Street Calls of the Week

Introduction & Market Context

Extendicare Inc (TSX:EXE) presented its second quarter 2025 results on August 7, highlighting strategic acquisitions and strong operational performance across its business segments. The company, which provides care and services for seniors across Canada, continues to position itself to meet the growing demographic needs of an aging population.

The company’s stock closed at $12.73 on August 7, up 0.55% for the day, but remains well below its 52-week high of $15.24, suggesting investors may still be cautious despite the positive quarterly results.

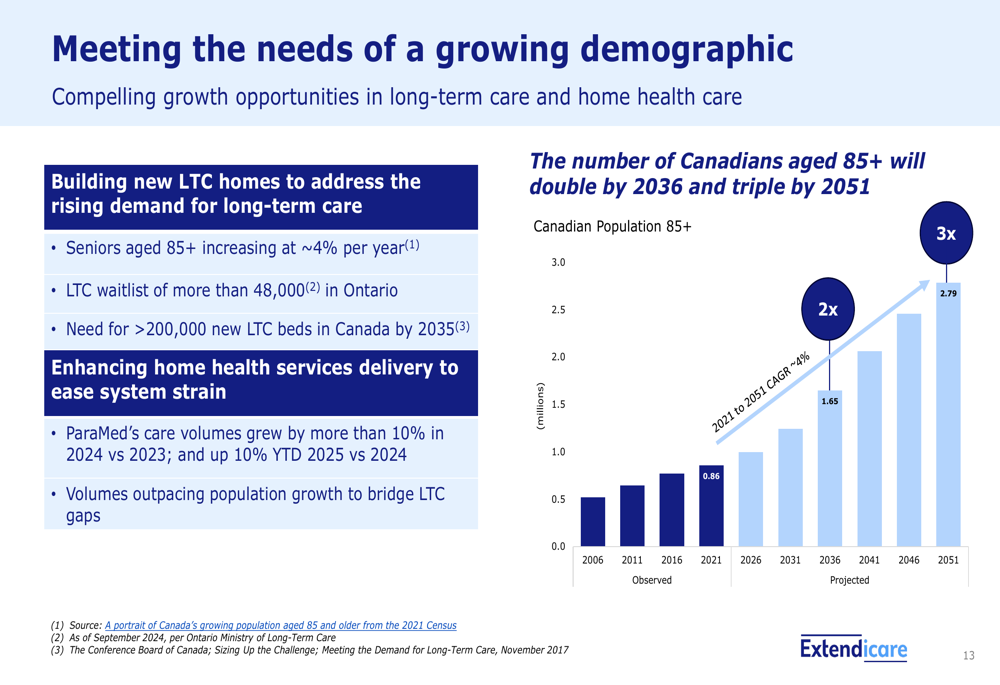

As shown in the company’s demographic outlook, the Canadian senior population aged 85+ is projected to double by 2036 and triple by 2051, creating substantial long-term demand for Extendicare’s services.

Quarterly Performance Highlights

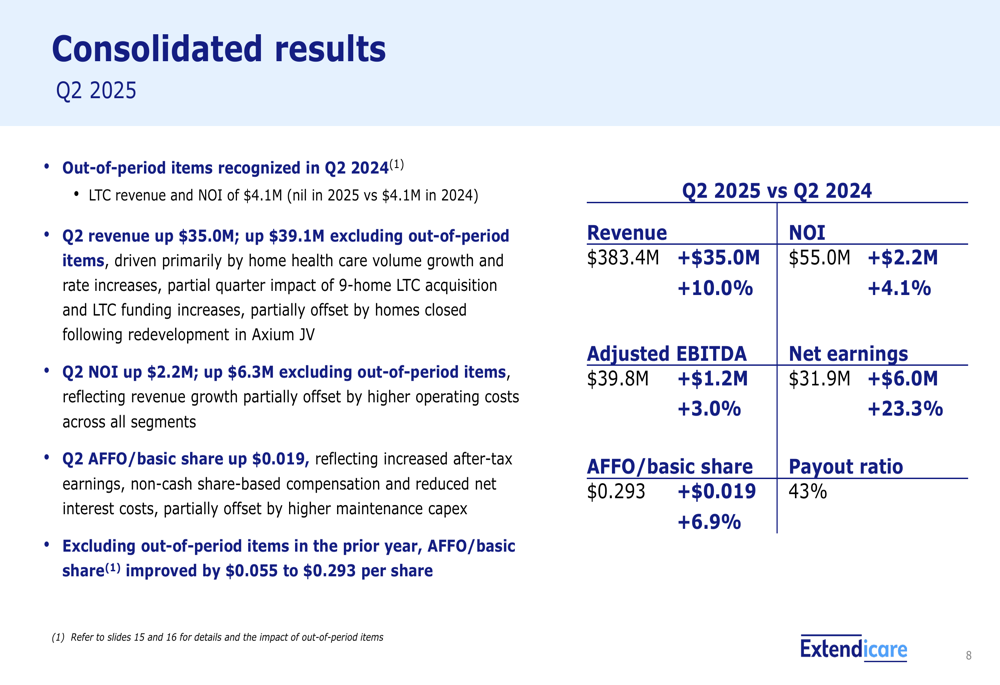

Extendicare reported solid financial results for Q2 2025, with adjusted EBITDA reaching $39.8 million, up 3.0% from $38.6 million in Q2 2024. When excluding out-of-period items from the prior year, the increase was more substantial at 15.4%.

The company’s AFFO (Adjusted Funds From Operations) per basic share rose 6.9% year-over-year to $0.293, with a healthy payout ratio of 43%. Net earnings increased by 23.3% to $31.9 million compared to the same period last year.

Revenue grew by 10.0% to $383.4 million, while NOI (Net Operating Income) increased by 4.1% to $55.0 million. These results demonstrate continued momentum following the company’s strong Q1 2025 performance, when Extendicare exceeded analyst expectations with an EPS of $0.176 against a forecast of $0.1604.

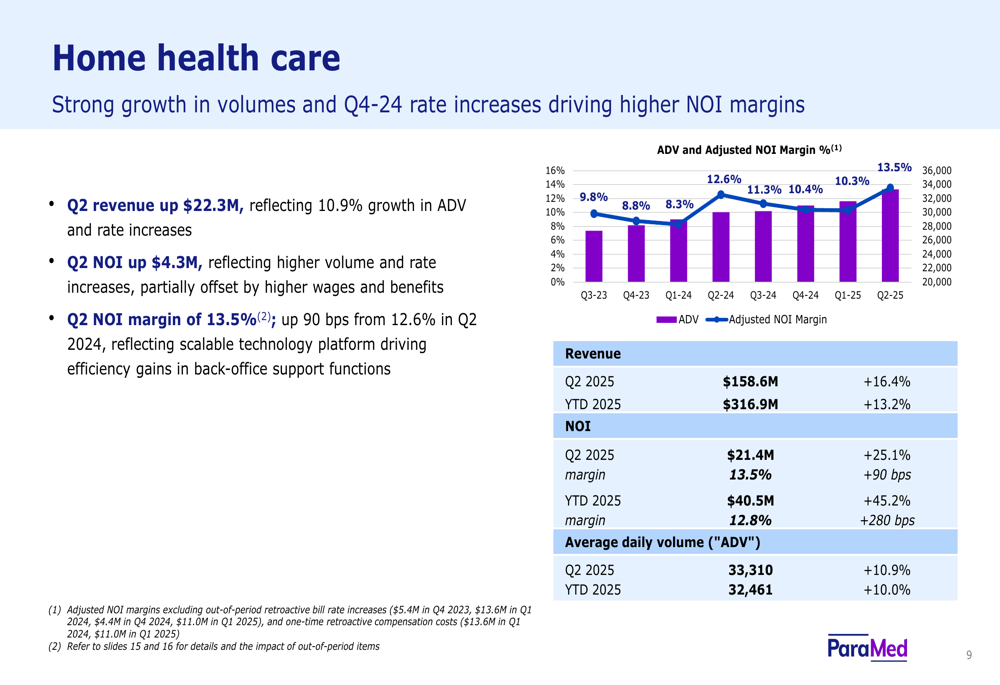

Home health care remained a standout performer with average daily volume (ADV) increasing by 10.9% year-over-year to 33,310 in Q2 2025. This segment saw significant improvement in its NOI margin, which rose 90 basis points to 13.5%.

Strategic Acquisitions

A key highlight of the quarter was Extendicare’s completion of two significant acquisitions that expand its footprint in both the long-term care and home health segments.

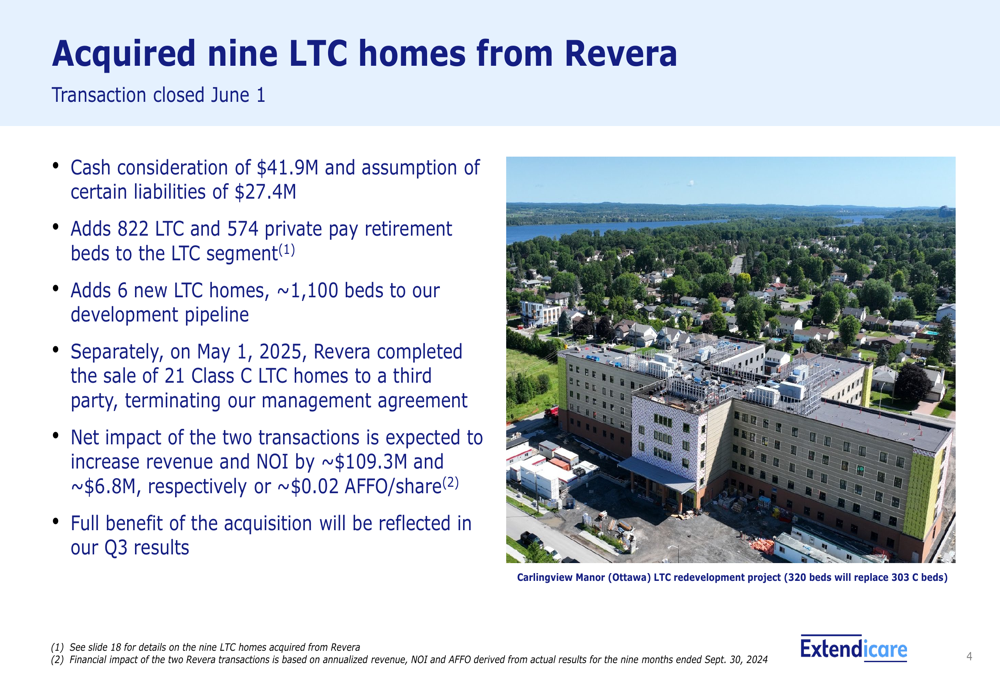

On June 1, the company closed the acquisition of nine long-term care homes from Revera for $41.9 million in cash, plus the assumption of $27.4 million in liabilities. This transaction adds 822 LTC beds and 574 private pay retirement beds to Extendicare’s portfolio, while also adding six new LTC homes with approximately 1,100 beds to the company’s development pipeline.

The acquisition is expected to increase annual revenue by approximately $109.3 million and NOI by $6.8 million, contributing approximately $0.02 to AFFO per share. The full benefit of this acquisition will be reflected in Q3 2025 results.

Additionally, on July 1, Extendicare acquired Closing the Gap for $75.1 million, which adds approximately 1.1 million service hours annually (equivalent to 3,109 ADV) in Ontario and Nova Scotia. This represents approximately a 10% increase in home health volumes for the company.

The Closing the Gap acquisition is expected to contribute approximately $84.2 million in revenue and $9.8 million in NOI to the home health segment, or approximately $0.06 to AFFO per share. The company anticipates achieving approximately $1.1 million in annualized cost synergies within the first year following the closing.

Development Pipeline and Capital Recycling

Extendicare continues to advance its strategy of redeveloping older Class C long-term care homes. During the quarter, the company completed the sale of three LTC projects to the Axium joint venture (London, Port Stanley, and St. Catharines, totaling 576 beds), generating $56.3 million in net proceeds and an $11.1 million after-tax gain.

The company is recycling this capital to fund new redevelopment projects. Currently, six LTC homes are under construction in the Axium JVs, which will provide 1,408 new beds to replace 1,097 Class C beds. The company is also advancing 18 other redevelopment projects to replace remaining Class C homes when conditions are favorable.

The table below outlines the current redevelopment projects, their expected opening dates, and estimated development costs:

Segment Performance Analysis

Extendicare’s performance varied across its three main business segments:

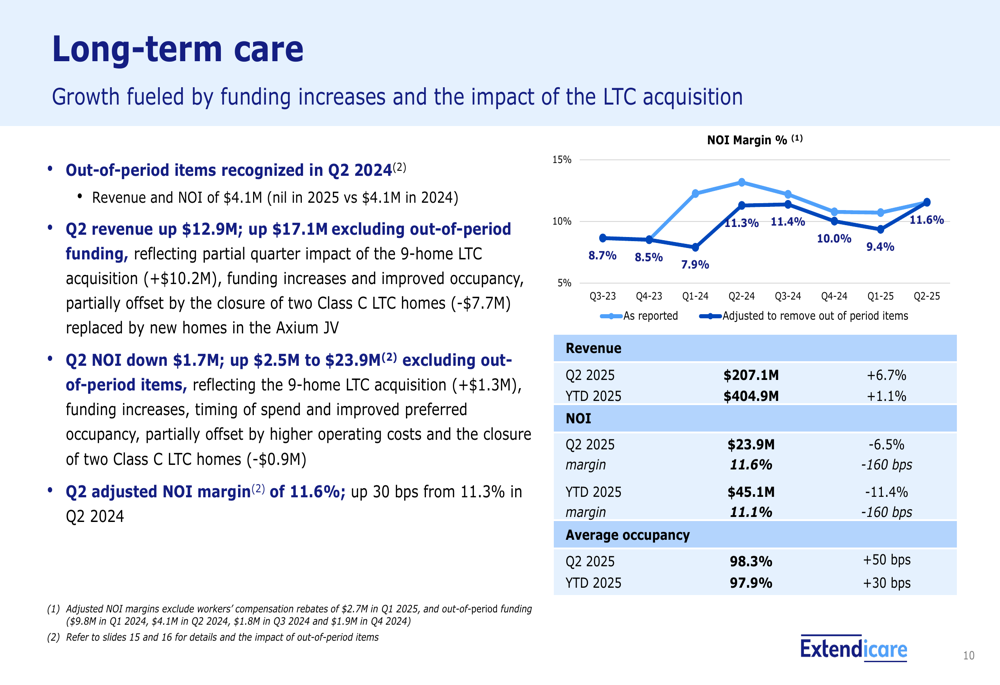

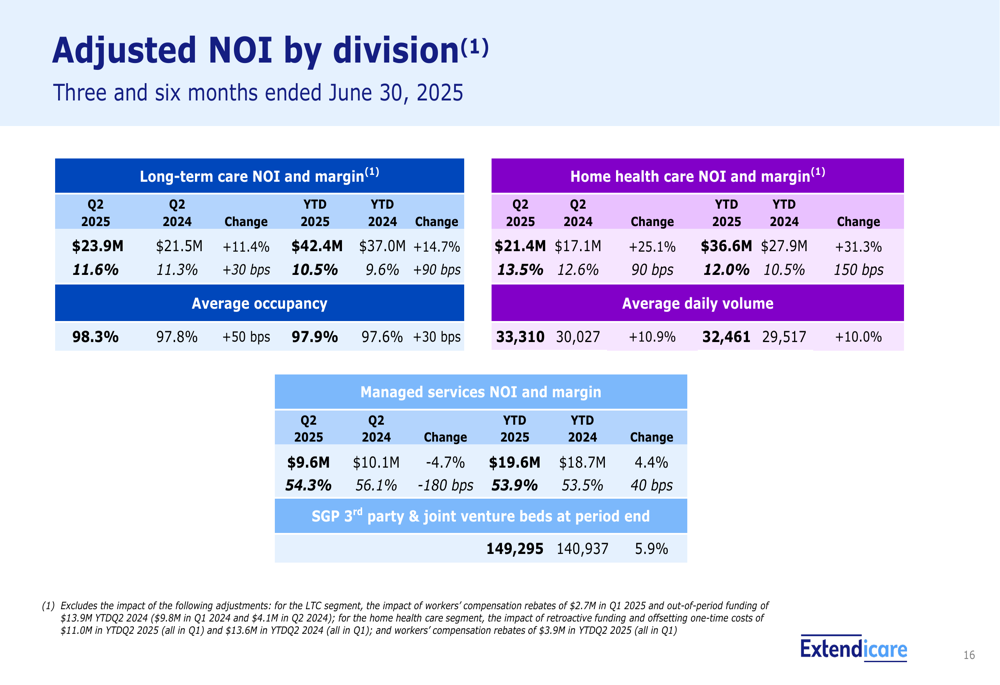

The Long-Term Care segment saw revenue increase by 6.7% to $207.1 million in Q2 2025. However, NOI decreased by 6.5% to $23.9 million, largely due to out-of-period funding of $4.1 million recognized in Q2 2024. Excluding these out-of-period items, NOI actually increased by $2.5 million or 11.4%. The adjusted NOI margin improved by 30 basis points to 11.6%, while average occupancy increased by 50 basis points to 98.3%.

The Home Health Care segment delivered strong results with revenue up $22.3 million, reflecting 10.9% growth in ADV and rate increases. NOI increased by $4.3 million, with margins expanding by 90 basis points to 13.5%. This performance continues the positive trend seen in previous quarters.

The Managed Services segment, which includes Extendicare Assist and SGP, saw a slight revenue decline of 1.6% to $17.7 million, primarily due to Revera’s sale of Class C LTC homes that were previously managed by Assist. Despite this, the segment maintained strong margins of 54.3%, though this represents a decrease of 180 basis points from the prior year. The SGP client base grew by 5.9% year-over-year, demonstrating continued organic growth in this business line.

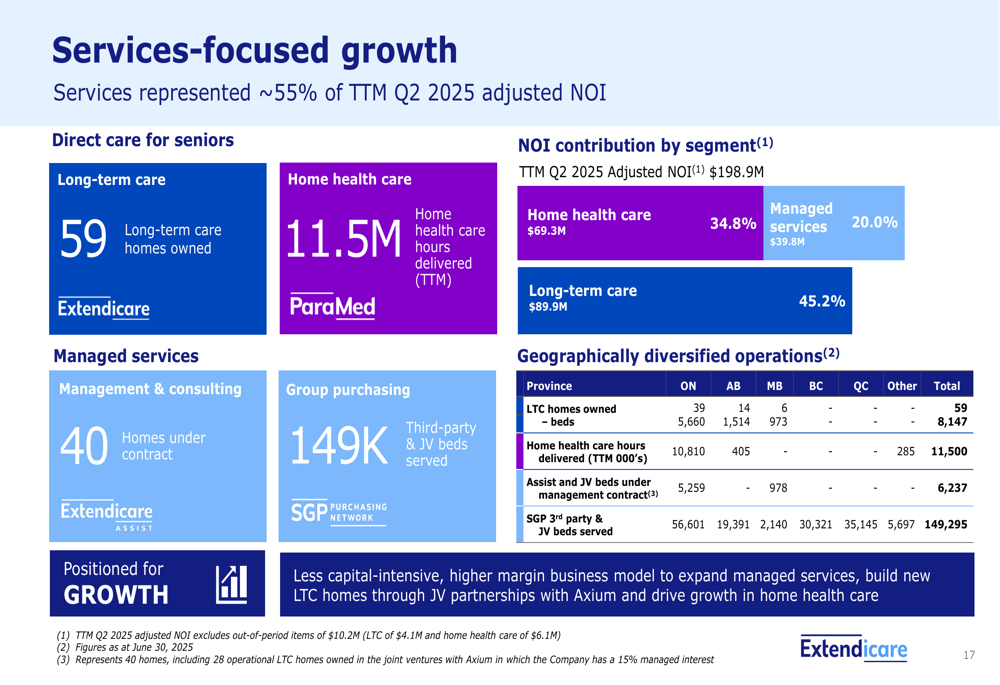

A breakdown of the NOI contribution by division shows that Long-Term Care accounts for 45.2% of total NOI, Home Health Care for 34.8%, and Managed Services for 20.0%.

Financial Position and Outlook

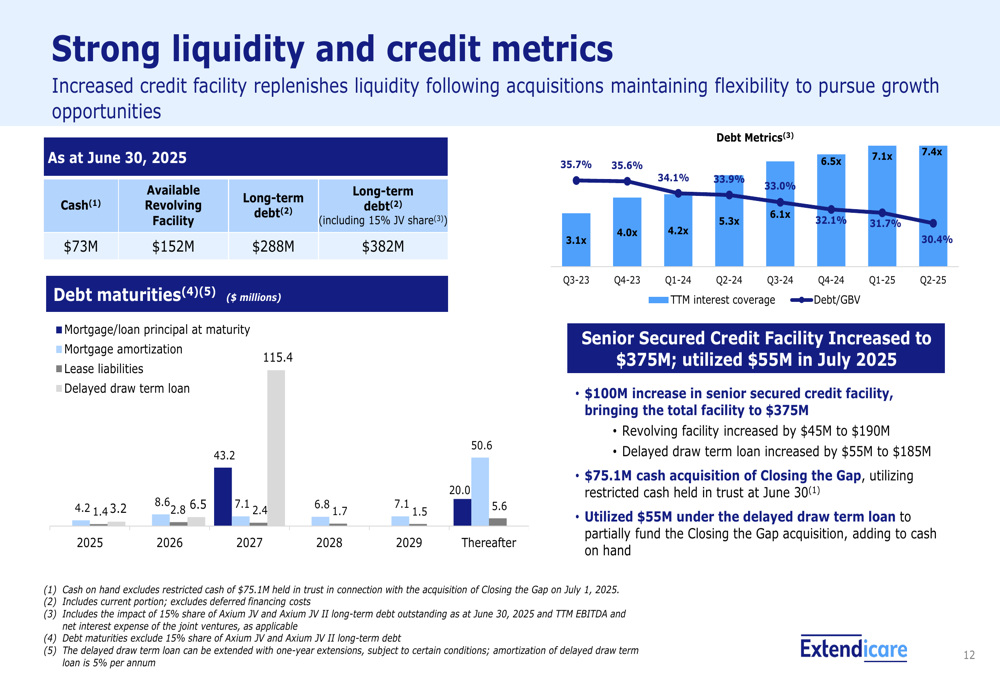

Extendicare has maintained a strong financial position to support its growth strategy. The company increased its senior secured credit facility by $100 million to a total of $375 million, with the revolving facility increased by $45 million to $190 million and the delayed draw term loan increased by $55 million to $185 million.

As of June 30, 2025, Extendicare had $73 million in cash and $152 million available on its revolving facility. Long-term debt stood at $288 million, or $382 million including the company’s 15% share of joint venture debt.

Looking ahead, Extendicare is well-positioned to capitalize on the growing demographic need for senior care services in Canada. The company’s strategic focus on services-based growth is evident in its portfolio mix, with services now representing approximately 55% of trailing twelve-month adjusted NOI.

The company’s less capital-intensive, higher-margin business model positions it to expand managed services, build new LTC homes through JV partnerships with Axium, and drive growth in home health care. With the Canadian population aged 85+ increasing at approximately 4% per year and an LTC waitlist of more than 48,000 in Ontario alone, Extendicare is addressing a market with substantial long-term growth potential.

The full impact of the recent acquisitions will be reflected in Extendicare’s Q3 2025 results, which should provide further insight into the company’s execution of its growth strategy and the integration of these new assets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.