With uncertainty rising, is gold’s bull run far from over?

Introduction & Market Context

Exelon Corporation (NASDAQ:EXC) released its second quarter 2025 earnings presentation on July 31, revealing a quarterly earnings decline but maintaining its full-year guidance based on strong year-to-date performance. The utility’s stock was down 2.33% in premarket trading to $43.23 following the release, after closing at $44.26 the previous day.

The company reported GAAP earnings of $0.39 per share for Q2 2025, down from $0.45 per share in the same period last year. Adjusted operating earnings also declined to $0.39 per share from $0.47 in Q2 2024. Despite this quarterly dip, Exelon reaffirmed its 2025 earnings guidance of $2.64-$2.74 per share, citing strong year-to-date performance and continued growth opportunities in transmission and data center markets.

Quarterly Performance Highlights

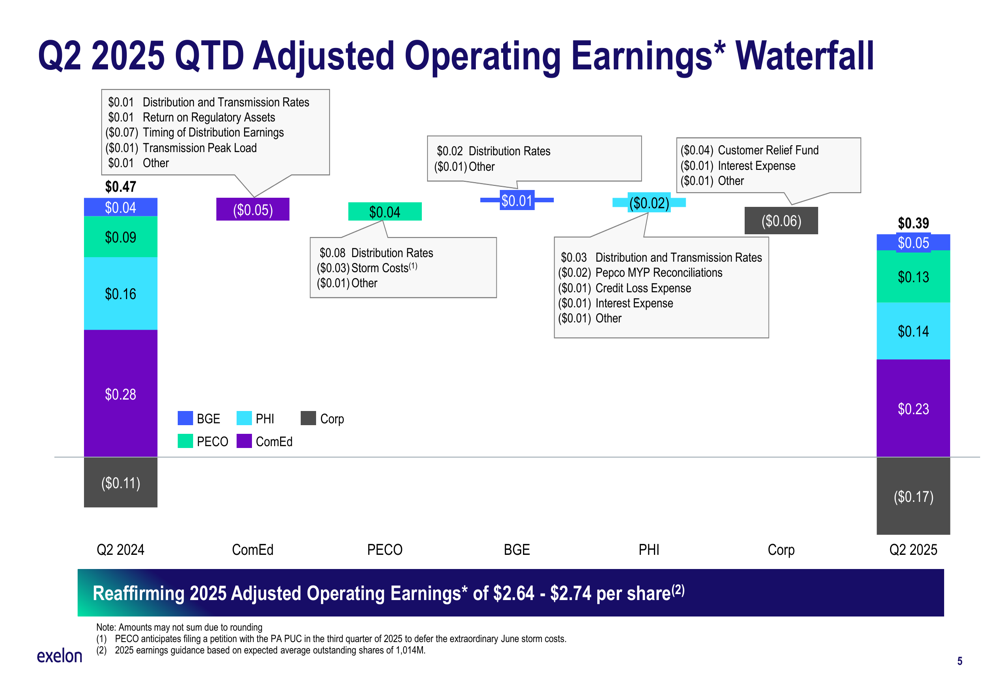

Exelon’s Q2 2025 results show a mixed performance across its utility subsidiaries. The earnings decline was primarily driven by timing of distribution earnings, transmission peak load impacts, and increased storm costs, partially offset by higher distribution and transmission rates.

As shown in the following quarterly earnings waterfall chart, ComEd earnings decreased from $0.16 to $0.13 per share, while PECO saw a significant drop from $0.28 to $0.14 per share, primarily due to storm costs and customer relief fund impacts:

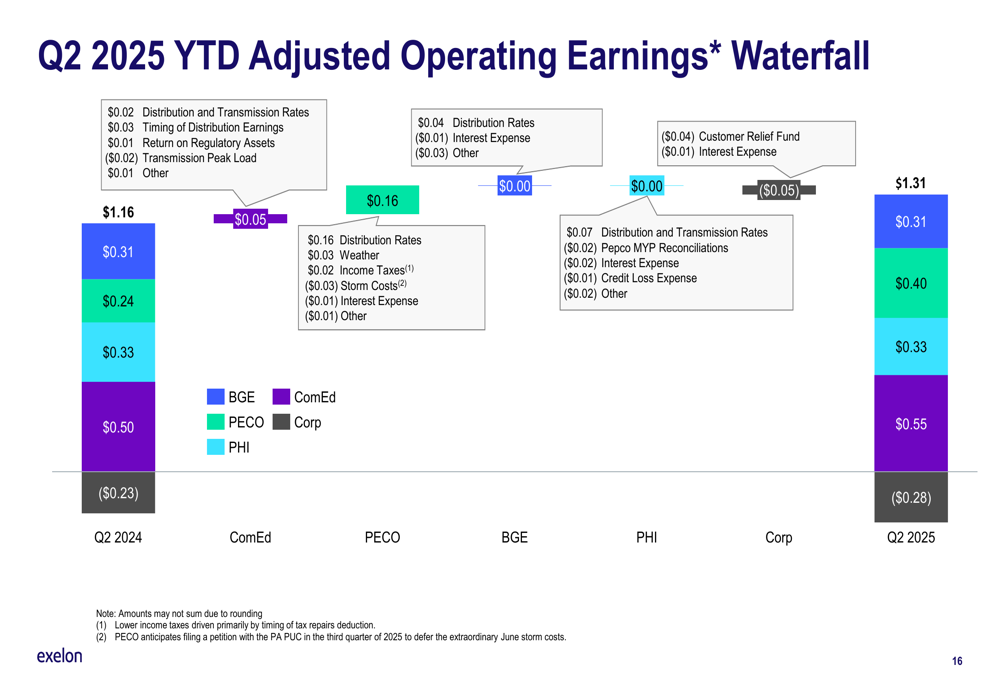

Despite the quarterly decline, Exelon’s year-to-date performance remains strong, with adjusted operating earnings reaching $1.31 per share compared to $1.16 for the same period in 2024. This 13% year-over-year improvement provides the foundation for the company’s maintained full-year guidance.

The year-to-date earnings improvement is illustrated in this comprehensive waterfall chart:

This stronger year-to-date performance aligns with Exelon’s robust Q1 2025 results, when the company reported earnings of $0.92 per share, significantly exceeding the forecasted $0.71. That quarter benefited from new distribution and transmission rates, favorable weather conditions, and timing of tax repairs.

Strategic Initiatives

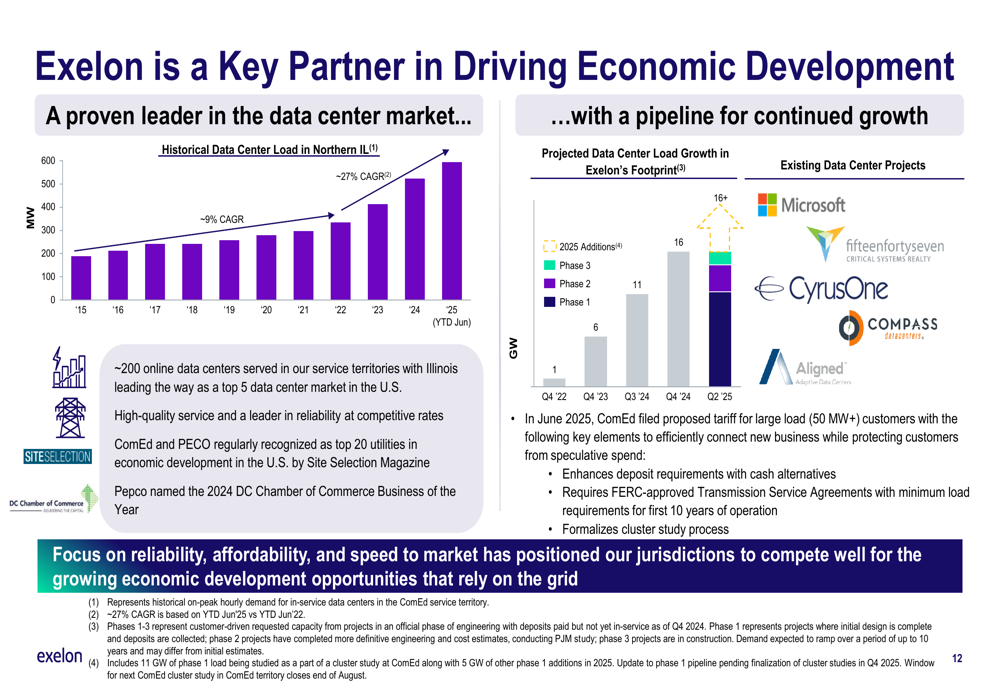

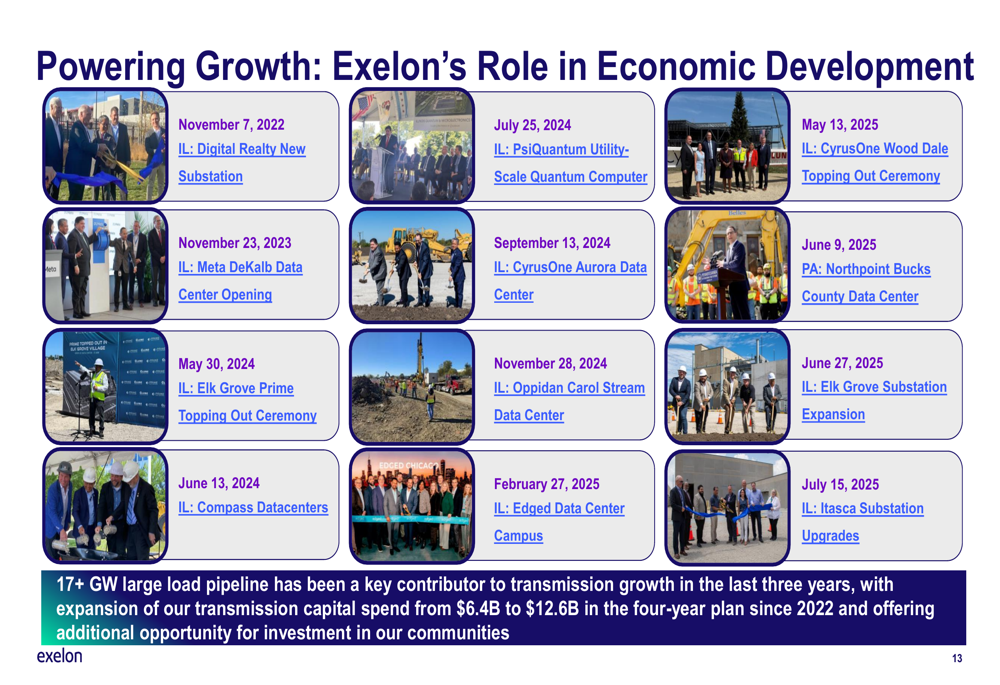

Exelon continues to position itself as a key partner in economic development, particularly in the rapidly growing data center market. The company highlighted its historical data center load growth in Northern Illinois, which has experienced approximately 27% CAGR from 2015 to June 2025.

The following chart illustrates Exelon’s leadership in the data center market and projected growth:

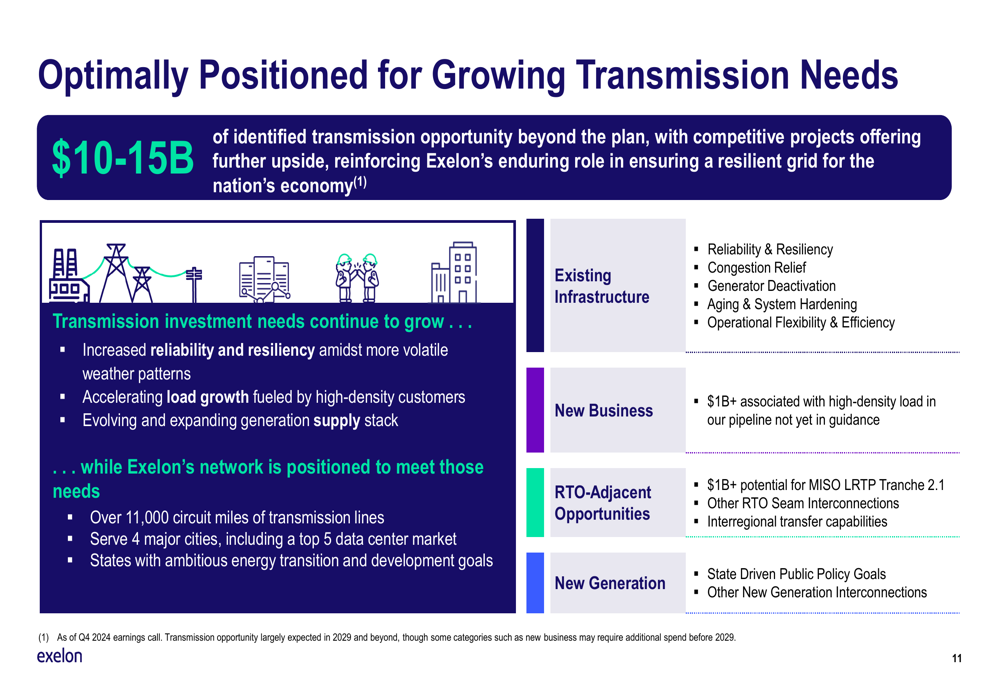

The company is also capitalizing on significant transmission investment opportunities, identifying $10-15 billion of potential projects beyond its current capital plan. These opportunities are driven by increased reliability needs, accelerating load growth from high-density customers, and an evolving generation supply stack.

As shown in this strategic overview of transmission opportunities:

Exelon emphasized its role in driving economic development across its service territories, showcasing various projects that demonstrate its contribution to regional growth:

Forward-Looking Statements

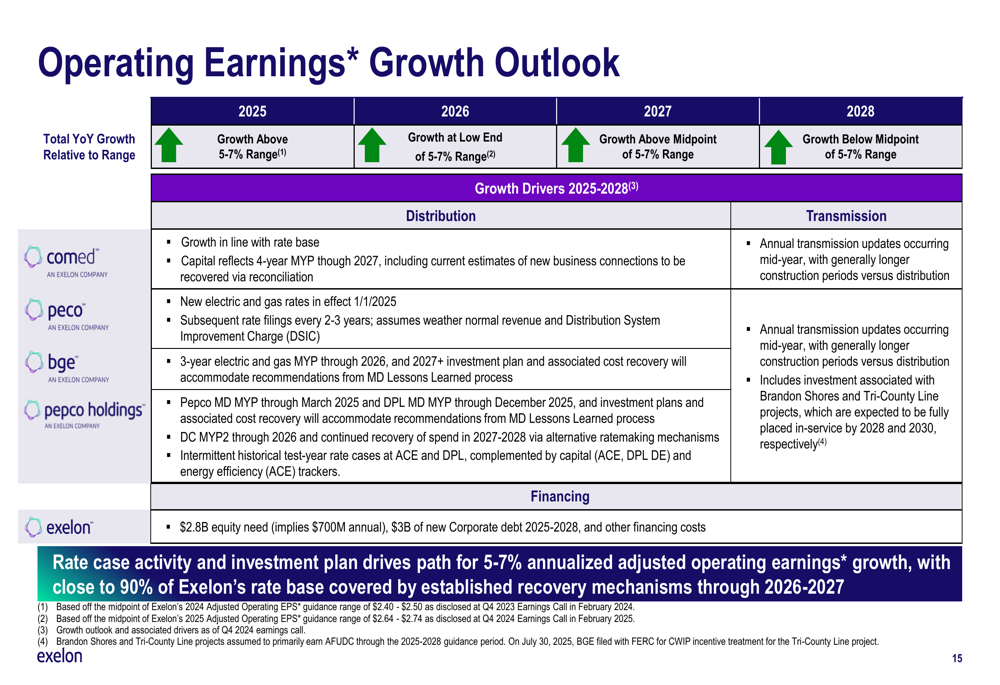

Despite the quarterly earnings decline, Exelon reaffirmed its 2025 earnings guidance of $2.64-$2.74 per share and maintained its 2024-2028 EPS CAGR of 5-7%, with expectations to be at the midpoint or better. The company’s confidence is supported by its $38 billion capital investment plan, which is expected to drive 7.4% rate base growth.

The following chart outlines Exelon’s operating earnings growth outlook through 2028:

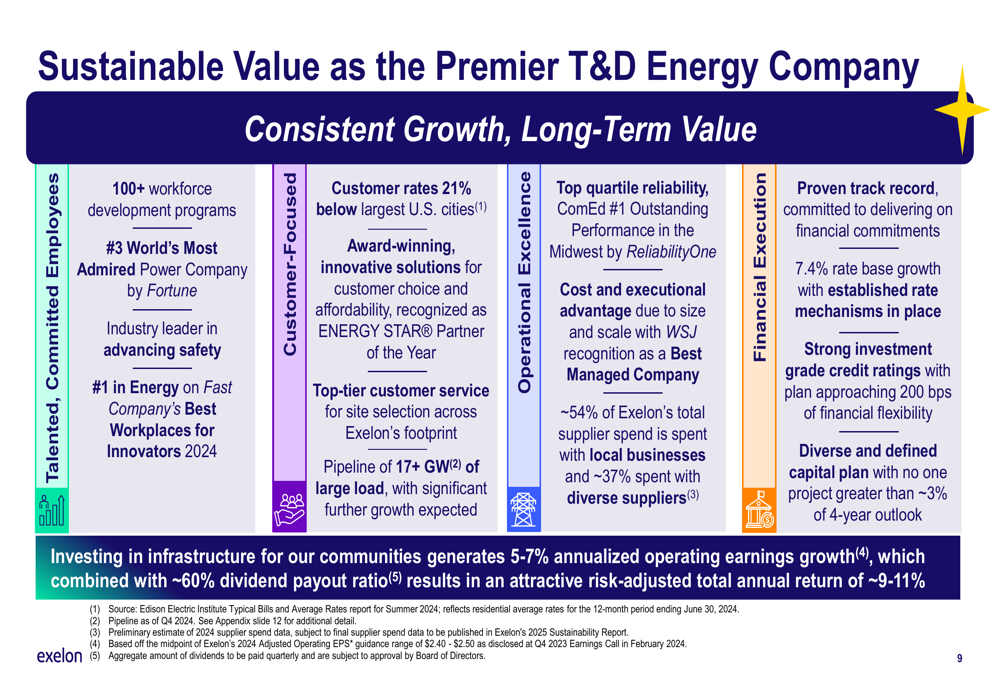

Exelon’s long-term strategy focuses on four key areas: talented committed employees, customer focus, operational excellence, and financial execution. The company positions itself as the premier T&D energy company, highlighting that customer rates remain 21% below the largest U.S. cities while maintaining top quartile reliability.

This comprehensive overview illustrates Exelon’s sustainable value proposition:

Financial Position

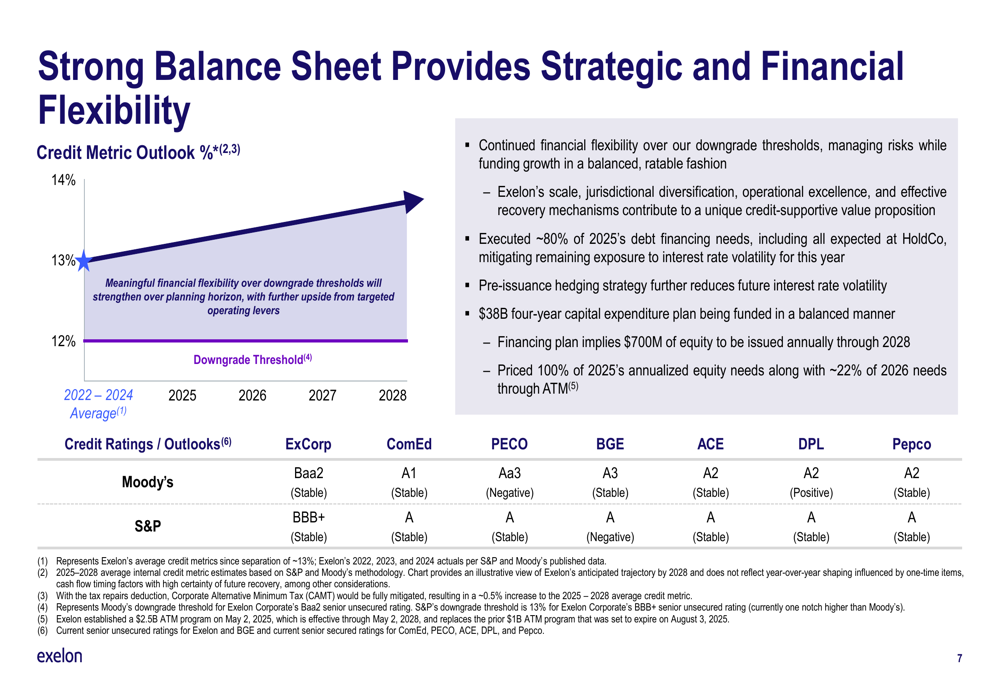

Exelon emphasized its strong balance sheet as a source of strategic and financial flexibility. The company’s credit metrics are trending upward from 12% towards 14% between 2022 and 2028, comfortably above the downgrade threshold of around 13%.

The following chart illustrates this positive credit metric trend:

The company has successfully executed its 2025 financing plan, with $700 million of equity already priced for issuance this year and $157 million (approximately 22%) of 2026’s annualized equity need priced for issuance next year. This balanced funding approach supports Exelon’s capital investment plan through 2028.

Exelon maintains a well-structured debt maturity profile with a weighted average long-term debt maturity of approximately 16 years, providing stability to its financing strategy. The company has also secured strong credit ratings across its subsidiaries, further enhancing its financial flexibility.

Regulatory & Industry Position

Exelon continues to navigate the regulatory landscape, with base rate cases remaining on track and orders expected in the next 6-9 months. The company is currently pursuing two open base rate cases: DPL DE Gas (requesting a $39.9 million revenue requirement increase) and ACE Electric (requesting a $108.9 million increase).

Energy security remains a top priority for Exelon, with the company advocating for states to consider all options to bring control and certainty to the energy supply needed to meet their policy goals. The company is engaged at federal, regional, and state levels to advance resilient, durable, and cost-effective solutions.

In June 2025, ComEd filed a proposed tariff for large load customers (50MW+) with enhanced deposit requirements, FERC-approved Transmission Service Agreements with minimum load requirements, and a formalized cluster study process. These measures aim to efficiently connect new business while protecting customers from speculative spending.

As Exelon navigates the remainder of 2025, the company’s focus on continued execution of operational, regulatory, and financial priorities will be critical to achieving its full-year guidance despite the Q2 earnings decline.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.