Street Calls of the Week

Introduction & Market Context

EuroGroup Laminations SpA (BIT:EGLA) presented its H1 2025 financial results on August 4, 2025, revealing modest revenue growth amid challenging macroeconomic conditions. The company’s stock traded at €3.58 during the presentation, showing a slight increase of 0.22% on the day, and significantly above its 52-week low of €2.10, indicating investor confidence despite mixed results.

The electrical components manufacturer, which specializes in motor cores for electric vehicles and industrial applications, highlighted its continued expansion in Asian markets while managing through volatility in North America and margin pressures across its business segments.

Executive Summary

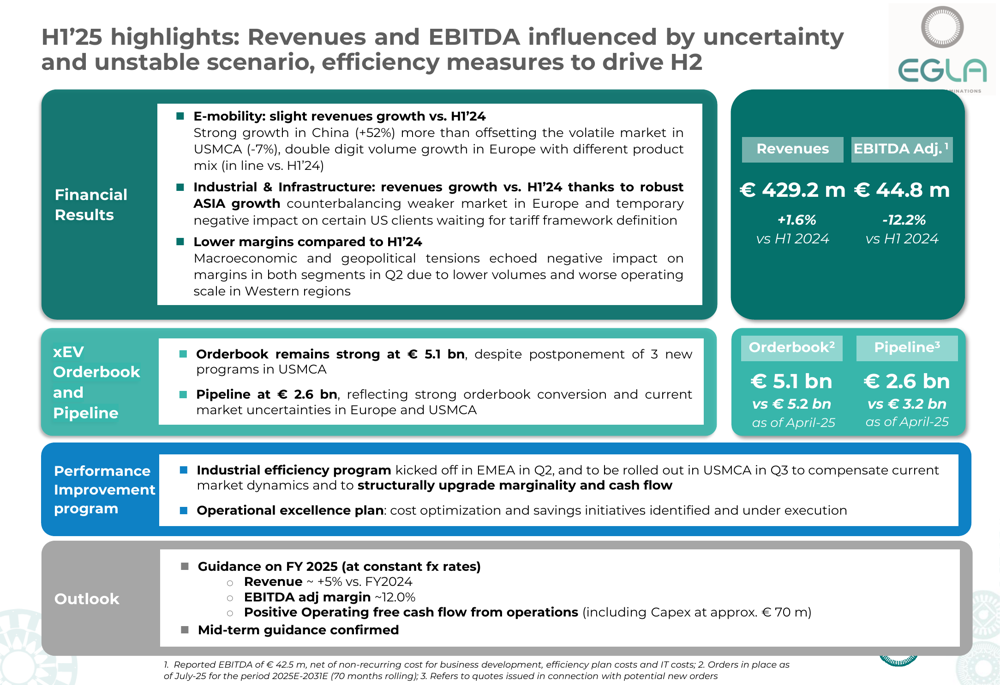

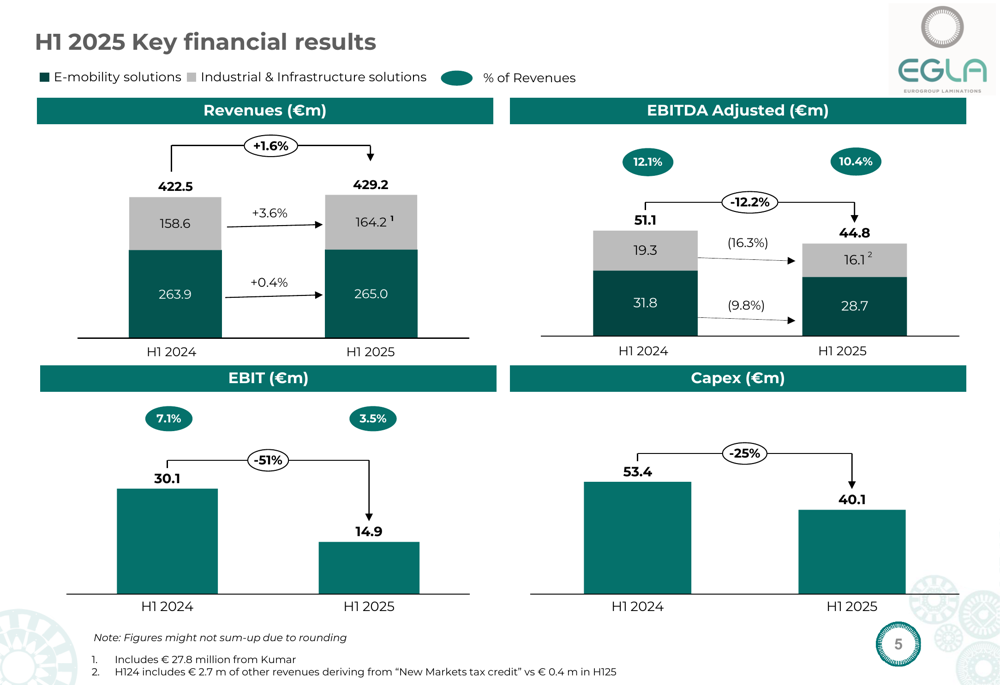

EuroGroup Laminations reported revenues of €429.2 million for H1 2025, representing a modest 1.6% increase compared to H1 2024. However, profitability metrics showed more significant pressure, with adjusted EBITDA declining 12.2% year-over-year to €44.8 million and EBITDA margin contracting to 10.4% from 12.1% in the prior-year period.

As shown in the following summary of key financial metrics:

The company maintained a strong orderbook of €5.1 billion as of April 2025, despite the postponement of three programs in the USMCA region. The pipeline remained robust at €2.6 billion, supporting the company’s growth outlook despite near-term challenges.

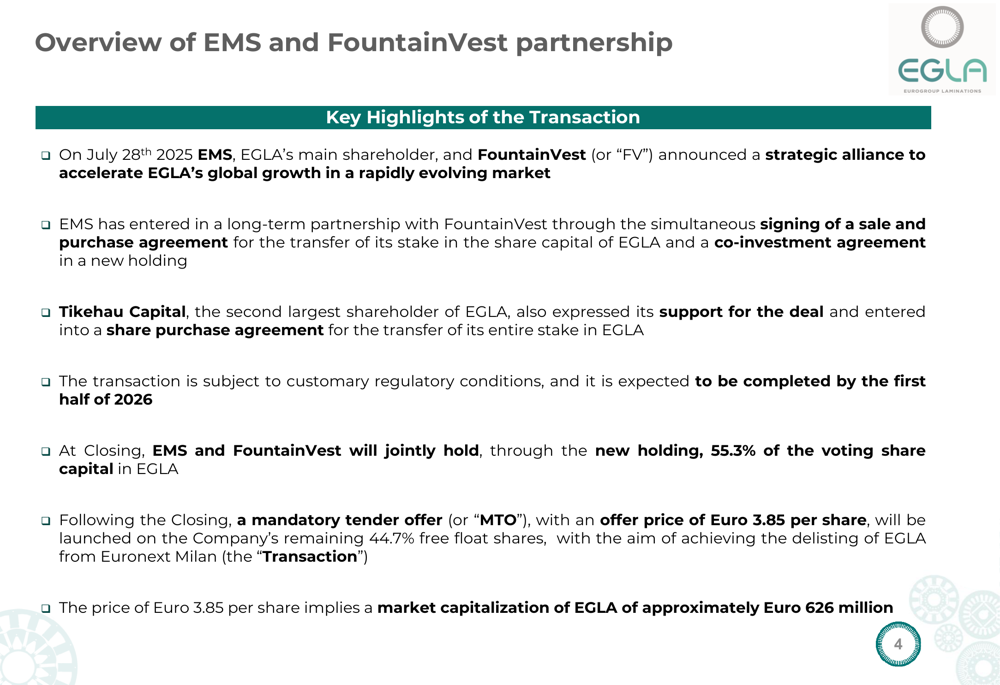

Perhaps the most significant development was the announcement of a strategic partnership with FountainVest, which could lead to the delisting of EuroGroup Laminations from Euronext (EPA:ENX) Milan, as detailed in the presentation:

Quarterly Performance Highlights

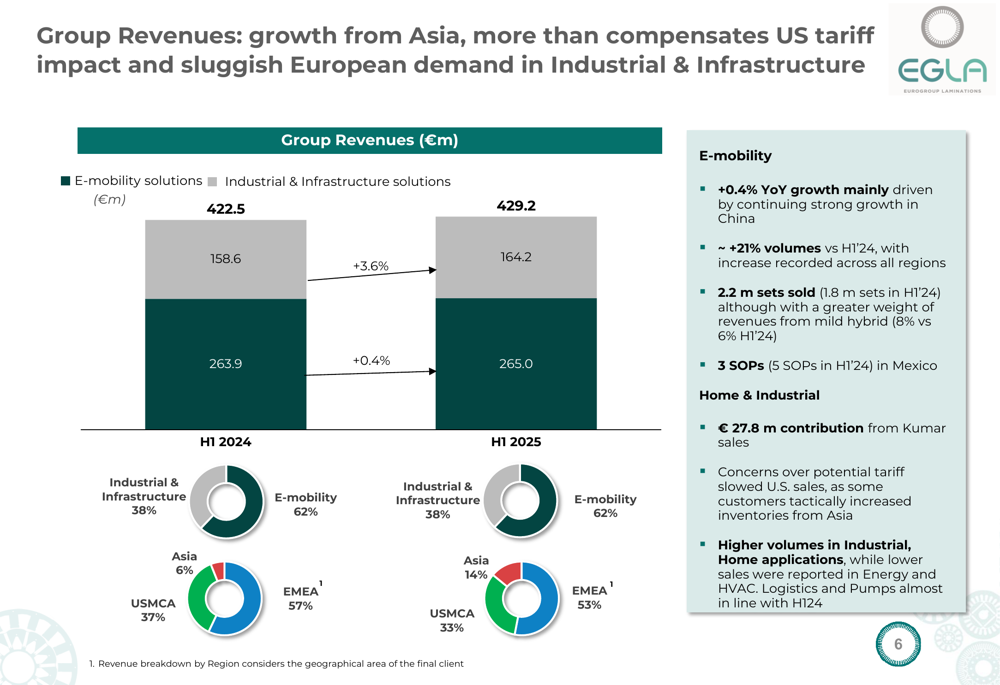

EuroGroup Laminations’ performance showed divergent trends across business segments and geographies. The E-mobility solutions segment posted revenues of €164.2 million, a slight increase from €158.6 million in H1 2024, while Industrial & Infrastructure solutions generated €265.0 million, essentially flat compared to €263.9 million in the prior year.

The detailed breakdown of financial results by segment reveals the pressure on profitability:

Geographically, the company experienced a significant shift in its revenue distribution. Asia’s contribution grew substantially to 14% of total revenue, up from just 6% in H1 2024, driven by exceptional 52% growth in China. Meanwhile, the EMEA region’s share decreased to 53% from 57%, and USMCA declined to 33% from 37%, reflecting the volatility in North American markets.

The following chart illustrates this geographic transformation:

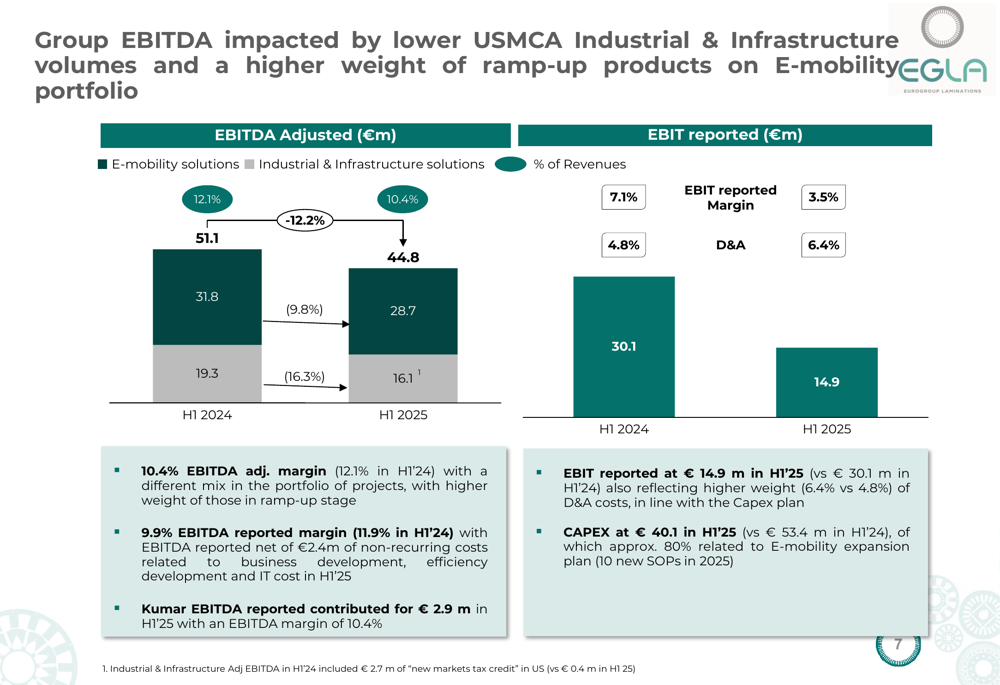

Profitability metrics showed considerable pressure, with EBITDA adjusted declining to €44.8 million from €51.1 million in H1 2024. The company attributed this decrease to lower USMCA Industrial & Infrastructure volumes and a higher proportion of ramp-up products in the E-mobility portfolio, which typically carry lower initial margins.

The EBITDA and EBIT performance is visualized in the following chart:

Strategic Initiatives

In response to margin pressures, EuroGroup Laminations has launched a comprehensive performance improvement program focused on four strategic areas: operational excellence, supplier optimization, supply chain & logistics transformation, and cross-functional governance. This initiative aims to enhance marginality and cash flow in the coming quarters.

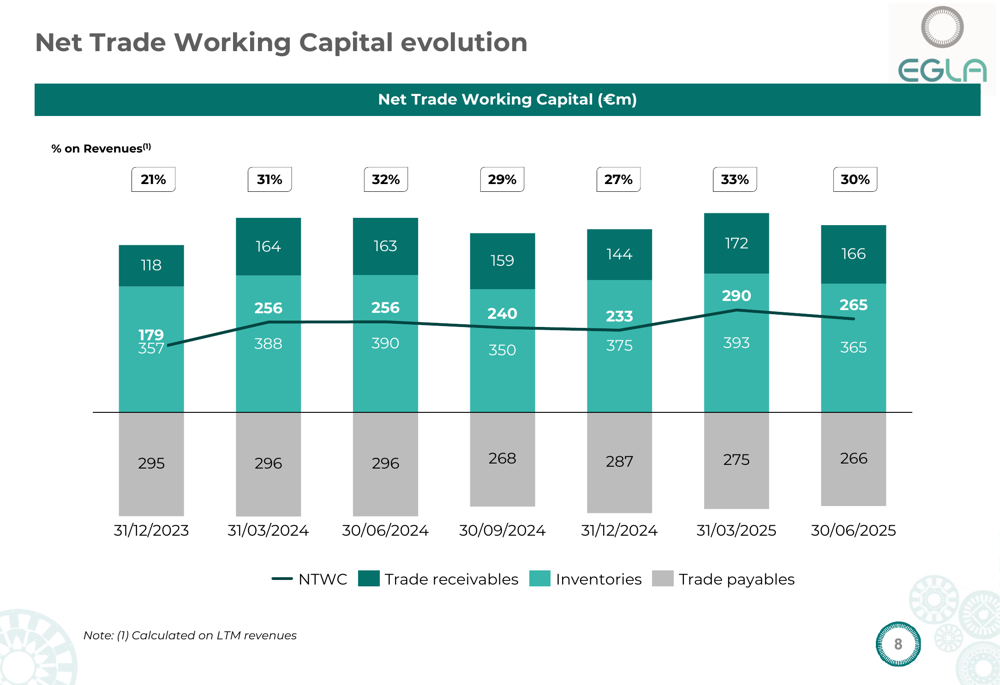

The company’s working capital management has been challenging, with Net Trade Working Capital increasing to €265 million as of June 2025, compared to €233 million at the end of 2024. This increase was primarily attributed to supporting seven Start of Production (SoP) events during the period.

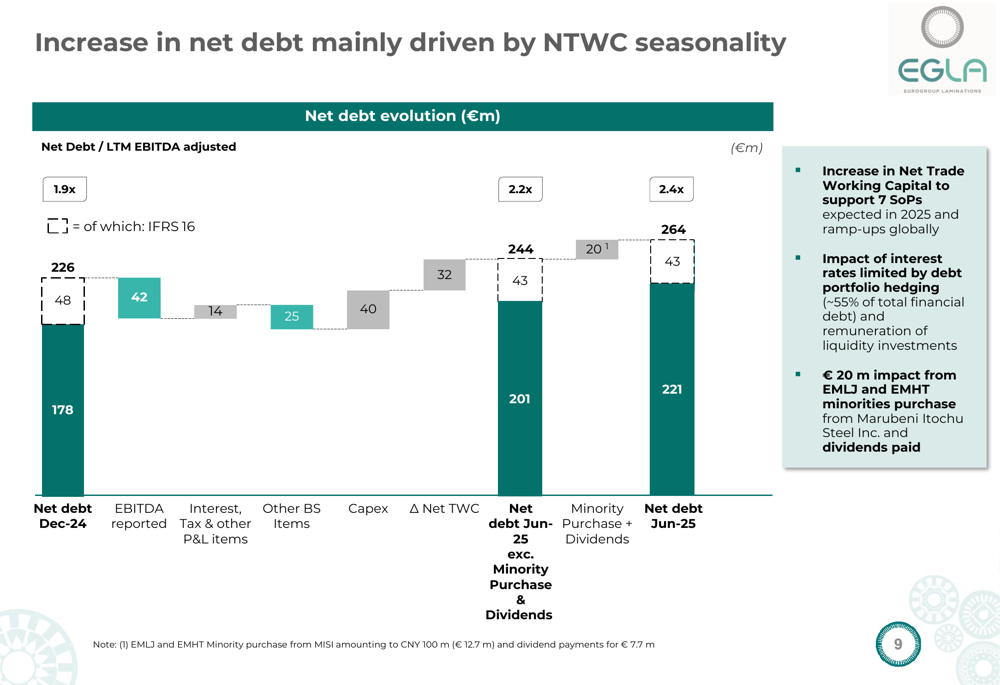

Net debt also increased to €264 million from €226 million in December 2024, driven by working capital needs and the €20 million impact from the purchase of EMLJ and EMHT minorities.

The most significant strategic development was the announcement of a partnership with FountainVest, which will see EMS and FountainVest jointly holding 55.3% of the voting share capital in EuroGroup Laminations. This partnership will lead to a mandatory tender offer at €3.85 per share, with the aim of delisting the company from Euronext Milan. The transaction, which values EuroGroup Laminations at approximately €626 million, is expected to be completed by the first half of 2026.

Forward-Looking Statements

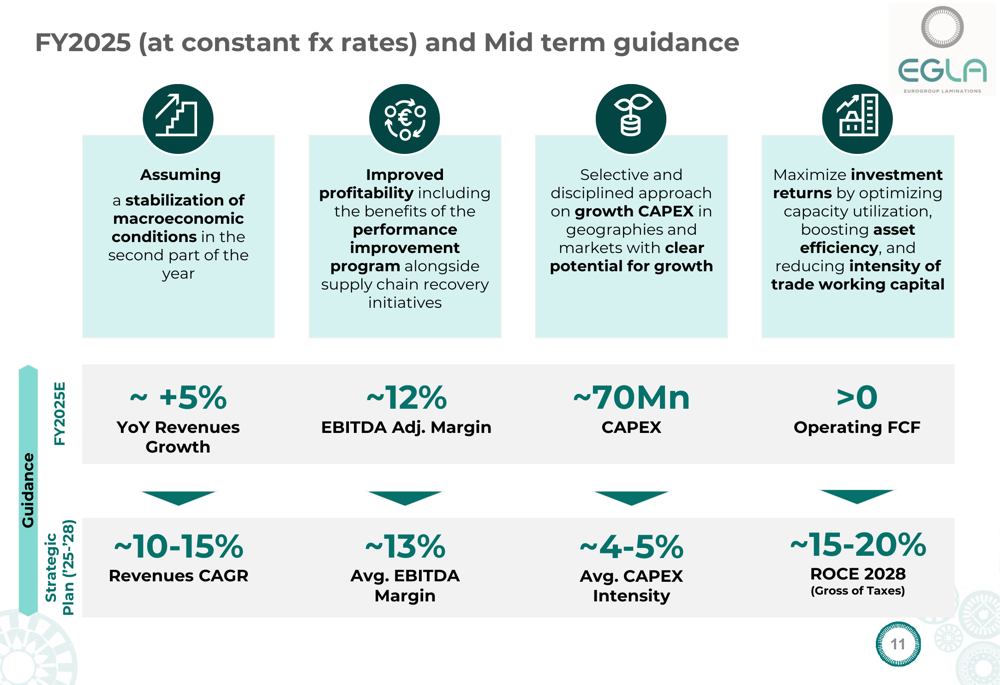

Despite near-term challenges, EuroGroup Laminations maintained its guidance for FY 2025, projecting revenue growth of approximately 5% year-over-year and an adjusted EBITDA margin of around 12%. The company expects capital expenditure of approximately €70 million and positive operating free cash flow for the full year.

Looking further ahead, the mid-term guidance remains ambitious, with projected revenue CAGR of 10-15%, average EBITDA margin of around 13%, and CAPEX intensity of 4-5%. The company targets a Return on Capital Employed (ROCE) of 15-20% by 2028.

These projections represent a recovery from the current margin pressures and align with the company’s strategic focus on operational improvements and geographic expansion, particularly in high-growth Asian markets.

Competitive Industry Position

EuroGroup Laminations continues to benefit from the global transition to electrification, particularly in the automotive sector. The company’s strong position in e-mobility components has enabled it to capture growth in China, where EV adoption continues to accelerate.

However, the company faces challenges in mature markets, particularly in the USMCA region where program postponements have affected near-term performance. The industrial business segment also showed weakness, with flat revenue growth and margin pressure.

The company’s strategic partnership with FountainVest appears designed to strengthen its competitive position in Asia, particularly China, while providing additional resources for global expansion. This move comes at a critical time as the company navigates through margin pressures and seeks to capitalize on the long-term electrification trend across multiple industries.

As EuroGroup Laminations implements its performance improvement program and continues its geographic expansion, investors will be watching closely to see if the company can deliver on its ambitious mid-term targets while managing through the current challenging environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.