Adaptimmune stock plunges after announcing Nasdaq delisting plans

Introduction & Market Context

Ferguson PLC (NYSE:FERG) delivered a strong finish to fiscal year 2025, with fourth-quarter results significantly outperforming the broader market despite challenging conditions. The company’s shares surged 8.31% in premarket trading to $232.35 following the release of its Q4 and full-year 2025 presentation on September 16, 2025, signaling investor confidence in the company’s performance and outlook.

The strong Q4 results represent a notable improvement from the previous quarter, when Ferguson missed analyst expectations with Q3 EPS of $2.50 (below the forecast of $2.61) and revenue of $7.62 billion (below the expected $7.79 billion). The company’s ability to accelerate growth in the final quarter demonstrates effective execution of its strategic initiatives and operational resilience.

Quarterly Performance Highlights

Ferguson’s fourth quarter showed impressive growth across key financial metrics, with particularly strong performance in the non-residential segment offsetting challenges in the residential market.

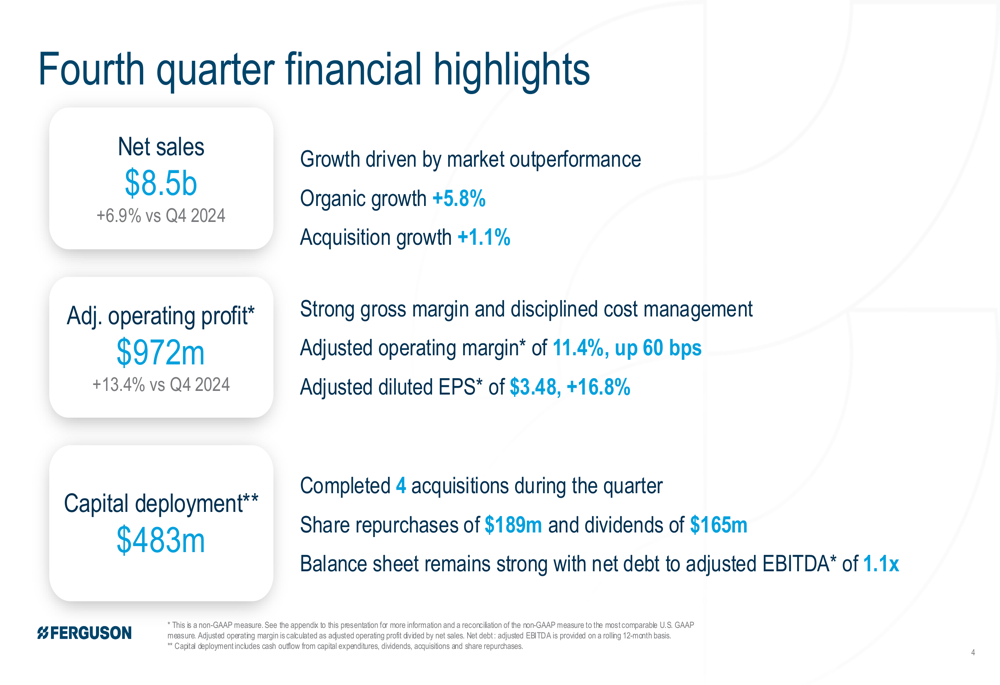

As shown in the following comprehensive overview of Q4 financial highlights:

Net sales reached $8.5 billion, representing a 6.9% increase compared to Q4 2024. This growth was driven by 5.8% organic growth and 1.1% acquisition growth. Adjusted operating profit rose to $972 million, a substantial 13.4% increase year-over-year, while adjusted operating margin expanded by 60 basis points to 11.4%. Adjusted diluted earnings per share grew 16.8% to $3.48.

The company maintained a strong balance sheet with a net debt to adjusted EBITDA ratio of 1.1x, providing financial flexibility for continued strategic investments. During the quarter, Ferguson deployed $483 million in capital, including funding for four acquisitions, $189 million in share repurchases, and $165 million in dividends.

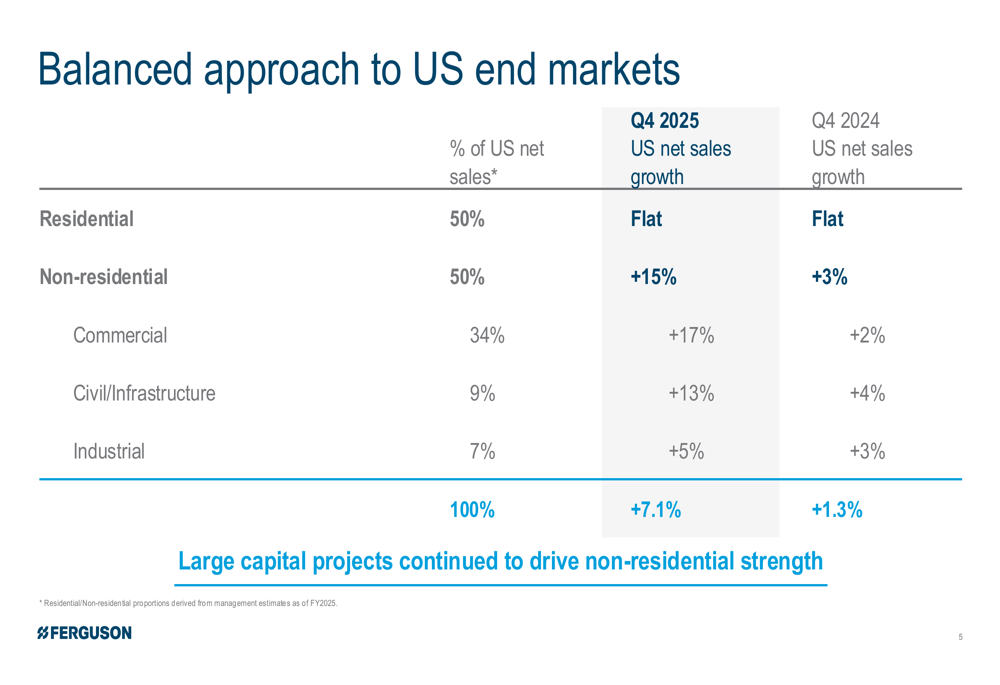

Ferguson’s balanced approach to end markets has been instrumental in navigating varying market conditions, as illustrated in this breakdown:

The non-residential segment, representing 50% of US net sales, delivered exceptional 15% growth in Q4 2025, a significant acceleration from the 3% growth in Q4 2024. This was primarily driven by the commercial subsegment, which grew 17%, and civil/infrastructure, which increased by 13%. Meanwhile, the residential segment, accounting for the other 50% of US net sales, remained flat year-over-year.

Detailed Financial Analysis

For the full fiscal year 2025, Ferguson achieved solid results despite market headwinds, as shown in this comprehensive summary:

Net sales for FY2025 reached $30.8 billion, representing a 3.8% increase over FY2024. Adjusted operating profit grew modestly by 0.6% to $2.8 billion, while adjusted operating margin contracted slightly to 9.2% from 9.5% in the previous year. Adjusted diluted EPS increased by 2.6% to $9.94. The company generated $1.9 billion in operating cash flow and returned $1.4 billion to shareholders.

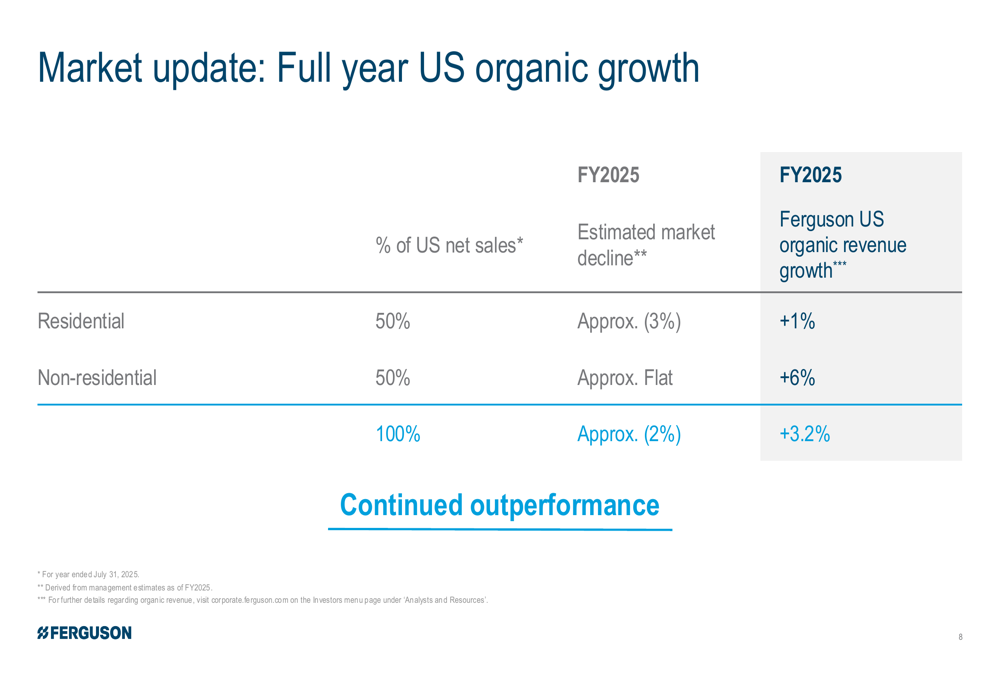

Ferguson’s performance is particularly impressive when viewed against the backdrop of broader market conditions:

Despite an estimated 2% decline in the overall US market, Ferguson achieved 3.2% organic revenue growth for the full year. In the residential segment, which faced an approximate 3% market decline, the company still managed 1% growth. The non-residential segment significantly outperformed with 6% growth against a flat market, demonstrating Ferguson’s ability to gain market share across its business segments.

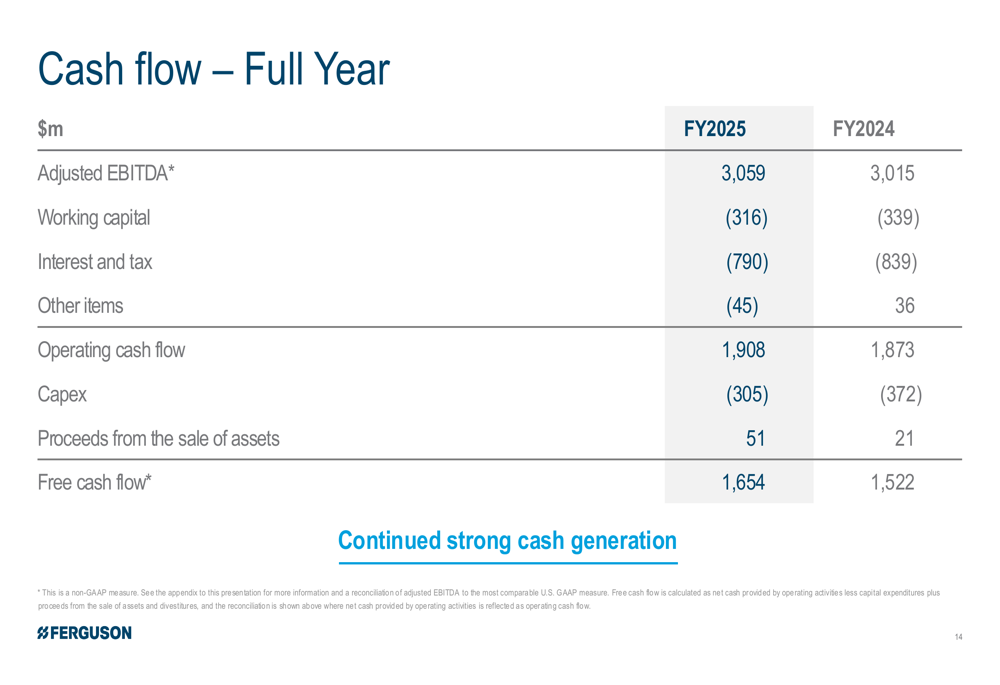

Cash flow generation remained strong throughout the fiscal year, providing the company with ample resources for strategic investments and shareholder returns:

Strategic Initiatives

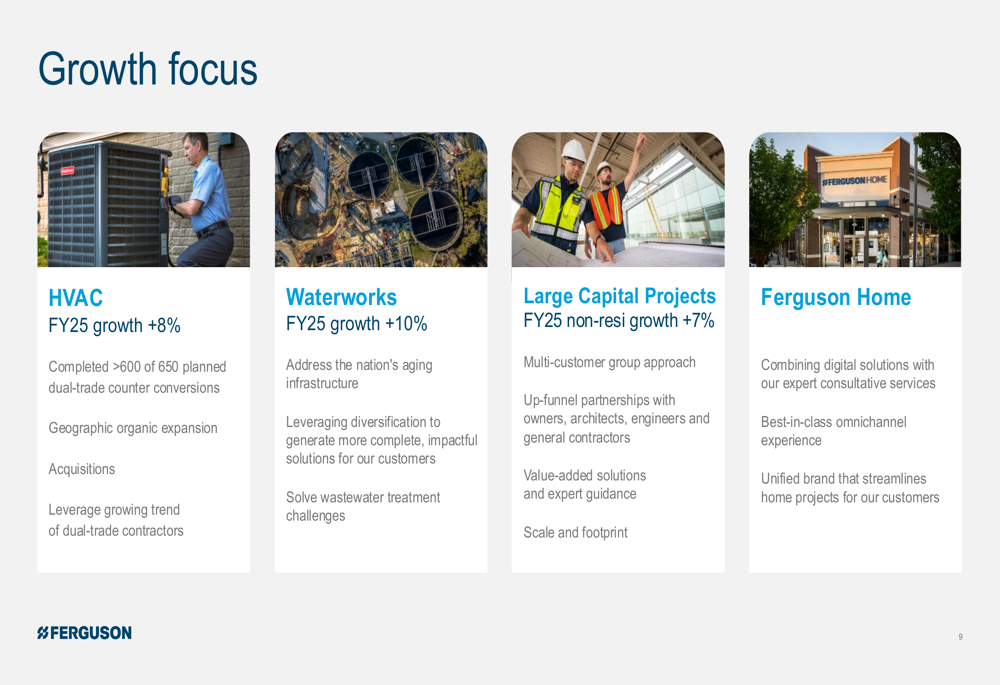

Ferguson’s growth strategy focuses on four key areas that have demonstrated strong performance and future potential:

The HVAC segment achieved 8% growth in FY2025, driven by dual-trade counter conversions, geographic expansion, and strategic acquisitions. Waterworks delivered impressive 10% growth, capitalizing on aging infrastructure needs and wastewater treatment challenges. Large capital projects contributed to 7% growth in the non-residential segment through multi-customer group approaches and value-added solutions. Ferguson Home continued to evolve by combining digital solutions with consultative services to provide an omnichannel experience.

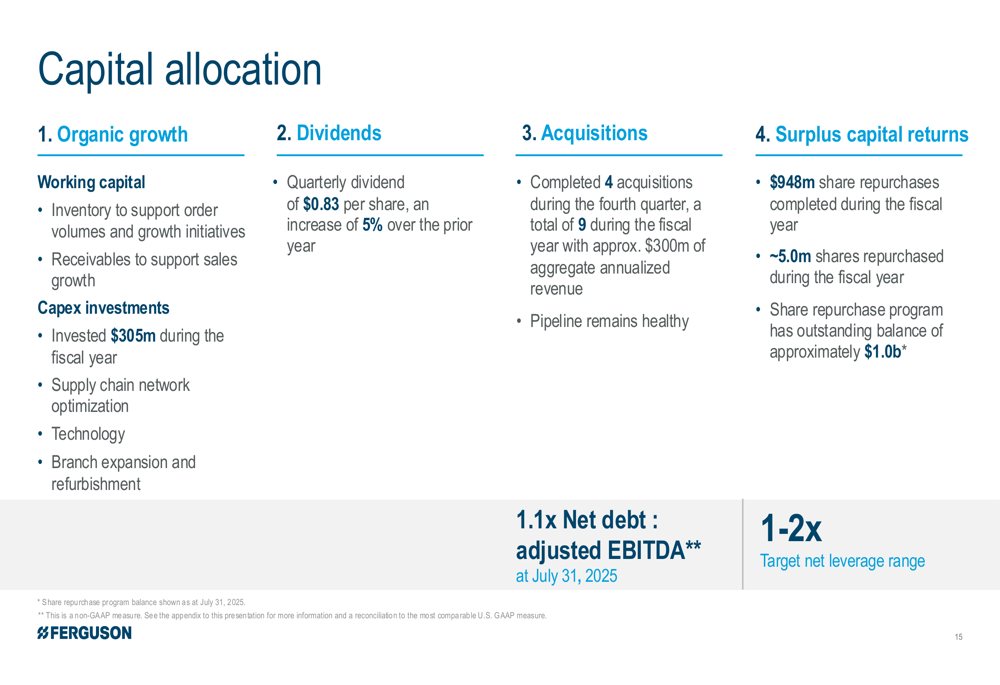

The company’s disciplined capital allocation strategy balances investments in organic growth, acquisitions, dividends, and share repurchases:

During FY2025, Ferguson invested $305 million in capital expenditures focused on supply chain, technology, and branch expansion. The quarterly dividend increased by 5% to $0.83 per share. The company completed nine acquisitions during the year, with approximately $300 million in aggregate annualized revenue. Share repurchases totaled $948 million (approximately 5.0 million shares), with $1.0 billion remaining on the current repurchase program.

Forward-Looking Statements

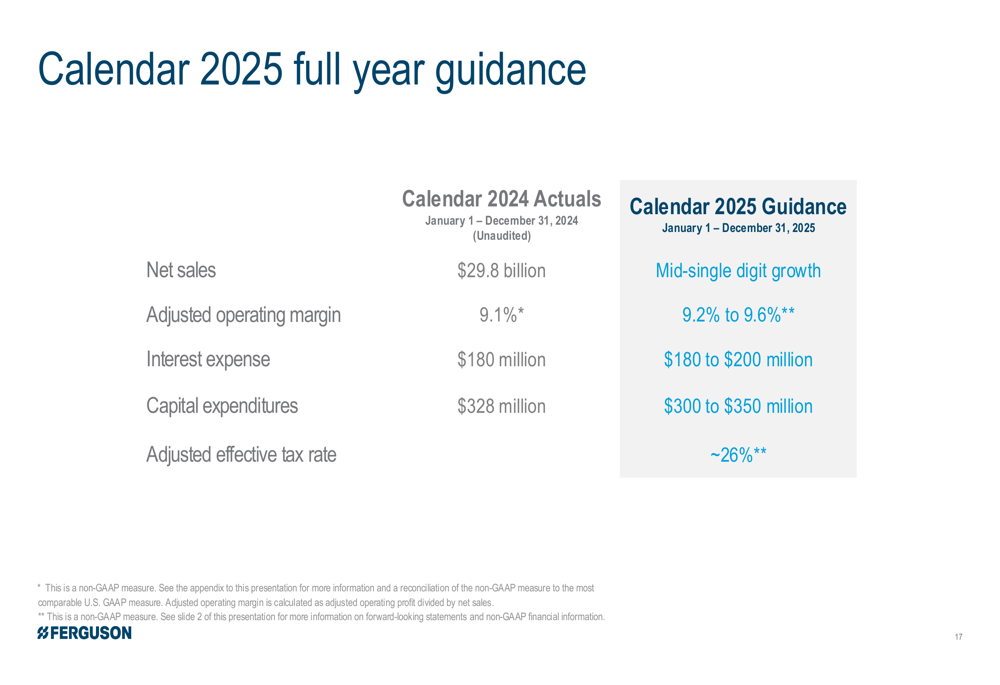

Looking ahead to calendar year 2025, Ferguson provided the following guidance:

The company expects mid-single-digit net sales growth with adjusted operating margin between 9.2% and 9.6%. Interest expense is projected to be between $180 million and $200 million, with capital expenditures ranging from $300 million to $350 million. The adjusted effective tax rate is expected to be approximately 26%.

In his closing remarks, CEO Kevin Murphy expressed confidence in the company’s medium-term outlook and emphasized Ferguson’s continued focus on investing in scale and capabilities to drive market share gains. This sentiment aligns with Murphy’s statement from the Q3 earnings call, where he highlighted that "Our associates continue to take care of our customers, outperform the market, and drove strong results."

Ferguson’s strong Q4 performance, coupled with its strategic focus on high-growth segments and disciplined capital allocation, positions the company well to continue outperforming the market despite ongoing macroeconomic challenges. The significant improvement from Q3 to Q4 demonstrates the company’s operational resilience and effective execution of its growth initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.