Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Fincantieri SpA (BIT:FCT) presented its Q1 2025 results on May 12, 2025, showcasing strong financial performance across all business segments. Despite reporting significant growth in key metrics, the company’s stock fell 6.44% in market trading, closing at €12.27, suggesting a disconnect between operational performance and investor sentiment.

The Italian shipbuilding giant delivered impressive year-over-year improvements in revenue, profitability, and order intake while continuing its strategic expansion into the underwater segment. According to available market data, Fincantieri currently trades at a P/E ratio of 10.77, indicating a relatively modest valuation compared to industry peers.

Quarterly Performance Highlights

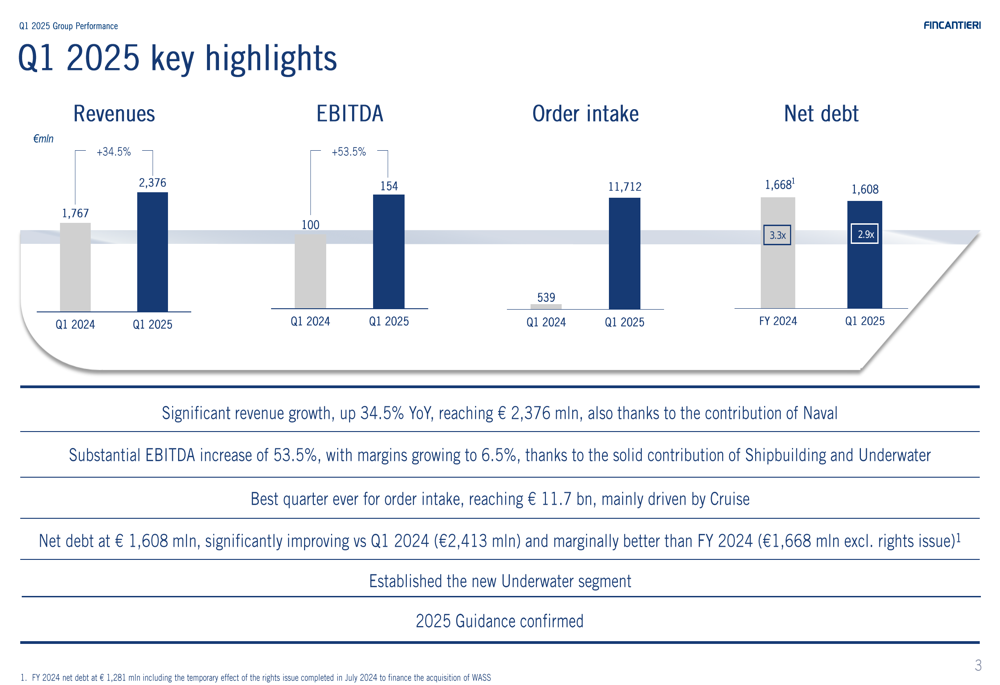

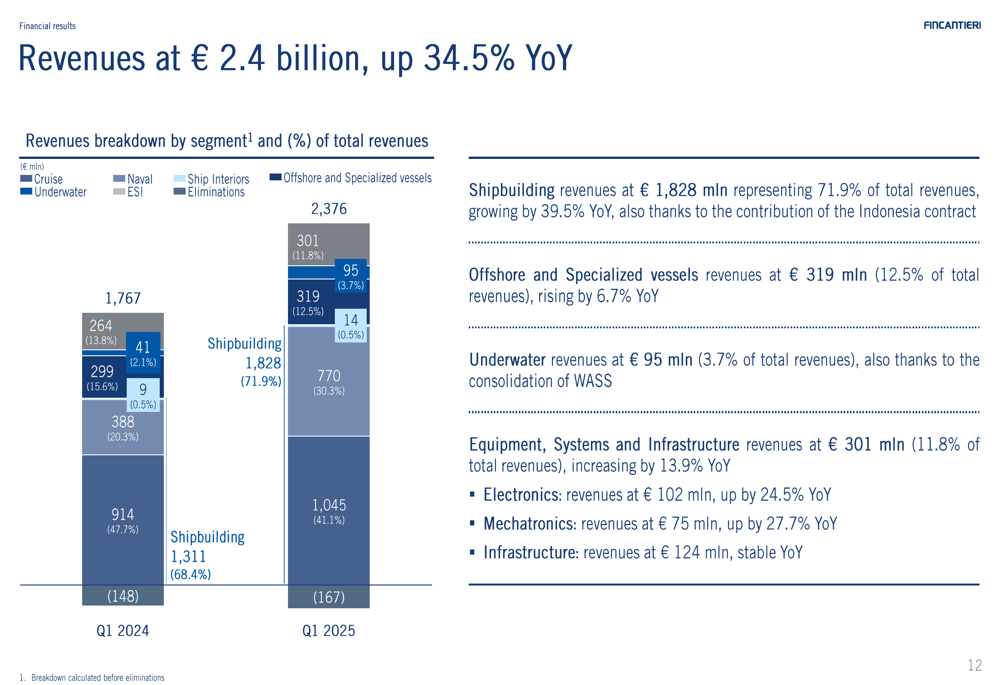

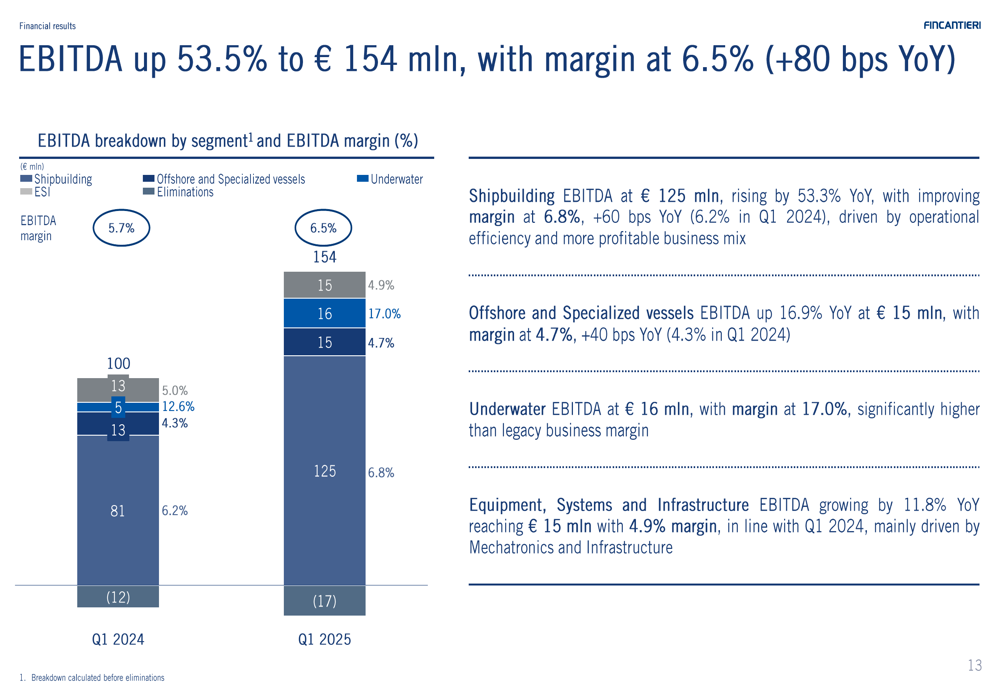

Fincantieri reported revenues of €2,376 million for Q1 2025, representing a substantial 34.5% increase compared to €1,767 million in the same period last year. EBITDA grew even more impressively at 53.5%, reaching €154 million versus €100 million in Q1 2024, with the EBITDA margin expanding by 80 basis points to 6.5%.

As shown in the following chart of key financial metrics:

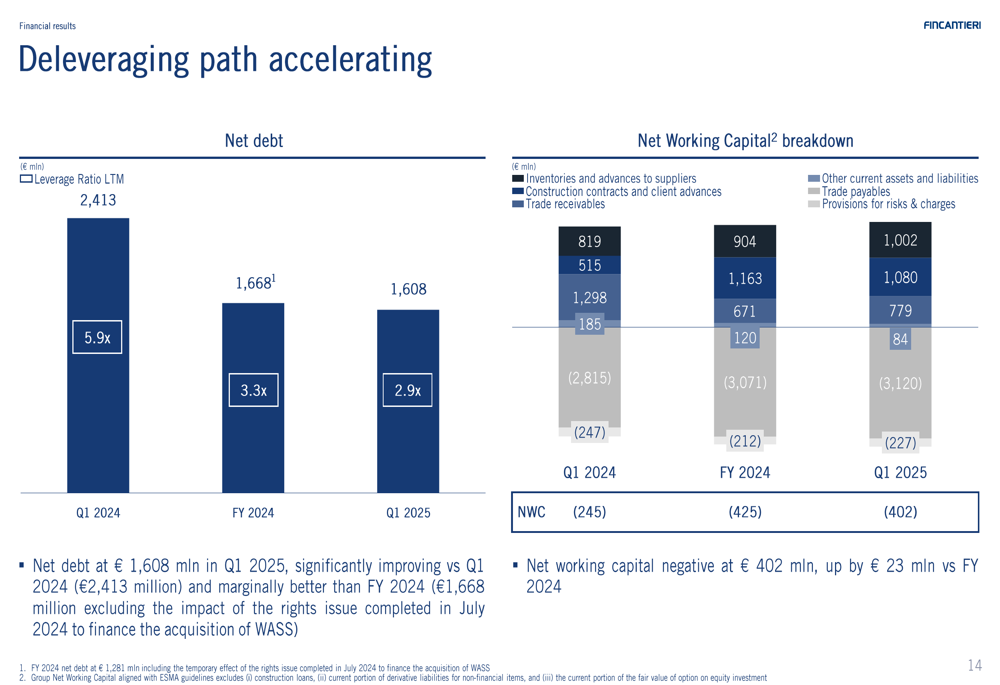

The company’s net debt position improved to €1,608 million, down from €1,668 million at the end of 2024 and significantly better than the €2,413 million reported in Q1 2024. This continued deleveraging demonstrates Fincantieri’s commitment to strengthening its balance sheet while pursuing growth opportunities.

The deleveraging trend is clearly illustrated in this visualization:

Order Intake and Backlog

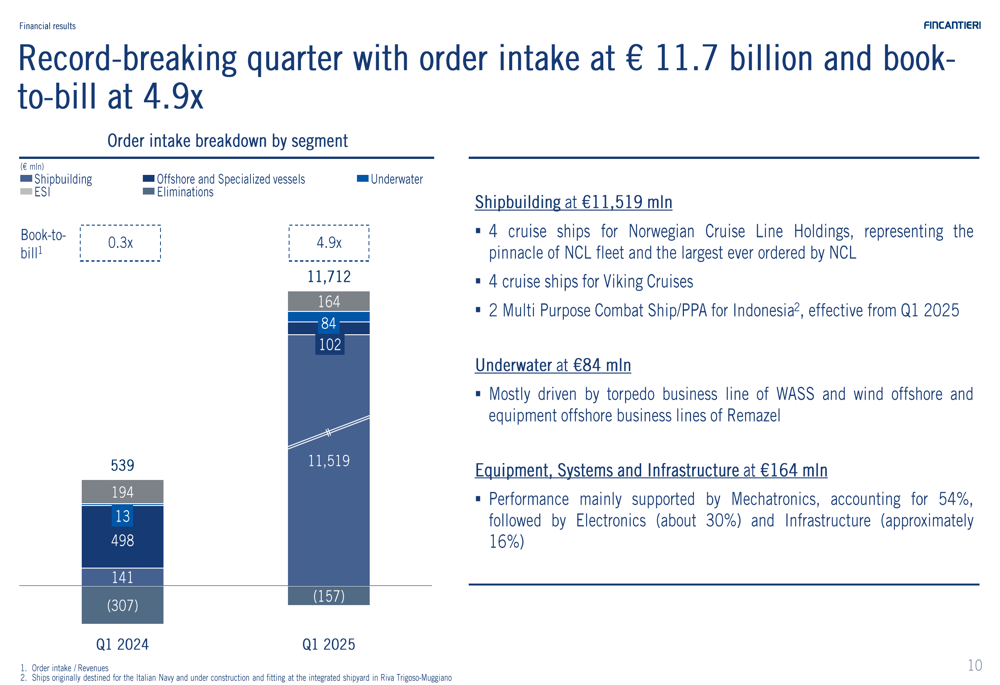

The first quarter of 2025 represented a record-breaking period for Fincantieri’s commercial activity, with order intake reaching an unprecedented €11,712 million compared to just €539 million in Q1 2024. This exceptional performance resulted in a book-to-bill ratio of 4.9x, indicating strong future revenue potential.

Major orders secured during the quarter included four cruise ships for Norwegian Cruise Line (NYSE:NCLH) Holdings, four cruise ships for Viking Cruises, and two Multi Purpose Combat Ships for Indonesia. These contracts have significantly expanded the company’s backlog, which grew by 30.2% to €40.3 billion compared to the end of 2024.

The following chart illustrates the record order intake breakdown by segment:

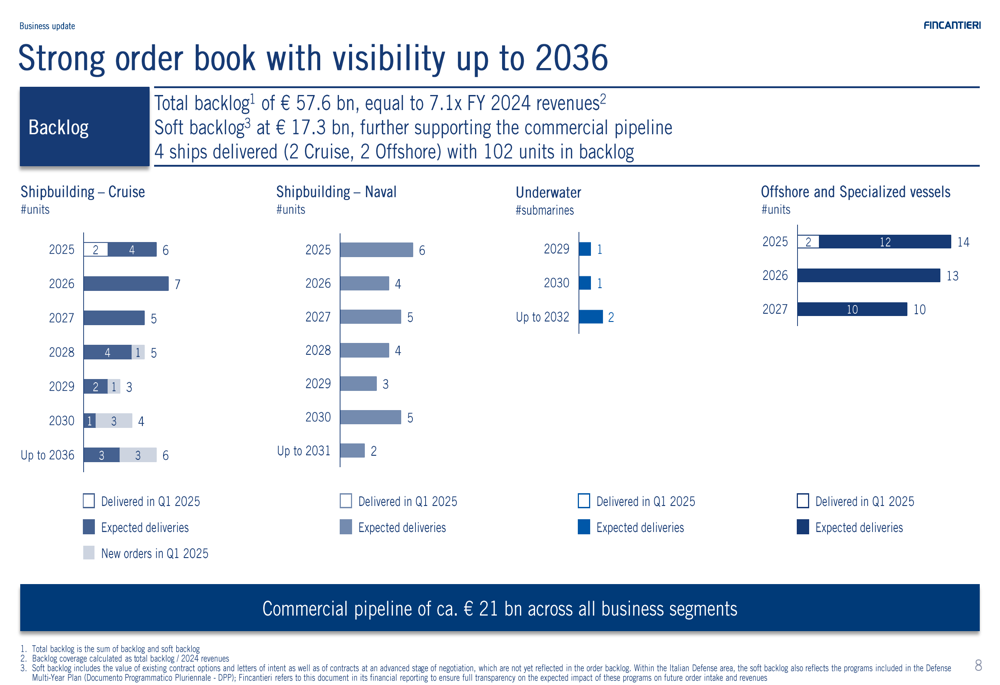

Total (EPA:TTEF) backlog, including both firm orders and soft backlog, reached €57.6 billion, equivalent to 7.1 times FY 2024 revenues. This provides exceptional visibility on future production, with scheduled deliveries extending all the way to 2036.

The strong order book visibility is demonstrated in this detailed breakdown:

Segment Performance

Fincantieri’s performance was robust across all business segments. The Shipbuilding division, which includes cruise and naval vessels, reported revenues of €1,828 million, up 39.5% year-over-year, with EBITDA rising 53.3% to €125 million and margin improving by 60 basis points to 6.8%.

The Offshore and Specialized Vessels segment generated revenues of €319 million, a 6.7% increase compared to Q1 2024, while EBITDA grew 16.9% to €15 million with a margin of 4.7%.

The following chart breaks down the company’s revenue by segment:

A notable development was the establishment of the new Underwater segment, which contributed €95 million in revenue and €16 million in EBITDA, achieving an impressive margin of 17.0% – the highest among all business segments.

The EBITDA performance across segments is illustrated in this breakdown:

The Equipment, Systems and Infrastructure division also performed well, with revenues increasing by 13.9% to €301 million and EBITDA growing by 11.8% to €15 million.

Strategic Initiatives

Fincantieri has updated its financial reporting structure to include the new Underwater business segment, reflecting the company’s strategic expansion into this high-margin area. Management highlighted their ambition to become a global leader in underwater technologies, capitalizing on growing defense budgets worldwide.

The company identified approximately €20 billion in commercial opportunities in the defense sector, leveraging its global footprint and technical capabilities. The staggered delivery schedule for cruise ships through 2036 provides a solid foundation for long-term revenue visibility, while the expansion into underwater systems represents a significant growth vector.

As summarized in the company’s concluding remarks:

Forward-Looking Statements

Fincantieri confirmed its 2025 guidance, expressing confidence in continued economic and financial outperformance relative to its Business Plan. Management emphasized the company’s "uniquely positioned investment story" built on three pillars: profitable growth in the cruise segment, defense opportunities, and expansion in the underwater dimension.

CEO Pietro Roberto Folgero highlighted the company’s strategic advancements, stating, "We are successfully implementing the group strategy in the underwater domain." He also emphasized the importance of digitalization and production capacity as key competitive advantages.

Despite the strong operational performance and positive outlook, investors appeared cautious, as reflected in the 6.44% stock price decline following the results announcement. This reaction may stem from broader market conditions or sector-specific concerns rather than company fundamentals, as Fincantieri’s financial metrics and order book suggest a robust growth trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.