US stock futures steady with China trade talks, Q3 earnings in focus

Finning International Inc . (TSX:FTT) shares rose 2.24% following the release of its Q2 2025 results presentation on August 6, 2025, which showed improved earnings per share despite flat revenue growth. The company’s stock closed at $61.64, approaching its 52-week high of $62.78, as investors responded positively to the equipment dealer’s operational efficiency and strong backlog figures.

Quarterly Performance Highlights

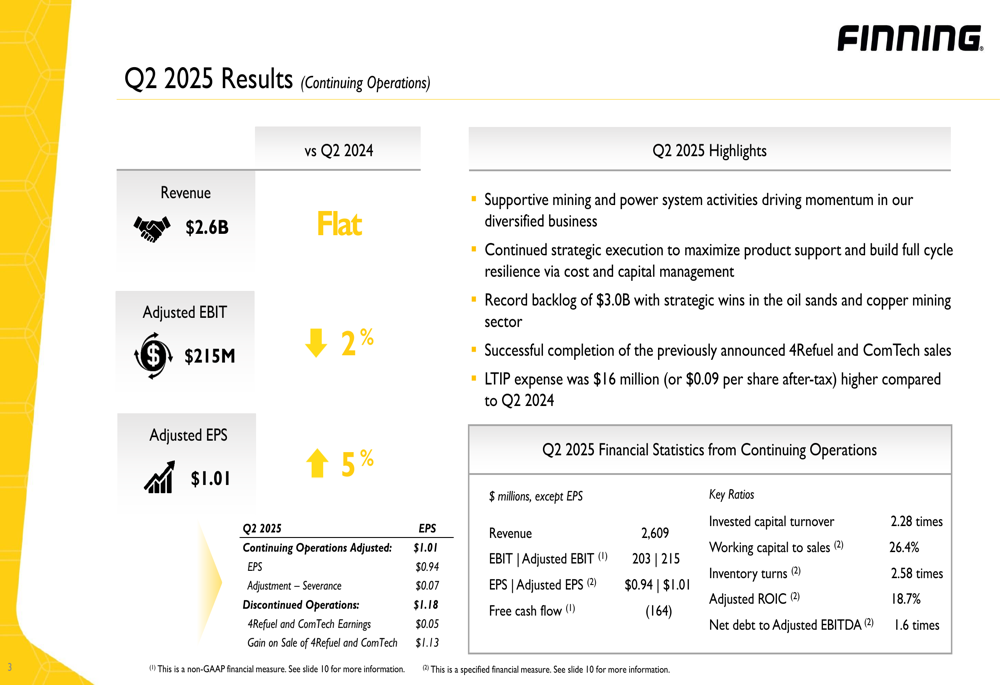

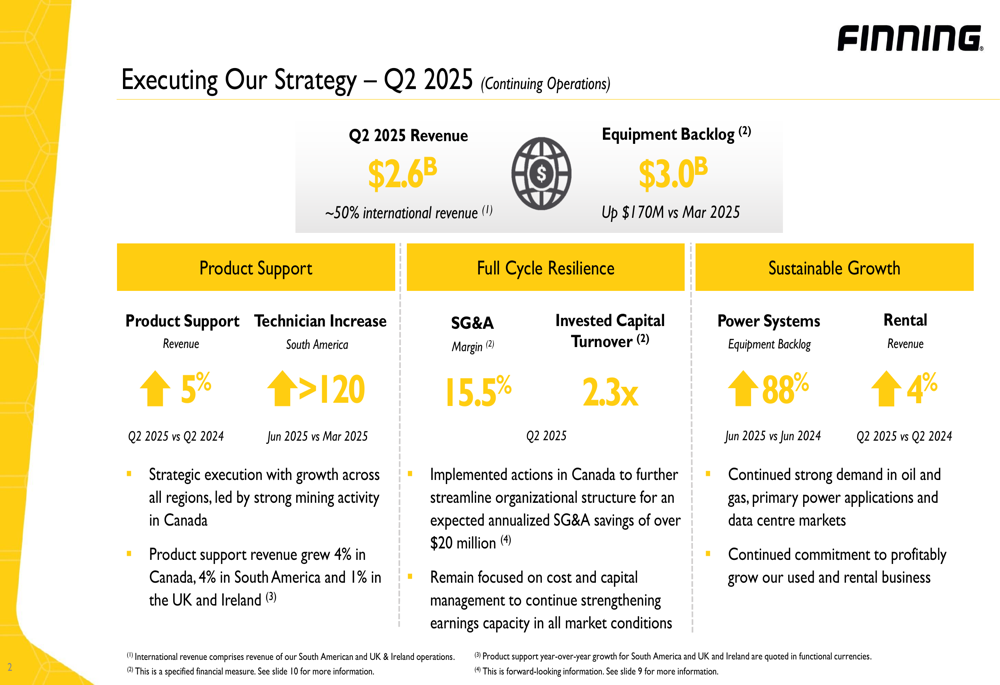

Finning reported Q2 2025 revenue of $2.6 billion, essentially flat compared to the same period last year, while adjusted earnings per share increased 5% year-over-year to $1.01. The company’s equipment backlog reached $3.0 billion, up $170 million from March 2025, providing visibility into future revenue streams.

"We continued our strategic execution with growth across all regions led by strong mining activity in Canada," noted the company in its presentation, highlighting a 5% increase in product support revenue compared to Q2 2024.

As shown in the following overview of key financial metrics:

While revenue remained flat, the company’s adjusted EBIT of $215 million represented a slight 2% decrease from Q2 2024. However, free cash flow was negative at $164 million, a significant contrast to the positive $135 million reported in Q1 2025.

Detailed Financial Analysis

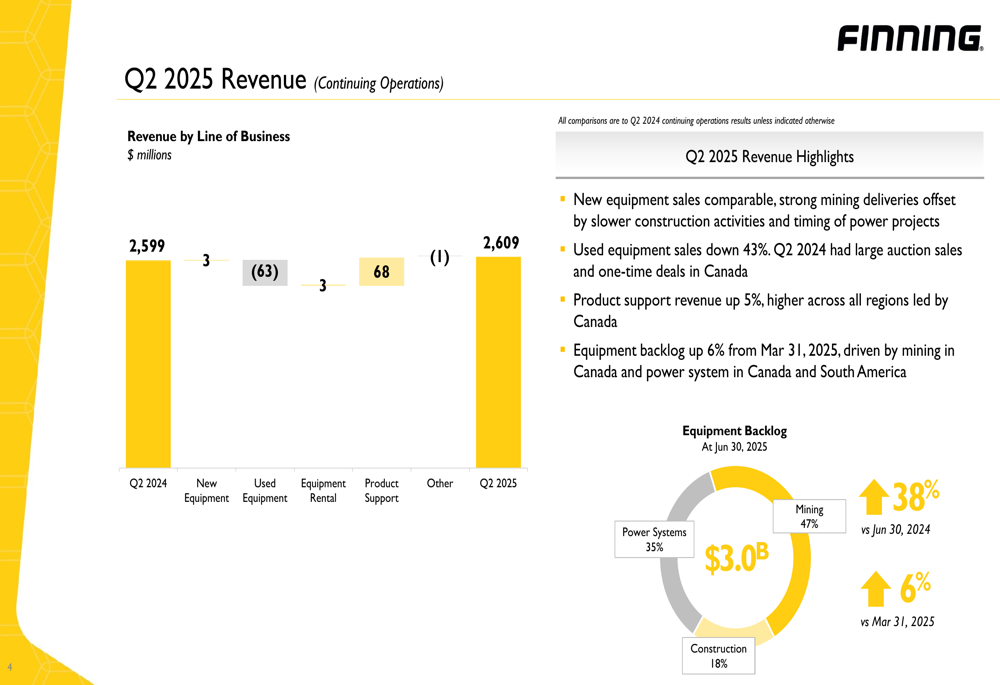

The company’s revenue composition showed significant shifts, with product support revenue increasing by $68 million (5%) year-over-year, while used equipment sales declined by $63 million (43%). New equipment sales remained relatively stable.

The following breakdown illustrates these revenue changes and the composition of the company’s growing backlog:

Notably, the equipment backlog is heavily weighted toward mining (47%) and power systems (35%), with mining backlog up 38% compared to June 2024. Power systems equipment backlog showed remarkable growth of 88% year-over-year, driven by strong demand in oil and gas, primary power applications, and data center markets.

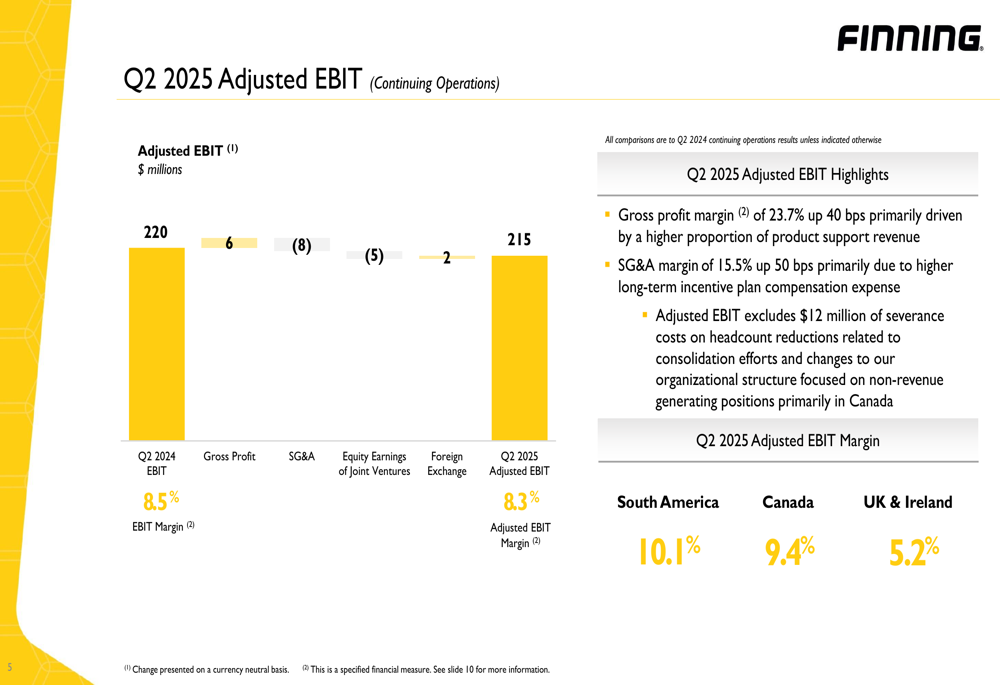

Despite flat revenue, Finning improved its gross profit margin to 23.7%, up 40 basis points from Q2 2024. However, this was offset by higher SG&A expenses, with SG&A margin increasing 50 basis points to 15.5%.

The following chart breaks down the components affecting adjusted EBIT:

Regional Performance

Finning’s operations across its three regions showed varying performance. The Canadian market delivered improved profitability despite revenue challenges, while South America maintained strong margins but showed signs of potential headwinds.

Canada

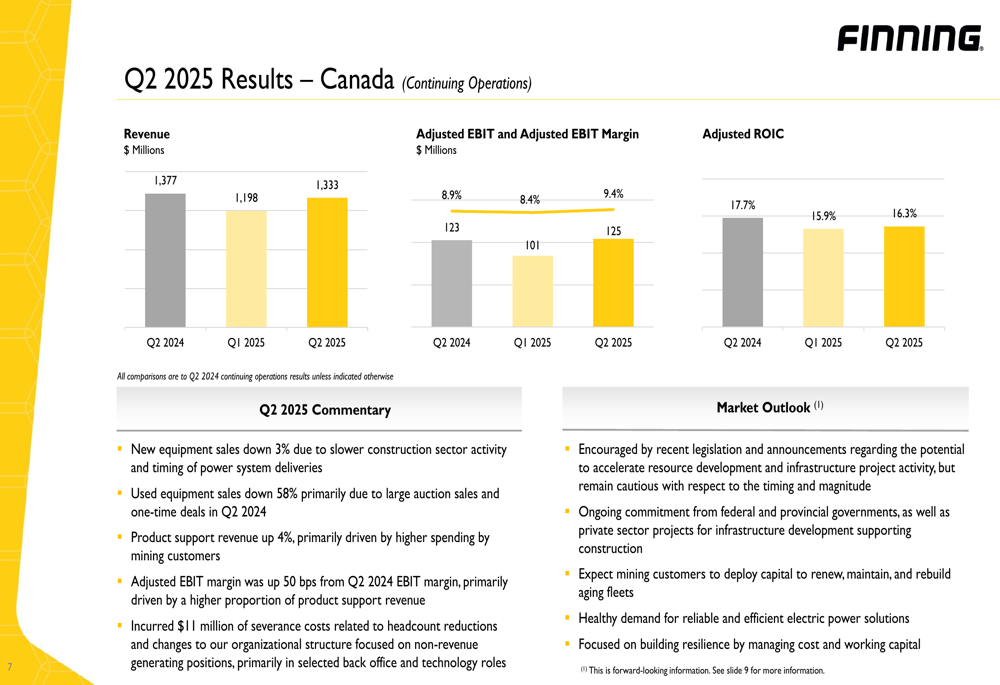

Canadian operations, which represent approximately half of Finning’s business, reported revenue of $1.33 billion in Q2 2025, down slightly from $1.38 billion in Q2 2024. Despite this, adjusted EBIT margin improved to 9.4%, up 50 basis points year-over-year.

The following chart details the Canadian performance metrics:

The company noted it had implemented actions in Canada to streamline organizational structure, incurring $11 million in severance costs but expecting annualized SG&A savings of over $20 million. Product support revenue in Canada grew by 4%, while new equipment sales declined 3% and used equipment sales dropped significantly by 58%.

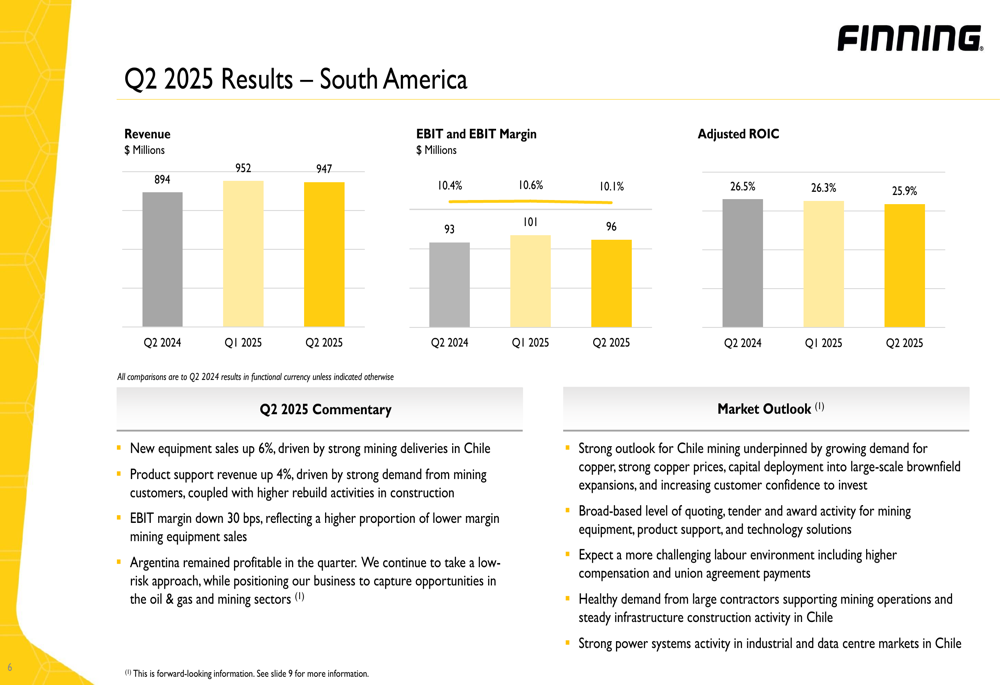

South America

South American operations continued to deliver the highest EBIT margins across Finning’s regions at 10.1%, though this represented a 30 basis point decline from Q2 2024. Revenue reached $947 million, up from $894 million in the same period last year.

The following chart illustrates South American performance:

New equipment sales in South America increased by 6% and product support revenue grew by 4%. The company highlighted that operations in Argentina remained profitable despite challenging economic conditions. Looking forward, Finning expects "a more challenging labor environment" in the region, which could pressure margins.

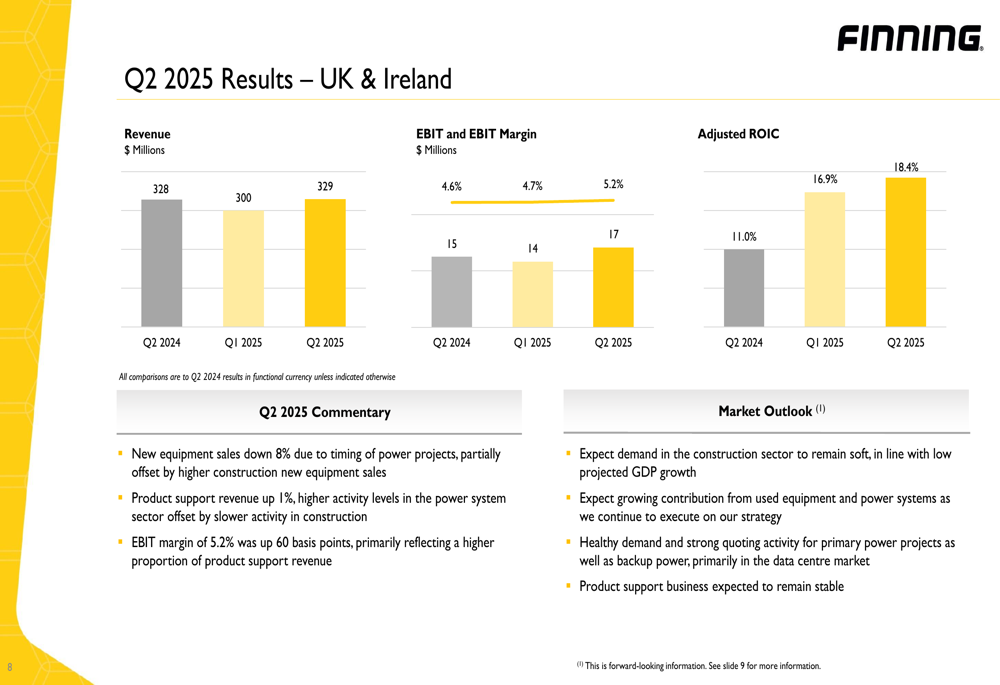

UK & Ireland

The UK & Ireland segment showed improvement in profitability despite market challenges, with EBIT margin increasing to 5.2%, up 60 basis points from Q2 2024. Revenue remained stable at $329 million.

The region saw an 8% decline in new equipment sales, offset partially by a 1% increase in product support revenue. Adjusted ROIC for the UK & Ireland improved significantly to 18.4%, up from 11.0% in Q2 2024, reflecting improved capital efficiency.

Strategic Initiatives & Outlook

Finning highlighted several strategic initiatives in its presentation, including continued investment in its technician workforce with more than 120 technicians added in South America between March and June 2025. The company also emphasized its commitment to "profitably grow our used and rental business" despite the current decline in used equipment sales.

The company’s overall strategy and key metrics are summarized in the following slide:

Looking ahead, Finning expressed cautious optimism about its markets. In Canada, the company is "encouraged by recent legislation" and expects mining customers to deploy capital. In South America, the outlook for Chilean mining remains strong, while the UK & Ireland construction sector is expected to "remain soft."

The power systems segment appears to be a particular bright spot, with "healthy demand and strong quoting activity for primary power projects" and continued strength in data center markets, which have contributed to the 88% year-over-year increase in power systems backlog.

Following a strong Q1 2025 where the company beat expectations with 7% revenue growth and an 18% increase in EPS, Q2 represents a more moderate performance but still demonstrates Finning’s ability to improve profitability metrics despite revenue challenges. The record $3 billion backlog provides a solid foundation for future quarters, though investors will be watching closely to see if the company can convert this backlog into revenue growth while managing potential labor challenges in South America.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.