C3is Inc. closes $2 million registered direct offering

Introduction & Market Context

Fasadgruppen Group AB (FG) presented its first quarter 2025 results on May 7, revealing a company navigating challenging market conditions while implementing strategic changes to improve profitability. The Swedish facade specialist’s stock closed at 19.92 SEK on May 6, down 1.63% and sitting near the lower end of its 52-week range (15.00-72.40 SEK), reflecting investor caution despite some positive operational indicators.

The presentation, led by CEO Martin Jacobsson, CFO Casper Tamm, and Head of IR Magnus Blomberg, highlighted a new organizational structure and strong adjusted EBITA growth, even as the company faced headwinds in organic sales growth due to weak new build activity, particularly in Sweden.

Quarterly Performance Highlights

Fasadgruppen reported a substantial increase in adjusted EBITA for Q1 2025, reaching 76.6 million SEK compared to 20.3 million SEK in Q1 2024, with margins expanding to 6.5% from 1.9%. This 276.5% year-over-year improvement came despite challenging organic sales trends.

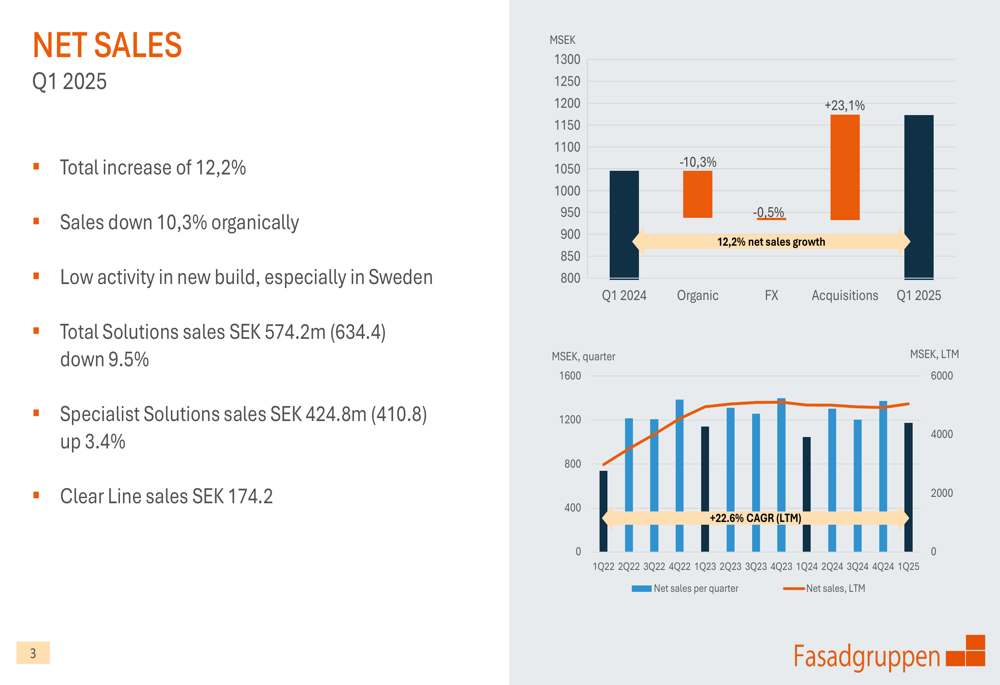

As shown in the following chart of quarterly net sales performance:

Total (EPA:TTEF) net sales increased by 12.2% year-over-year, driven primarily by acquisitions (+23.1%), while organic growth declined by 10.3%. The company attributed this organic decline mainly to low activity in new build projects, especially in Sweden. The newly established segment reporting showed varied performance: Total Solutions sales decreased 9.5% to 574.2 million SEK, while Specialist Solutions grew 3.4% to 424.8 million SEK. The newly acquired Clear Line contributed 174.2 million SEK.

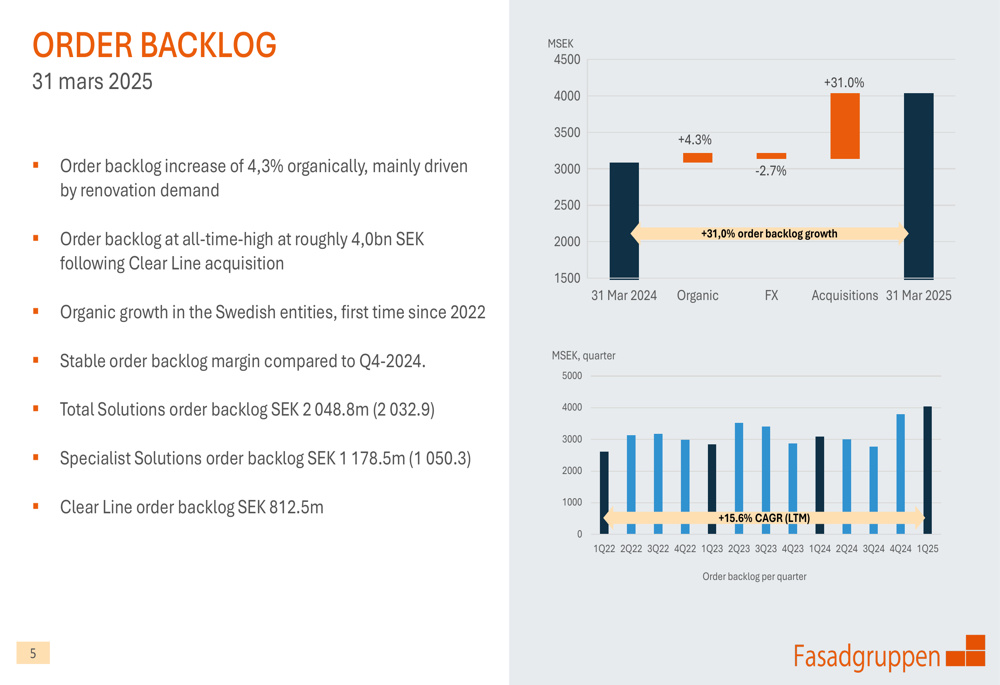

Despite the sales challenges, Fasadgruppen’s order backlog reached an all-time high of approximately 4.0 billion SEK, showing organic growth of 4.3%, primarily driven by renovation demand.

The order backlog growth is visualized in this chart:

The company noted this was the first time since 2022 that Swedish entities showed organic growth in order backlog, potentially signaling a market inflection point. Total Solutions order backlog stood at 2,048.8 million SEK, Specialist Solutions at 1,178.5 million SEK, and Clear Line at 812.5 million SEK.

Detailed Financial Analysis

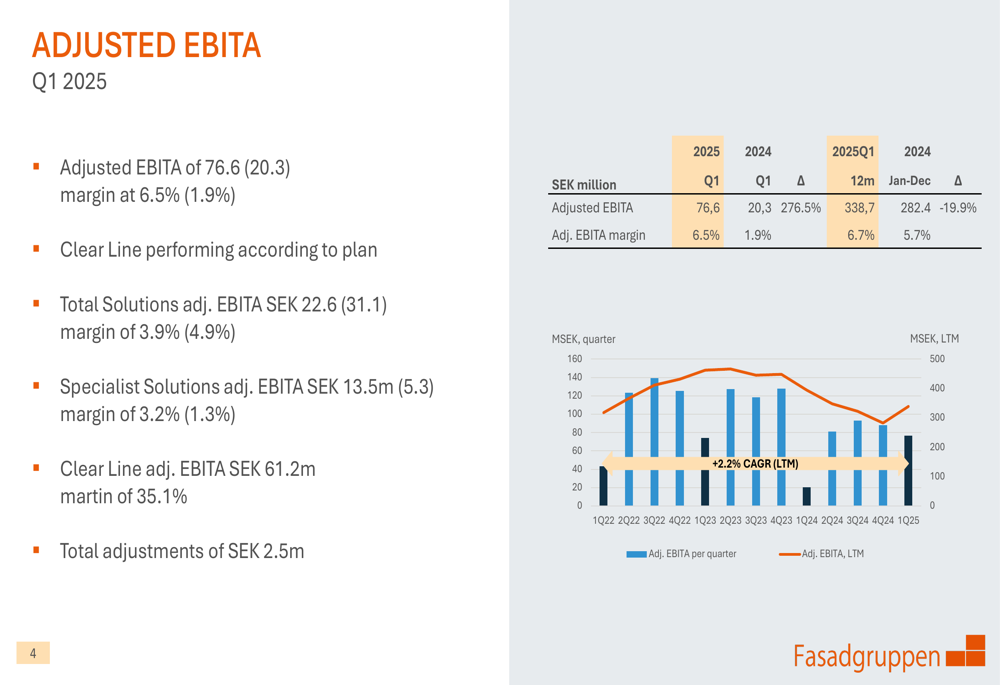

Fasadgruppen’s adjusted EBITA performance varied across segments, as illustrated in the following chart:

The Total Solutions segment recorded adjusted EBITA of 22.6 million SEK (31.1 million SEK in Q1 2024) with a margin of 3.9% (4.9%). Specialist Solutions showed improvement with adjusted EBITA of 13.5 million SEK (5.3 million SEK) and a margin of 3.2% (1.3%). The Clear Line segment delivered strong profitability with adjusted EBITA of 61.2 million SEK and a margin of 35.1%.

Cash flow performance weakened in Q1 2025, with operating cash flow at -31.7 million SEK compared to 18.4 million SEK in Q1 2024. The company attributed this to business ramping up and a delayed payment of 3 million GBP related to the Clear Line acquisition.

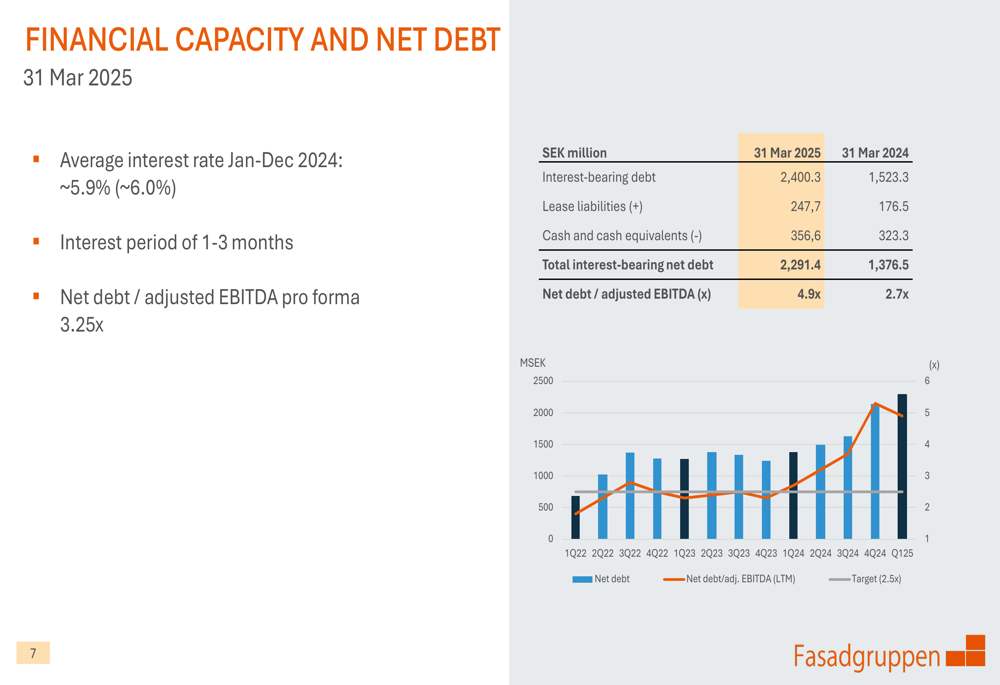

The company’s debt position has increased significantly, as shown in this financial capacity overview:

Total interest-bearing net debt reached 2,291.4 million SEK as of March 31, 2025, compared to 1,376.5 million SEK a year earlier. This pushed the net debt to adjusted EBITDA ratio to 4.9x, well above both the previous year’s 2.7x and the company’s target of below 2.5x. On a pro forma basis, the ratio stands at 3.25x, with management emphasizing their focus on deleveraging.

The Clear Line acquisition, while increasing debt, has brought strong cash flow potential to the group. Historical data shows Clear Line’s three-year average cash conversion at 87.0%, comparable to Fasadgruppen’s 86.8%.

Strategic Initiatives & Forward-Looking Statements

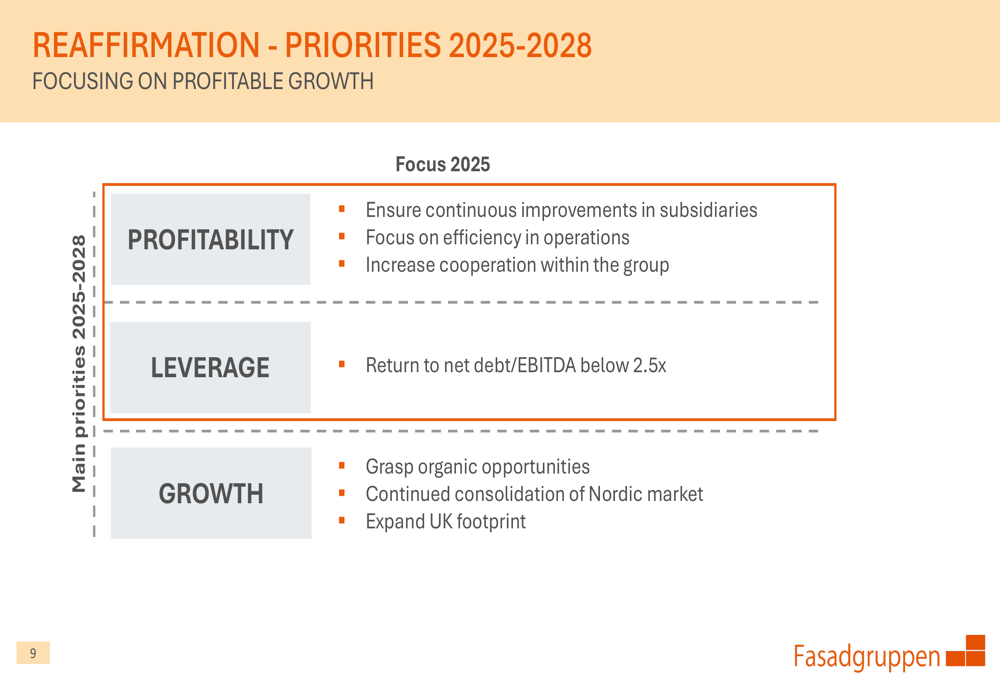

Fasadgruppen reaffirmed its strategic priorities for 2025-2028, focusing on three key areas as outlined in this strategic framework:

The company’s profitability initiatives include continuous improvements in subsidiaries, operational efficiency, and increased intra-group cooperation. For leverage, the clear priority is returning to a net debt/EBITDA ratio below 2.5x. Growth strategies involve organic opportunities, continued Nordic market consolidation, and expanding the UK footprint.

In its concluding remarks, management highlighted positive signs in the market with a stronger order backlog, while acknowledging continued low activity in new build projects. The company characterized 2025 as a year of deleveraging and profitability measures, with the Clear Line acquisition performing according to plan.

As the construction and renovation market continues to evolve, Fasadgruppen’s focus on profitability over growth represents a strategic pivot that aims to strengthen the company’s financial position amid challenging market conditions. The growing order backlog provides some optimism for future organic growth recovery, though investors appear to be taking a cautious approach until deleveraging progress becomes more evident.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.