Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

FTAI Infrastructure LLC (NASDAQ:FIP) released its second quarter 2025 earnings presentation on August 8, 2025, highlighting a transformative rail acquisition and strong EBITDA growth despite posting a net loss. The infrastructure company’s stock has experienced significant volatility, with fundamentals showing a 12.97% decline on August 7, 2025, ahead of the earnings release.

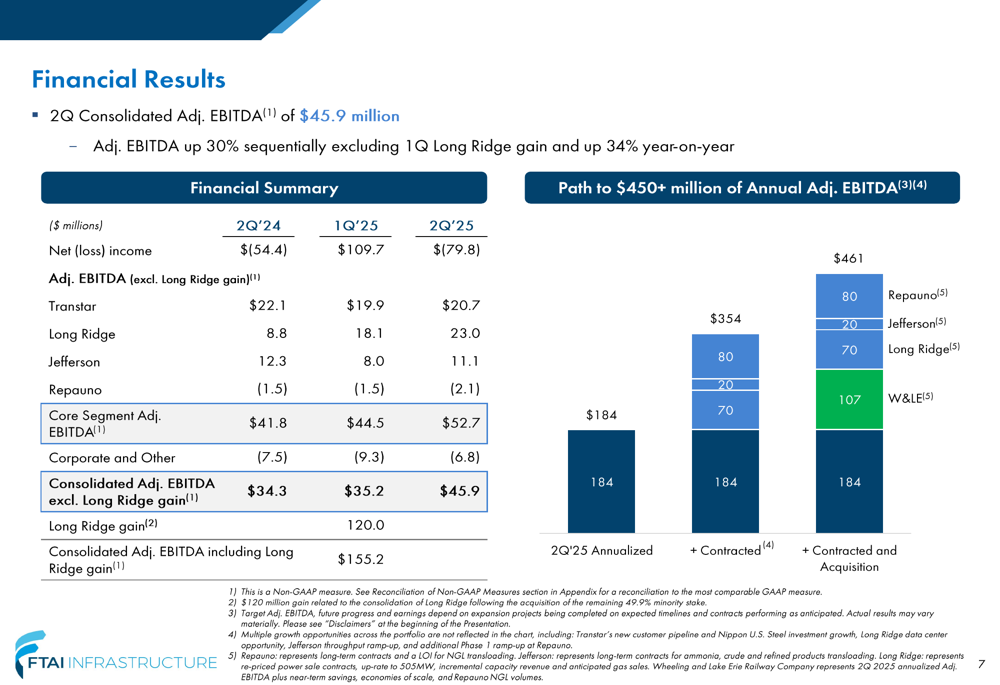

The company reported Q2 2025 consolidated adjusted EBITDA of $45.9 million, representing a 30% sequential increase from Q1 (excluding a one-time gain) and a 34% year-over-year improvement. However, FTAI Infrastructure also posted a net loss of $79.8 million for the quarter, contrasting with the $109.7 million net income reported in Q1 2025, which had included a substantial one-time gain.

Strategic Initiatives

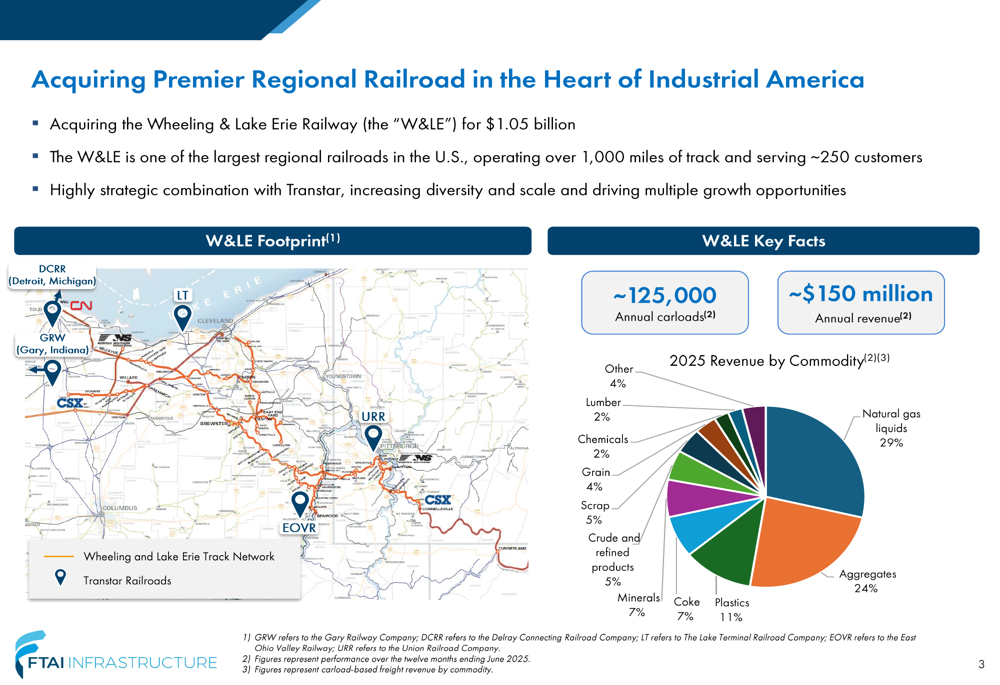

The centerpiece of FTAI Infrastructure’s strategic initiatives is the acquisition of Wheeling & Lake Erie Railway (W&LE) for $1.05 billion. This strategic purchase will significantly expand the company’s rail operations, adding over 1,000 miles of track serving approximately 250 customers.

As shown in the following acquisition overview, W&LE’s operations will complement FTAI’s existing Transtar business, with a diverse revenue mix across commodities including natural gas liquids (29%), aggregates (24%), and plastics (11%):

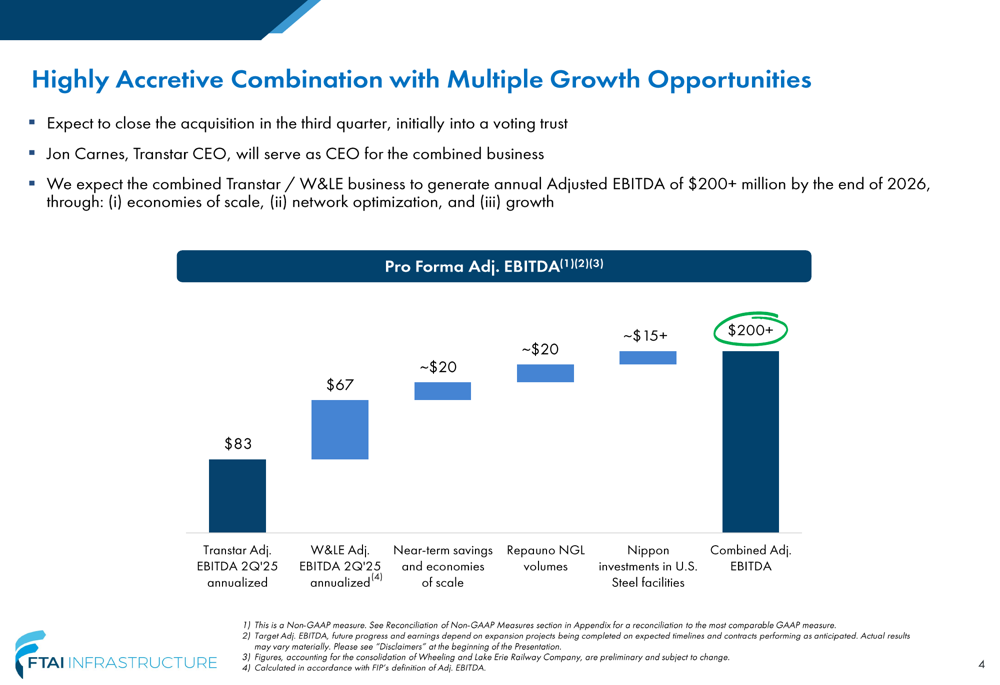

The company expects to close the W&LE acquisition in Q3 2025 into a voting trust, with Transtar CEO Jon Carnes serving as CEO for the combined business. Management projects substantial synergies from the combination, targeting annual adjusted EBITDA of over $200 million by the end of 2026 through economies of scale, network optimization, and growth initiatives.

The following chart illustrates how the combined rail operations are expected to drive significant EBITDA growth:

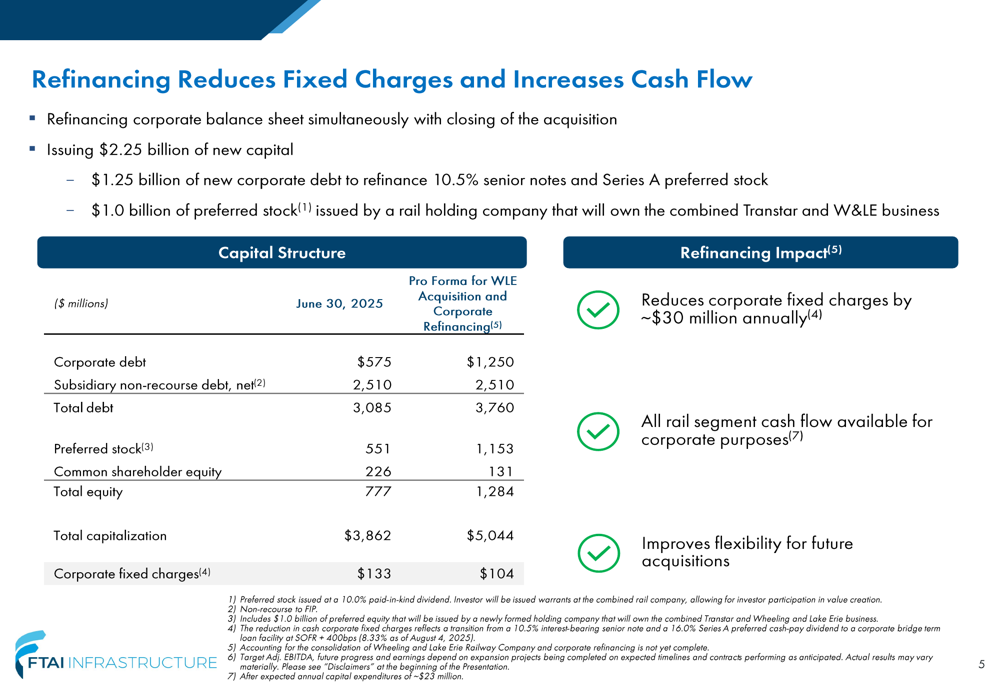

Alongside the rail acquisition, FTAI Infrastructure announced a comprehensive corporate refinancing plan to reduce fixed charges and increase financial flexibility. The refinancing includes $2.25 billion of new capital, comprising $1.25 billion of new corporate debt to refinance existing 10.5% senior notes and Series A preferred stock, plus $1.0 billion of preferred stock issued by a rail holding company that will own the combined Transtar and W&LE business.

The refinancing is expected to reduce corporate fixed charges by approximately $30 million annually, as detailed in this capital structure overview:

Quarterly Performance Highlights

FTAI Infrastructure reported consolidated adjusted EBITDA of $45.9 million for Q2 2025, representing a 30% sequential increase from Q1 (excluding a one-time gain) and a 34% year-over-year improvement from Q2 2024. The company’s core segment adjusted EBITDA reached $52.7 million, up from $44.5 million in Q1 2025 and $41.8 million in Q2 2024.

Despite these positive operational metrics, the company reported a net loss of $79.8 million for Q2 2025, compared to net income of $109.7 million in Q1 2025, which had included a one-time $120 million gain related to Long Ridge.

The company highlighted significant developments across its portfolio that are driving growth into the second half of 2025:

Segment Analysis

Railroad (Transtar)

The Railroad segment generated adjusted EBITDA of $20.7 million in Q2 2025, up 4% from $19.9 million in Q1 2025. This improvement came despite a slight decrease in average rate per car, as carload volumes increased to 59,600 from 58,800 in the previous quarter.

Management highlighted future growth opportunities from Nippon’s investments in U.S. Steel facilities, which are expected to generate approximately $15+ million of incremental annual adjusted EBITDA. The segment’s performance is also expected to benefit significantly from the pending acquisition of Wheeling & Lake Erie Railway.

Long Ridge

The Long Ridge power and gas segment reported adjusted EBITDA of $23.0 million in Q2 2025, up from $18.1 million in Q1 2025, despite scheduled annual maintenance performed in May that temporarily reduced the power plant’s capacity factor to 83% from 99% in the previous quarter.

Management noted that incremental $30 million in annual capacity payments began on June 1, and recent capacity auction results represent an additional $6 million in incremental adjusted EBITDA beginning June 2026. The segment’s growth strategy includes a PJM fast-tracked uprate, excess gas production, and behind-the-meter opportunities.

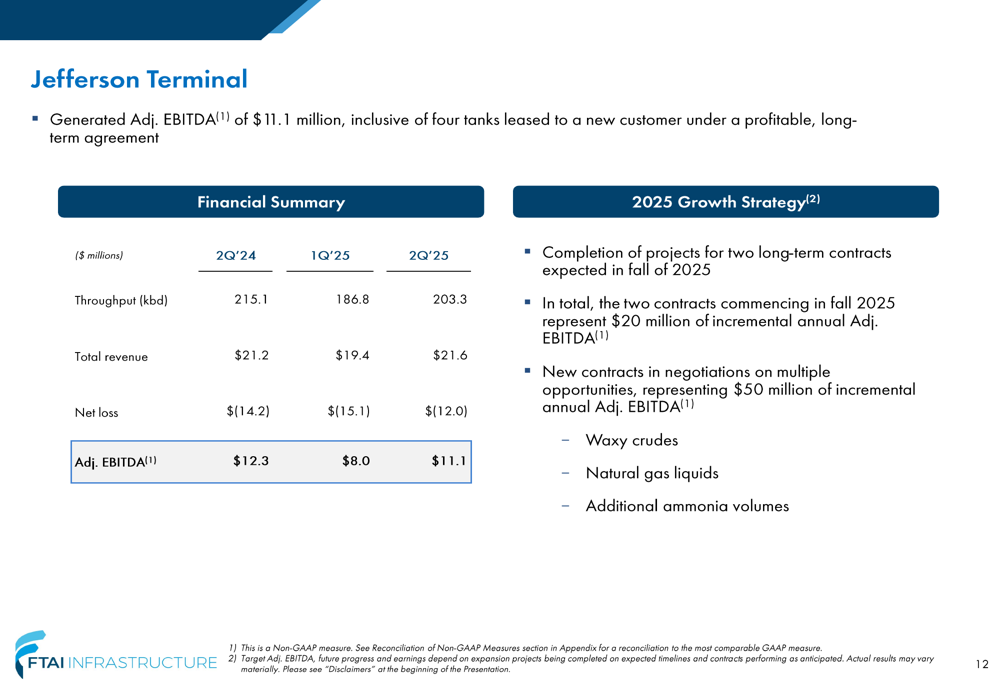

Jefferson Terminal

Jefferson Terminal generated adjusted EBITDA of $11.1 million in Q2 2025, up from $8.0 million in Q1 2025. The improvement was driven by increased throughput, which rose to 203,300 barrels per day from 186,800 in the previous quarter.

The segment’s outlook is positive, with management highlighting the completion of projects expected in fall 2025 that represent $20 million of incremental adjusted EBITDA. Additionally, new contracts under negotiation could contribute an additional $50 million of incremental adjusted EBITDA.

Repauno

The Repauno segment reported an adjusted EBITDA loss of $2.1 million in Q2 2025, slightly worse than the $1.5 million loss in Q1 2025. However, the company made significant progress on financing and construction activities, closing a $300 million tax-exempt financing at a 6.5% average coupon to fund phase two construction.

The following contract overview illustrates Repauno’s growth potential, with phase two operations targeted for Q4 2026:

Forward-Looking Statements

FTAI Infrastructure outlined a path to achieving over $450 million in annual adjusted EBITDA, driven by contracted growth across its segments and the strategic acquisition of Wheeling & Lake Erie Railway. The company emphasized that its growth strategy is supported by several key initiatives:

1. The transformational acquisition of W&LE, expected to close in Q3 2025

2. Nippon’s investments in U.S. Steel facilities generating approximately $15+ million of incremental annual adjusted EBITDA

3. Jefferson Terminal projects representing $20 million of incremental adjusted EBITDA

4. Repauno contracts and LOIs representing approximately $80 million of annual adjusted EBITDA

Management’s focus on reducing corporate fixed charges through refinancing is expected to improve financial flexibility and support future acquisitions. The company projects that the combined Transtar and W&LE rail business will generate annual adjusted EBITDA of over $200 million by the end of 2026, representing a significant portion of the company’s overall growth target.

While FTAI Infrastructure’s presentation emphasized adjusted EBITDA growth and strategic initiatives, investors should note the company’s continued net losses and the execution risks associated with integrating a major acquisition while simultaneously implementing a complex refinancing plan. The stock’s recent volatility suggests the market is still assessing the long-term impact of these strategic moves on the company’s financial performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.