Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

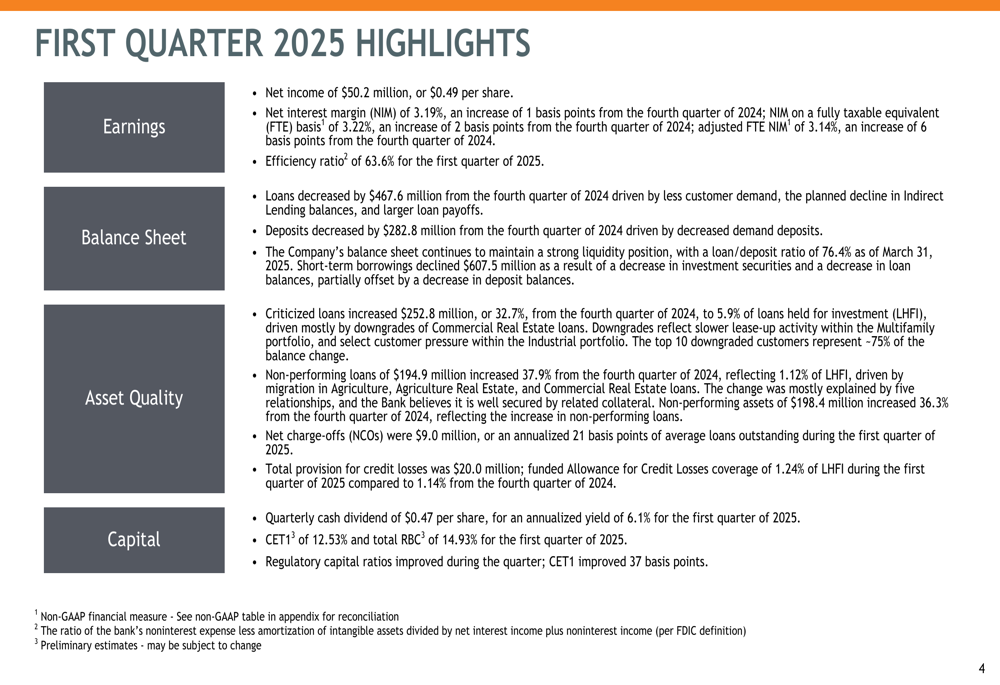

First Interstate BancSystem, Inc. (NASDAQ:FIBK) released its first quarter 2025 investor presentation on April 29, revealing mixed results with deteriorating asset quality metrics despite maintaining strong capital ratios. The bank reported net income of $50.2 million, or $0.49 per share, representing a slight sequential decline from $0.50 per share in the previous quarter.

The Montana-based regional bank, which operates 300 branches across the western United States with $28.3 billion in assets, saw its stock decline 5.58% in after-hours trading following the presentation, suggesting investor concerns about the bank’s performance and outlook.

Quarterly Performance Highlights

First Interstate reported a net interest margin (NIM) of 3.19% for Q1 2025, a modest 2 basis point increase from the previous quarter. The efficiency ratio stood at 63.6%, showing slight improvement from 64.6% a year earlier. The bank maintained its quarterly cash dividend of $0.47 per share, representing an annualized dividend yield of 6.1%.

As shown in the following chart of quarterly highlights:

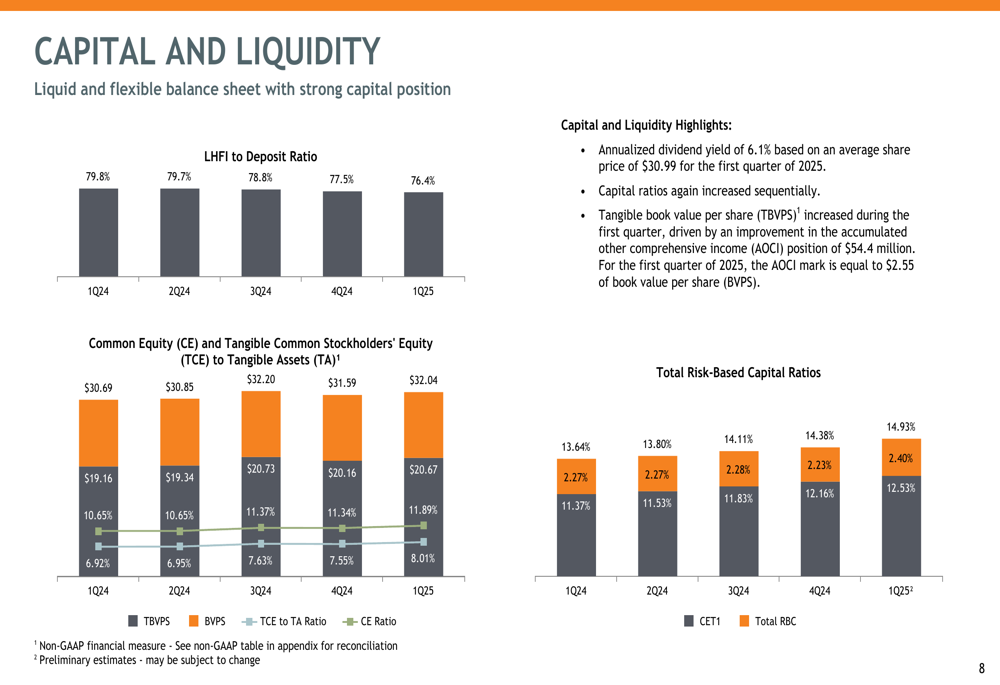

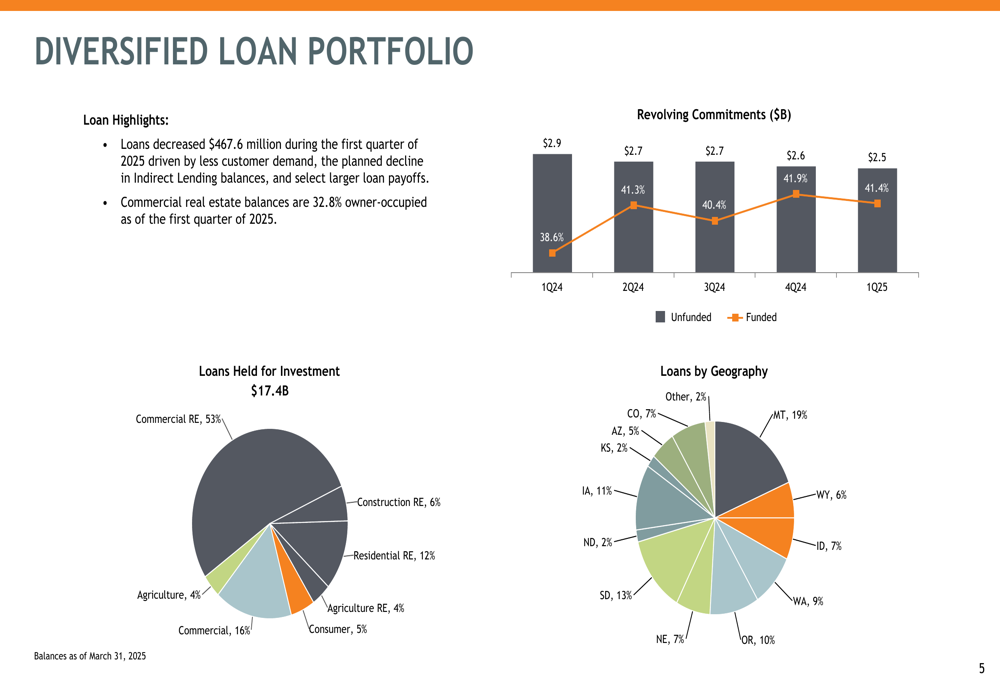

The bank’s balance sheet contracted during the quarter, with loans decreasing by $467.6 million and deposits declining by $282.8 million. This resulted in a loan-to-deposit ratio of 76.4%, down from 79.8% a year earlier, indicating increased liquidity but potentially lower earning asset deployment.

Asset Quality Concerns

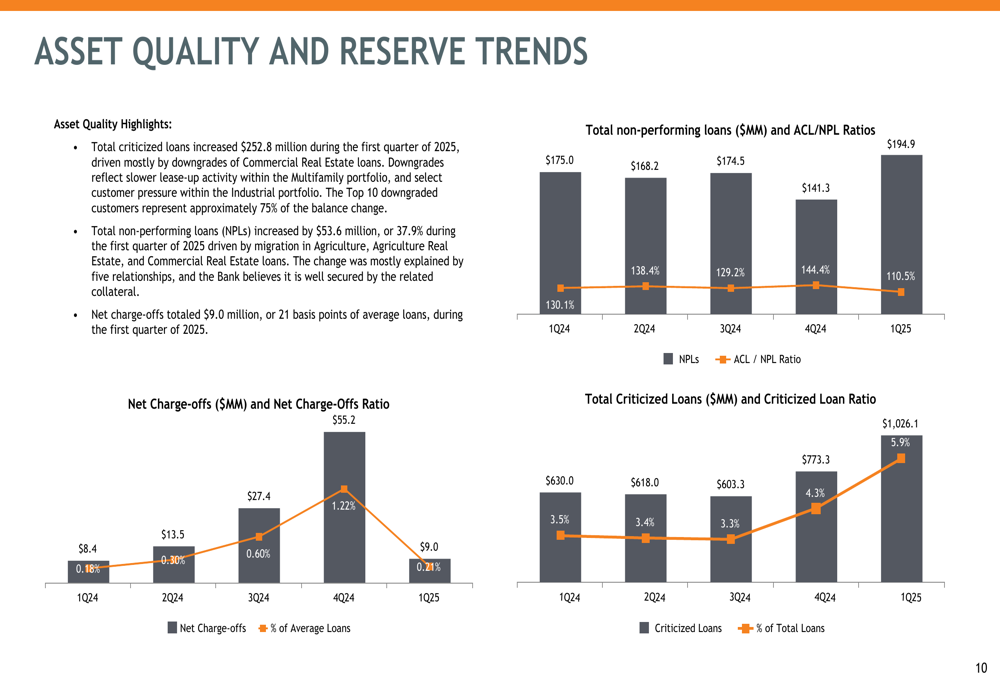

The most concerning aspect of First Interstate’s presentation was the significant deterioration in asset quality metrics. Criticized loans increased by $252.8 million during the quarter, while non-performing loans rose by $53.6 million. This trend represents a substantial increase from the previous year, with total criticized loans more than doubling from $430.0 million in Q1 2024 to $1,026.1 million in Q1 2025.

The following chart illustrates this concerning trend in asset quality metrics:

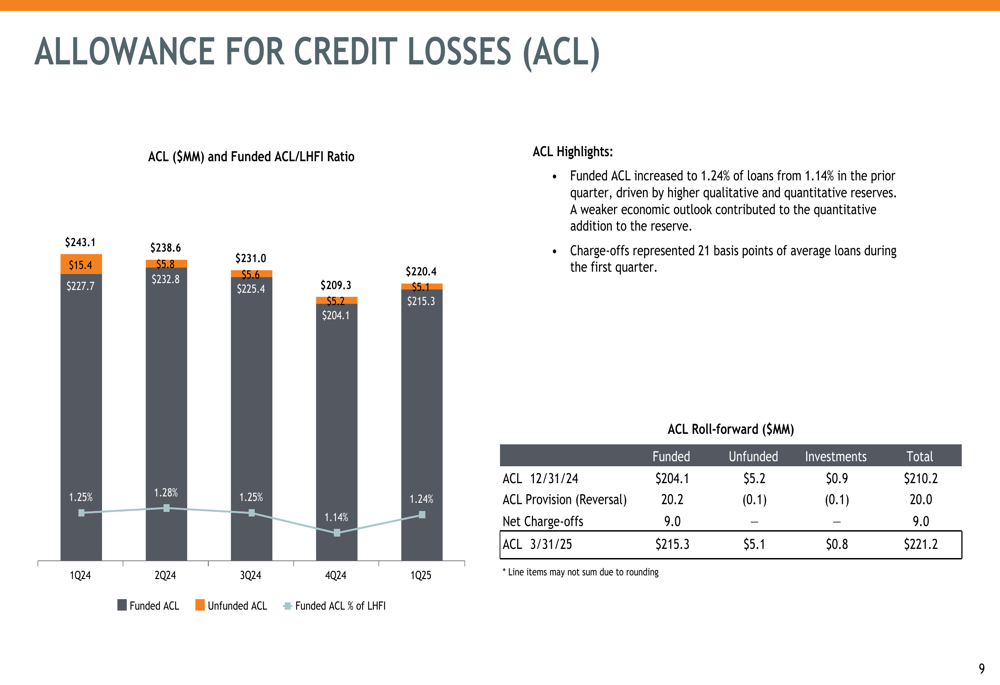

In response to these credit quality concerns, the bank increased its allowance for credit losses (ACL) to 1.24% of loans held for investment, up from 1.14% in the previous quarter. Net charge-offs for the quarter represented 21 basis points of average loans.

As shown in the following ACL chart:

Capital Position and Dividend

Despite the asset quality challenges, First Interstate maintained strong capital ratios, with Common Equity Tier 1 (CET1) at 12.53% and total risk-based capital at 14.93%. These ratios exceed regulatory requirements and provide a substantial buffer against potential loan losses.

The bank’s tangible book value per share increased to $20.67, up from $19.16 a year earlier, representing continued growth in shareholder equity despite the challenging operating environment.

The following chart shows the bank’s capital position trends:

Loan and Deposit Trends

First Interstate’s loan portfolio remains well-diversified across geographies and sectors, with commercial real estate representing 53% of total loans, followed by commercial loans at 16% and residential real estate at 12%. The bank’s geographic footprint spans multiple states, with Montana representing the largest concentration at 19% of loans.

The following chart details the composition of the bank’s loan portfolio:

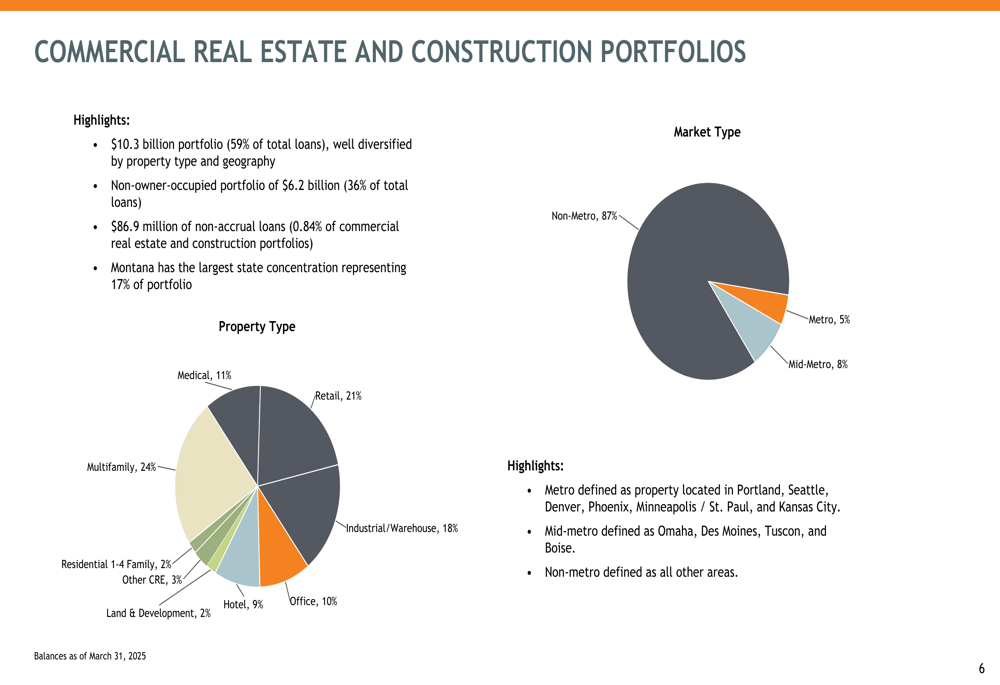

Within the commercial real estate portfolio, which totals $10.3 billion or 59% of total loans, the bank maintains diversification across property types with multifamily representing 24%, retail at 21%, and industrial/warehouse at 18%. The bank noted that 87% of its commercial real estate exposure is in non-metropolitan markets, potentially insulating it from some of the commercial real estate challenges facing major urban centers.

As illustrated in this breakdown of the commercial real estate portfolio:

On the funding side, First Interstate’s deposit base remains relatively stable in composition despite the overall decline in balances. Consumer deposits represent 46% of the total, with business deposits accounting for 54%. By account type, savings accounts make up 34% of deposits, demand deposits 26%, time deposits 27%, and non-interest-bearing accounts 14%.

Forward Guidance

Looking ahead, First Interstate provided guidance for 2025, anticipating modest loan and deposit growth, primarily in the second half of the year. This represents a shift from the current trend of declining balances and will require successful execution of the bank’s relationship banking strategy.

The bank expects net interest income to increase in 2025, driven by anticipated Federal Reserve rate cuts and the resulting positive impact on net interest margin. Non-interest income is projected to remain stable, while non-interest expenses are expected to increase modestly.

The guidance appears optimistic given the current trends, particularly the significant increase in criticized and non-performing loans. Investors will likely focus on whether the bank can stabilize asset quality metrics in the coming quarters while returning to balance sheet growth.

First Interstate’s presentation demonstrates that while the bank maintains strong capital and liquidity positions, it faces challenges in loan growth and asset quality that will require careful management in the quarters ahead. The high dividend yield may continue to attract income-focused investors, but the deteriorating credit metrics will likely remain a concern until a clear improvement trend emerges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.