Street Calls of the Week

Introduction & Market Context

EQT Corporation (NYSE:EQT), America’s largest natural gas producer, presented its first quarter 2025 results on April 22, showcasing record-setting financial performance and announcing a strategic acquisition. The company continues to position itself as "The Premier American Natural Gas Company" and the only domestic, large-scale vertically integrated natural gas producer, with a focus on capitalizing on growing demand from data centers and LNG exports.

The presentation comes amid a backdrop of increasing natural gas demand, particularly from data centers supporting AI infrastructure and coal-to-gas switching in power generation. EQT (ST:EQTAB)’s strategy of tactical production management and vertical integration appears to be paying dividends in this environment of structural changes in natural gas markets.

Quarterly Performance Highlights

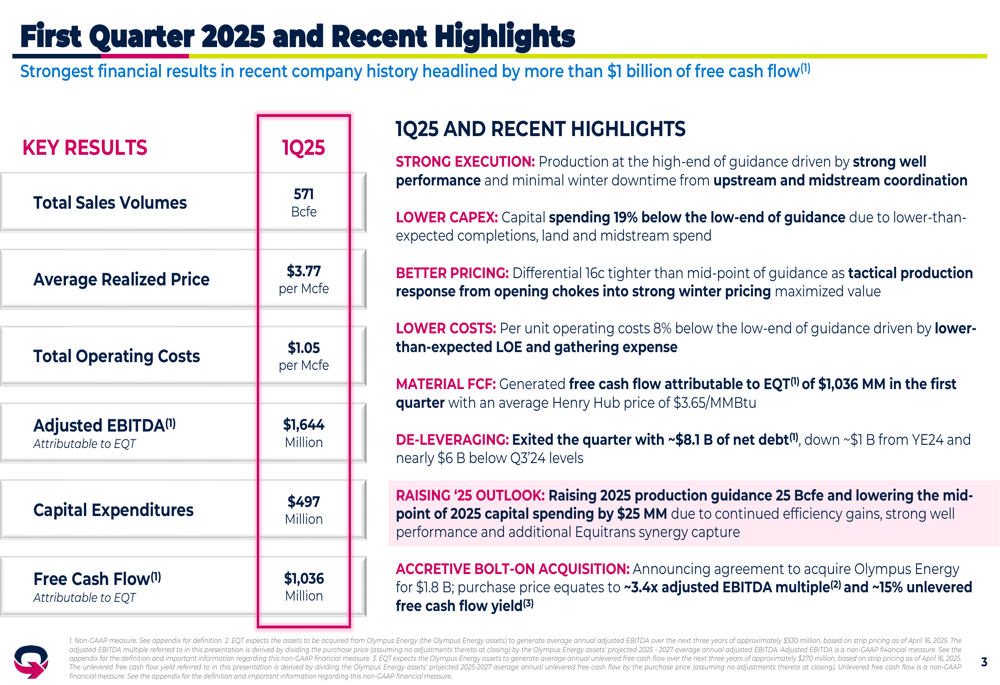

EQT reported impressive financial results for Q1 2025, with total sales volumes of 571 Bcfe and an average realized price of $3.77 per Mcfe. The company achieved total operating costs of $1.05 per Mcfe, generating adjusted EBITDA attributable to EQT of $1,644 million and free cash flow attributable to EQT of $1,036 million, with capital expenditures of $497 million.

As shown in the following chart highlighting key financial results and recent achievements, EQT demonstrated strong execution across multiple metrics:

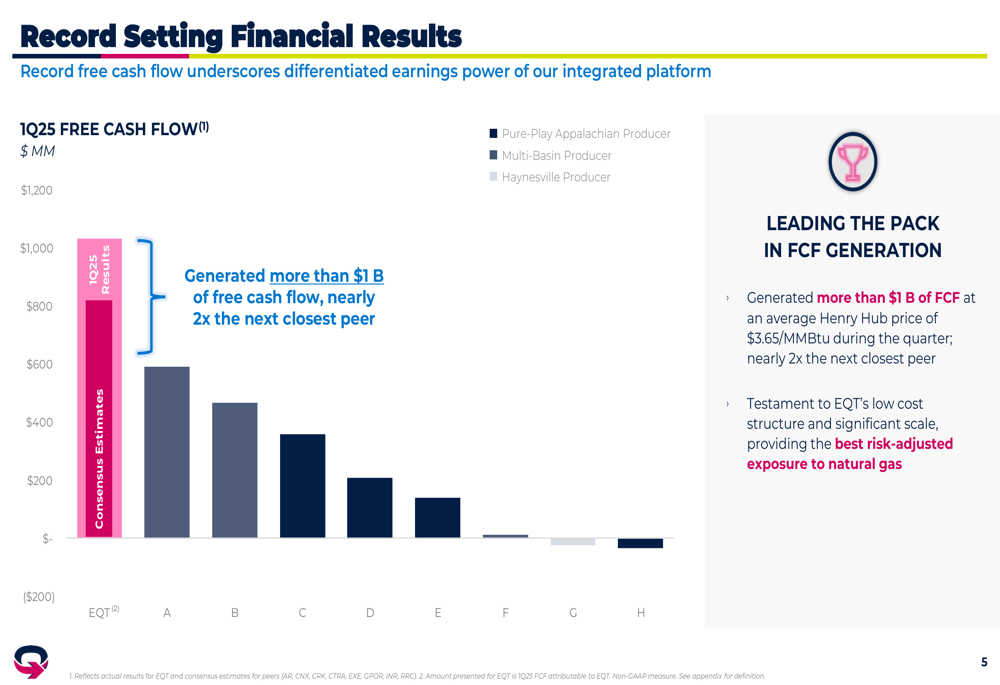

The company’s free cash flow performance was particularly noteworthy, substantially outpacing industry peers. EQT generated more than $1 billion in free cash flow at an average Henry Hub price of $3.65/MMBtu during the quarter, nearly double that of the next closest competitor.

The following comparison illustrates EQT’s superior free cash flow generation relative to peers:

Strategic Initiatives

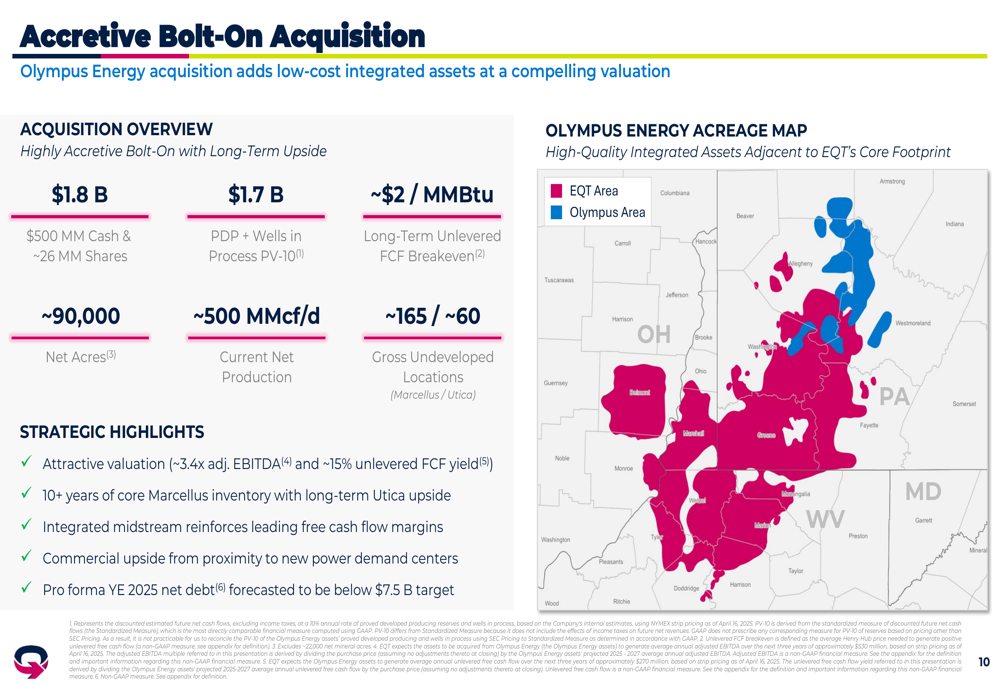

A major announcement in the presentation was EQT’s acquisition of Olympus Energy for $1.8 billion. This bolt-on acquisition includes 90,000 net acres, approximately 500 MMcf/d of current production, and around 225 gross undeveloped locations across the Marcellus and Utica formations. The acquisition is valued at approximately 3.4x adjusted EBITDA and offers a 15% unlevered free cash flow yield.

The strategic benefits of this acquisition are illustrated in the following map showing how the Olympus acreage complements EQT’s existing footprint:

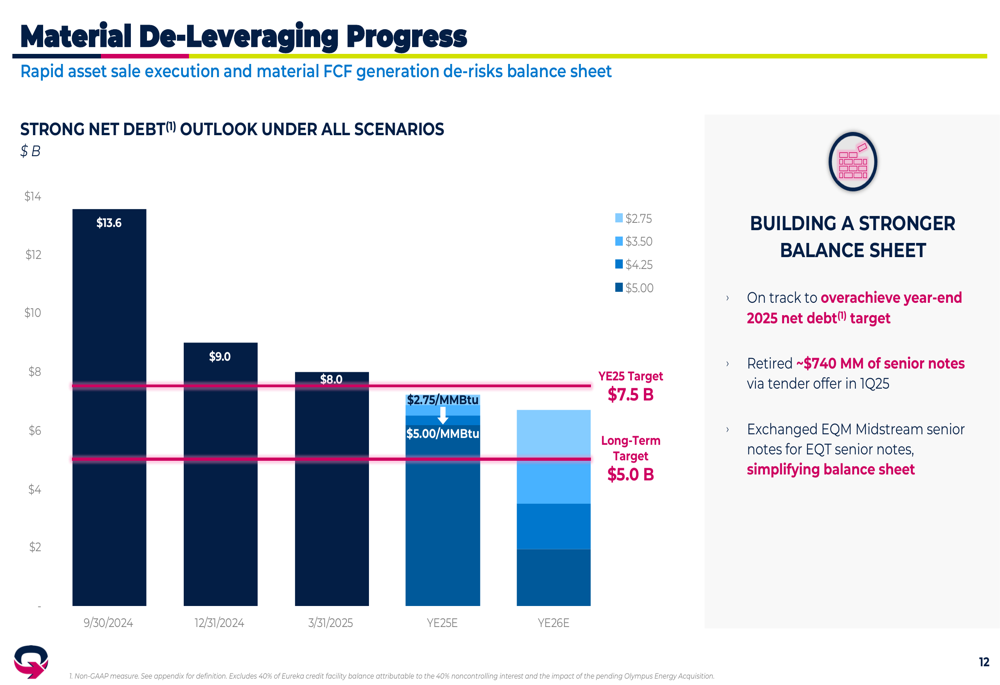

EQT also highlighted significant progress in de-leveraging its balance sheet, retiring approximately $740 million of senior notes and simplifying its balance sheet with EQM Midstream senior notes. The company is on track to achieve its year-end 2025 net debt target of $7.5 billion.

The following chart demonstrates EQT’s de-leveraging progress and outlook:

Operational Efficiency & Environmental Leadership

The presentation emphasized EQT’s continued operational efficiency gains, with completion efficiency increasing by approximately 30% compared to 2023. The company reached a new all-time high in completion efficiency during Q1 2025, leading to material well cost savings and lower overall maintenance capital. These improvements have allowed operations to drop from 3 to 2 frac crews in April while maintaining completion pace.

EQT also highlighted the benefits of its integrated midstream coordination following the Equitrans integration, reporting a 90% decrease in production lost due to winter storms. This improved reliability was demonstrated by comparing the impacts of the 2022 Winter Storm Elliott to the 2025 Winter Storm Heather.

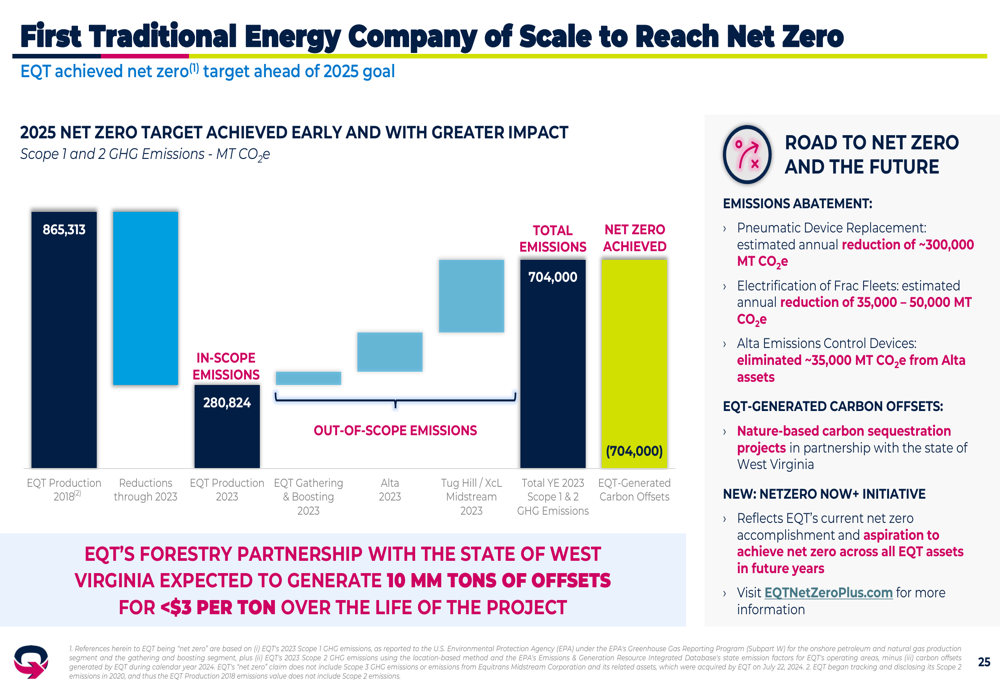

In a significant environmental achievement, EQT announced it has become the first traditional energy company of scale to reach net zero for Scope 1 and 2 greenhouse gas emissions, achieving this target ahead of its 2025 goal:

Forward-Looking Statements

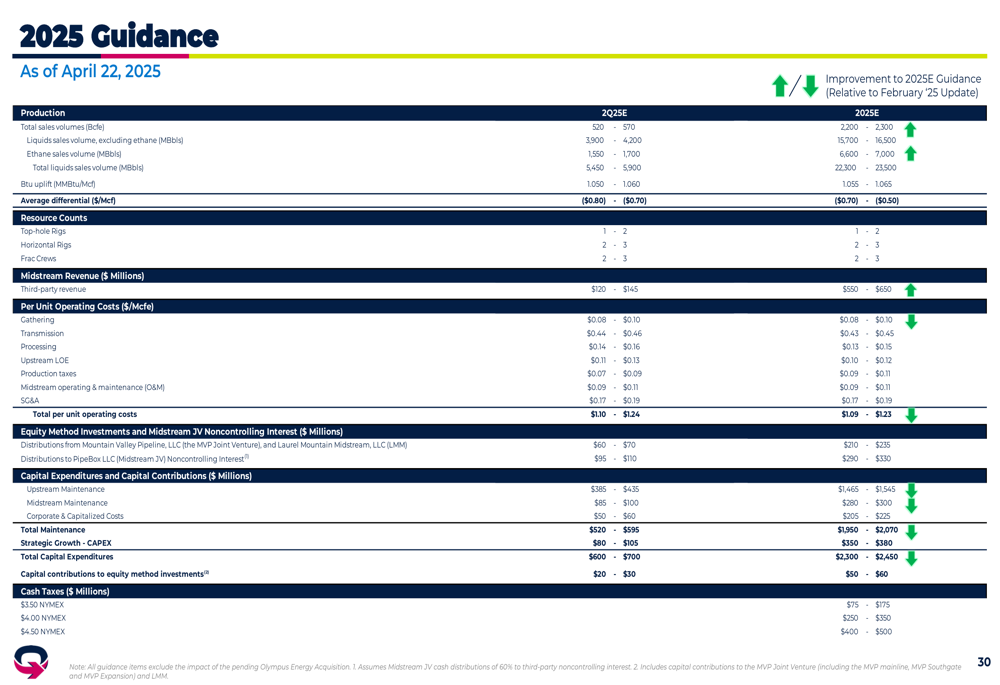

Looking ahead, EQT provided updated guidance for 2025, showing improvements relative to its February 2025 update. The company expects to benefit from structural basis improvement, projecting a compression of corporate basis by approximately 30¢ in 2028 and beyond, which would translate to over $600 million of annual free cash flow uplift.

The detailed 2025 guidance covers production, resource counts, midstream revenue, unit operating costs, and capital expenditures:

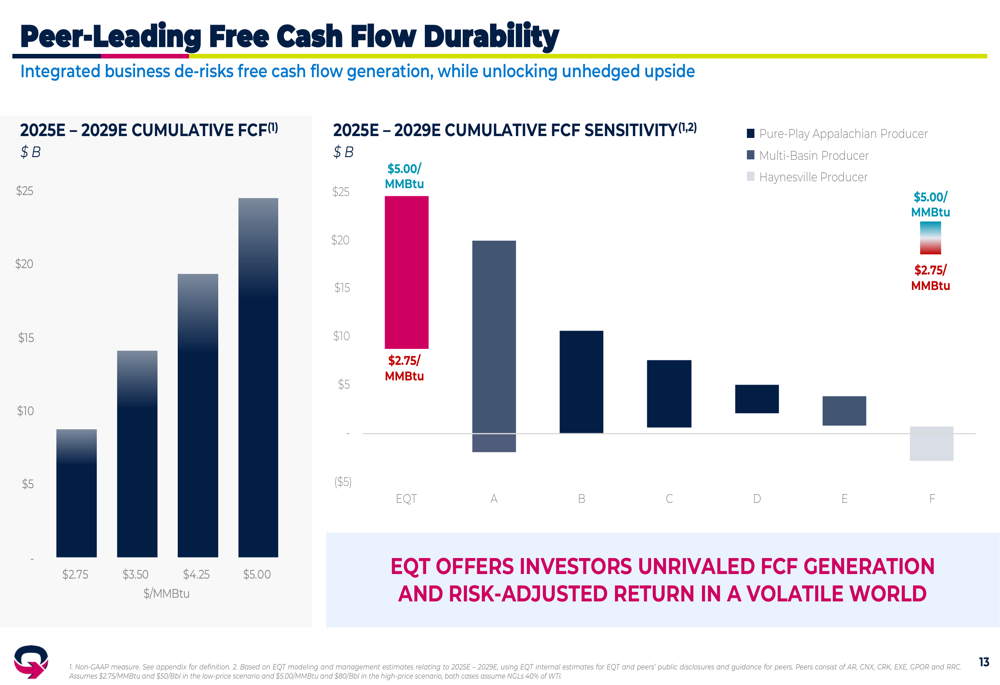

EQT emphasized its peer-leading free cash flow durability across various price scenarios. At $5.00/MMBtu, the company projects significantly higher cumulative free cash flow from 2025-2029 compared to peers, while maintaining strong cash generation even at lower price points of $2.75/MMBtu.

The following chart illustrates EQT’s projected free cash flow durability compared to peers:

EQT also highlighted the growing natural gas demand from data centers, noting that approximately 55 gigawatts of data centers are under development in EQT’s operational area, with 1 gigawatt equating to approximately 0.15 Bcf/d of natural gas demand. This emerging demand source, combined with continued LNG export growth and coal retirements, supports the company’s bullish outlook on natural gas fundamentals.

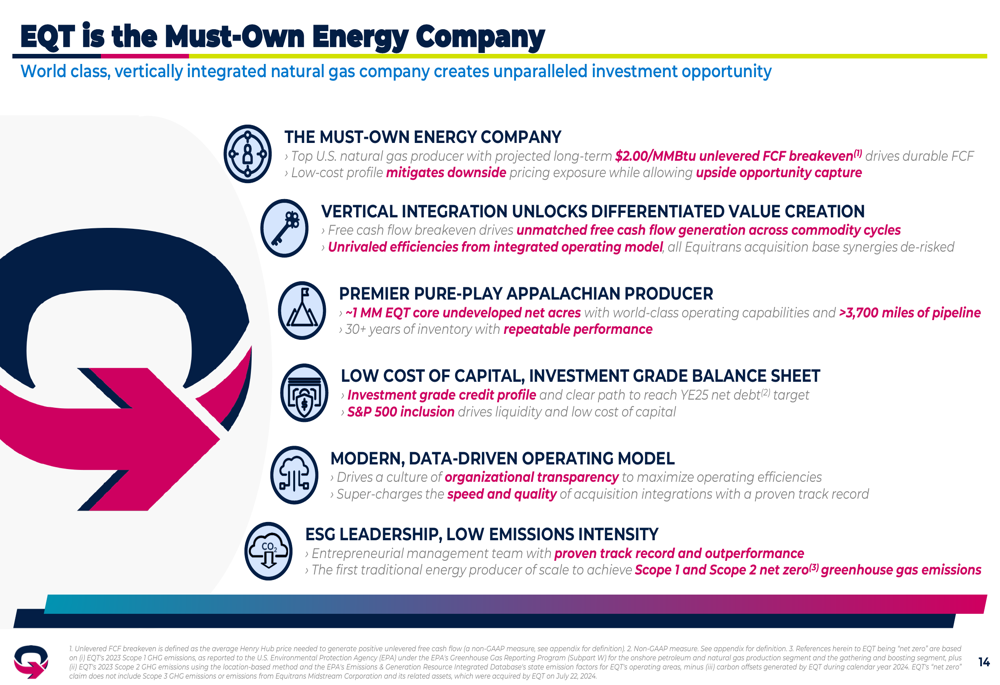

In summarizing its investment case, EQT presented itself as "the Must-Own Energy Company" based on its low-cost profile, vertical integration, premier Appalachian position, investment-grade balance sheet, data-driven operating model, and ESG leadership:

With its record financial performance, strategic acquisition, operational efficiency gains, and environmental leadership, EQT appears well-positioned to capitalize on growing natural gas demand while maintaining financial discipline and returning value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.