One & One Green Technologies stock soars 100% after IPO debut

Franklin Covey Company (NYSE:FC) released its third-quarter fiscal 2025 results on July 2, revealing significant year-over-year declines in both revenue and profitability, which led the company to lower its full-year guidance. Despite these challenges, the company highlighted growth in subscription metrics and deferred revenue, particularly in its Education division.

Quarterly Performance Highlights

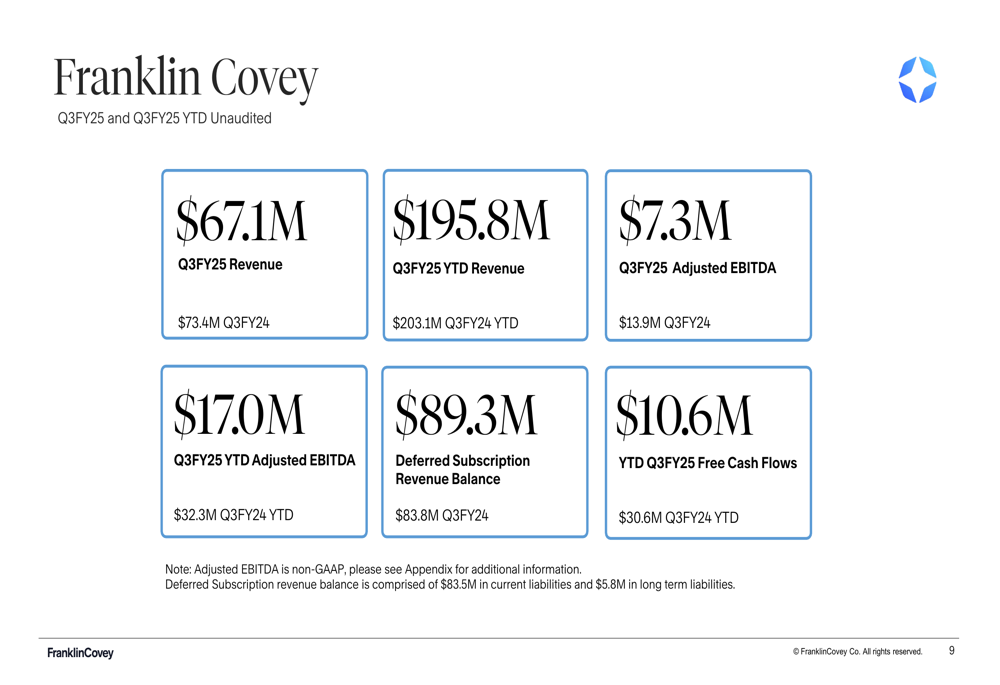

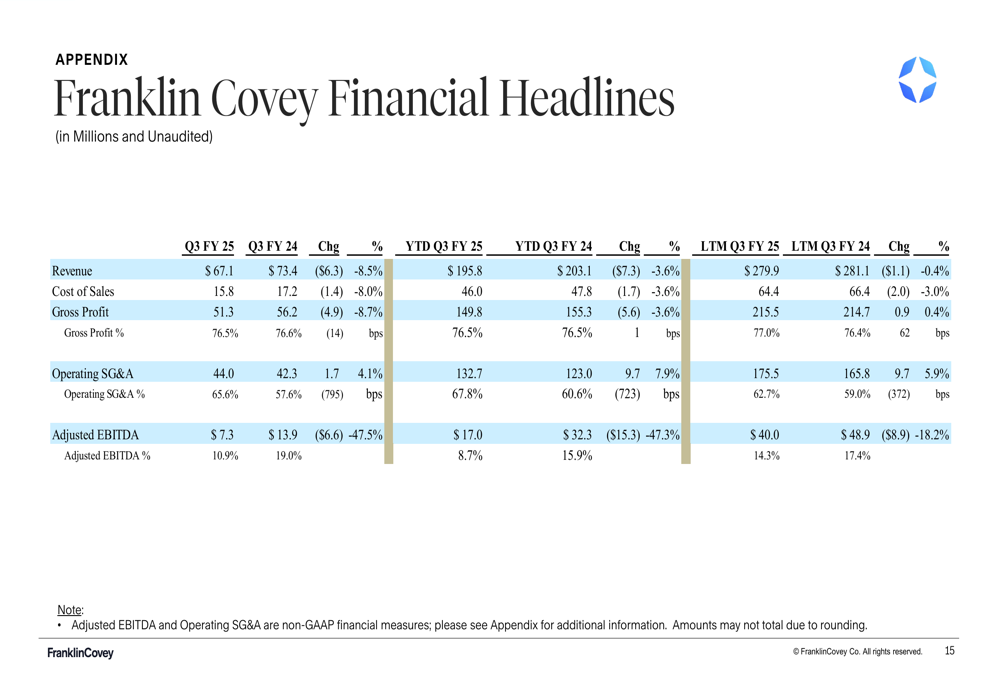

Franklin Covey reported Q3 FY2025 revenue of $67.1 million, down 8.6% from $73.4 million in the same quarter last year. The company’s adjusted EBITDA declined more substantially, falling 47.5% to $7.3 million compared to $13.9 million in Q3 FY2024. Year-to-date free cash flow also decreased significantly to $10.6 million, down from $30.6 million in the prior year period.

As shown in the following financial highlights from the presentation:

Despite meeting the low end of its revenue guidance range ($67M - $71M), the company’s performance fell short of analyst expectations. According to the earnings call transcript, Franklin Covey posted an earnings per share (EPS) of -$0.11, significantly below the anticipated $0.32, representing a negative surprise of 134.38%.

The company’s stock showed resilience following the announcement, rising 3.86% in aftermarket trading to $25.04, despite the disappointing results.

Detailed Financial Analysis

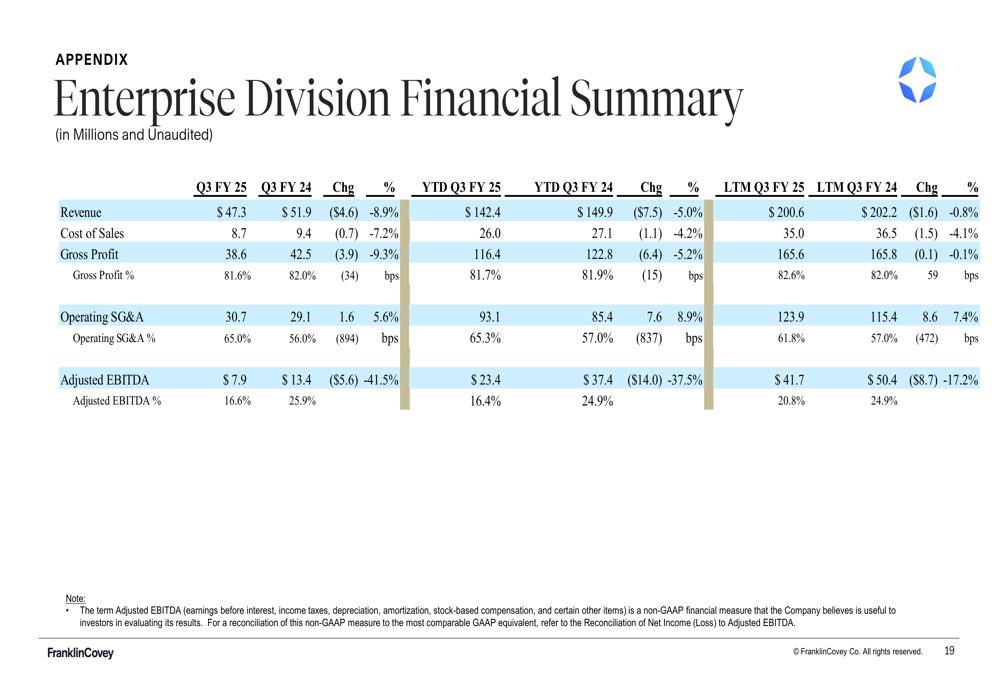

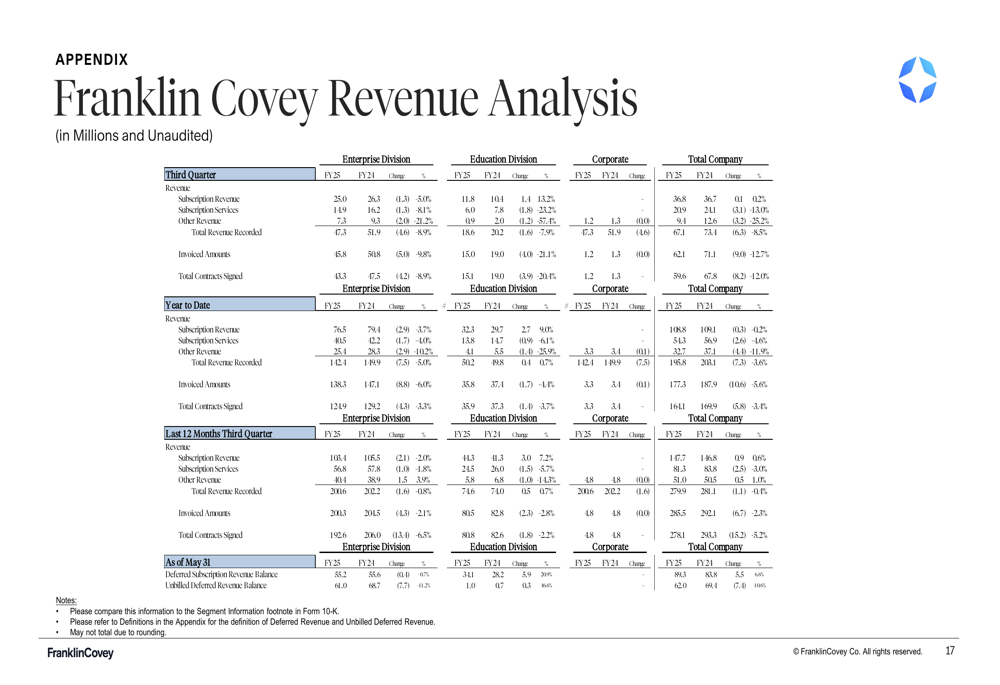

The Enterprise Division, Franklin Covey’s largest segment, reported North America revenue of $37.1 million, down 8.6% from $40.6 million in Q3 FY2024. Subscription revenue within this division declined to $20.9 million from $22.0 million in the prior year period.

The following slide details the Enterprise Division’s financial performance:

The International segment of the Enterprise Division also experienced declines, with direct revenue falling to $7.5 million from $8.5 million in Q3 FY2024, while revenue from international licensee partners remained flat at $2.7 million.

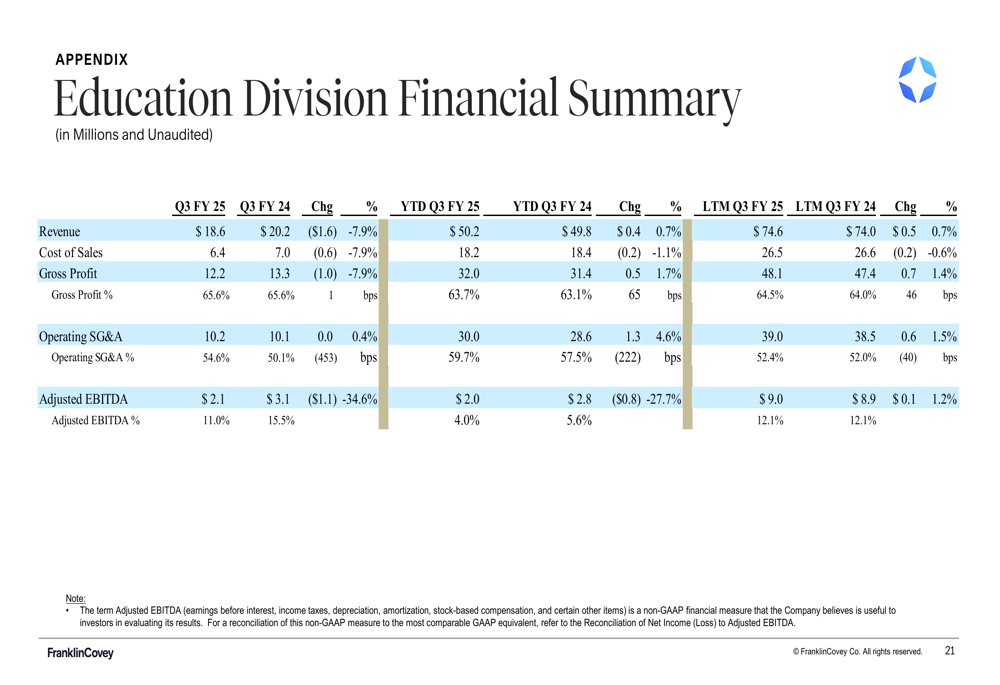

The Education Division, which the company highlighted as a growth area, reported revenue of $18.6 million, down 7.9% from $20.2 million in the prior year period. However, the division showed strength in deferred subscription revenue, which increased 20.9% to $34.1 million.

The comprehensive breakdown of Education Division performance is illustrated here:

Despite current revenue declines, the company emphasized positive subscription metrics in Education, noting a 13% increase in subscription revenue and a 21% growth in deferred revenue balance during Q3. The company also reported approaching 8,000 Leader In Me schools globally, indicating continued expansion of its educational programs.

Forward-Looking Statements

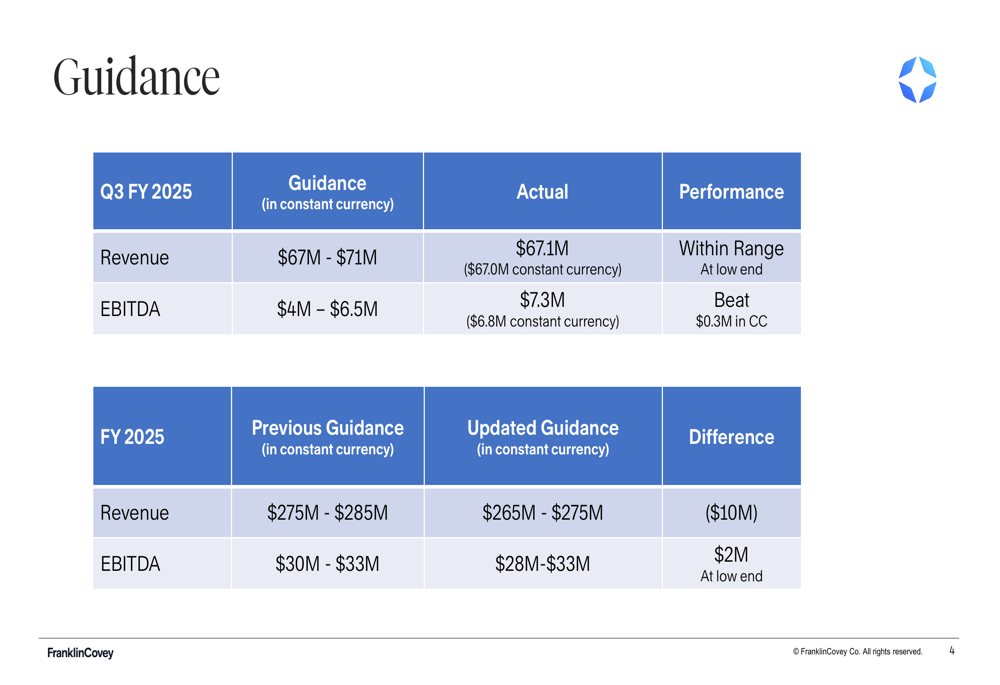

In response to the challenging quarter, Franklin Covey revised its full-year guidance downward. The updated FY2025 revenue guidance is now $265 million to $275 million, reduced from the previous range of $275 million to $285 million. Similarly, adjusted EBITDA guidance was lowered at the bottom end to $28 million - $33 million, compared to the previous range of $30 million - $33 million.

The following slide shows the guidance revision alongside actual Q3 performance:

During the earnings call, CEO Paul Walker expressed optimism despite the challenging environment, stating, "We’re pleased that in the middle of an uncertain environment, we’ve continued to win and expect to win many large deals in our enterprise and education businesses." The company cited macroeconomic uncertainty, government actions, and increased cost scrutiny by organizations as factors affecting current performance.

Strategic Initiatives

Franklin Covey continues to emphasize the strengths of its business model, including high revenue retention, strong gross margins (which remained at 76.5% in Q3), upfront invoicing practices, and low capital intensity. The company also highlighted that 62% of its revenue comes from multi-year contracts, providing some stability to future revenue streams.

The company’s revenue analysis across divisions provides insight into its overall business composition:

According to the earnings call, Franklin Covey is implementing cost reduction strategies, which saved $3 million in Q3. The company is also investing in AI-driven product innovations, with 43% of clients reportedly adopting AI coaching.

Despite current headwinds, Franklin Covey maintains that its subscription-based model positions it well for future growth. The company’s deferred subscription revenue balance increased to $89.3 million, up 6.6% from $83.8 million in Q3 FY2024, suggesting potential for future revenue recognition.

The comprehensive financial summary below illustrates the company’s year-to-date and last twelve months performance:

While Franklin Covey faces significant challenges in the current economic environment, management remains focused on long-term value creation through its subscription model, particularly in the Education segment where deferred revenue growth remains strong. Investors will be watching closely to see if the company can translate these subscription metrics into improved financial performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.