Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

Eurocash Group (WSE:EUR) presented its Q2 and 1H 2025 results on August 28, 2025, demonstrating resilience in a challenging market environment. While the company’s wholesale relevant market contracted by 3.5% year-over-year in Q2, Eurocash managed to limit its revenue decline to just 1.2%, showcasing its ability to outperform the broader market.

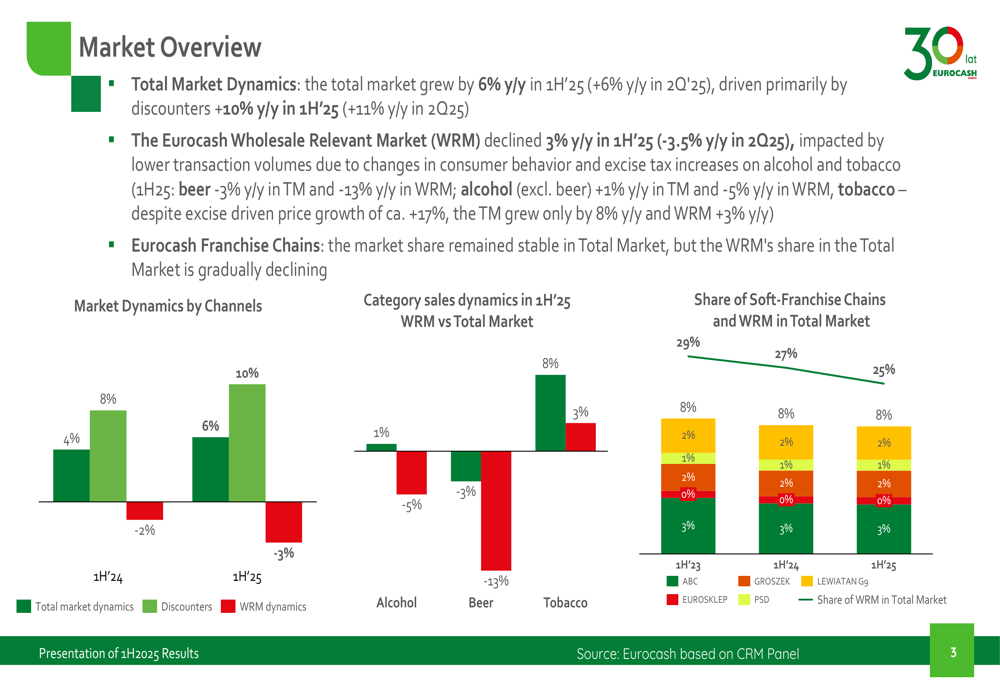

The Polish retail landscape continued to show divergent trends, with the total market growing by 6% year-over-year in 1H 2025, driven primarily by a 10% expansion in the discount channel. Meanwhile, the wholesale relevant market, which represents Eurocash’s core business, declined by 3% during the same period.

As shown in the following market overview chart, this divergence in channel performance has been a consistent trend:

Quarterly Performance Highlights

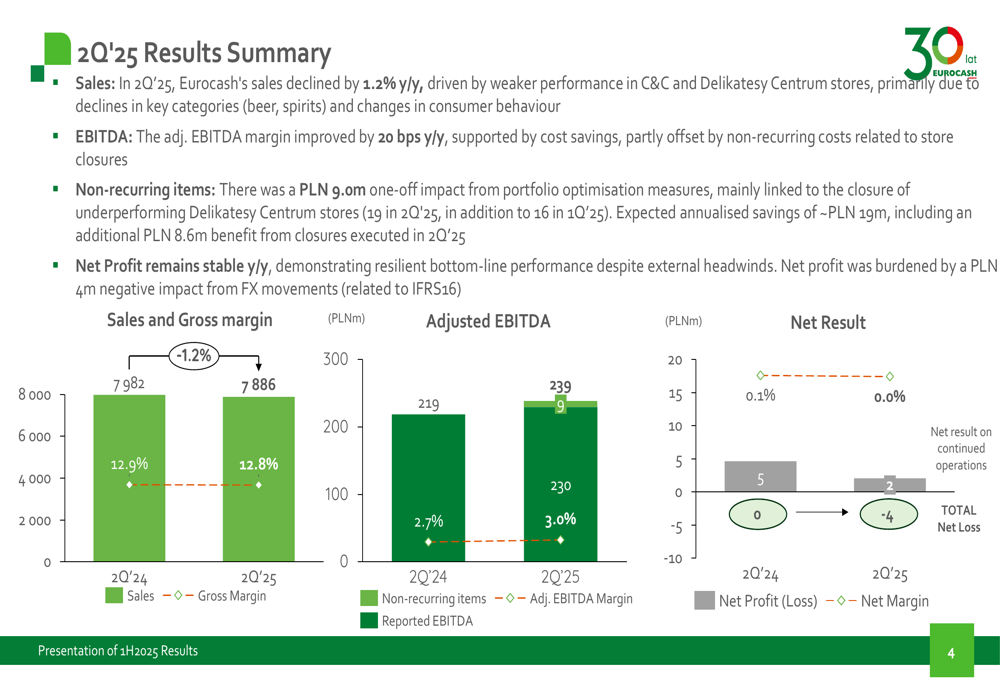

Despite the challenging market conditions, Eurocash delivered notable improvements in profitability during Q2 2025. The company’s EBIT grew by 24% year-over-year to PLN 82 million, while adjusted EBITDA margin expanded to 3.0% from 2.7% in the comparable period last year.

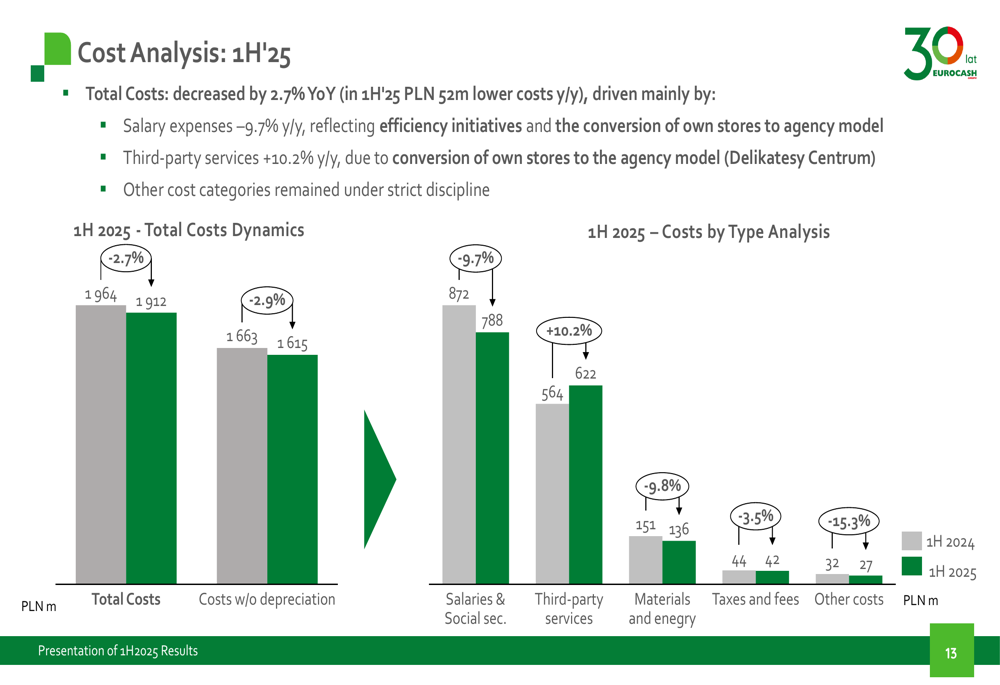

This performance was largely driven by the company’s strong cost discipline, with PLN 52 million in cost savings achieved during the first half of 2025. The company’s franchise store network also demonstrated resilience with positive like-for-like growth of 1.1%.

The following chart illustrates Eurocash’s Q2 2025 financial performance:

Sales declined slightly by 1.2% year-over-year to PLN 7,886 million, while the gross margin remained relatively stable at 12.8%. The adjusted EBITDA increased to PLN 239 million, representing a 9.1% improvement compared to Q2 2024.

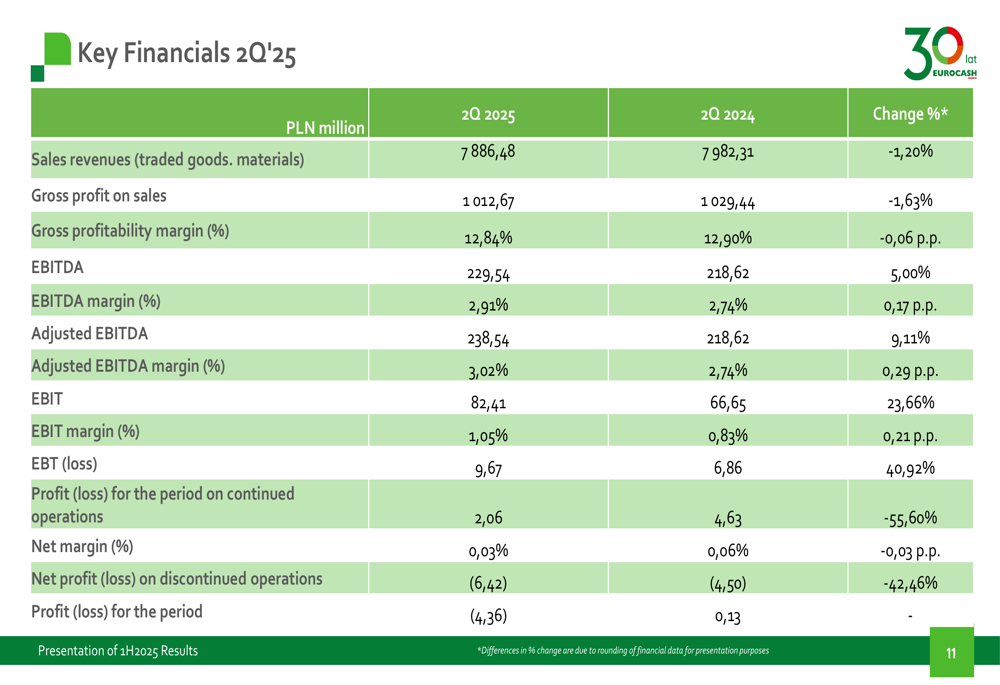

A detailed breakdown of the company’s financial results shows:

Segment Performance Analysis

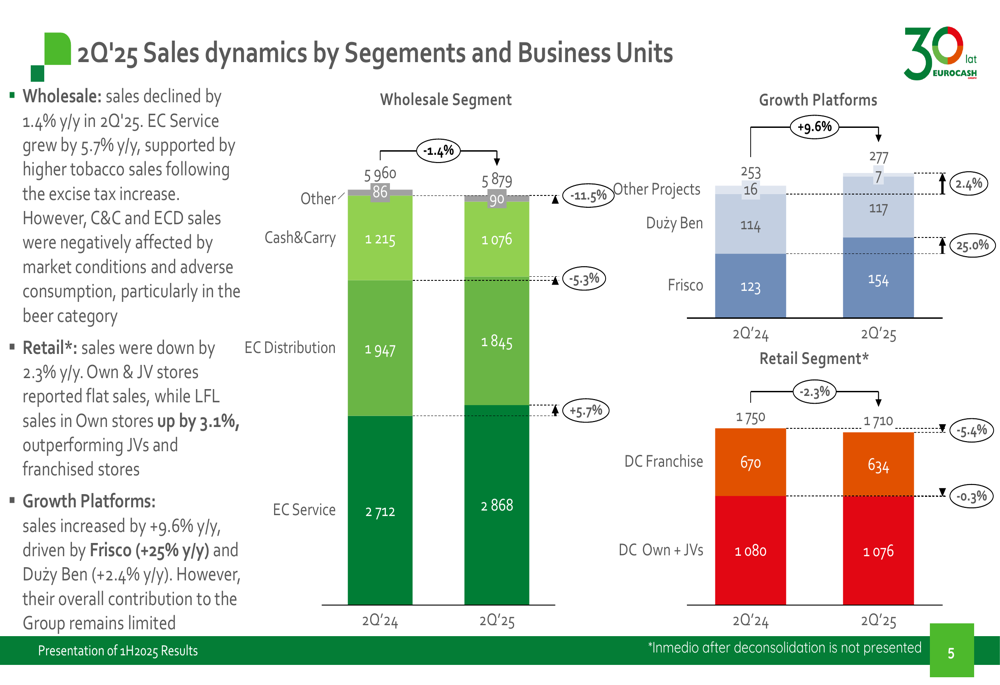

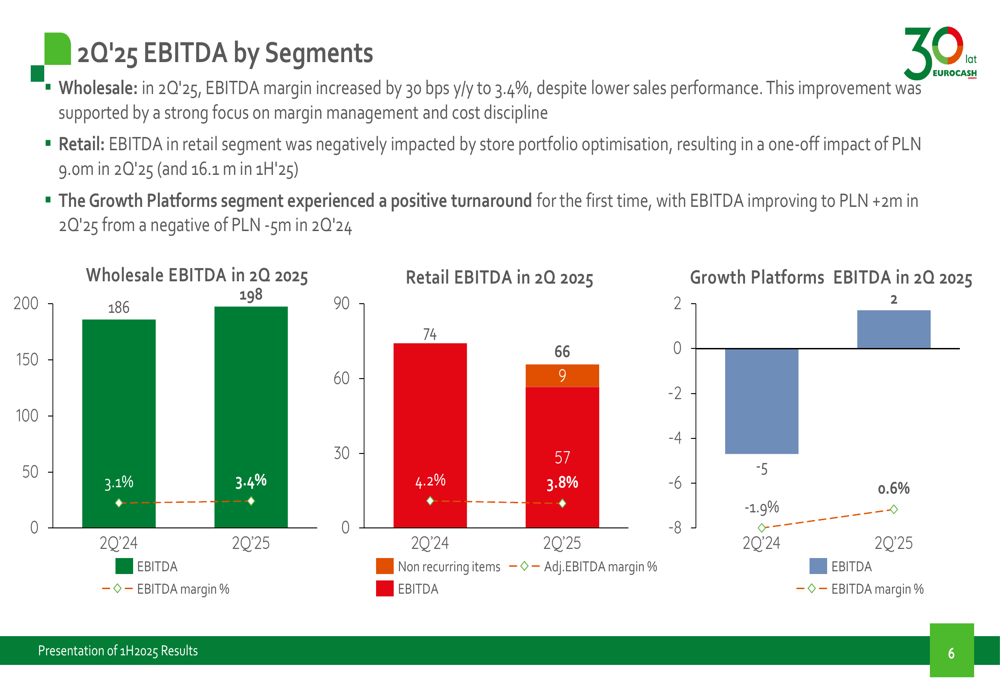

Eurocash’s performance varied across its business segments. The wholesale segment, which represents the largest portion of the company’s business, saw a 1.4% decline in sales but managed to increase its EBITDA margin by 30 basis points to 3.4%.

The retail segment experienced a 2.3% decrease in sales, though like-for-like sales in own stores grew by 3.1%. The segment’s EBITDA was negatively impacted by store portfolio optimization efforts.

The following chart breaks down sales dynamics by segment:

In terms of profitability by segment, the wholesale business continued to be the primary driver of earnings:

Growth Initiatives

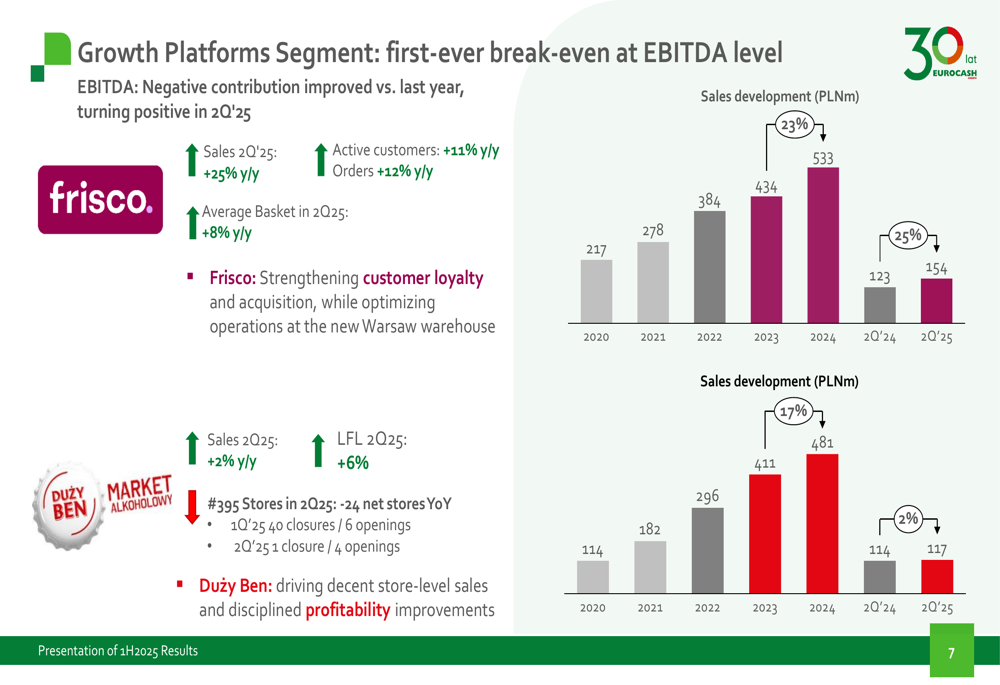

A notable bright spot in Eurocash’s results was the performance of its growth platforms, which include the Frisco e-commerce operation and Duży Ben alcohol stores. These businesses collectively increased sales by 9.6% year-over-year and, importantly, turned EBITDA-positive in Q2 2025.

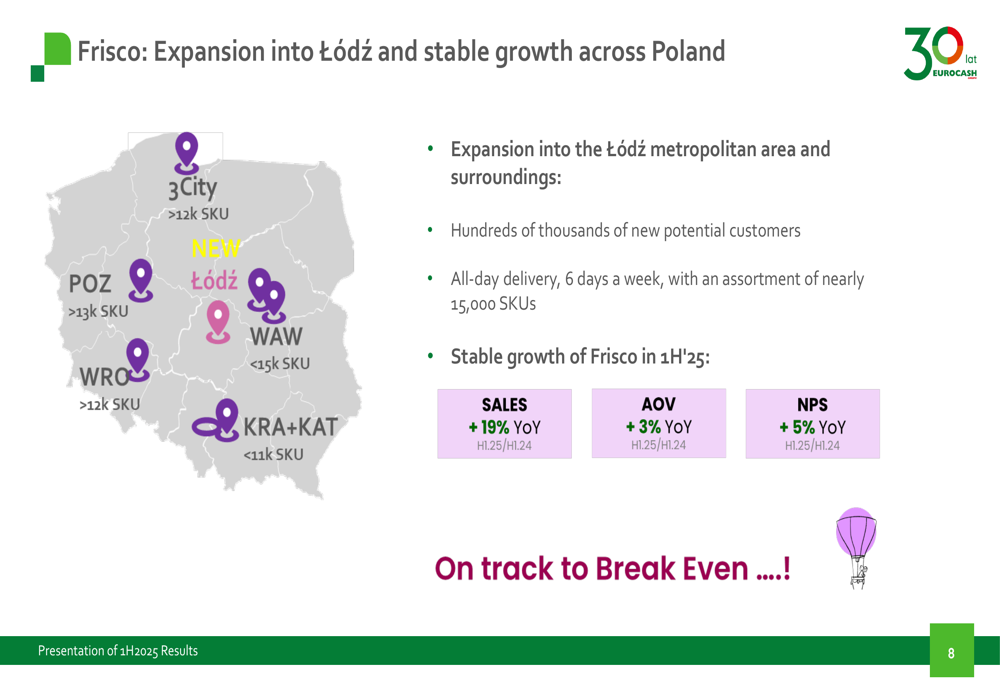

Frisco, the company’s e-commerce platform, delivered particularly strong results with sales growth of 25% year-over-year. The business continued its expansion, recently entering the Łódź metropolitan area, adding hundreds of thousands of potential new customers.

The following chart details the performance of these growth platforms:

Frisco’s expansion into Łódź represents a strategic move to capture additional market share in Poland’s growing e-commerce sector:

Financial Position

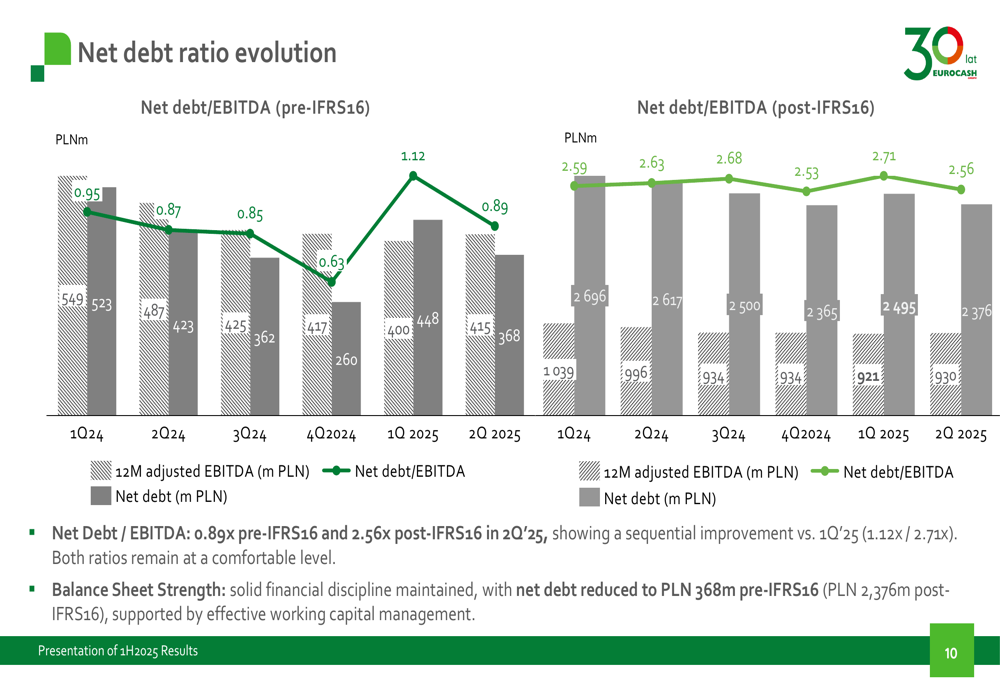

Eurocash maintained a solid financial position, with improvements in its cash conversion cycle and a reduction in net debt. The company’s net debt to EBITDA ratio stood at 0.89x pre-IFRS16 and 2.56x post-IFRS16 in Q2 2025, indicating a stable financial foundation.

The following chart illustrates the evolution of Eurocash’s net debt ratio:

Cost management remained a key focus area, with total costs decreasing by 2.7% year-over-year in the first half of 2025. Particularly significant reductions were achieved in salaries and social security expenses (-9.7%) and materials costs (-9.8%).

Forward-Looking Statements

Looking ahead, Eurocash plans to publish its updated strategy in November 2025, with management suggesting that the sum-of-the-parts value of the business is currently undervalued by the market.

The company continues to strengthen its franchise store loyalty, with the number of soft-franchise stores increasing by 428 compared to year-end 2024. The franchise network maintained a stable share of approximately 8% in the total market while increasing its share in the wholesale relevant market to 31.6% in Q2 2025, up from 28.8% in Q2 2024.

Eurocash’s ability to maintain profitability despite challenging market conditions demonstrates the resilience of its business model and the effectiveness of its cost management initiatives. As the company continues to develop its growth platforms and optimize its store network, it appears well-positioned to navigate the evolving Polish retail landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.