Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

FGI Industries Ltd (NASDAQ:FGI), a global supplier of kitchen and bath products, presented its first quarter 2025 results on May 13, highlighting continued revenue growth amid challenging market conditions. The company, which went public in January 2022, reported an 8.0% year-over-year revenue increase, though profitability metrics declined compared to the same period last year.

Trading at $0.58 in after-hours trading, up 3.57% from its last close of $0.56, FGI remains significantly below its 52-week high of $1.36, reflecting ongoing investor concerns about the company’s profitability trajectory.

Quarterly Performance Highlights

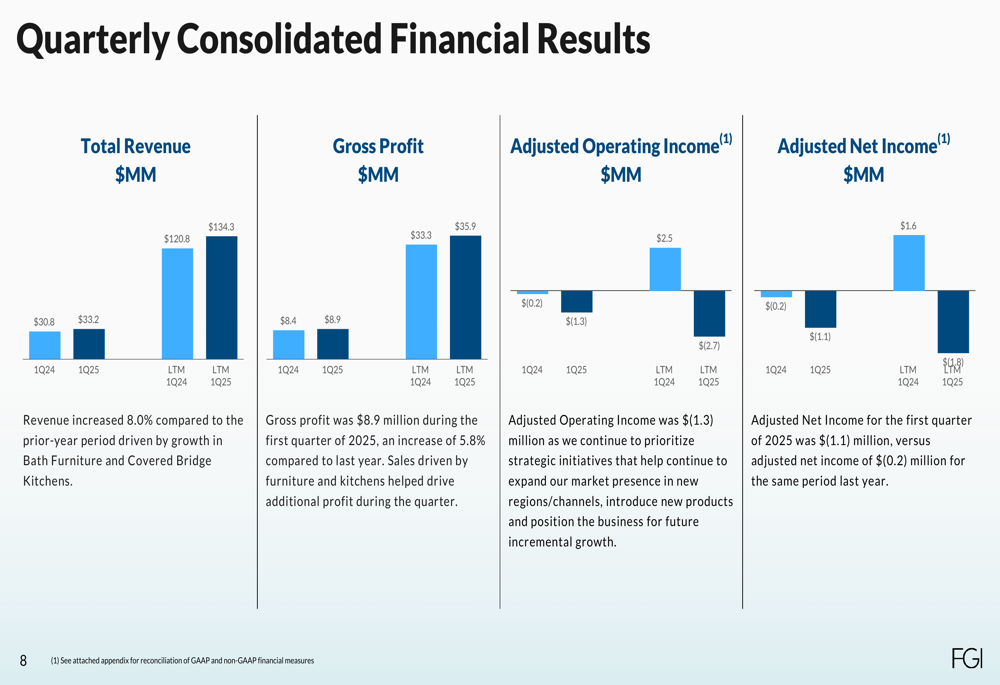

FGI reported Q1 2025 revenue of $33.2 million, representing an 8.0% increase from $30.8 million in Q1 2024. This growth was primarily driven by expansion in Bath Furniture and the company’s Covered Bridge product line.

As shown in the following consolidated financial results chart:

Despite the revenue growth, adjusted operating income declined to $(1.3) million from $(0.2) million in the prior year period. Similarly, adjusted net income fell to $(1.1) million from $(0.2) million year-over-year. The last twelve months (LTM) figures also show a concerning trend, with LTM adjusted operating income at $(2.7) million compared to $2.5 million in the previous LTM period.

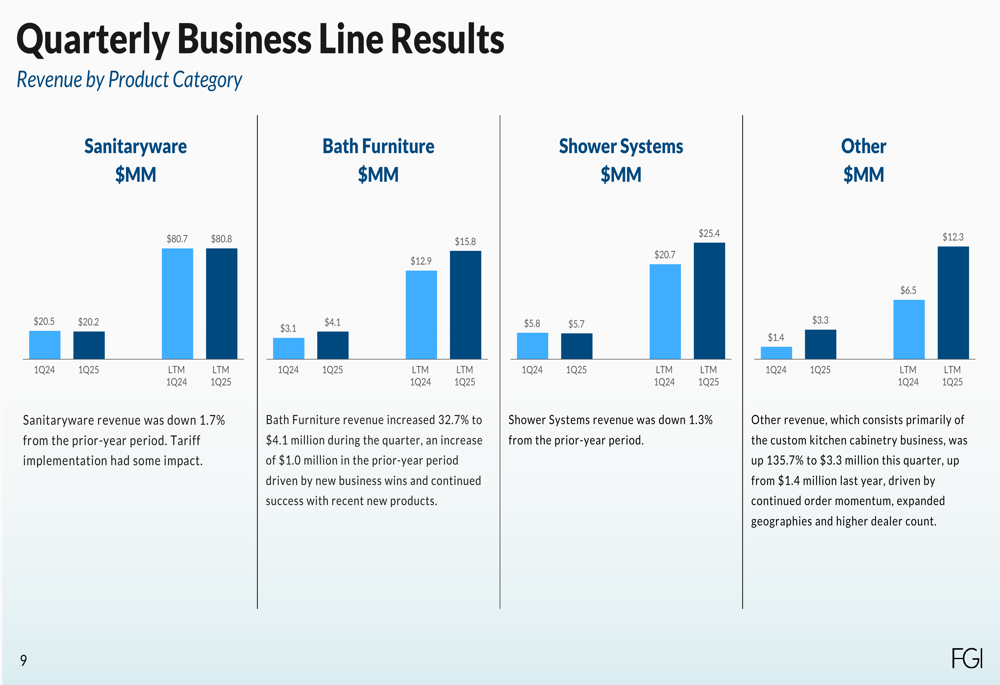

The company’s product category breakdown reveals varied performance across segments:

Sanitaryware, the company’s largest segment representing over 60% of total revenue, remained relatively flat at $20.2 million compared to $20.5 million in Q1 2024. Bath Furniture showed the strongest growth, increasing from $3.1 million to $4.1 million (32.3% growth), while Shower Systems slightly decreased to $5.7 million from $5.8 million. The "Other" category, which includes the Covered Bridge product line, more than doubled from $1.4 million to $3.3 million.

Strategic Initiatives

FGI continues to execute its "Brands, Products, Channels" (BPC) growth strategy, focusing on product innovation and geographic expansion. The company highlighted several key initiatives in its presentation:

The company’s diversified portfolio spans multiple product categories and price points, with a global footprint that generates approximately 36.3% of revenue from international markets. FGI is particularly focused on expanding its presence in India and the UK, while it has decided to exit the Australasia market.

Product innovation remains central to FGI’s strategy, with the company noting that its FLUSH GUARD technology is gaining market acceptance, while JETCOAT and Covered Bridge Cabinetry continue to show growth. These innovations are part of FGI’s broader effort to differentiate its offerings in a competitive market.

Financial Position & Outlook

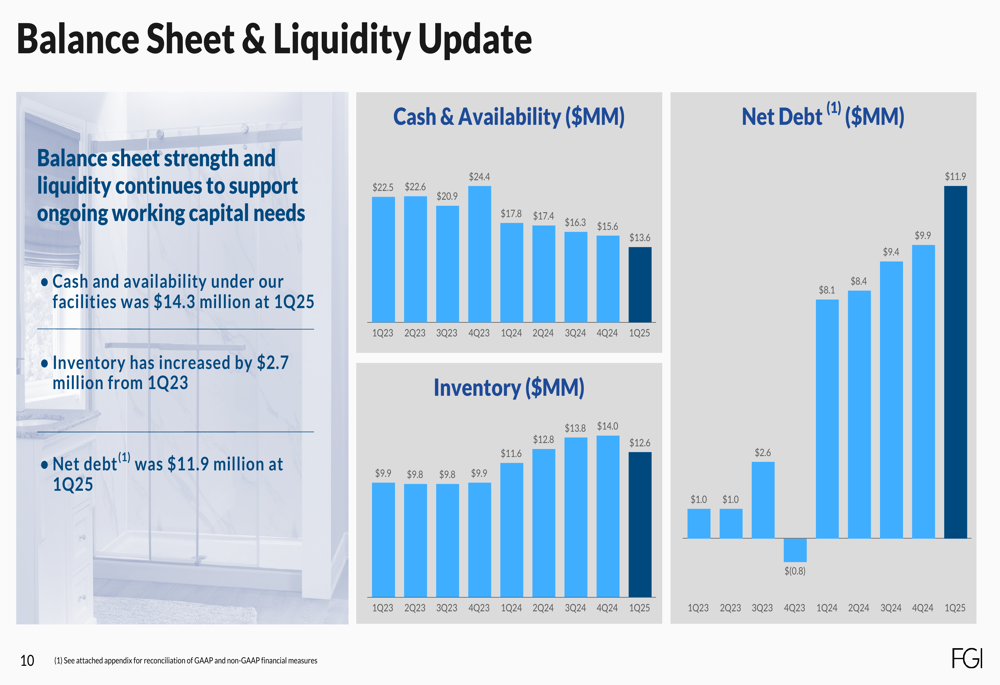

FGI’s balance sheet shows increasing pressure, with net debt rising to $11.9 million in Q1 2025 from $9.9 million in Q4 2024 and just $1.0 million in Q1 2023. Cash and availability decreased to $13.6 million, continuing a downward trend from $15.6 million in Q4 2024 and $24.4 million in Q4 2023.

The following chart illustrates these concerning trends:

On a positive note, inventory levels decreased to $12.6 million from $14.0 million in the previous quarter, suggesting improved inventory management or potentially reduced stocking in response to uncertain demand.

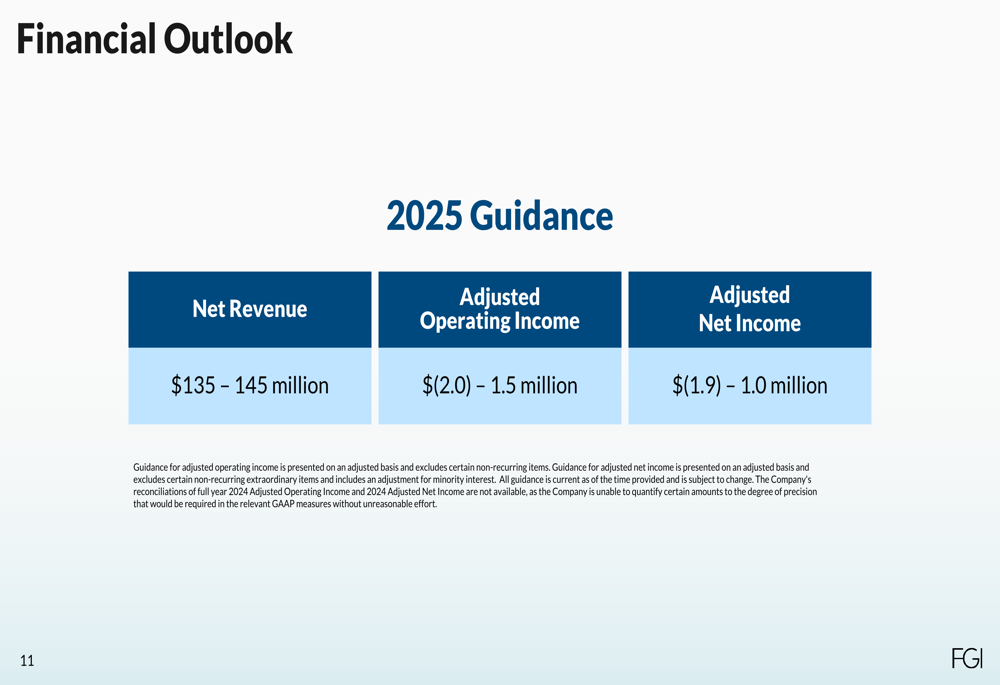

For fiscal year 2025, FGI provided the following guidance:

The company expects full-year revenue between $135-145 million, with adjusted operating income ranging from $(2.0) million to $1.5 million and adjusted net income between $(1.9) million and $1.0 million. This guidance reflects continued revenue growth but acknowledges ongoing profitability challenges.

Forward-Looking Statements

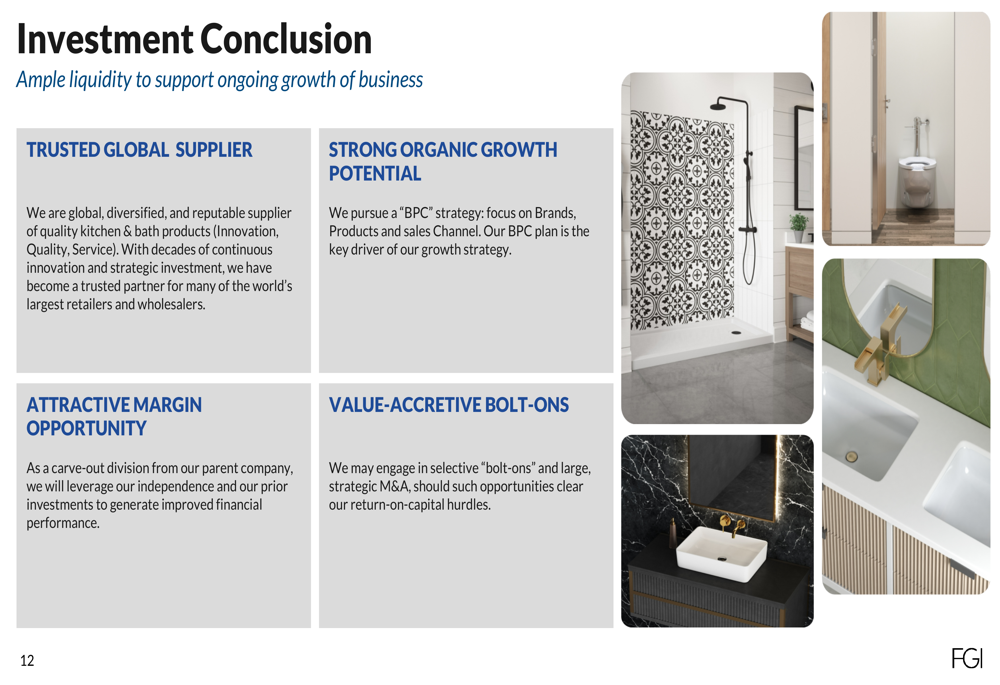

FGI’s management emphasized that the demand outlook remains "clouded by the tariff environment," suggesting potential headwinds for the remainder of 2025. Despite these challenges, the company maintains that it has "ample liquidity to support ongoing growth" and continues to position itself as a trusted global supplier with strong organic growth potential.

The company’s investment thesis centers on four key pillars: being a trusted global supplier, having strong organic growth potential, presenting an attractive margin opportunity, and pursuing value-accretive bolt-on acquisitions. However, the declining profitability metrics and increasing debt levels raise questions about the company’s ability to achieve its margin improvement goals in the near term.

FGI’s performance in the coming quarters will be crucial in determining whether its strategic initiatives can successfully address the profitability challenges while maintaining revenue growth in an increasingly complex global trade environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.