Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

First Advantage Corp (NASDAQ:FA) released its Q1 2025 earnings presentation on May 8, 2025, highlighting flat revenue but improved margins driven by synergy realization from its Sterling acquisition. Despite the company’s positive messaging about exceeding expectations, the stock was down 8.48% in premarket trading, suggesting investor concerns about the company’s performance.

The background screening provider completed its acquisition of Sterling in late 2024, and this quarter’s results reflect the company’s ongoing integration efforts. The presentation emphasized strong execution, synergy realization, and cost discipline as key drivers of the quarter’s performance.

Quarterly Performance Highlights

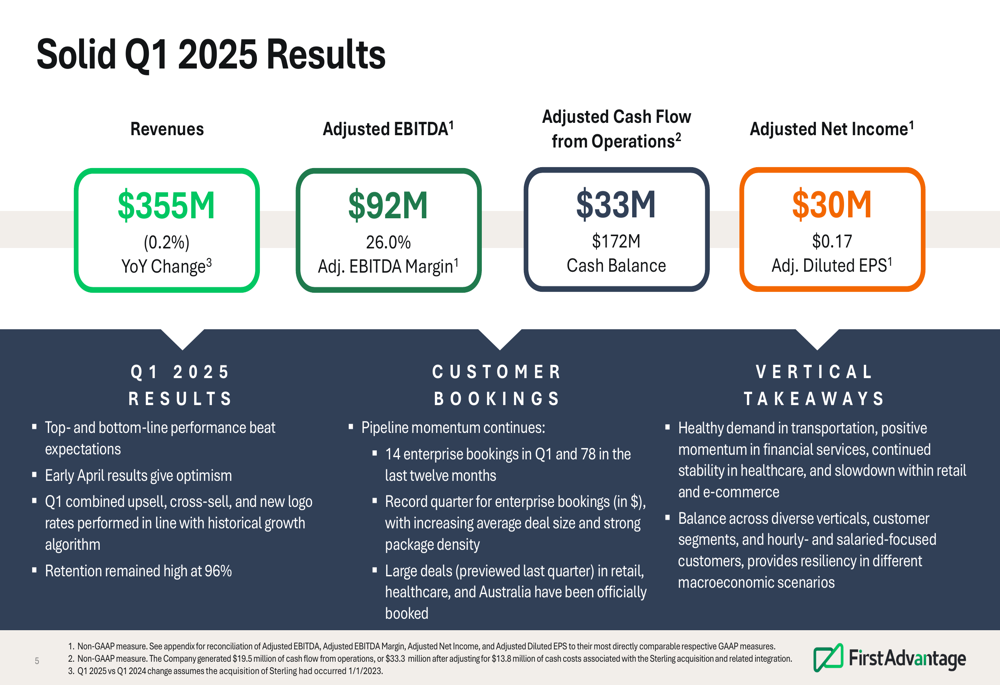

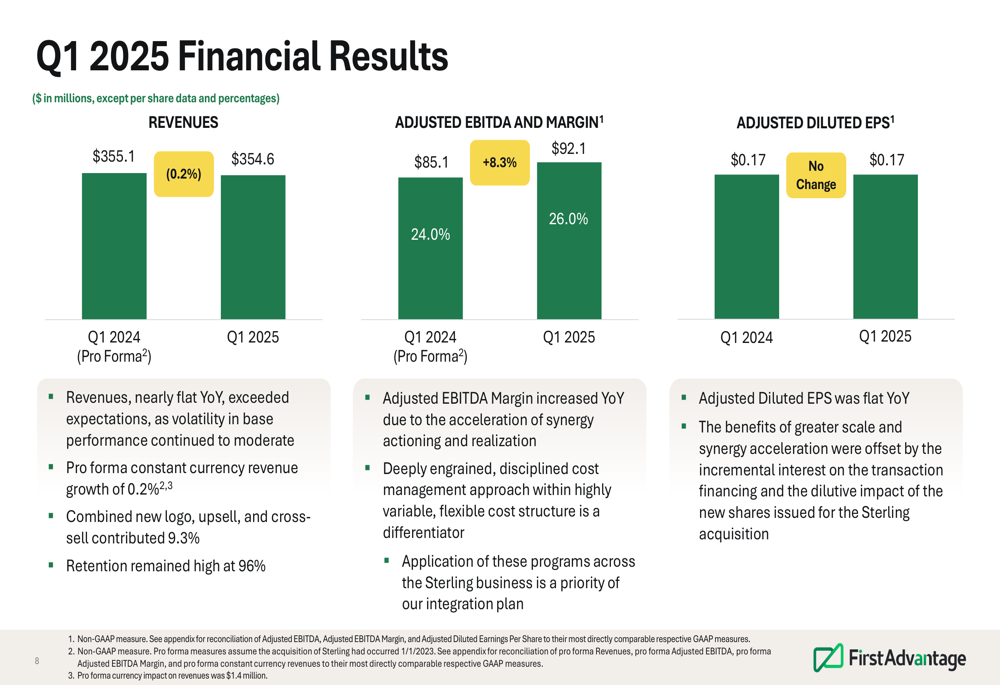

First Advantage reported Q1 2025 revenues of $355.1 million, representing a slight decline of 0.2% year-over-year, though the company noted this exceeded their expectations. On a constant currency basis, revenues grew 0.2%. More impressively, Adjusted EBITDA increased 8.3% to $92.1 million, with margins expanding from 24.0% to 26.0% year-over-year.

As shown in the following financial results summary:

The company maintained its high customer retention rate of 96% and reported 14 enterprise bookings in Q1, with 78 in the last twelve months. Management highlighted a record quarter for enterprise bookings in dollar terms, with increasing average deal size and strong package density.

A detailed comparison of Q1 2025 versus Q1 2024 financial results reveals the margin improvement despite flat revenue:

CEO Scott Staples noted that the company’s performance benefited from "strong execution, synergy realization, and cost discipline." The presentation highlighted varying performance across industry verticals, with healthy demand in transportation, positive momentum in financial services, continued stability in healthcare, and slowdown within retail and e-commerce.

Sterling Acquisition Synergies

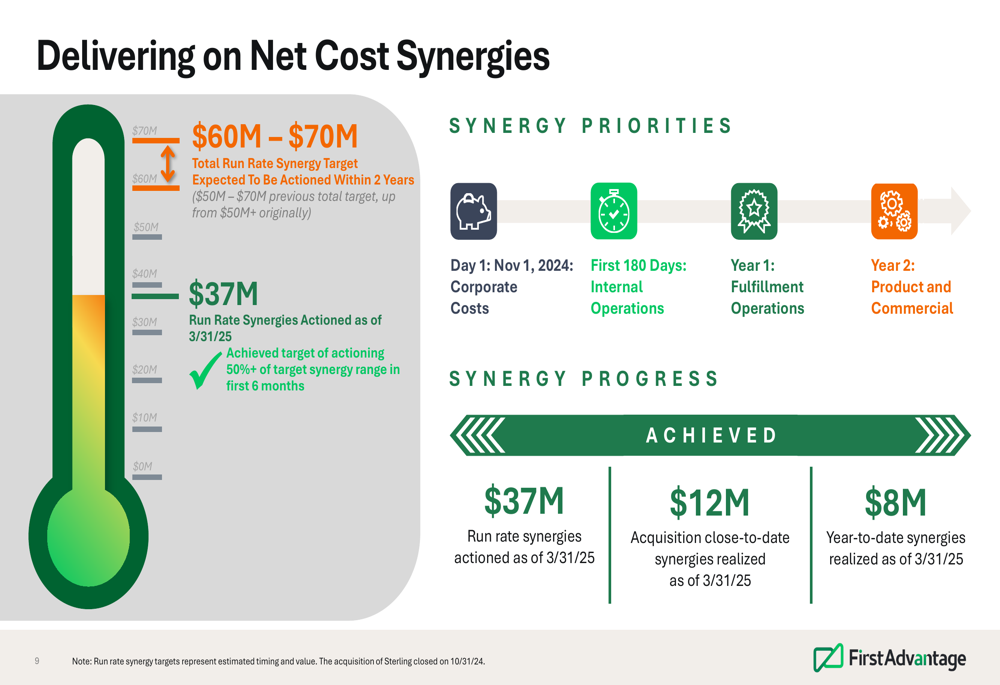

A significant focus of the presentation was on synergy realization from the Sterling acquisition. First Advantage increased its total run rate synergy target to $60-$70 million from the original $50+ million, expected to be actioned within two years of the acquisition.

The company reported substantial progress on this front, with $37 million in run rate synergies already actioned as of March 31, 2025, and $8 million in synergies realized year-to-date. This represents achievement of their target to action more than 50% of the target synergy range within the first six months post-acquisition.

The following chart illustrates the company’s synergy progress and timeline:

The synergy priorities follow a phased approach, starting with corporate costs on day one, followed by internal operations in the first 180 days, fulfillment operations in year one, and product and commercial synergies in year two.

Balance Sheet and Cash Flow

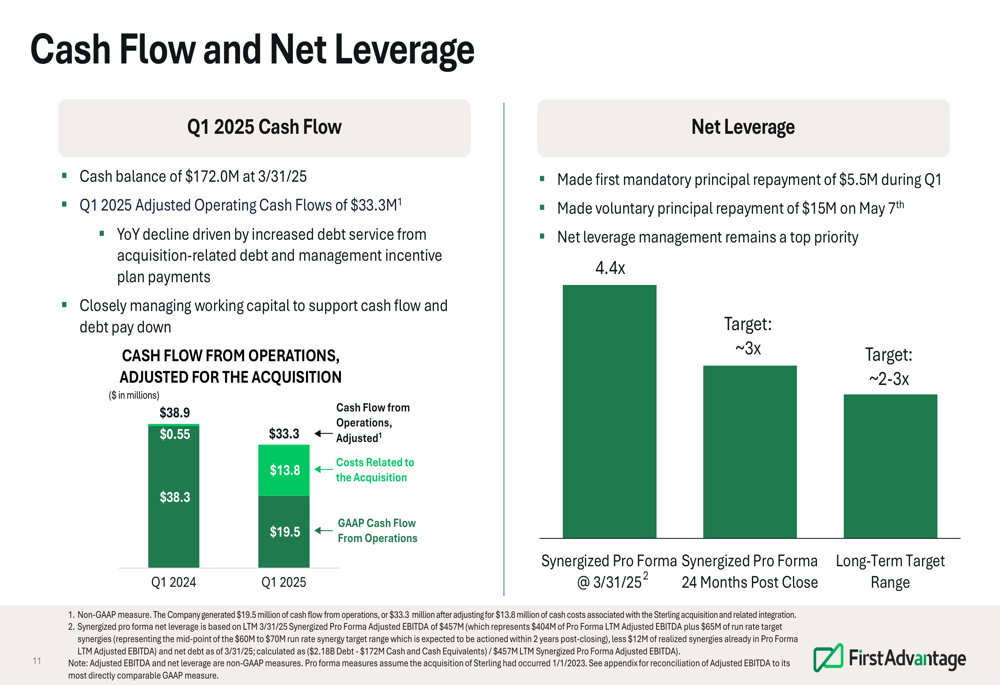

First Advantage reported a cash balance of $172.0 million as of March 31, 2025. The company generated $33.3 million in Adjusted Operating Cash Flows during Q1, representing a year-over-year decline of 14.5%, which management attributed to debt service and management incentive plan payments.

Deleveraging remains a top priority for the company. During Q1, First Advantage made its first mandatory principal repayment of $5.5 million and subsequently made a voluntary principal repayment of $15 million on May 7th. The company is targeting a net leverage ratio of approximately 3x within 24 months of the Sterling acquisition closing, with a longer-term target of 2-3x.

The following chart shows the company’s cash flow and net leverage information:

Forward Guidance

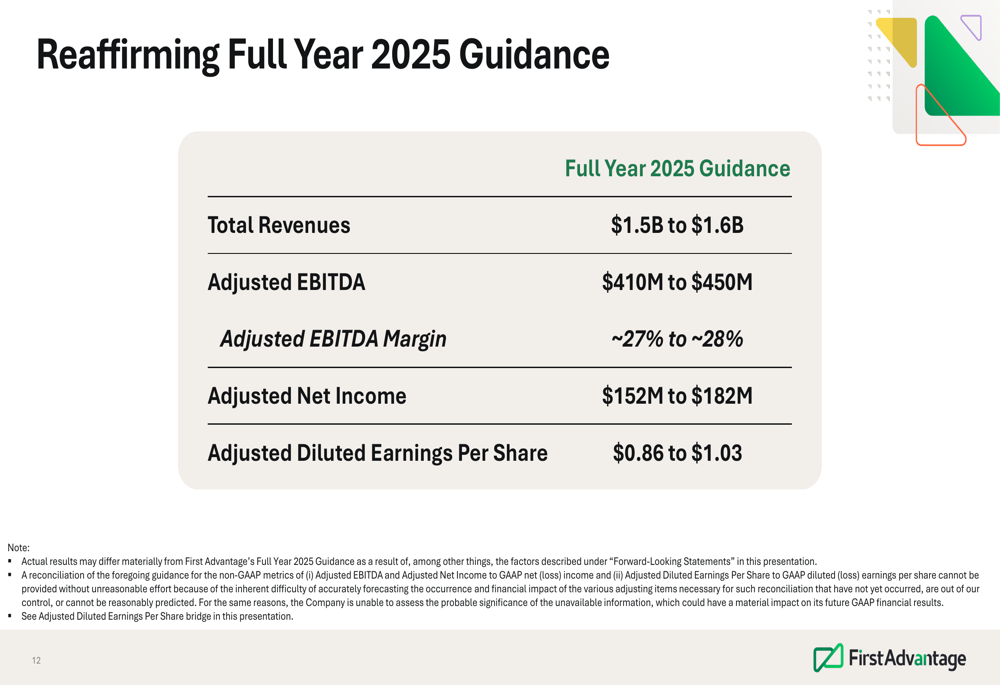

First Advantage reaffirmed its full year 2025 guidance, projecting:

- Total (EPA:TTEF) Revenues: $1.5 billion to $1.6 billion

- Adjusted EBITDA: $410 million to $450 million

- Adjusted EBITDA Margin: ~27% to ~28%

- Adjusted Net Income: $152 million to $182 million

- Adjusted Diluted Earnings Per Share: $0.86 to $1.03

The company’s guidance is displayed in the following table:

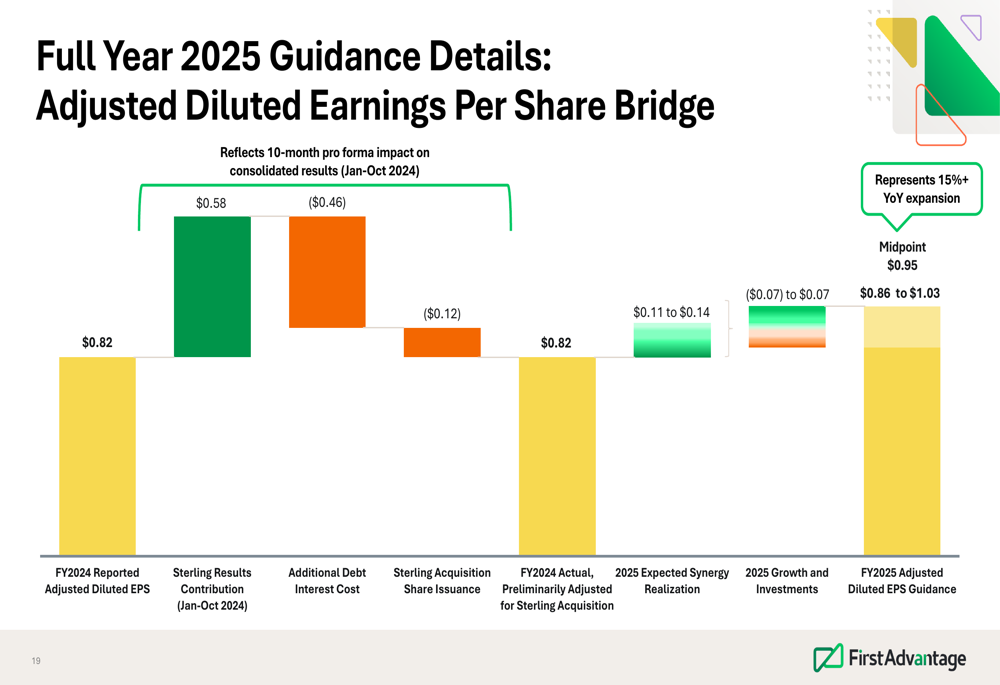

Management expects to realize $30-$35 million in actioned synergies in 2025. The company also provided a detailed bridge from FY2024 Reported Adjusted Diluted EPS of $0.82 to the FY2025 guidance midpoint of $0.95, showing the positive impact of Sterling results contribution and synergy realization, offset by additional debt interest costs and share issuance dilution:

Market Reaction and Analyst Perspectives

Despite the company’s positive messaging about exceeding expectations, First Advantage’s stock was down 8.48% in premarket trading at $13.70, according to available data. This follows a challenging Q4 2024, when the company missed EPS expectations, resulting in a significant stock decline.

The market reaction suggests investors may be concerned about the flat revenue growth, despite margin improvements. The company’s Q4 2024 earnings report had shown an EPS of $0.18, below the forecasted $0.23, which led to a 13.89% drop in the stock price at that time.

First Advantage is planning to hold its inaugural Investor Day on May 28, 2025, in New York City, which may provide more clarity on the company’s long-term strategy and growth prospects. The event will also be available via live webcast for investors unable to attend in person.

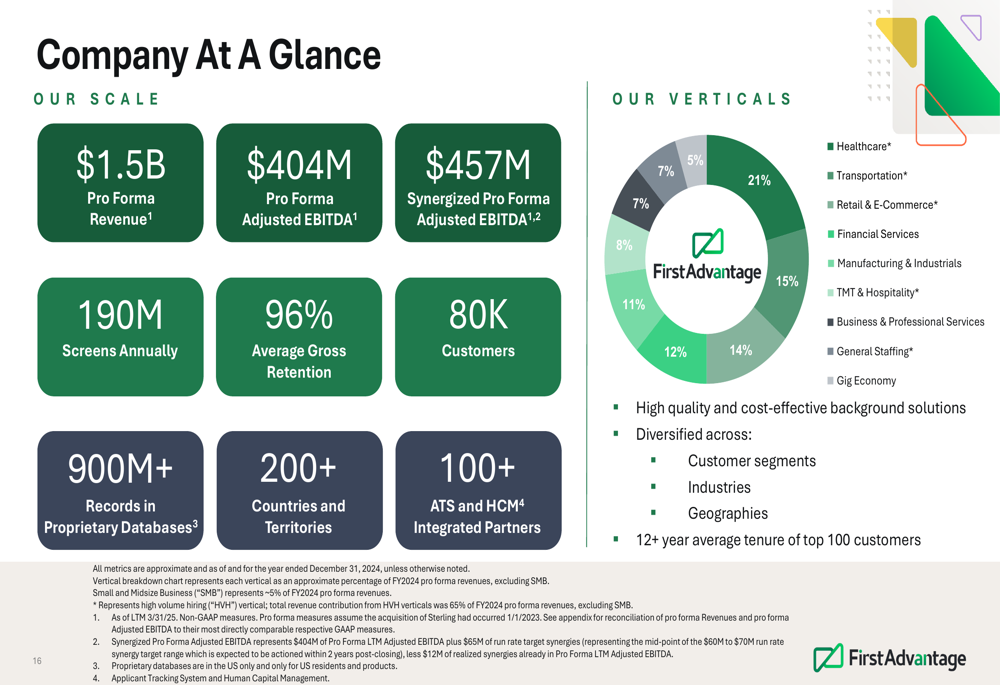

As the company continues to integrate Sterling and realize synergies, investors will be watching closely to see if First Advantage can maintain its margin improvements while returning to revenue growth in future quarters. The company’s diversification across customer segments, industries, and geographies, as shown in the following overview, may provide resilience in different macroeconomic scenarios:

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.