Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Fluor Corporation (NYSE:FLR) shares plunged 16.75% in premarket trading Friday after the engineering and construction giant reported second-quarter results that showed a significant earnings decline and lowered full-year guidance. The company’s Q2 2025 presentation, delivered on August 1, revealed an adjusted EPS of $0.43, down 41% from the $0.73 reported in Q1.

Introduction & Market Context

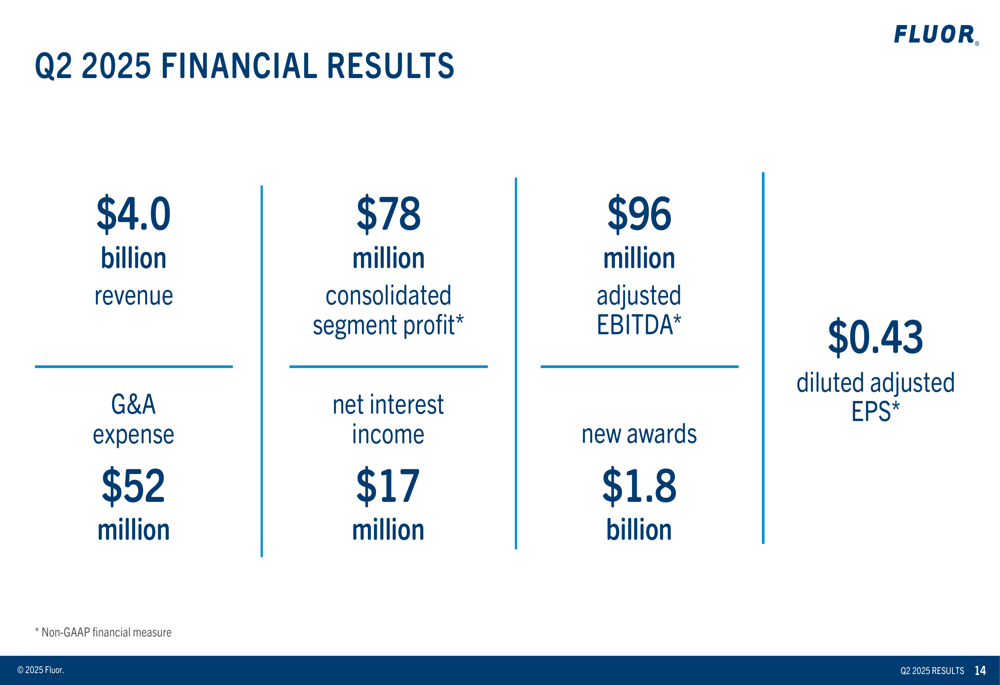

Fluor reported Q2 2025 revenue of $4.0 billion, in line with the previous quarter but below analyst expectations. The company’s consolidated segment profit fell to $78 million, with adjusted EBITDA of $96 million. The results triggered a sharp selloff, with the stock dropping to $47.26 in premarket trading, erasing most of its gains for the year.

The engineering and construction firm faced multiple headwinds during the quarter, including cost growth on infrastructure projects, an unexpected arbitration ruling, and slower-than-anticipated progress on several key initiatives.

Quarterly Performance Highlights

Fluor’s Q2 2025 financial results showed mixed performance across its business segments. The company reported new awards of $1.8 billion (72% reimbursable) and maintained a substantial backlog of $28.2 billion (80% reimbursable).

As shown in the following chart of key financial metrics:

By segment, Urban Solutions posted a profit of $29 million, which included a $54 million net impact from cost growth and expected recoveries on three infrastructure projects. The segment also experienced lower take-up on two mining and metals projects and slower-than-expected revenue ramp on a large life sciences project.

The following chart details Urban Solutions’ performance:

Energy Solutions reported a profit of $15 million, reflecting reduced contributions as projects near completion. Results were negatively impacted by an unexpected $31 million arbitration ruling related to a project completed by Fluor’s Mexico joint venture in 2021.

The segment’s new awards and backlog trends are illustrated here:

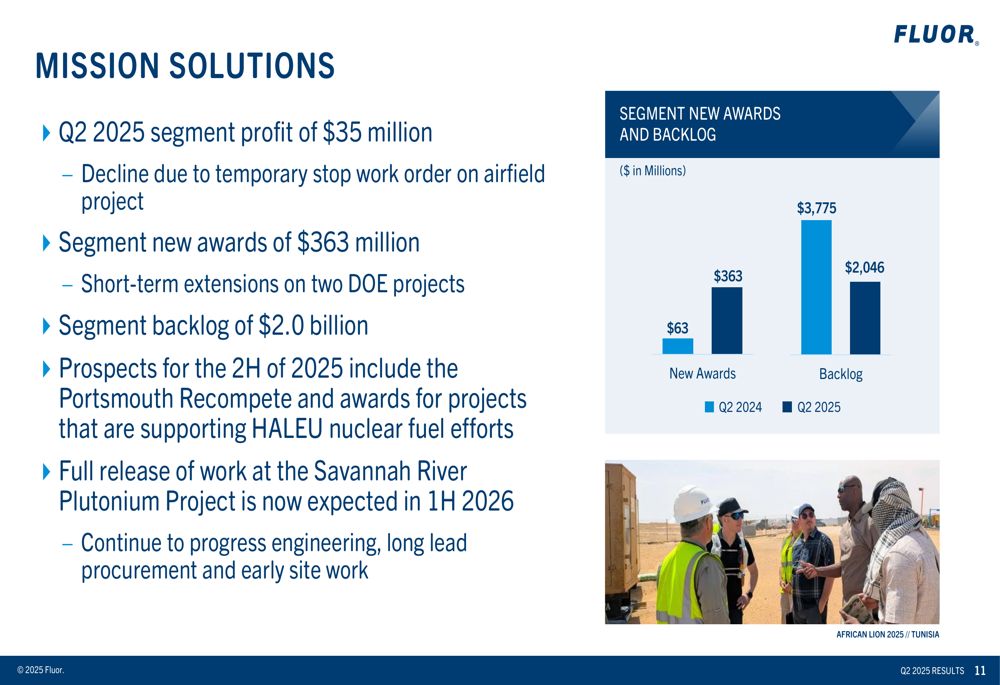

Mission Solutions delivered a profit of $35 million, with the decline attributed to a temporary stop work order on an airfield project. The segment secured new awards of $363 million, primarily from short-term extensions on two Department of Energy projects.

Operational Updates

A significant milestone for Fluor was the progress on its LNG Canada project, which achieved Ready for Start-Up (RFSU) for Train 1 in Q2 and shipped its first cargo in June. The company is now focused on achieving Train 2 RFSU and recently reached a settlement agreement covering COVID claims and other matters.

"We recently reached a settlement agreement covering our COVID claims and other matters," the company noted in its presentation, adding that its joint venture was awarded a contract to update the FEED package for a proposed phase 2 expansion of the facility.

Infrastructure projects continued to present challenges. The Gordie Howe project is 97% complete with substantial completion expected in Q3 2025. The 635/LBJ project stands at 78% complete with substantial completion projected for Q2 2026, while the I-35 Phase 2 project is 58% complete with completion anticipated in Q4 2026.

Fluor reported increased oversight and strengthened execution teams on these projects, noting it is "taking action against certain subcontractors and designers for poor performance."

Financial Analysis

Fluor ended the quarter with $2.3 billion in cash and marketable securities. Operating cash flow was negative at -$21 million, continuing the negative trend from Q1 (-$286 million). The company attributed this to increased working capital on several large projects, funding of project cost growth in infrastructure, and timing of accounts receivable collections.

The company spent $44 million on legacy project funding during Q2 and maintained its expectation for 2025 funding of $200 million, though it anticipates additional funding will be required in 2026.

Share repurchases remained a priority, with $153 million spent during Q2. Fluor expects 2025 repurchases to total between $450-500 million, demonstrating confidence in its long-term outlook despite current challenges.

Regarding its investment in NuScale Power, Fluor expects to complete a 15 million share conversion this month and is "working with NuScale on a path to return value to shareholders."

Forward Guidance

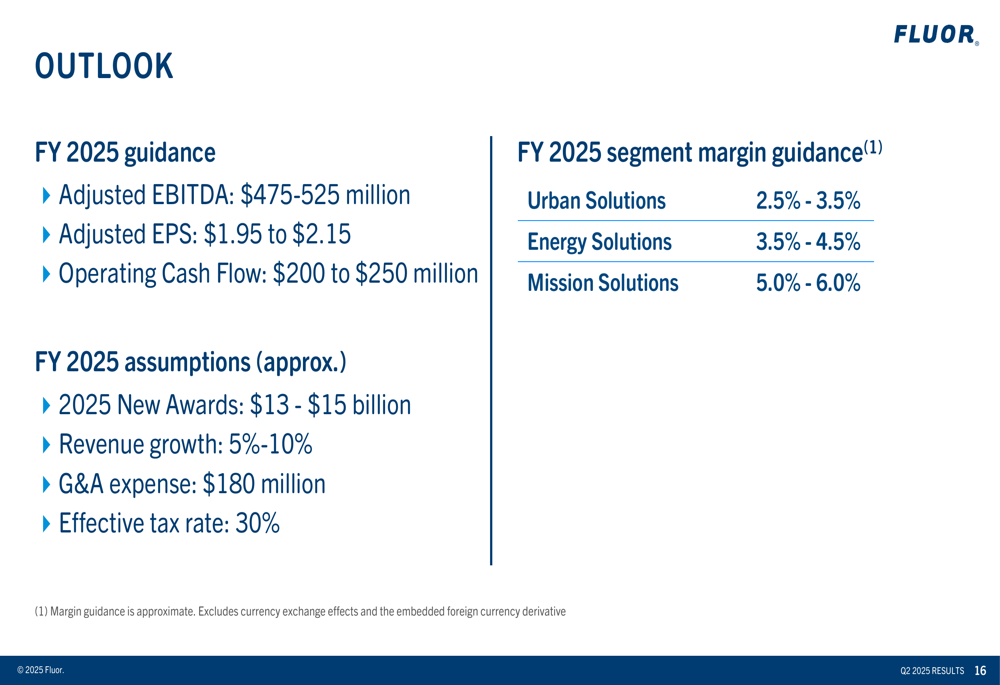

In a significant development, Fluor lowered its full-year 2025 guidance substantially from previous projections. The company now expects:

This revised outlook represents a significant reduction from the guidance provided after Q1 results, when Fluor projected adjusted EBITDA between $575-675 million and adjusted EPS between $2.25-2.75.

The company’s assumptions for 2025 include new awards of $13-15 billion, revenue growth of 5-10%, G&A expense of approximately $180 million, and an effective tax rate of 30%.

Segment margin guidance reflects the operational challenges, with Urban Solutions expected to deliver margins of 2.5-3.5%, Energy Solutions 3.5-4.5%, and Mission Solutions 5.0-6.0%.

Strategic Initiatives

Despite current challenges, Fluor highlighted several strategic initiatives and market opportunities. In Urban Solutions, the company is leveraging its global capabilities for mining projects, noting opportunities in copper, green steel production, aluminum recycling, and rare earth and critical minerals. Management specifically highlighted the U.S. mining resurgence as presenting "significant opportunity."

For Energy Solutions, while acknowledging pressure from reduced capital expenditure and soft battery and chemicals markets, Fluor identified "multiple opportunities in the nuclear and gas-fired power generation market."

In Mission Solutions, prospects for the second half of 2025 include the Portsmouth Recompete and awards for projects supporting High-Assay Low-Enriched Uranium (HALEU) nuclear fuel efforts. The full release of work at the Savannah River Plutonium Project is now expected in the first half of 2026.

The company’s continued focus on reimbursable contracts (80% of backlog) suggests a strategic emphasis on risk mitigation in an uncertain economic environment.

Conclusion

Fluor’s Q2 2025 results reveal a company facing significant operational challenges across multiple segments, resulting in lowered full-year guidance and a sharp negative market reaction. While the company maintains a substantial backlog and continues to advance strategic initiatives in growth markets, the immediate outlook has deteriorated considerably from just three months ago.

Investors will likely focus on whether management can address the infrastructure project challenges, improve cash flow generation, and deliver on its revised guidance for the remainder of 2025. The stock’s premarket decline of nearly 17% suggests significant investor concern about the company’s near-term prospects, despite its continued share repurchase program and long-term positioning in energy transition and infrastructure markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.