Walmart halts H-1B visa offers amid Trump’s $100,000 fee increase - Bloomberg

Introduction & Market Context

Freshworks Inc. (NASDAQ:FRSH) presented its Q2 2025 earnings results on July 29, 2025, showcasing continued revenue growth and improved profitability metrics. Despite the company’s solid performance, Freshworks’ stock experienced a slight decline in aftermarket trading, falling 1.24% to $11.17, according to market data. The software provider continues to trade near its 52-week low of $10.87, well below its 52-week high of $19.77.

The customer experience and IT service management software company reported revenue of $204.7 million for the quarter, representing an 18% year-over-year increase, while significantly improving its operating margins and cash flow generation.

Quarterly Performance Highlights

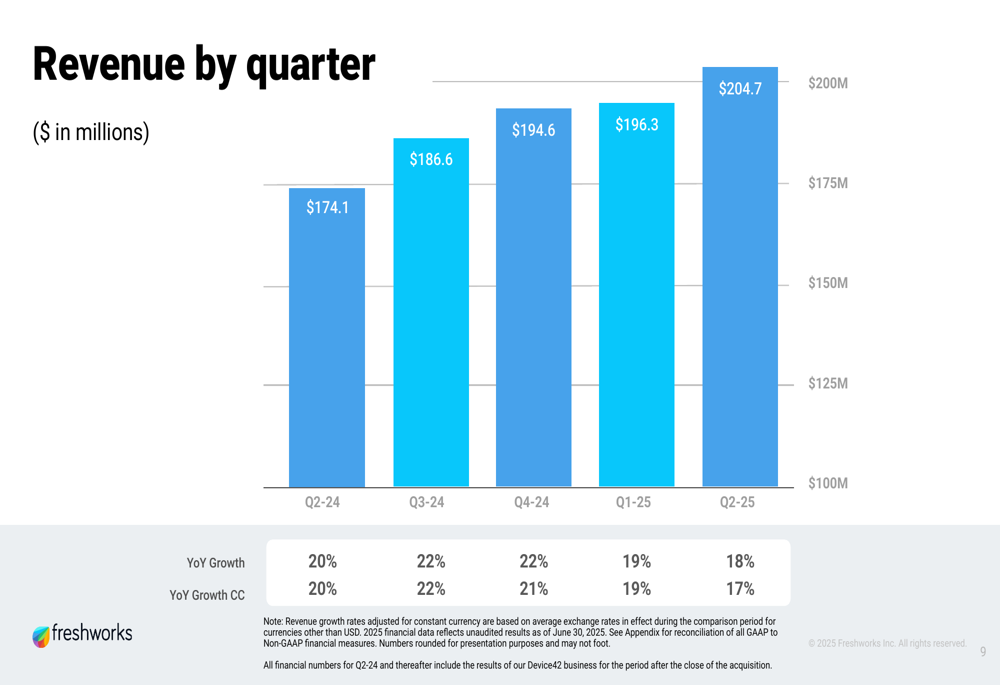

Freshworks’ Q2 2025 revenue reached $204.7 million, up 18% compared to the same period last year, or 17% on a constant currency basis. This continues the company’s pattern of steady growth over the past five quarters, as illustrated in the following revenue chart:

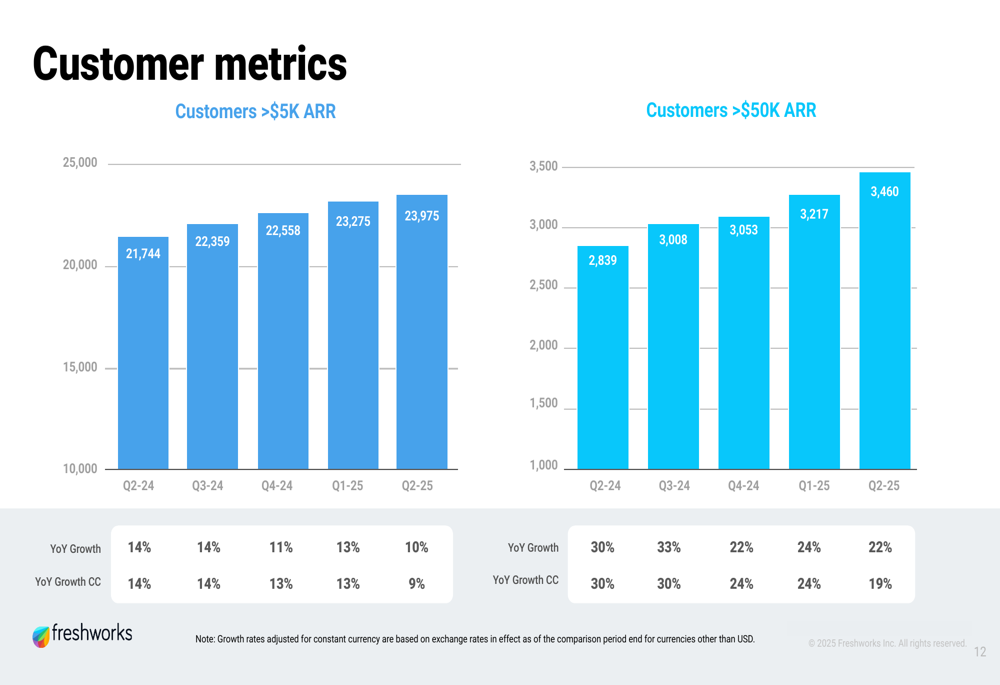

The company’s customer base expanded to over 74,600 customers across 120+ countries, representing an 8% year-over-year increase. More importantly, Freshworks demonstrated strong growth in higher-value customer segments.

As shown in the following chart, customers with Annual Recurring Revenue (ARR) exceeding $5,000 grew to 23,975 (10% YoY growth), while customers with ARR exceeding $50,000 increased to 3,460 (22% YoY growth):

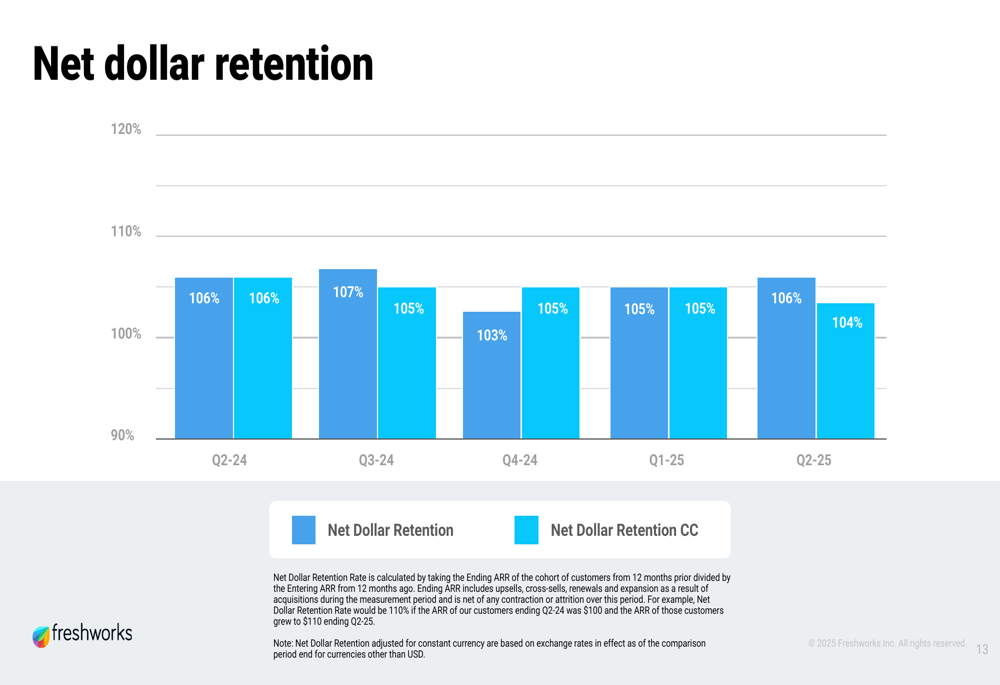

Freshworks maintained solid customer retention metrics, with Net Dollar Retention (NDR) at 106%, or 104% on a constant currency basis, indicating that existing customers are continuing to expand their usage of Freshworks products:

Customer and Product Strategy

Freshworks continues to expand its customer base across diverse industry verticals. The company highlighted several new customer wins in Q2, including AEP Energy, Covington & Burling LLP, Manchester Metropolitan University, Reed, and Seagate.

The presentation emphasized Freshworks’ broad customer base across multiple industries, as shown in this customer overview:

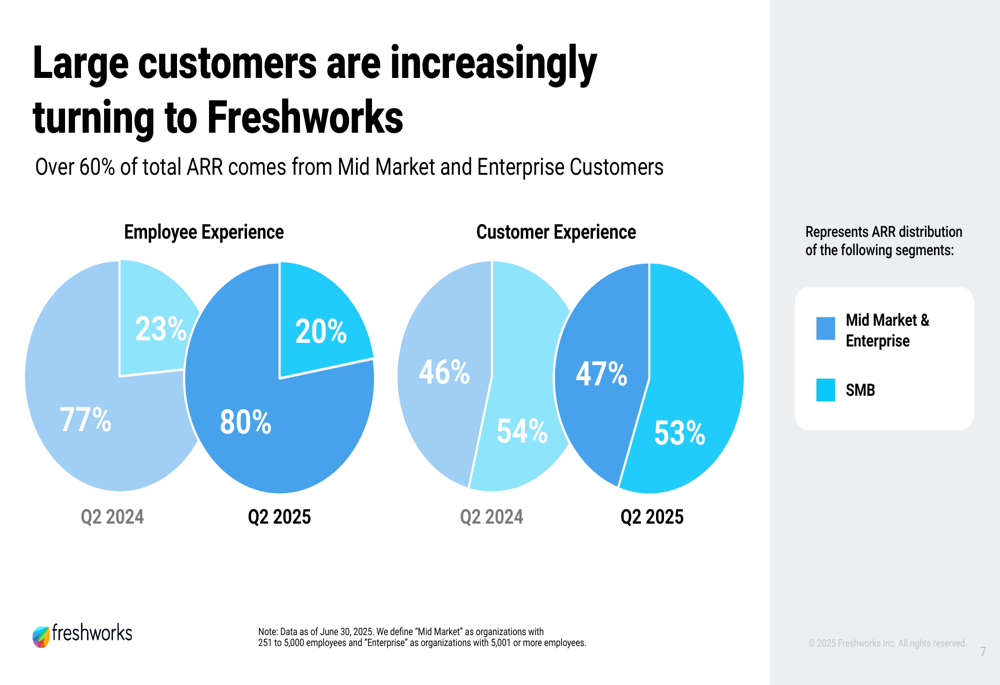

A key aspect of Freshworks’ strategy is its focus on mid-market and enterprise customers. According to the presentation, over 60% of total ARR now comes from mid-market and enterprise customers. The following chart shows the ARR distribution between mid-market & enterprise customers versus small and medium businesses:

Freshworks’ product portfolio is organized into two main categories: Employee Experience (including Freshservice, Freshservice for Business Teams, and Device42) and Customer Experience (including Freshdesk Omni, Freshdesk, Freshchat, Freshsales, and Freshmarketer). The company’s AI capabilities, branded as Freddy AI, are integrated across the product suite.

Detailed Financial Analysis

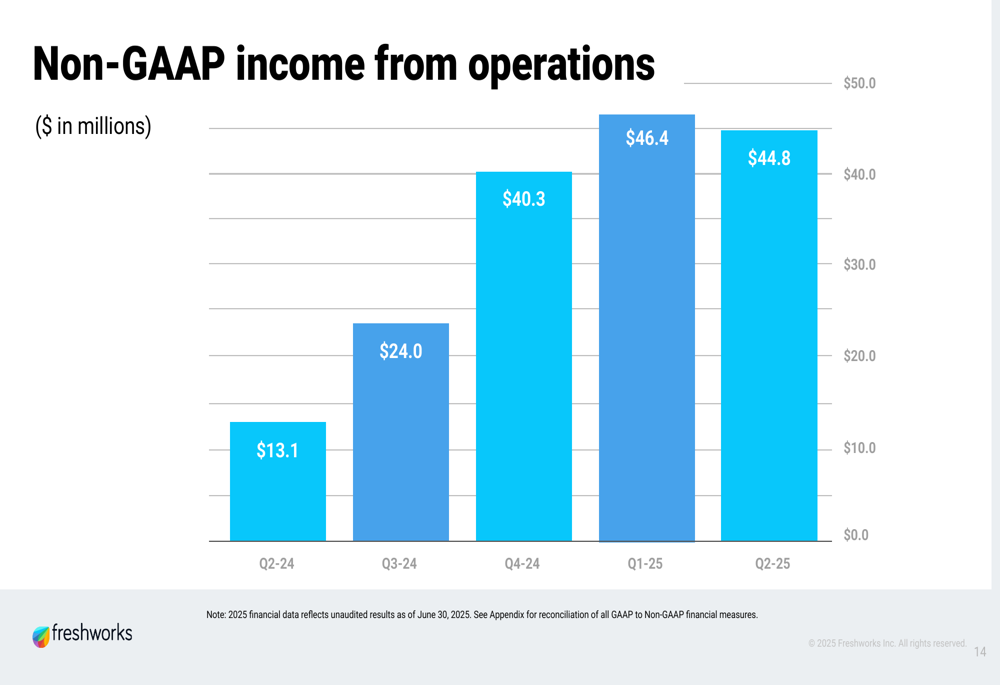

Beyond revenue growth, Freshworks demonstrated significant improvements in profitability metrics during Q2 2025. Non-GAAP income from operations reached $44.8 million, continuing an upward trend over the past five quarters:

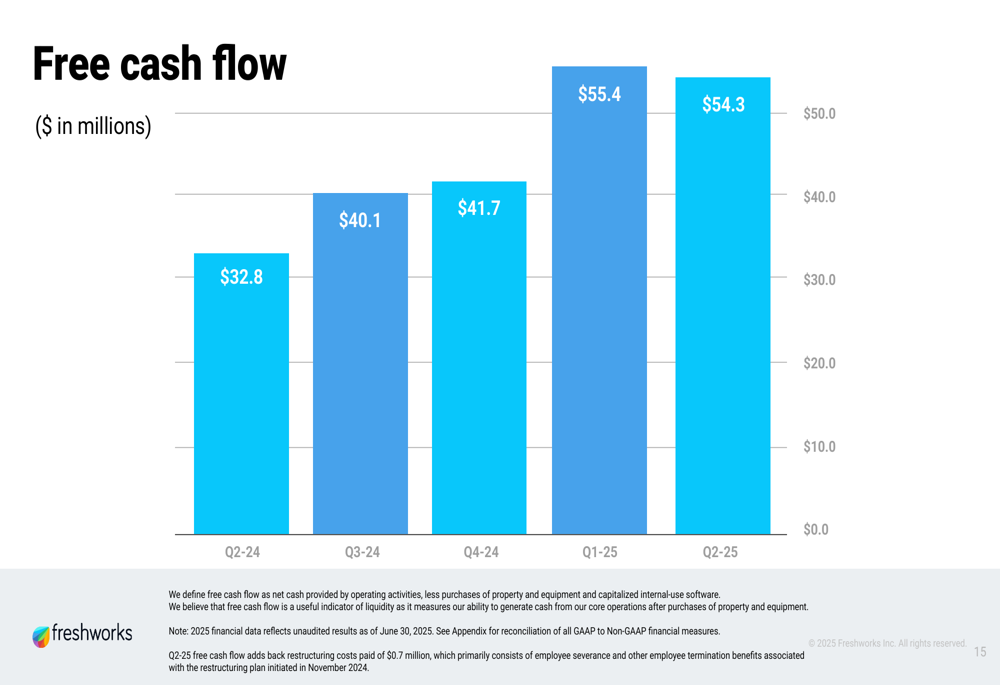

Free cash flow also showed strong performance, reaching $54.3 million in Q2 2025, compared to $32.8 million in Q2 2024, representing a 65% year-over-year increase:

The company’s GAAP operating margin improved substantially from -25% in Q2 2024 to -4% in Q2 2025, while non-GAAP operating margin expanded from 8% to 22% over the same period. According to the earnings call transcript, this 14 percentage point improvement in non-GAAP operating margin reflects the company’s increasing operational efficiency.

From a geographic perspective, Freshworks maintains a diversified revenue base with North America contributing 46% of revenue, Europe/Middle East/Africa 39%, Asia-Pacific 12%, and Rest of World 3%. This distribution has remained relatively stable over the past five quarters.

Forward-Looking Statements

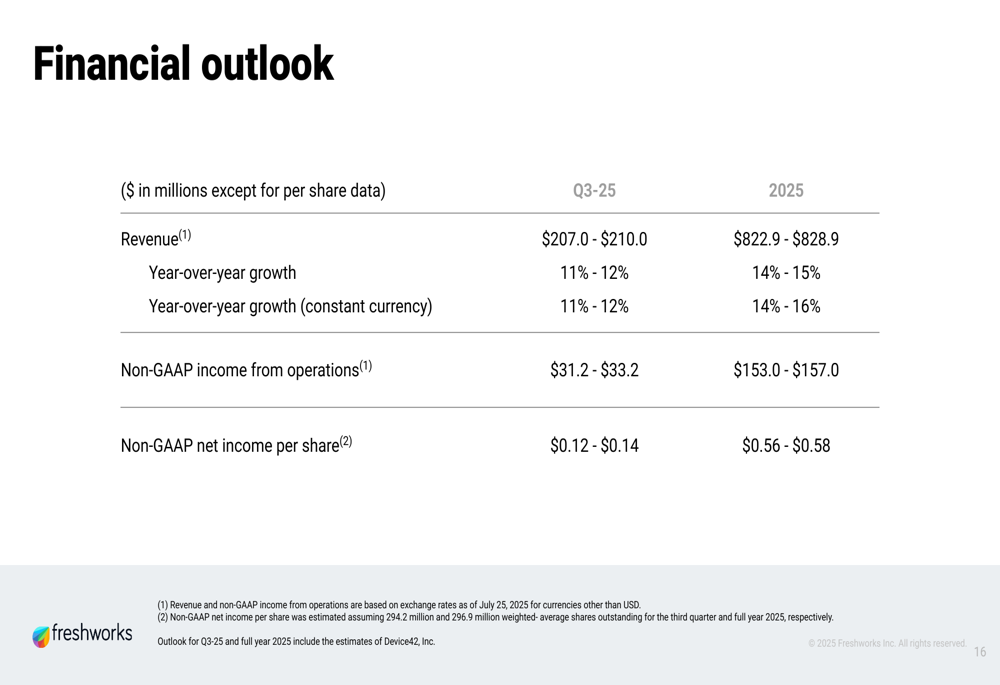

Freshworks provided a positive outlook for both Q3 2025 and the full year. For Q3, the company expects revenue between $207.0 and $210.0 million, representing 11-12% year-over-year growth. For the full year 2025, Freshworks forecasts revenue between $822.9 and $828.9 million, indicating 14-15% growth.

The following table details Freshworks’ complete financial guidance for the upcoming periods:

During the earnings call, CEO Dennis Woodside emphasized the mainstream adoption of AI across industries, noting that "Customers are no longer just experimenting with AI, they’re moving beyond the pilot phase." He also highlighted the company’s commitment to AI integration, stating, "We believe that every one of our customers should be using AI."

While not explicitly mentioned in the presentation, the earnings call transcript revealed that AI product adoption doubled during the quarter, contributing significantly to revenue growth. The company also addressed the ongoing integration of its Device42 acquisition, with plans for a cloud version release in 2026.

Despite the positive financial results and outlook, investors reacted cautiously, with the stock declining slightly in aftermarket trading. This may reflect broader market concerns about competition in the software space and potential macroeconomic pressures that could impact customer spending in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.