Gold prices rebound after heavy losses; U.S.-China tensions resurface

Introduction & Market Context

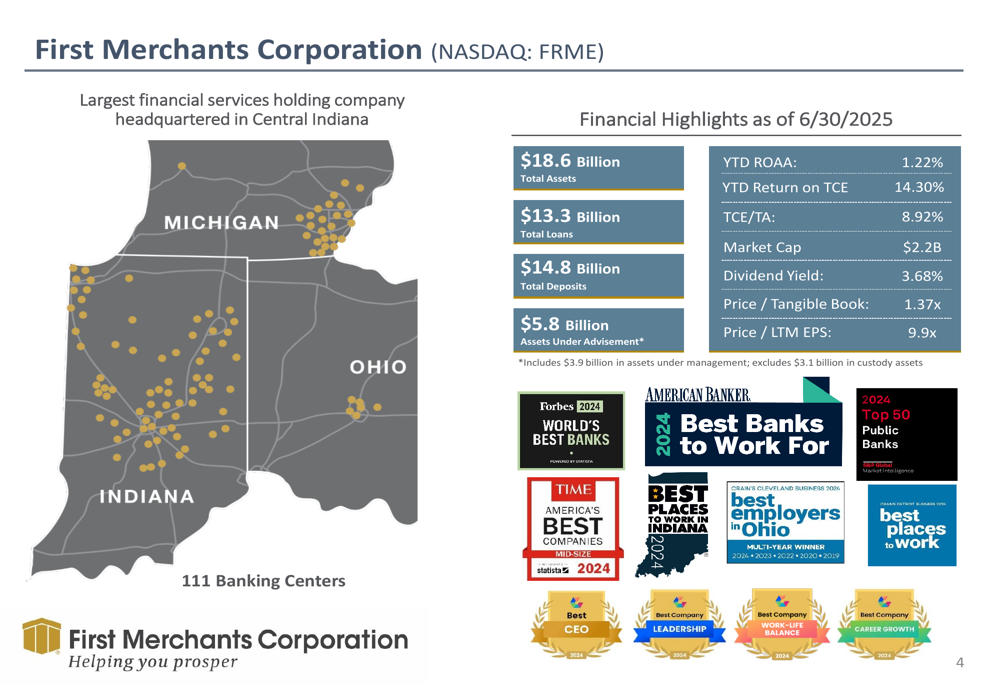

First Merchants Corporation (NASDAQ:FRME), a regional bank with a market cap of $2.2 billion, presented its second quarter 2025 results showcasing significant growth in profitability and strong commercial lending activity. The bank, which operates 111 banking centers primarily in Central Indiana, reported substantial improvements in key performance metrics compared to the same period last year.

As of October 14, 2025, First Merchants stock is trading at $36.71, up 2.29% for the day, reflecting positive investor sentiment following the company’s strong quarterly performance. The stock is currently trading at an attractive price-to-earnings ratio of 9.9x, suggesting potential undervaluation relative to its growth profile.

As shown in the following overview of the company’s position and recent recognitions:

Quarterly Performance Highlights

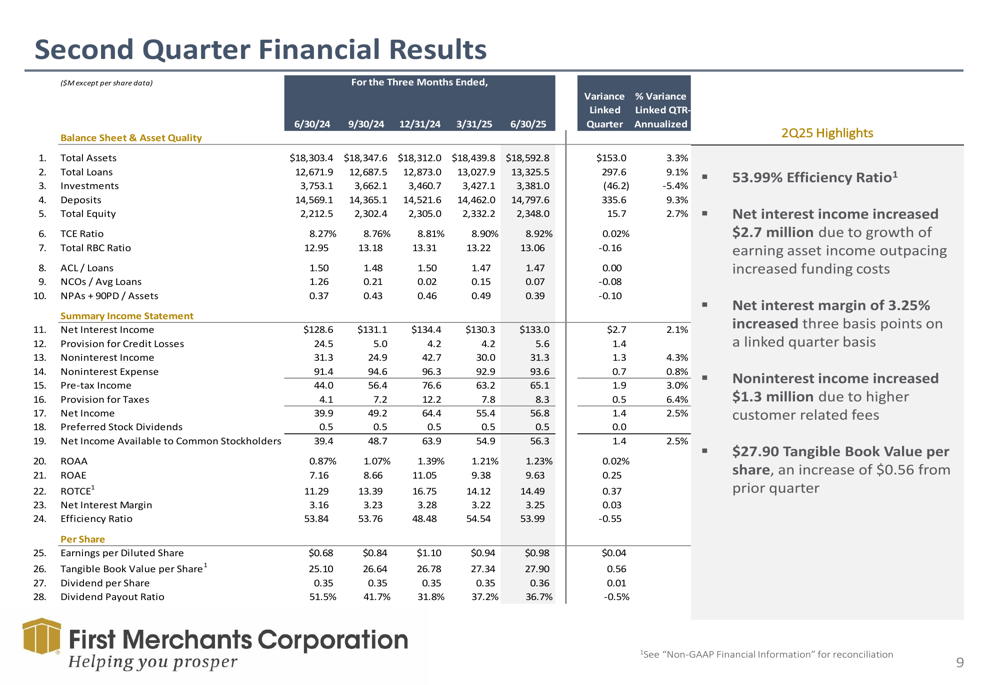

First Merchants reported net income of $56.4 million for Q2 2025, representing a substantial 44.1% increase compared to the same quarter in 2024. Earnings per share reached $0.98, also up 44.1% year-over-year, demonstrating the company’s ability to translate revenue growth into shareholder value.

The bank achieved a return on assets (ROA) of 1.23% and a pre-tax, pre-provision ROA of 1.53%, indicating strong core profitability. Return on equity (ROE) and return on tangible common equity (ROTCE) were 9.63% and 14.49%, respectively, reflecting efficient capital utilization.

The detailed second quarter results, showing significant improvement across multiple metrics, can be seen in the following financial summary:

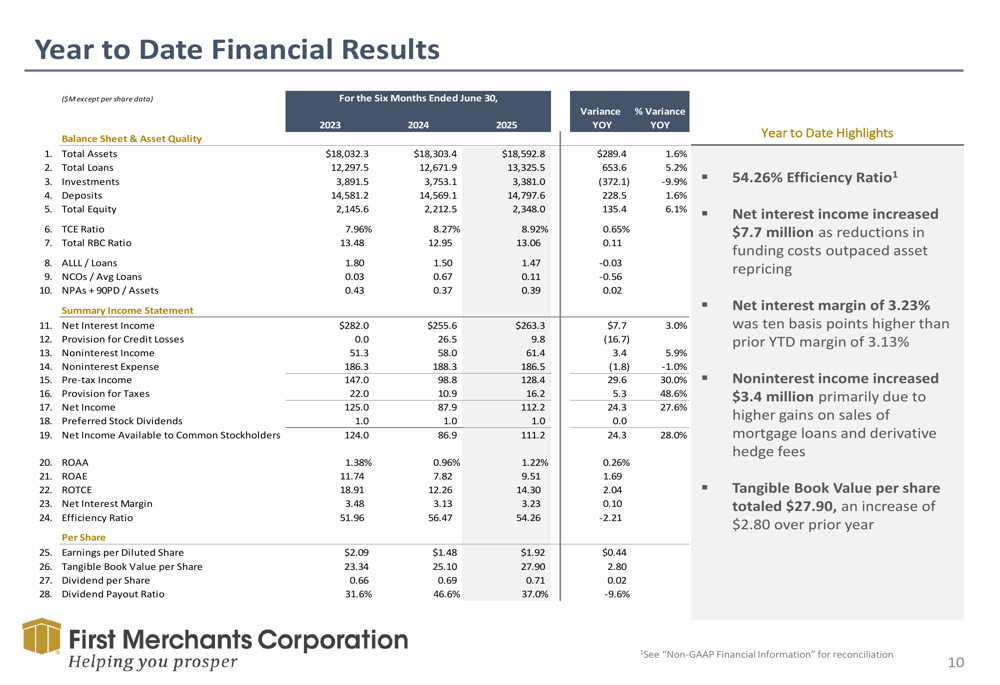

Year-to-date, First Merchants has generated net income of $111.2 million, or $1.92 per share, representing a 28% increase from the first half of 2024. This performance has been driven by growth in both net interest income and noninterest income, as well as disciplined expense management.

The year-to-date financial performance, highlighting the consistent improvement in key metrics, is illustrated below:

Loan and Deposit Portfolio Analysis

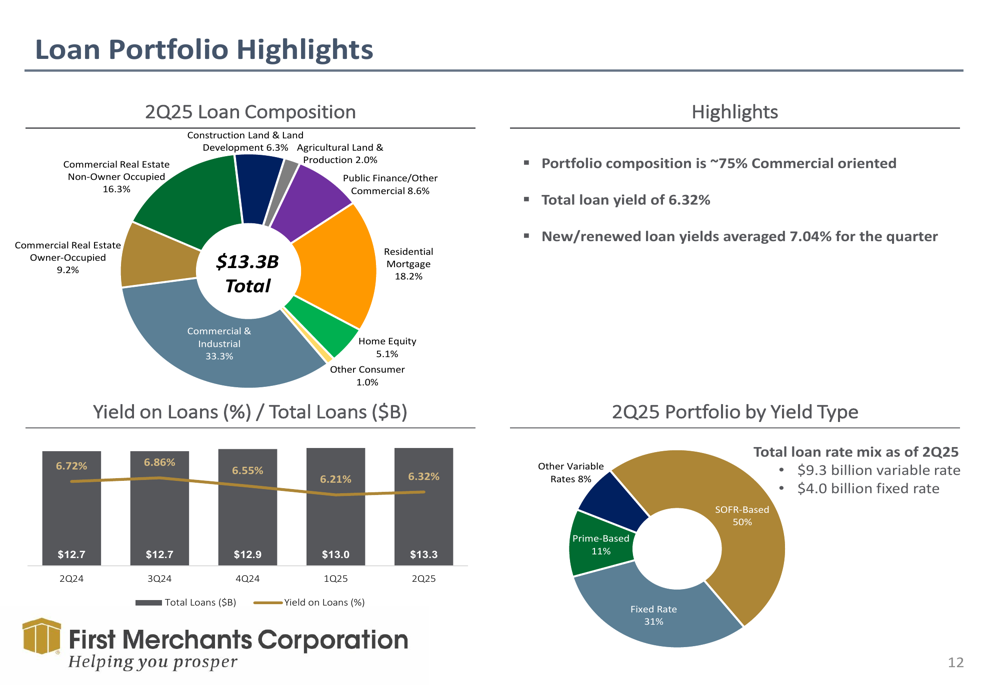

First Merchants reported robust loan growth during the second quarter, with total loans increasing by 9.1% on an annualized basis to reach $13.3 billion. Commercial loans, which grew by 10.7%, were the primary driver of this expansion, while consumer loans increased by a more modest 4.4%.

The loan portfolio remains well-diversified, with Commercial & Industrial loans representing the largest segment at 33.3%, followed by Residential Mortgage at 18.2% and Commercial Real Estate Non-Owner Occupied at 16.3%. This diversification helps mitigate concentration risks while allowing the bank to capitalize on various market opportunities.

The composition of the loan portfolio and its yield characteristics are detailed in the following chart:

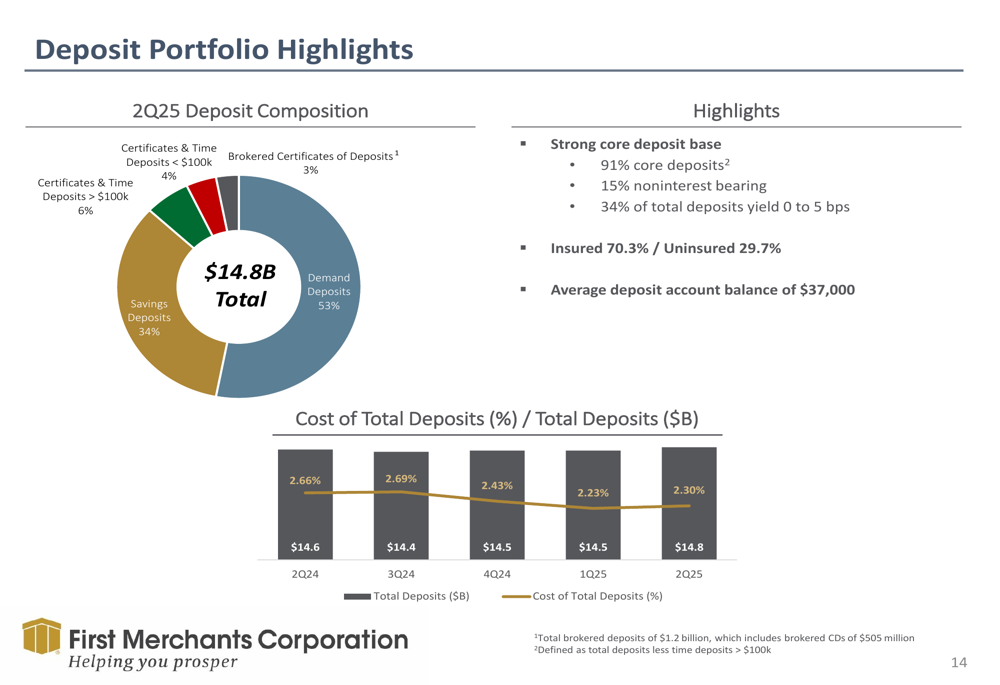

On the funding side, total deposits grew by 9.3% during the quarter to reach $14.8 billion. However, there was a notable divergence between commercial and consumer deposits. Commercial deposits increased by 19.5% or approximately $347 million, while consumer deposits declined by 7.4% or about $108 million, reflecting the competitive environment for retail deposits and the bank’s strategic focus on commercial relationships.

The deposit composition remains favorable with 53% in demand deposits and 34% in savings deposits, providing a stable and relatively low-cost funding base. The following chart illustrates the deposit portfolio breakdown:

Financial Metrics and Profitability

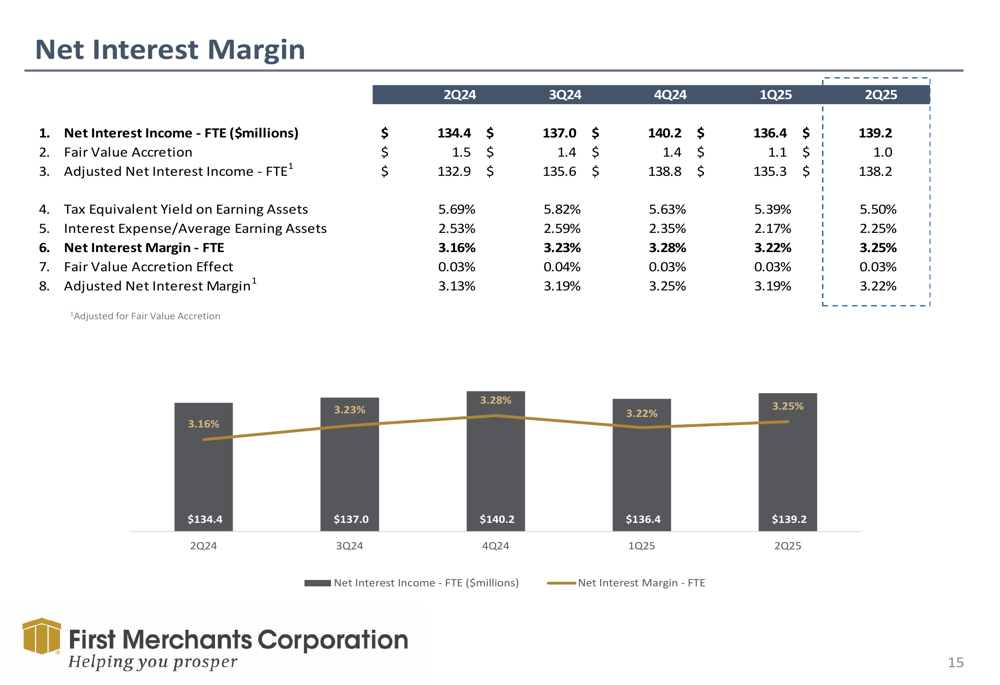

First Merchants’ net interest margin improved to 3.25% in Q2 2025, up from 3.16% in the same quarter last year. This expansion occurred despite the challenging interest rate environment, demonstrating the bank’s effective balance sheet management and pricing discipline.

The trend in net interest margin over the past year is shown in the following chart:

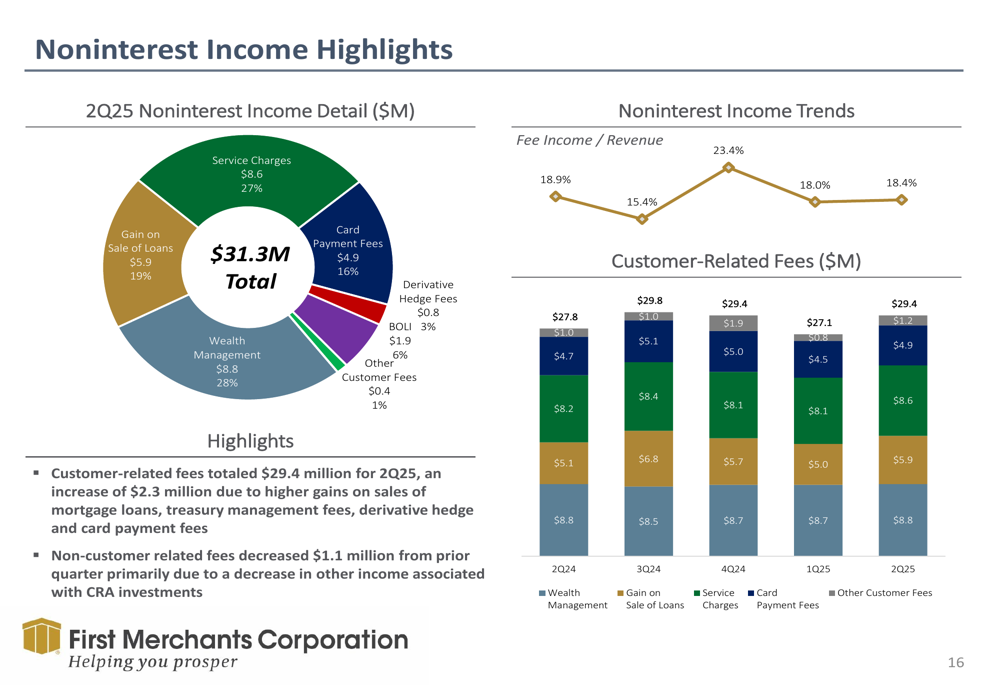

Noninterest income totaled $31.3 million for the quarter, representing a diversified revenue stream. Wealth management fees contributed $8.8 million, while service charges and card payment fees generated $8.6 million and $4.9 million, respectively. Gain on sale of loans added another $5.9 million to the total.

The breakdown of noninterest income sources is illustrated below:

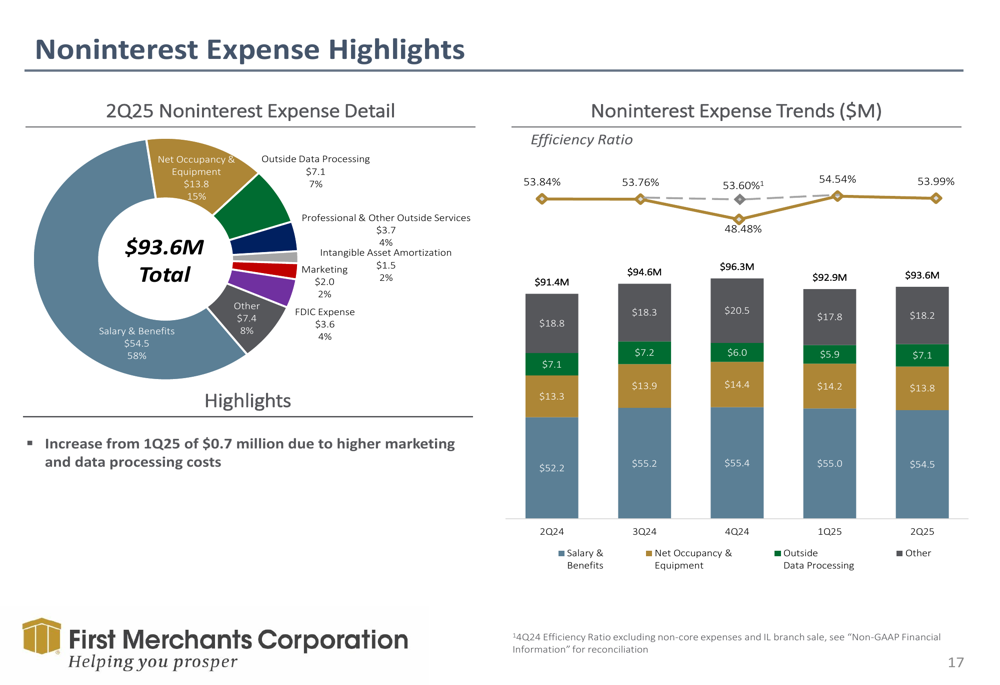

The bank maintained strong expense discipline, with an efficiency ratio of 53.99%, indicating that it spent approximately 54 cents to generate each dollar of revenue. Noninterest expenses totaled $93.6 million for the quarter, with salary and benefits accounting for 58% of the total.

The composition of noninterest expenses is detailed in the following chart:

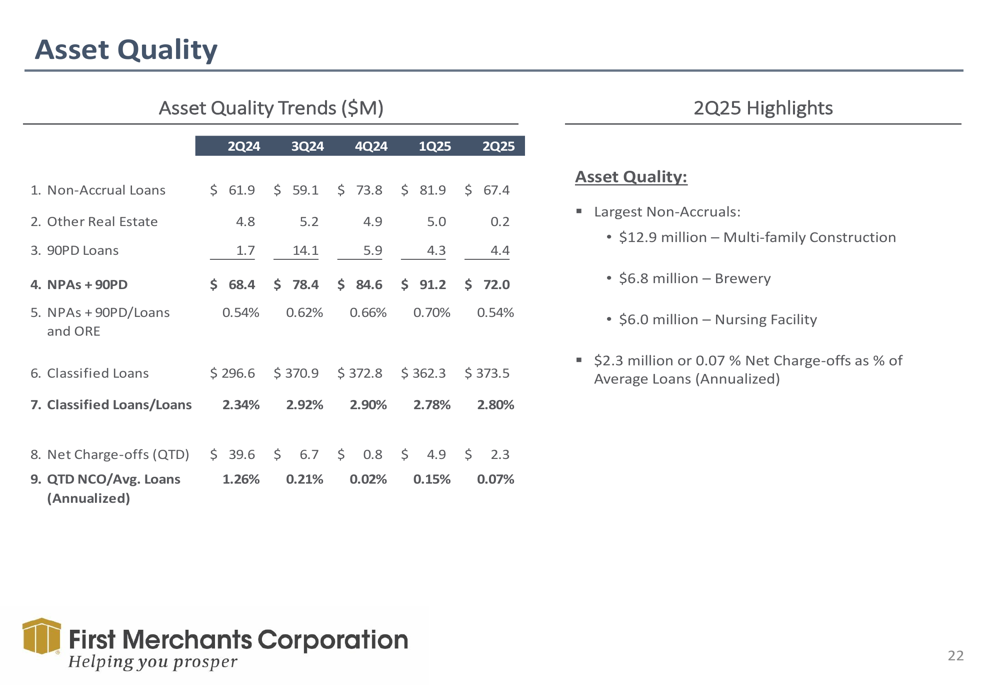

Asset Quality and Capital Position

Asset quality remained strong during the quarter, with classified loans stable at approximately 2.8% of the portfolio. The bank reported low net charge-offs, indicating effective credit risk management. The allowance for credit losses on loans stood at $159.7 million or 1.20% of total loans, providing adequate coverage for potential credit losses.

The trend in asset quality metrics is illustrated in the following chart:

First Merchants maintained a solid capital position, with a tangible common equity ratio of 8.92% and a total risk-based capital ratio well above regulatory requirements. During the first half of 2025, the bank redeemed $30 million in subordinated debt and repurchased $30 million in shares, demonstrating its commitment to optimizing its capital structure while returning value to shareholders.

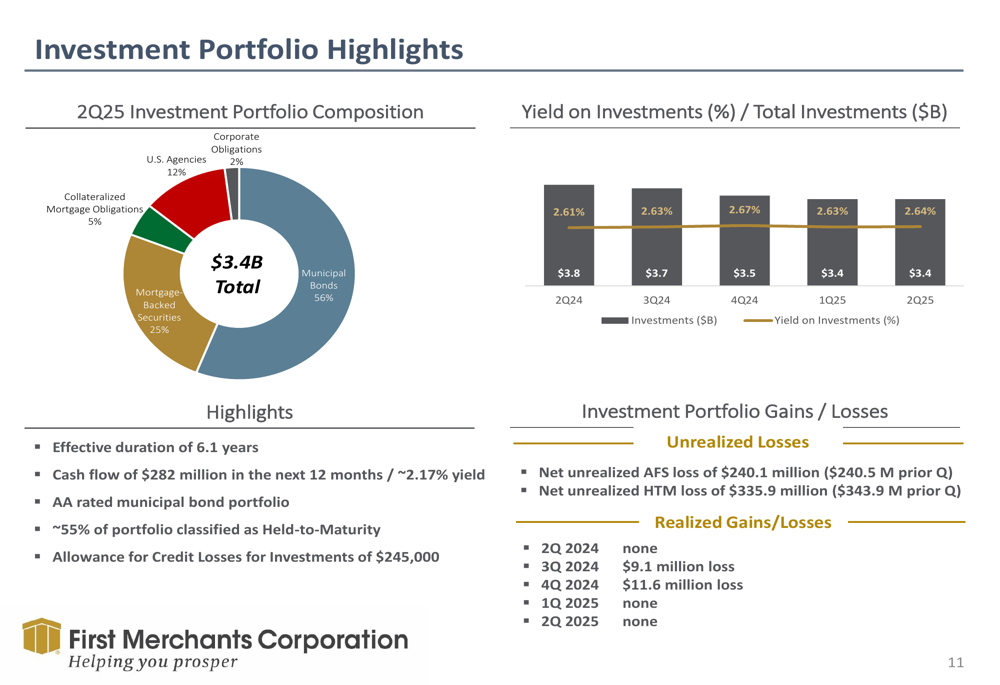

The bank’s investment portfolio, totaling $3.4 billion, is primarily composed of high-quality securities, with municipal bonds representing 56% of the total. The portfolio has an effective duration of 6.1 years and is generating a yield of 2.64%.

The investment portfolio composition is shown in the following chart:

Forward-Looking Statements

Looking ahead, First Merchants remains focused on enhancing the financial wellness of the diverse communities it serves. The bank’s strategic imperatives include building an inclusive culture, pursuing organic and acquisition-based growth, accelerating digital transformation, and expanding its shareholder base.

Management expects continued loan growth in the mid to high single digits for the remainder of 2025, with a focus on commercial lending. The bank anticipates modest margin compression in the latter half of the year due to potential Federal Reserve rate cuts, but expects to maintain strong overall profitability.

CEO Mark Hardwick emphasized the company’s focus on maintaining margins, stating, "We’re seeing really nice growth, and even from the margin standpoint, it’s like, let’s just maintain where we are." President Mike Stewart added that the business models of their clients are growing and performing well, supporting the bank’s optimistic outlook.

First Merchants has demonstrated a strong track record of shareholder value creation, with a 10-year total return of 230.1% from 2014 to 2024. The bank’s consistent growth in earnings per share, dividends, and tangible book value has positioned it well for continued success in the competitive regional banking landscape.

With its strong capital position, diversified loan portfolio, and focus on commercial relationships, First Merchants appears well-positioned to navigate the evolving economic environment while continuing to deliver value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.