Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

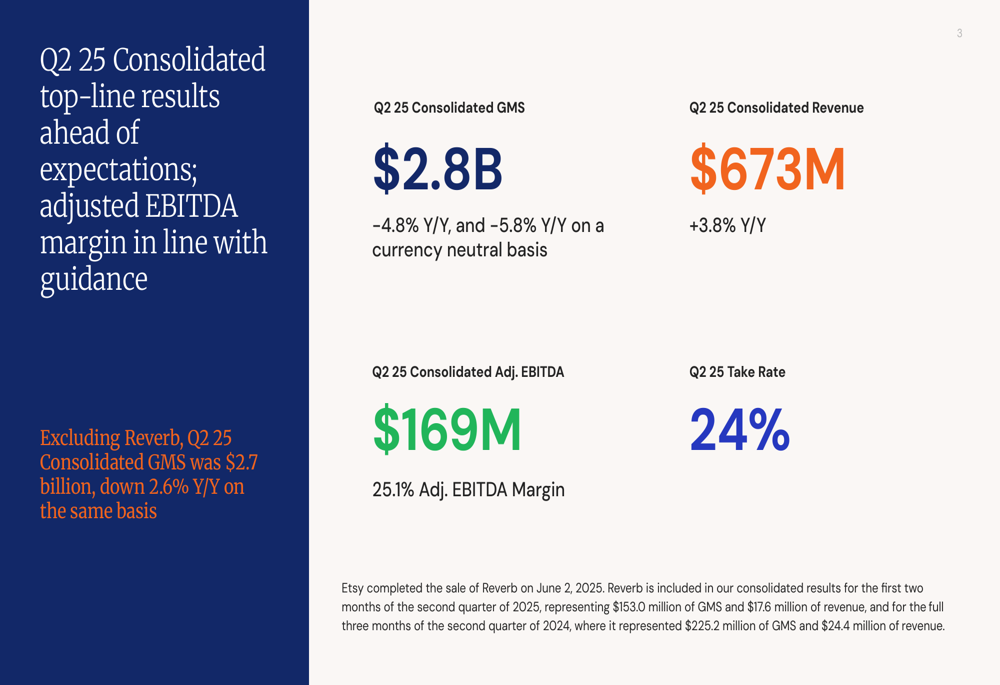

Etsy Inc (NASDAQ:ETSY) presented its second quarter 2025 financial results on July 30, revealing a company navigating challenges in gross merchandise sales (GMS) while successfully growing revenue through improved monetization. The e-commerce platform, known for handcrafted and unique items, reported consolidated revenue growth of 3.8% year-over-year to $673 million, despite a 4.8% decline in GMS to $2.8 billion.

Following the earnings release, Etsy’s stock increased 2.19% during regular trading hours, closing at $70.41, though it retreated 2.14% in aftermarket trading to $68.90. According to available data, the stock is currently trading below its 52-week high of $76.52, with a 52-week low of $40.05.

Quarterly Performance Highlights

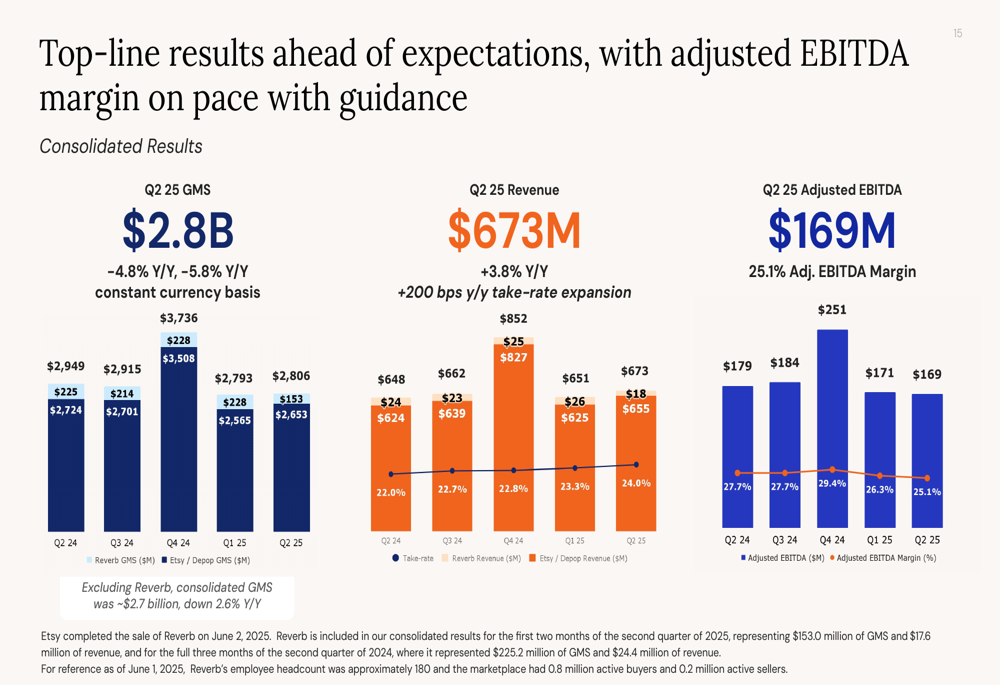

Etsy’s Q2 2025 results showed mixed performance across key metrics. While GMS declined, the company maintained strong profitability with a consolidated adjusted EBITDA of $169 million, representing a 25.1% margin. The company’s take rate reached 24%, exceeding expectations and serving as a primary driver of revenue growth despite the GMS decline.

As shown in the following consolidated financial highlights chart:

The quarter also marked a significant portfolio change with Etsy completing the sale of Reverb on June 2, 2025. Reverb contributed $153.0 million of GMS and $17.6 million of revenue for the first two months of Q2 2025, compared to $225.2 million of GMS and $24.4 million of revenue for the full three months of Q2 2024.

Looking at individual marketplace performance, Etsy’s core marketplace GMS was $2.4 billion, down 5.4% year-over-year, while Depop showed impressive growth with GMS of $250 million, up 35.3% year-over-year. The company attributed Depop’s strong performance to growth in app download share, new buyer and active seller growth, and improved search and recommendation relevance.

The following chart illustrates the top-line results with adjusted EBITDA margin:

Strategic Initiatives

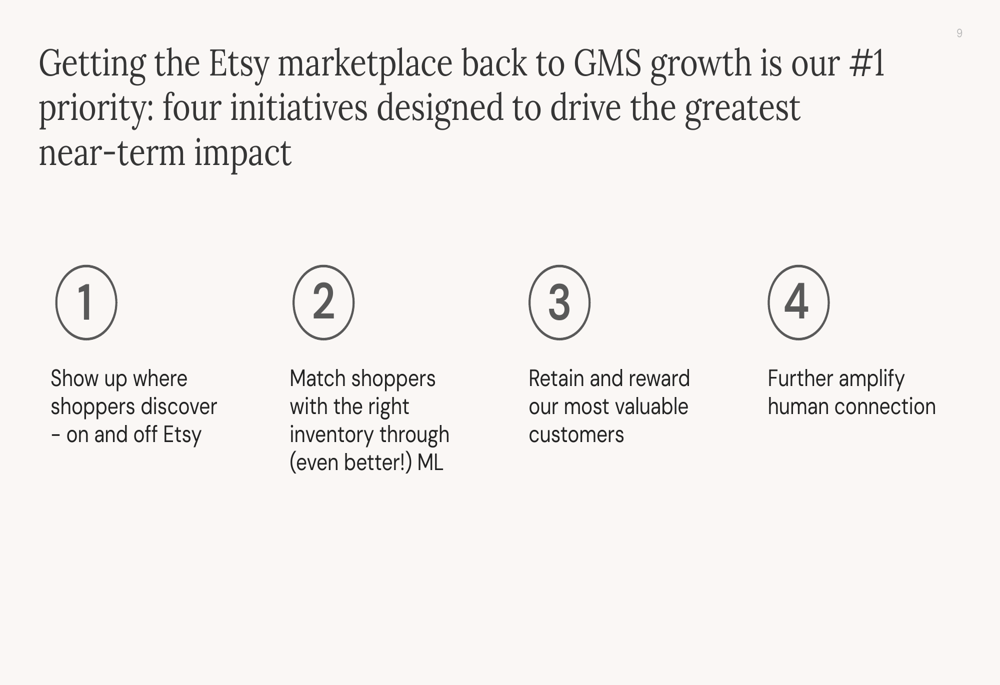

Etsy outlined four key initiatives designed to drive GMS growth: enhancing discovery both on and off the platform, improving matching of shoppers with inventory through machine learning, retaining and rewarding valuable customers, and amplifying human connection.

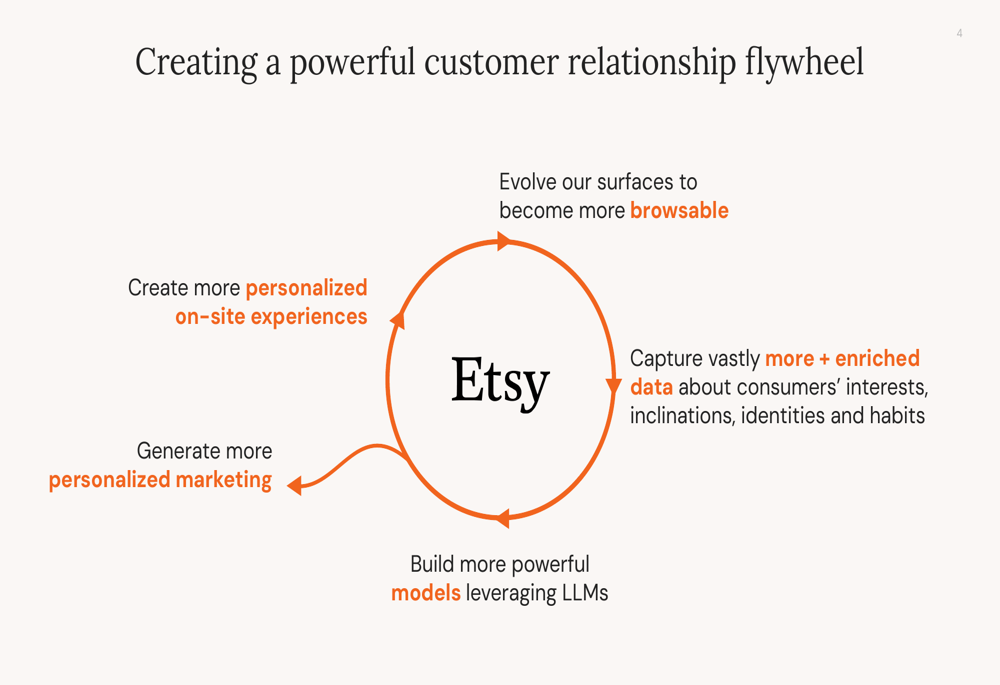

A significant focus of Etsy’s strategy is leveraging artificial intelligence and machine learning to create more personalized experiences. The company reported being identified as a top retail e-commerce recipient of agentic chatbot traffic and highlighted its integration with Apple’s Visual Intelligence for seamless product discovery.

The company’s customer relationship flywheel illustrates how Etsy plans to leverage data and AI to create more personalized experiences:

Etsy is also seeing positive results from its app investments, with app GMS growing year-over-year and representing approximately 45% of total GMS in Q2. Monthly active users increased 7% year-over-year, and app downloads were up compared to the previous year.

In search and recommendations, Etsy is implementing new ranking models using LLMs and generative AI to better understand listings, users, and their activity. This approach is already showing results at Depop, where there has been a 2x increase in the share of products bought from recommendations since late 2022.

The following chart illustrates Etsy’s approach to matching shoppers with inventory through machine learning:

Detailed Financial Analysis

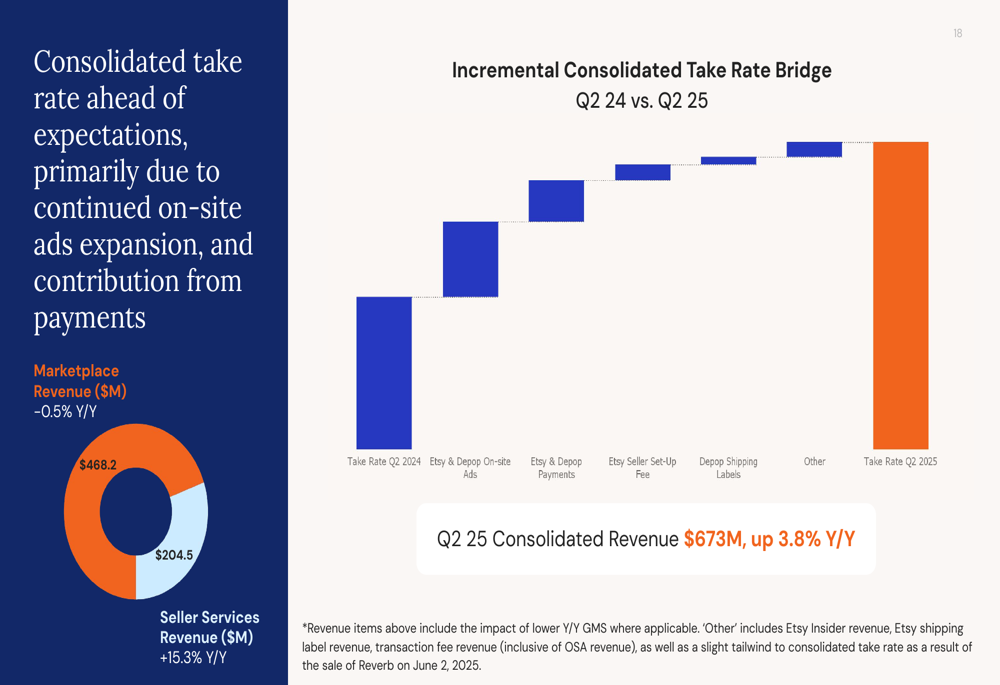

Etsy’s consolidated take rate improvement was a key driver of revenue growth, primarily due to continued on-site ads expansion and contribution from payments. While marketplace revenue decreased slightly by 0.5% year-over-year, seller services revenue grew significantly by 15.3%.

The take rate bridge from Q2 2024 to Q2 2025 shows the various components contributing to the improvement:

On the marketing front, Etsy increased its consolidated marketing spend as a percentage of revenue, with a particular focus on performance marketing and paid social. The company is shifting its brand media approach from linear TV to streaming platforms and accelerating social investment on certain platforms.

Etsy maintains strong financial flexibility with a cash balance of approximately $1.5 billion. During Q2 2025, the company repurchased approximately $335 million in shares and generated $90 million in consolidated free cash flow.

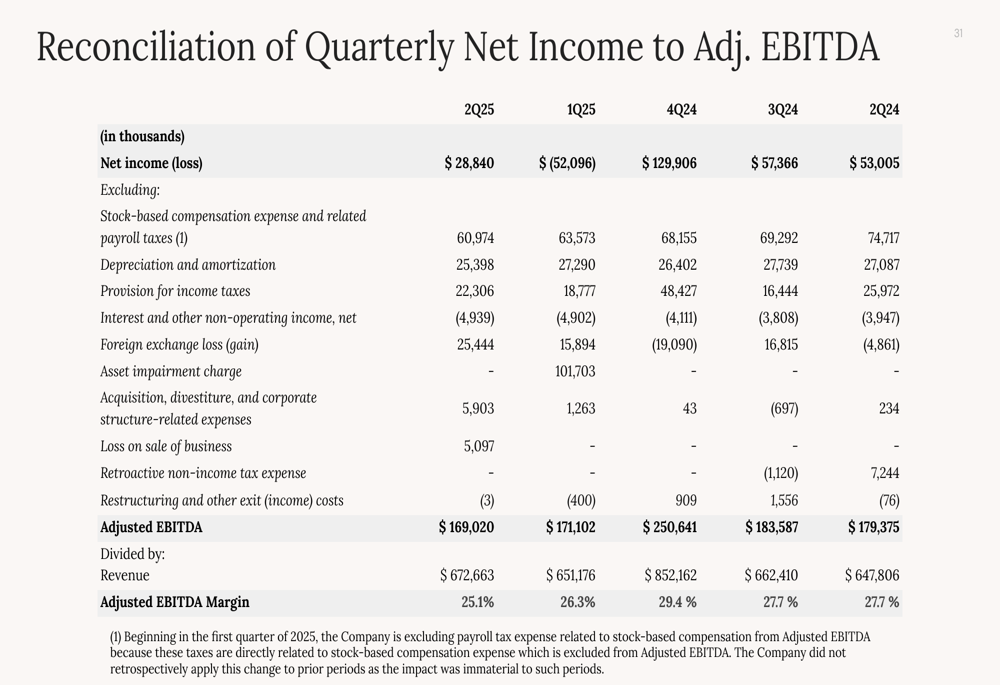

The reconciliation of net income to adjusted EBITDA shows the company’s profitability metrics across recent quarters:

Forward-Looking Statements

Looking ahead to Q3 2025, Etsy provided guidance for GMS between $2.6 billion and $2.7 billion, which at the midpoint would represent further quarter-over-quarter improvement in the comparable growth rate. The company expects a take rate of approximately 24.5% and an adjusted EBITDA margin of around 25%.

CEO Josh Silverman expressed optimism about early promising signals that the company’s flywheel is gaining speed. The company’s strategic focus remains on personalization, with a goal of achieving near-total personalization in marketing messages by year-end, up from approximately 40% in Q2 2025.

Etsy’s leadership highlighted four key initiatives that will drive their approach through the remainder of 2025 and beyond:

Etsy faces ongoing challenges in reversing the GMS decline in its core marketplace while continuing to invest in product development, AI capabilities, and marketing. The company’s ability to further improve monetization through take rate optimization while reaccelerating GMS growth will be critical factors for investors to watch in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.