Futures slip, bank earnings ahead, Powell to speak - what’s moving markets

Introduction & Market Context

Telefonaktiebolaget LM Ericsson (NASDAQ:ERIC) presented its third quarter 2025 earnings on October 14, showcasing improved profitability metrics despite facing headwinds in organic sales growth. The Swedish telecommunications equipment manufacturer reported a 2% year-over-year decline in organic sales, though this was offset by significant margin improvements and a substantial cash boost from the divestment of its iconectiv business.

Ericsson shares reacted modestly to the results, with the stock down 0.85% at the regular session close and showing a further 0.24% decline in after-hours trading to $8.22.

Quarterly Performance Highlights

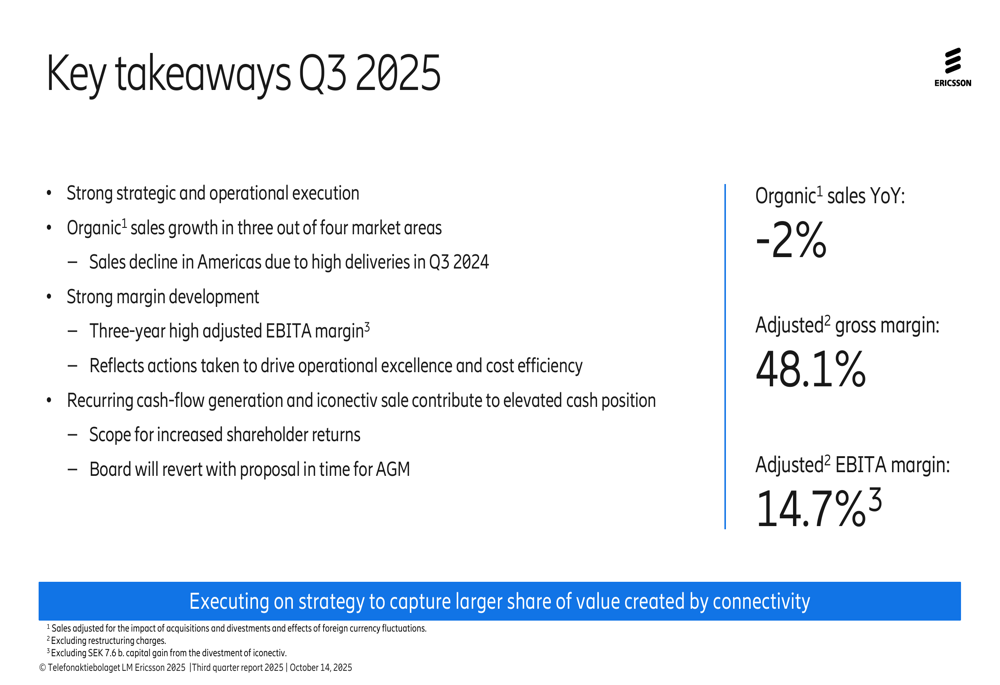

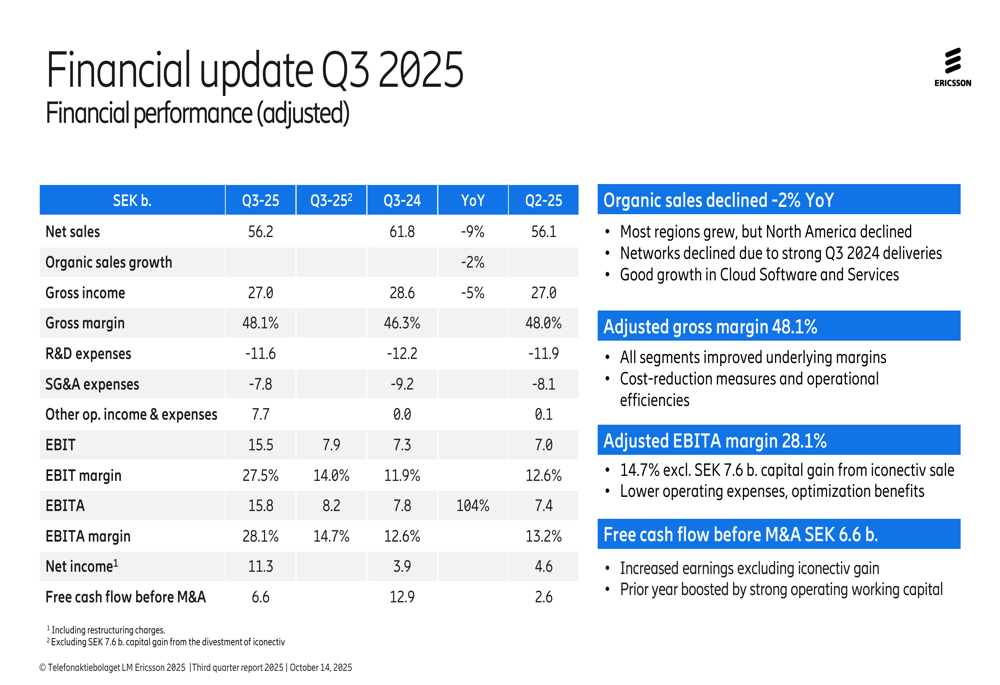

Ericsson’s third quarter showed mixed results, with the company achieving strong margin development despite sales challenges. The company reported net sales of SEK 56.2 billion, representing a 9% year-over-year decline, though organic sales (adjusted for currency effects) declined by a more modest 2%.

The adjusted gross margin improved to 48.1%, up from 46.3% in the same quarter last year, reflecting the company’s continued focus on operational efficiency and cost management. Notably, the adjusted EBITA margin reached 14.7%, representing a three-year high when excluding the capital gain from the iconectiv divestment.

As shown in the following key takeaways slide:

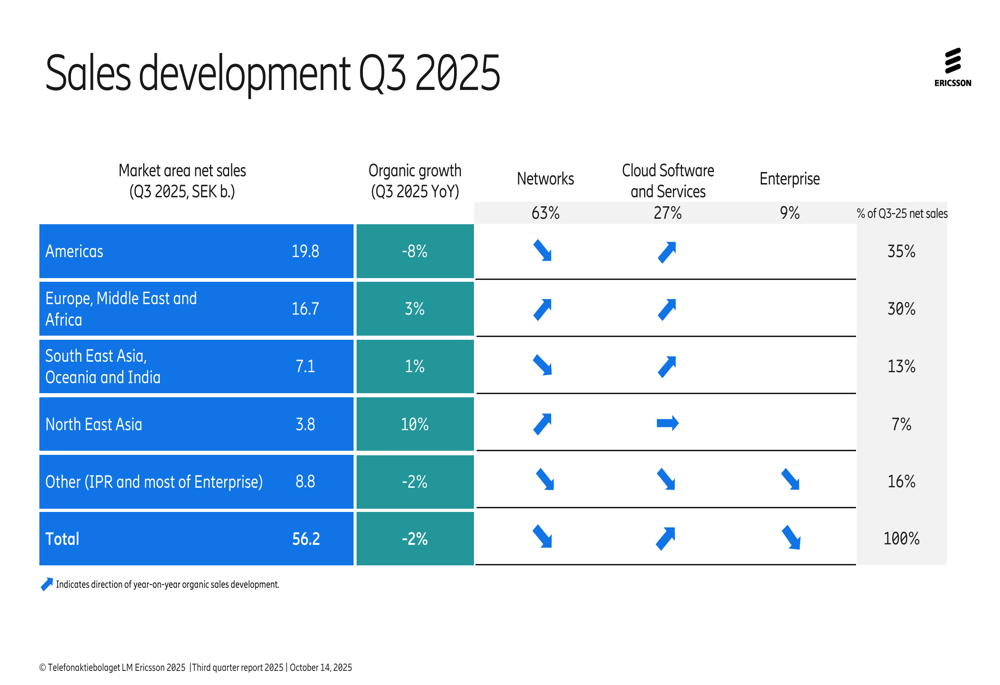

The company’s performance varied significantly across regions, with three out of four market areas showing organic growth. North East Asia led with 10% growth, while Europe, Middle East and Africa grew by 3%, and South East Asia, Oceania and India increased by 1%. However, the Americas region, which represents 35% of Ericsson’s net sales, declined by 8% year-over-year.

The following regional breakdown illustrates these disparities:

Detailed Financial Analysis

Ericsson’s financial results show the impact of both operational improvements and strategic divestments. The company reported EBIT of SEK 15.5 billion, representing a margin of 27.5%, though this includes the SEK 7.6 billion capital gain from the iconectiv sale. Excluding this one-time gain, the adjusted EBITA margin was 14.7%, still showing improvement over previous quarters.

The company’s comprehensive financial data reveals the following performance metrics:

The financial improvements came despite currency headwinds and challenging market conditions in some regions. Ericsson attributed the margin gains to cost-reduction measures, operational efficiencies, and improved delivery performance, continuing the positive trend seen in the previous quarter when the company reported a 48% gross margin.

Segment Performance Analysis

Ericsson’s three main business segments showed varying performance in Q3 2025:

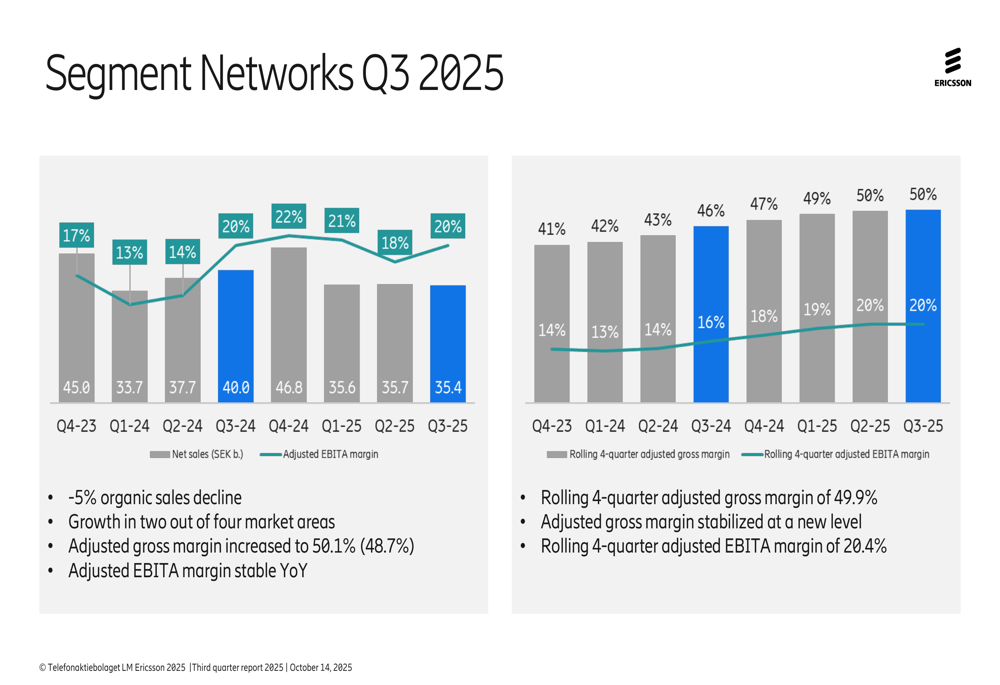

The Networks segment, which represents 63% of net sales, experienced a 5% organic sales decline, though it maintained a stable adjusted EBITA margin year-over-year at 20.3%. The segment’s gross margin improved to 50.1% from 48.7% in the same period last year, reflecting the benefits of cost actions and operational efficiency.

The following chart illustrates the Networks segment performance:

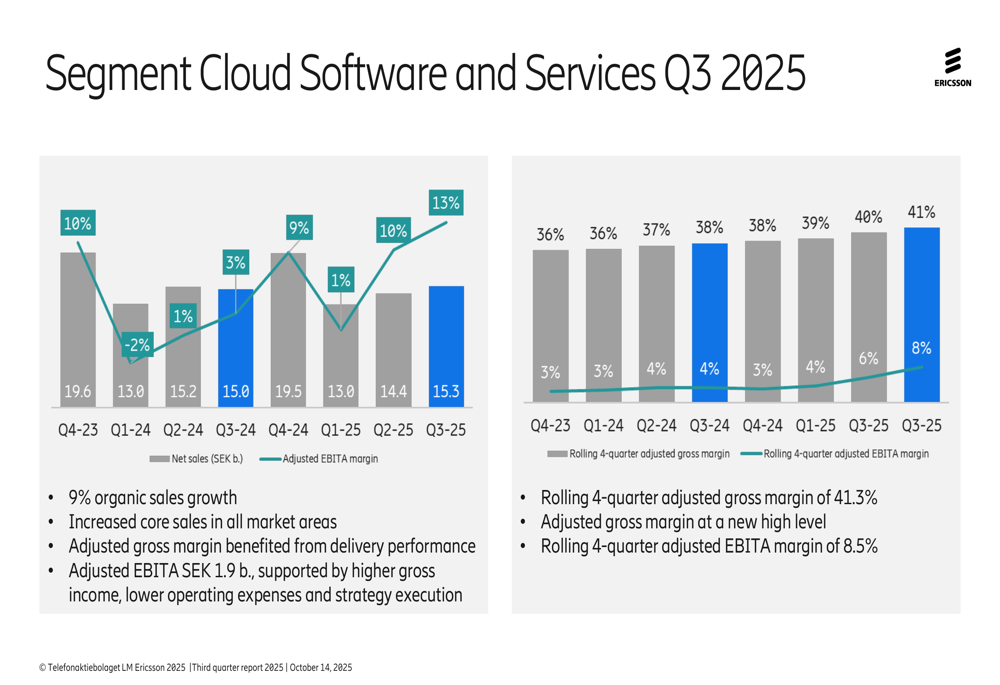

In contrast, the Cloud Software and Services segment, accounting for 27% of sales, delivered strong 9% organic growth with increased core sales across all market areas. This segment’s adjusted EBITA reached SEK 1.9 billion, with the margin improving significantly to 12.5%, up 9.6 percentage points year-over-year.

The segment’s performance is detailed in this chart:

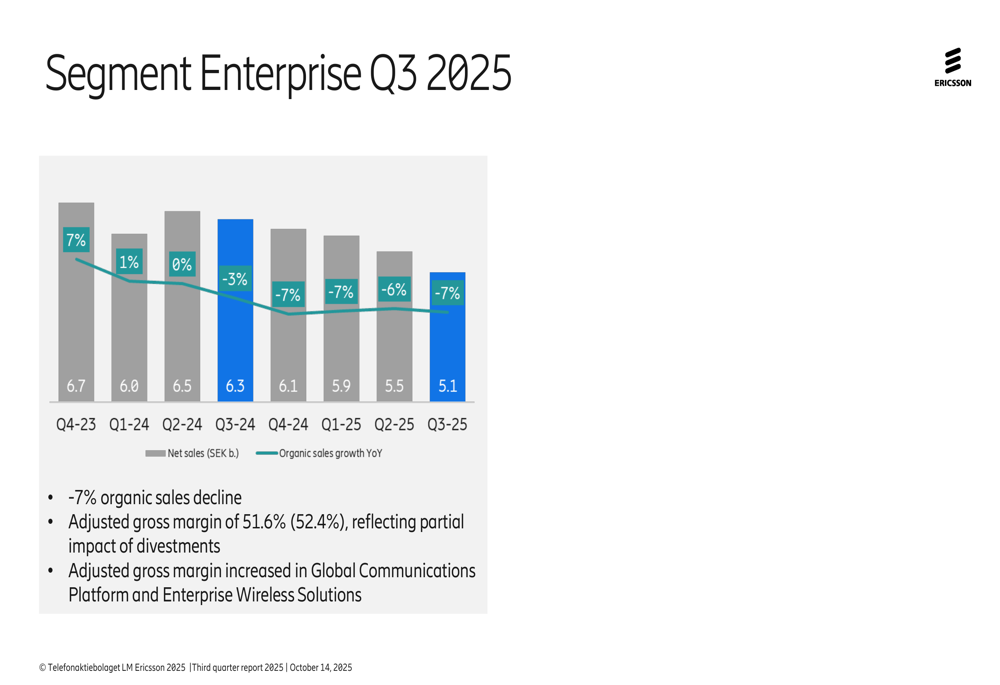

The Enterprise segment, representing 9% of sales, faced challenges with a 7% organic sales decline. However, its adjusted gross margin remained robust at 51.6%, though slightly down from 52.4% in Q3 2024. This segment’s results were partially impacted by recent divestments.

Cash Position and Capital Allocation

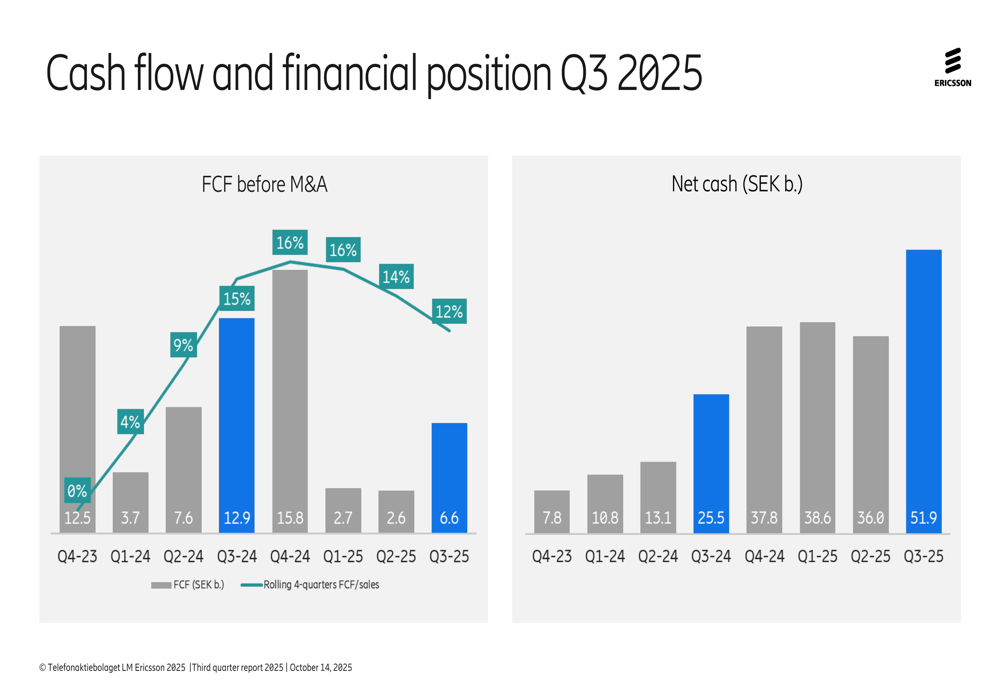

Ericsson significantly strengthened its financial position during the quarter, with free cash flow before M&A reaching SEK 6.6 billion. While this represents a decrease from the SEK 12.9 billion generated in Q3 2024, it shows improvement from the SEK 2.6 billion in Q2 2025.

The company’s net cash position surged to SEK 51.9 billion, up from SEK 36.0 billion in the previous quarter, largely due to the proceeds from the iconectiv sale. This substantial cash reserve has prompted the company to indicate potential for increased shareholder returns, with the board expected to make a proposal in time for the Annual General Meeting.

The following chart shows the evolution of Ericsson’s cash position:

Outlook and Forward Guidance

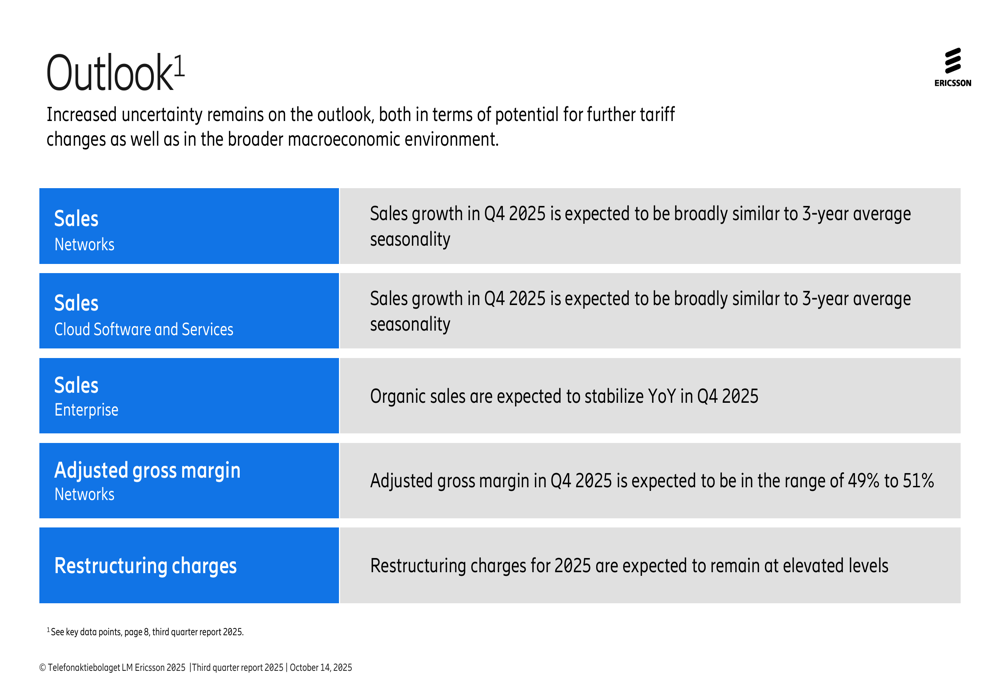

Looking ahead, Ericsson provided a cautiously optimistic outlook for the remainder of 2025, while acknowledging increased uncertainty due to potential tariff changes and the broader macroeconomic environment.

For Q4 2025, the company expects sales growth to be broadly similar to the 3-year average seasonality for both Networks and Cloud Software and Services segments. The Enterprise segment is anticipated to stabilize year-over-year in the fourth quarter. Ericsson also projects adjusted gross margin in Q4 2025 to range between 49% and 51%.

The company’s detailed outlook is presented here:

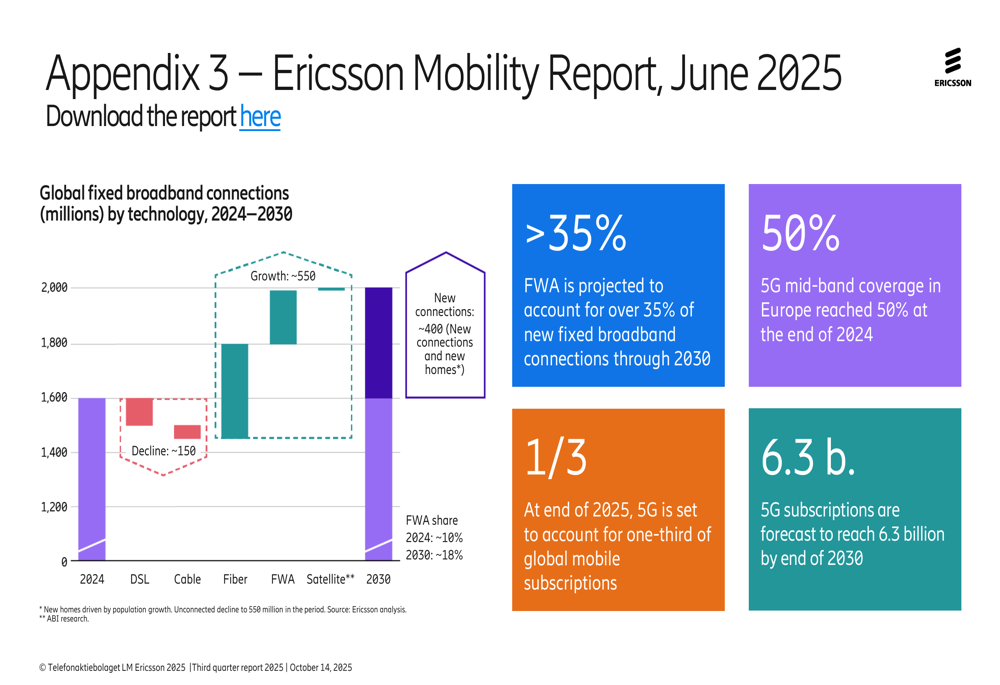

Ericsson also highlighted longer-term industry trends from its Mobility Report, projecting that Fixed Wireless Access (FWA) will account for over 35% of new fixed broadband connections through 2030. The company expects 5G subscriptions to reach 6.3 billion by the end of 2030, underscoring the continued growth potential in the telecommunications infrastructure market.

In summary, Ericsson’s Q3 2025 results demonstrate the company’s ability to improve profitability despite sales challenges, with the iconectiv divestment significantly strengthening its financial position. While regional performance varies and market uncertainties persist, the company’s focus on operational efficiency and cost management continues to yield margin improvements, positioning it to potentially increase shareholder returns in the near future.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.