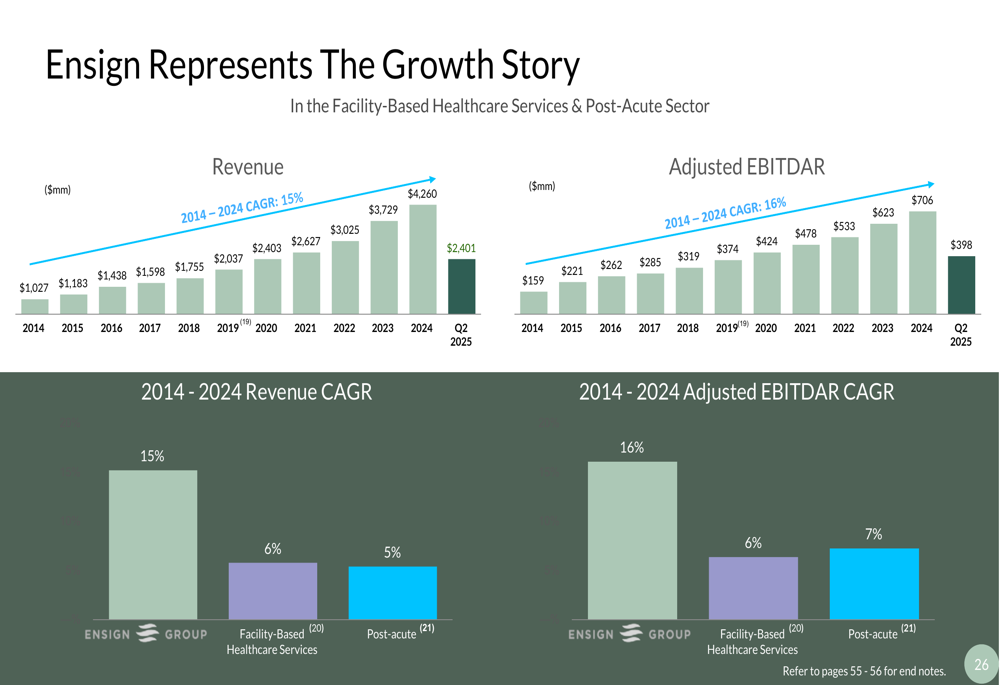

Ensign’s long-term growth trajectory remains impressive, with a 15% revenue CAGR and 16% adjusted EBITDAR CAGR from 2014 to 2024. This consistent performance underscores the sustainability of Ensign’s business model and growth strategy.

The following chart illustrates Ensign’s growth story over the past decade:

This growth has translated into exceptional returns for shareholders, as shown in the following chart:

Conclusion

Ensign Group’s Q2 2025 investor presentation highlights a company executing effectively on multiple fronts: delivering strong financial results, successfully integrating acquisitions, improving clinical quality, and expanding its real estate portfolio through Standard Bearer REIT. With a market capitalization of $10.24 billion and trading near its 52-week high, investor confidence in Ensign’s growth strategy appears strong.

The company’s decentralized operating model, focus on clinical excellence, and disciplined acquisition approach have created a virtuous cycle that continues to drive performance. As demographic trends remain favorable for post-acute care providers, Ensign appears well-positioned to maintain its growth trajectory while continuing to expand its relatively small 2.4% market share in a highly fragmented industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.