Street Calls of the Week

Introduction & Market Context

Eurocash Group (WSE:EUR) presented its first quarter 2025 results on May 15, 2025, revealing a challenging market environment for Poland’s leading wholesale distributor and retail operator. The company reported a 7.6% year-over-year decline in sales amid broader market headwinds, particularly in the wholesale retail market (WRM) segment, which contracted by 4.1% compared to a milder 1.2% decline in the same period last year.

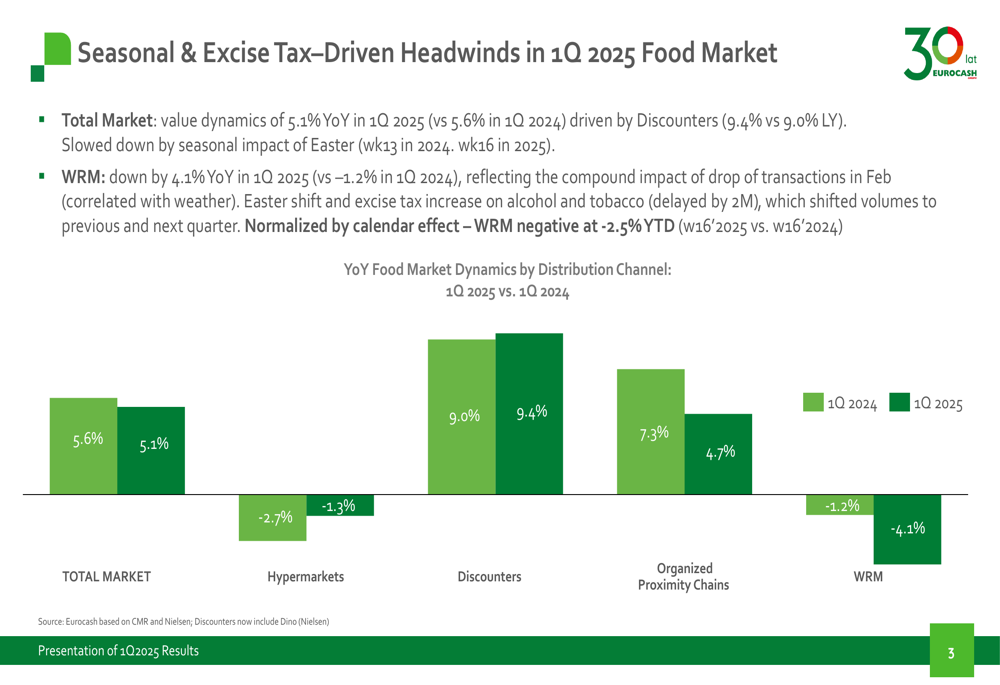

The broader food market in Poland showed value growth of 5.1% year-over-year in Q1 2025, slightly down from 5.6% in Q1 2024. Discounters continued to outperform with 9.4% growth, while organized proximity chains slowed to 4.7% growth from 7.3% a year earlier.

As shown in the following chart of food market dynamics by distribution channel:

Quarterly Performance Highlights

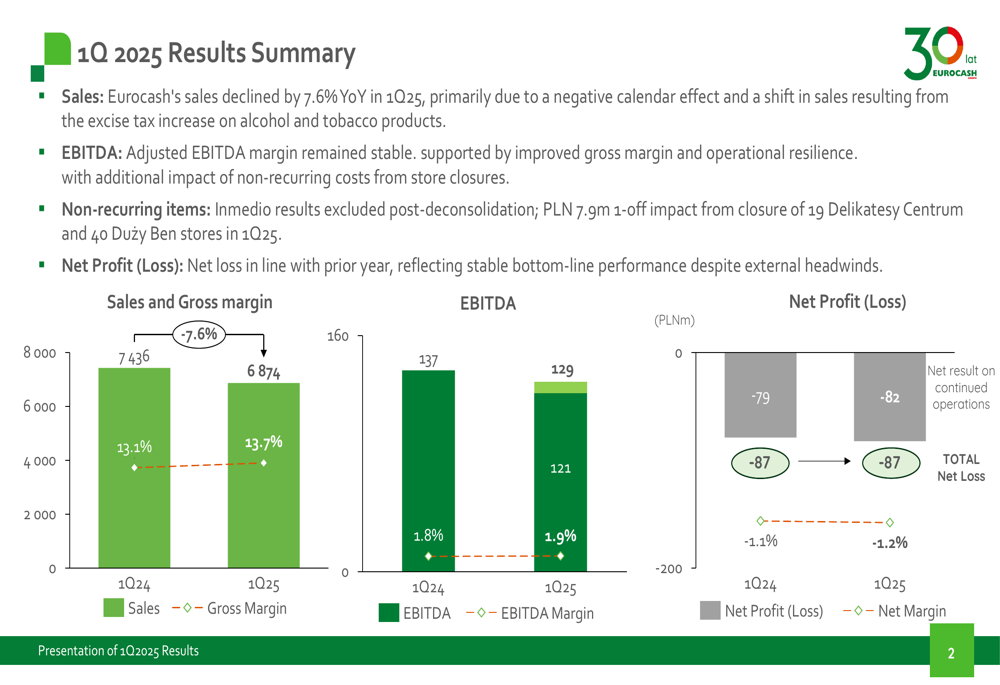

Eurocash reported total sales of 6,874 million PLN in Q1 2025, down 7.6% from 7,436 million PLN in Q1 2024. Despite the revenue decline, the company managed to improve its gross margin from 13.1% to 13.7% year-over-year. EBITDA decreased from 137 million PLN to 129 million PLN, though EBITDA margin slightly increased from 1.8% to 1.9%.

The company’s net loss remained stable at 87 million PLN in both Q1 2024 and Q1 2025, with net margin slightly decreasing from -1.1% to -1.2%. These results reflect Eurocash’s efforts to maintain profitability despite sales pressure.

The following summary chart illustrates the key financial metrics for Q1 2025:

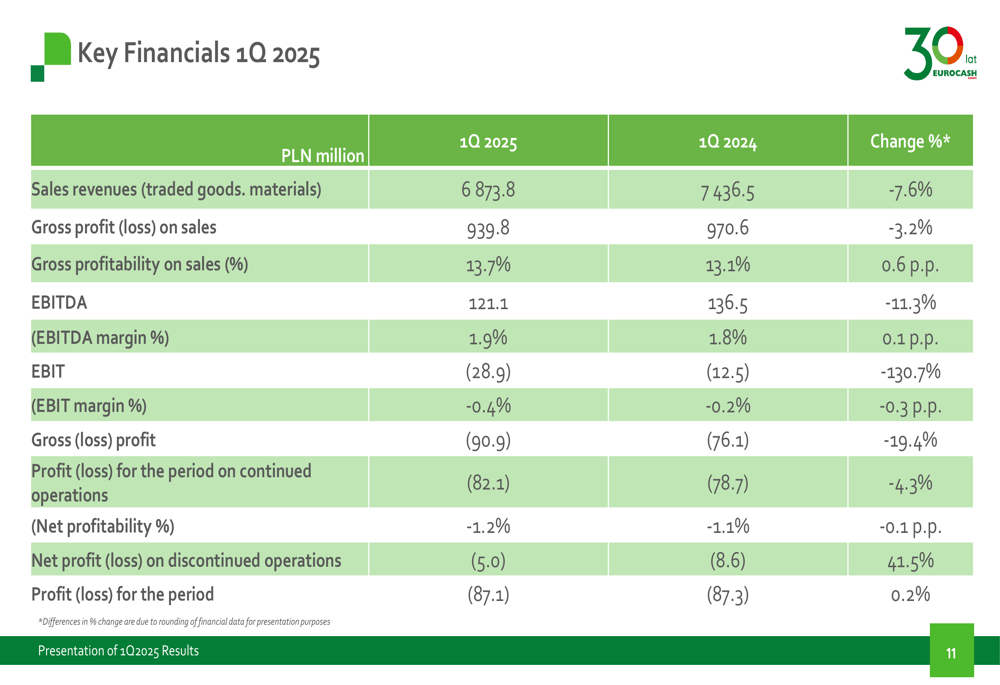

A more detailed breakdown of the financial performance is presented in this comprehensive table:

Segment Performance Analysis

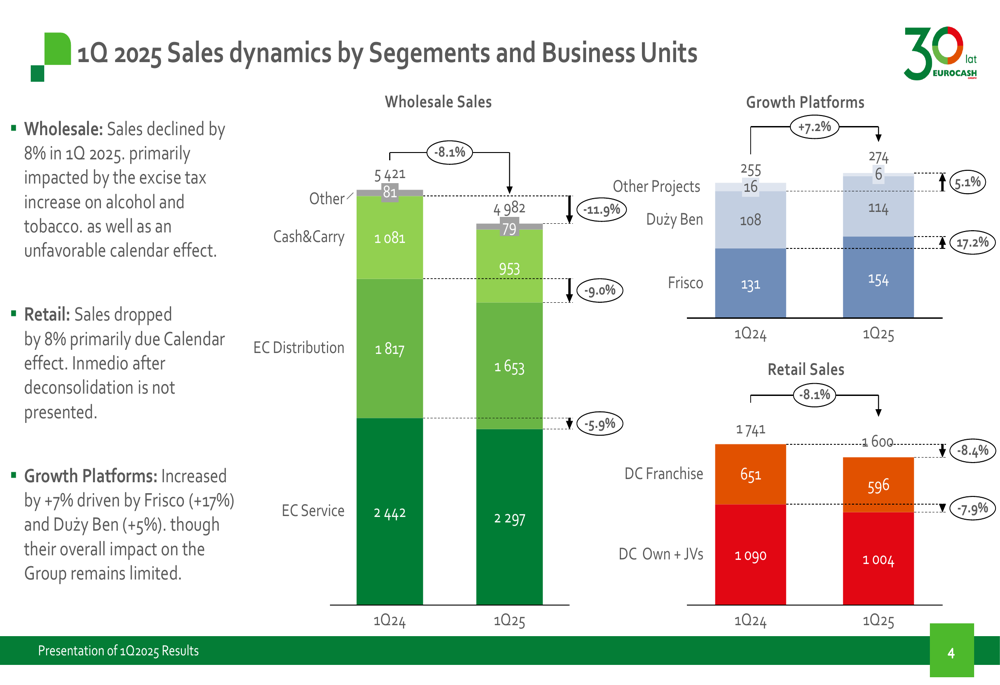

Eurocash’s wholesale segment, which represents the largest portion of the company’s business, experienced an 8% sales decline in Q1 2025. Within this segment, Cash & Carry sales fell from 1,081 million PLN to 953 million PLN, while EC Distribution decreased from 1,817 million PLN to 1,653 million PLN.

The retail segment also saw an 8% sales drop, which the company attributed primarily to calendar effects. Delikatesy Centrum franchise sales declined from 651 million PLN to 596 million PLN, while company-owned stores and joint ventures saw sales decrease from 1,090 million PLN to 1,004 million PLN.

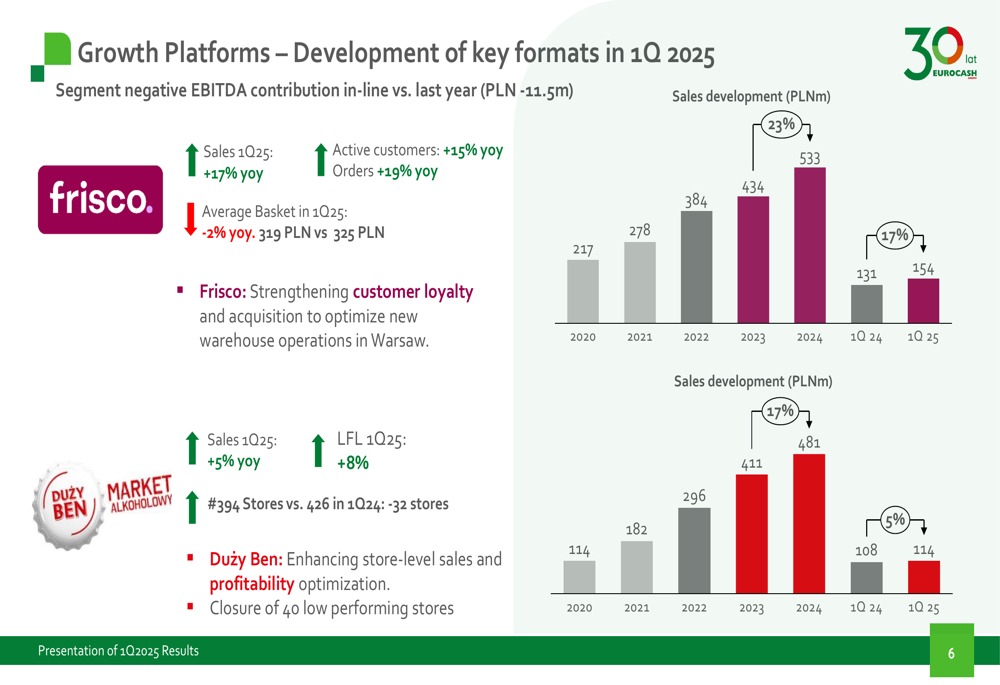

In contrast, Eurocash’s growth platforms increased by 7%, driven by strong performance from online grocery retailer Frisco (+17%) and alcohol chain Duży Ben (+5%).

The following chart details the sales dynamics across different segments:

EBITDA performance varied across segments, with wholesale EBITDA decreasing from 144 million PLN to 125 million PLN, and retail EBITDA declining from 47 million PLN to 37 million PLN. The EBITDA margin in wholesale fell slightly by 0.2 percentage points to 2.5%, while retail saw a 0.4 percentage point decrease to 2.3%.

Strategic Initiatives

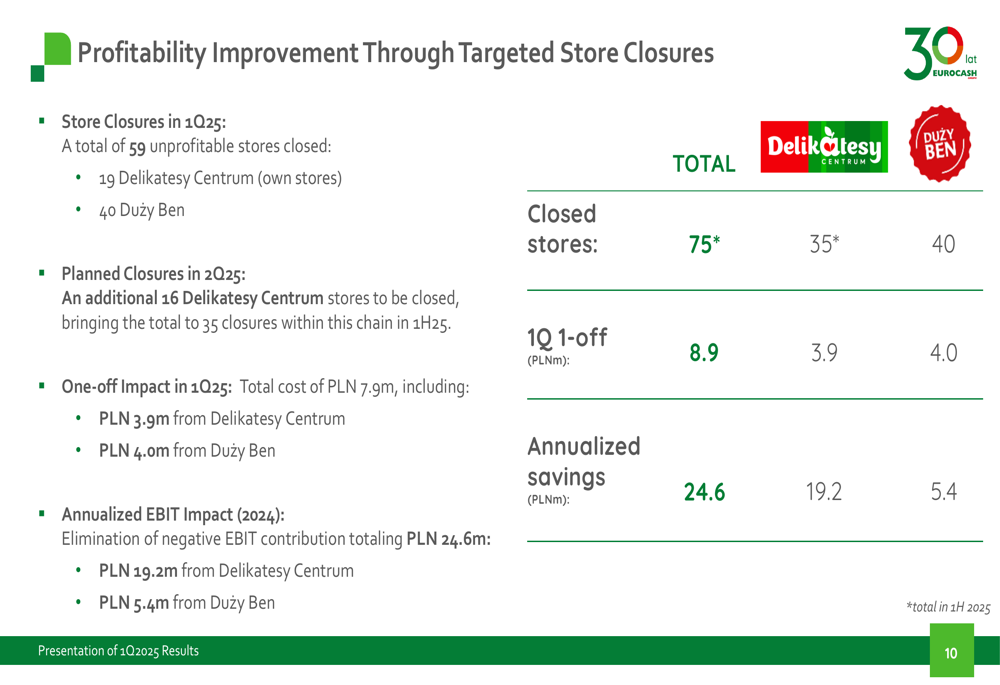

In response to challenging market conditions, Eurocash has implemented a strategic store closure program aimed at improving profitability. During Q1 2025, the company closed 75 stores, including 35 Delikatesy Centrum locations and 40 Duży Ben stores. An additional 16 Delikatesy Centrum stores are planned for closure in Q2 2025.

These closures resulted in a one-off impact of 8.9 million PLN in Q1 2025, but are expected to generate annualized savings of 24.6 million PLN. The Delikatesy Centrum closures are projected to deliver 19.2 million PLN in annual savings, while the Duży Ben closures should contribute 5.4 million PLN.

The company’s profitability improvement strategy through store closures is detailed in the following chart:

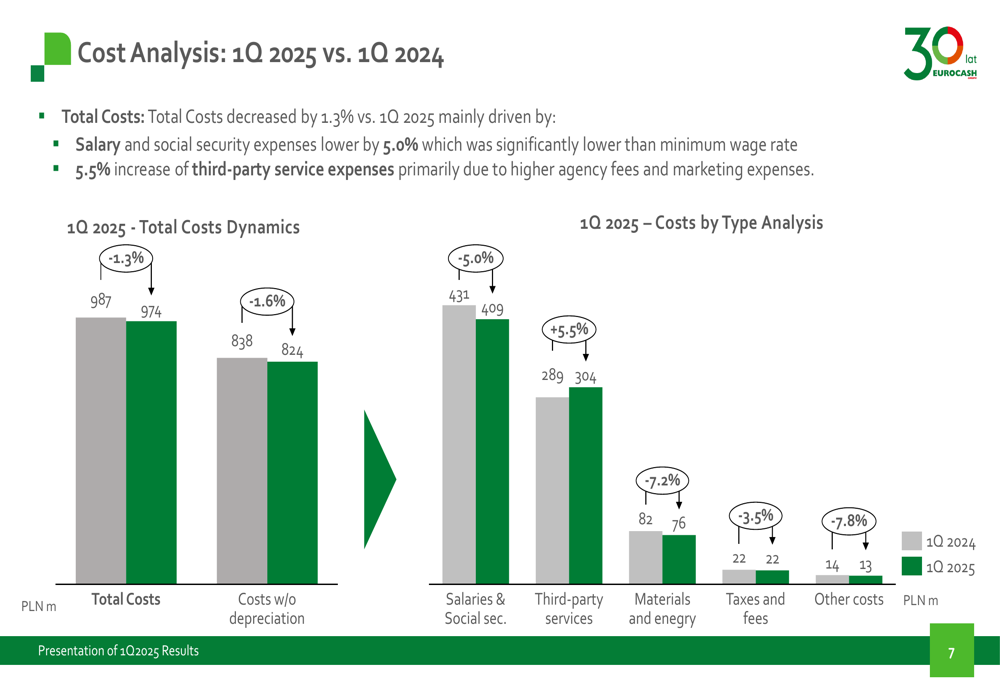

Eurocash has also maintained its focus on cost management, with total costs decreasing by 1.3% year-over-year. Salary and social security expenses decreased by 5.0%, while third-party service expenses increased by 5.5%. The following cost analysis provides further details:

Growth Platforms Performance

Despite challenges in traditional segments, Eurocash’s growth platforms showed promising results. Frisco, the company’s online grocery business, delivered 17% year-over-year sales growth in Q1 2025, with a 15% increase in active customers and 19% growth in orders. The average basket size decreased slightly by 2% to 319 PLN.

Duży Ben, the company’s alcohol retail chain, achieved 5% sales growth and 8% like-for-like growth, despite operating 32 fewer stores compared to Q1 2024 (394 vs. 426). This performance demonstrates improving store economics following the strategic closure of underperforming locations.

The development of these growth platforms is illustrated in the following chart:

Financial Position and Outlook

Eurocash maintained a stable financial position, with its net debt to EBITDA ratio at 1.12 before IFRS16 effects (2.71 after IFRS16). The company’s cash conversion cycle improved by 6 days year-over-year, reflecting enhanced working capital management.

Net financial expenses remained broadly in line with historical patterns, with Q1 2025 net financial expenses at 82 million PLN compared to 79 million PLN in Q1 2024. Financial expenses were 62 million PLN, partially offset by 16 million PLN in financial income.

While Eurocash continues to face market headwinds, particularly in the wholesale segment, its focus on margin improvement, cost management, and strategic store closures demonstrates a disciplined approach to navigating challenging conditions. The growth of digital platforms like Frisco provides a potential avenue for future expansion as consumer shopping habits continue to evolve.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.