Goldman Sachs chief credit strategist Lotfi Karoui departs after 18 years - Bloomberg

Introduction & Market Context

GCC SAB de CV (BMV:GCC) reported mixed second-quarter 2025 results on July 23, showing modest revenue growth but significant margin pressure amid persistent inflationary challenges and operational disruptions. The cement and concrete producer continues to navigate a complex market environment characterized by regional demand disparities, evolving trade dynamics, and currency pressures.

The company’s stock closed at $175.72 on August 4, 2025, down 0.5% for the day and currently trading well below its 52-week high of $223.62, reflecting ongoing investor concerns following a disappointing Q1 2025 performance when the company missed both revenue and EPS expectations.

Quarterly Performance Highlights

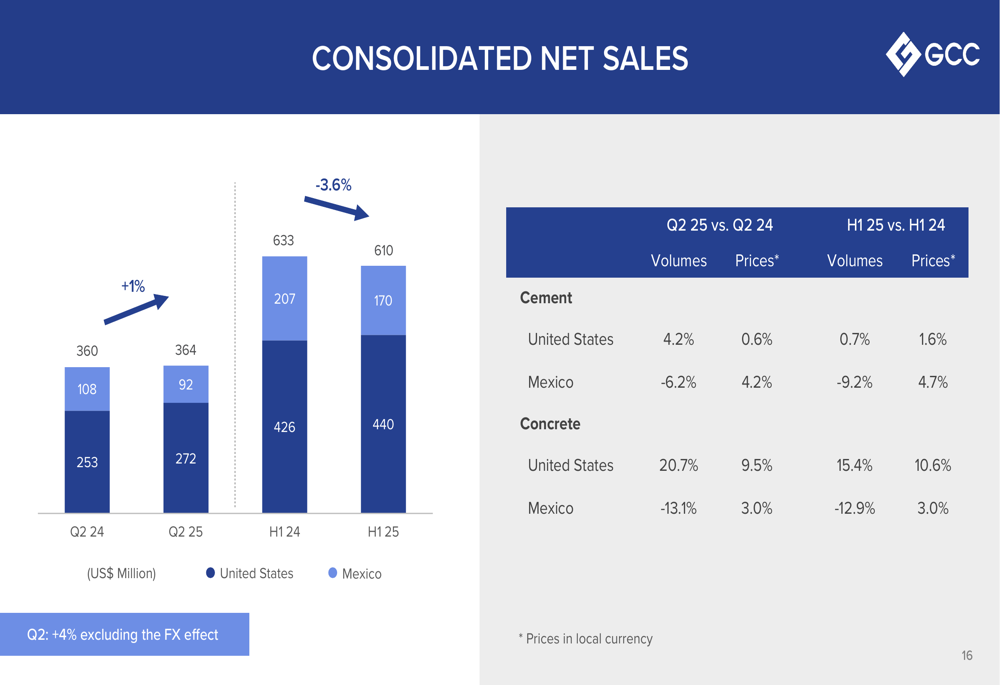

GCC reported consolidated net sales of US$364 million for Q2 2025, representing a modest 1% increase from US$360 million in Q2 2024. However, when excluding foreign exchange effects, sales grew by a more substantial 4%.

As shown in the following chart of quarterly sales performance:

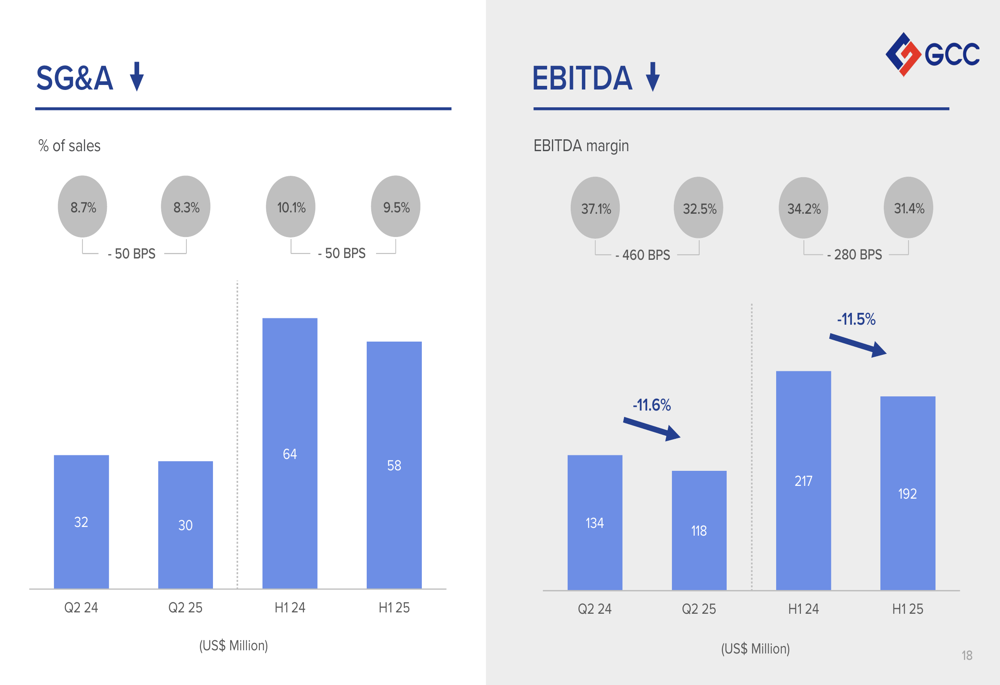

Despite the revenue growth, EBITDA declined 11.6% year-over-year to US$118.4 million, with EBITDA margin contracting to 32.5% from 37.1% in Q2 2024. The company noted that Q2 2024 had set a high benchmark with record margins that included several one-off benefits.

The following chart illustrates the EBITDA performance:

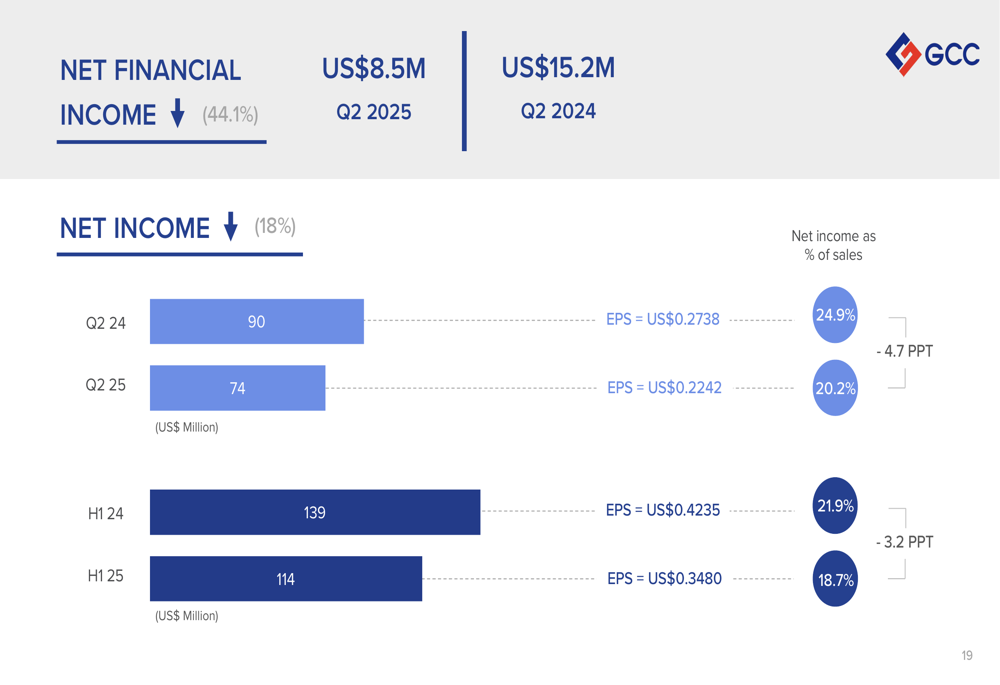

Net income for the quarter fell to US$73.5 million (20.2% of sales) from US$89.6 million (24.9% of sales) in Q2 2024, resulting in earnings per share of US$0.2242, down from US$0.2738 in the prior-year period.

The net income decline is detailed in this chart:

Regional Performance Analysis

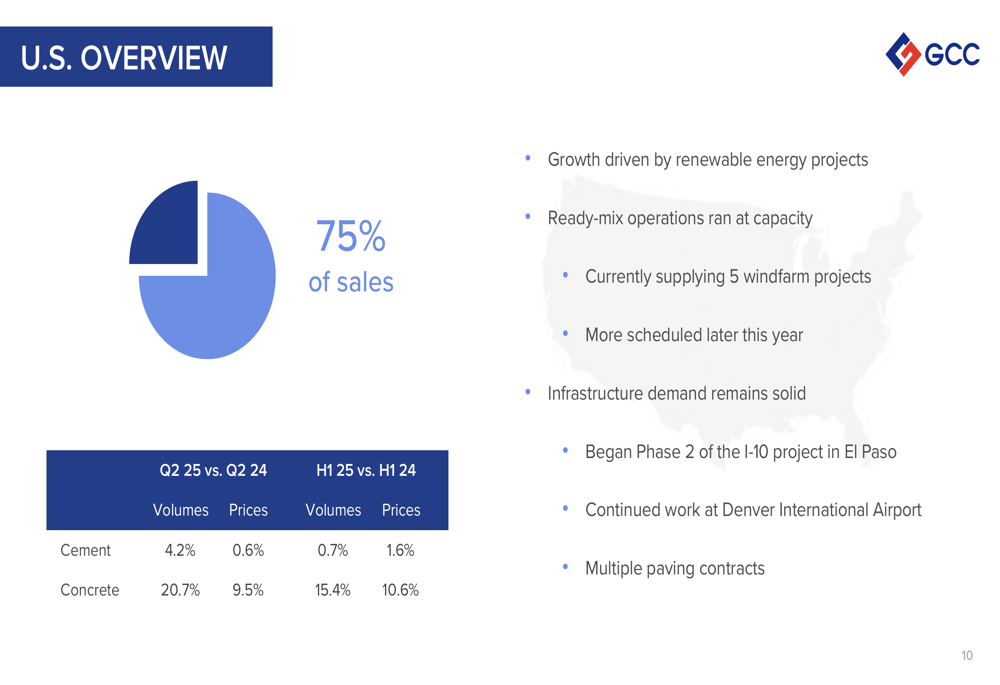

GCC’s operations continue to show divergent trends between its US and Mexican markets, with the US accounting for 75% of total sales and showing stronger performance.

In the United States, cement volumes increased 4.2% year-over-year with a modest price increase of 0.6%. Concrete volumes showed robust growth of 20.7% with a significant price increase of 9.5%. Growth was primarily driven by renewable energy projects, with the company currently supplying five windfarm projects. Infrastructure demand remained solid, including Phase 2 of the I-10 project in El Paso and ongoing work at Denver International Airport.

The US market performance is illustrated here:

However, challenges persisted in the US residential segment due to elevated housing inventory, declining home affordability, and mortgage rates above 5.5%. Additionally, the Rapid City cement plant was offline for half the quarter, forcing GCC to redirect supply from other plants and putting pressure on margins.

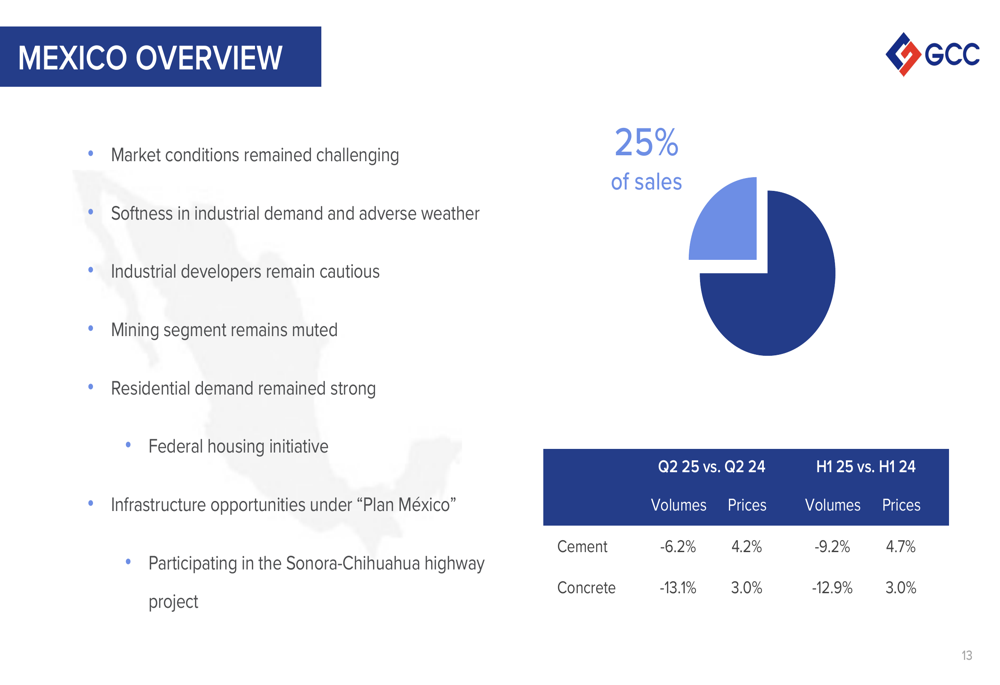

In Mexico, which represents 25% of sales, cement volumes declined 6.2% while prices increased 4.2%. Concrete volumes fell more sharply at 13.1% with a price increase of 3.0%. The Mexican market faced headwinds from softness in industrial demand, adverse weather conditions, and cautious industrial developers.

The Mexican market performance is shown here:

Strategic Initiatives & Capital Allocation

Despite margin pressures, GCC continues to invest in strategic growth while implementing cost optimization measures. The company has launched a company-wide cost and expense optimization program targeting US$12 million in reductions, with US$5 million already realized and the remaining US$7 million expected in the second half of 2025.

On the capital allocation front, GCC opened a new cement distribution terminal in Trenton, Texas in early July to address growing customer demand. The Odessa cement plant expansion remains on track, with US$458 million deployed of the total investment and US$174 million remaining for the balance of the year.

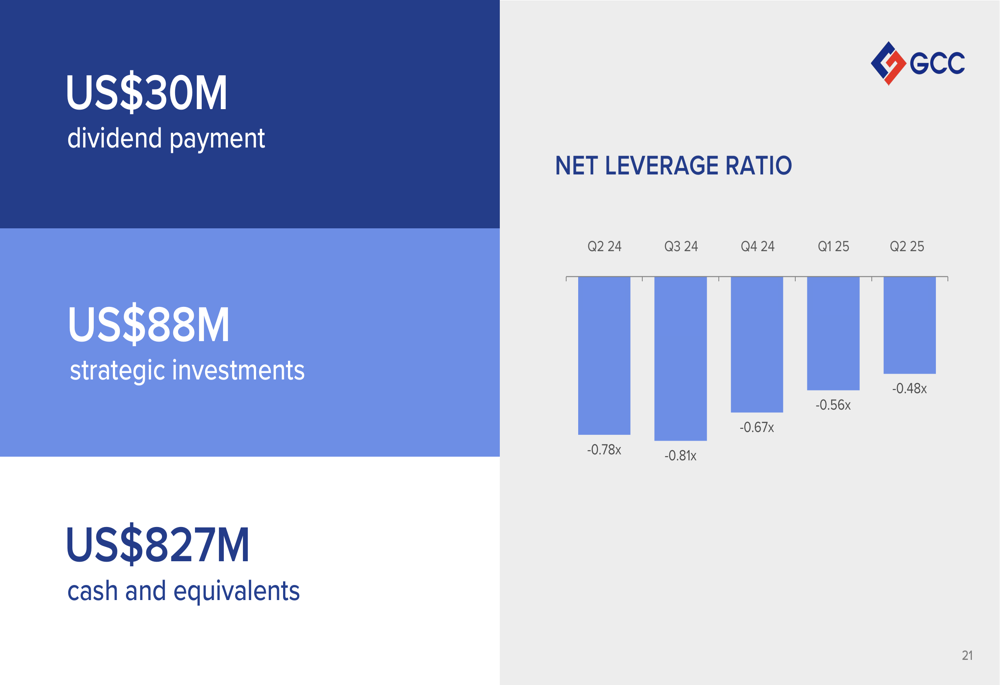

The company paid a US$30 million dividend during the quarter and reported US$827 million in cash and equivalents, maintaining a negative net leverage ratio of -0.48x, indicating a strong net cash position despite recent investments.

The company’s leverage position is detailed in this chart:

Financial Analysis

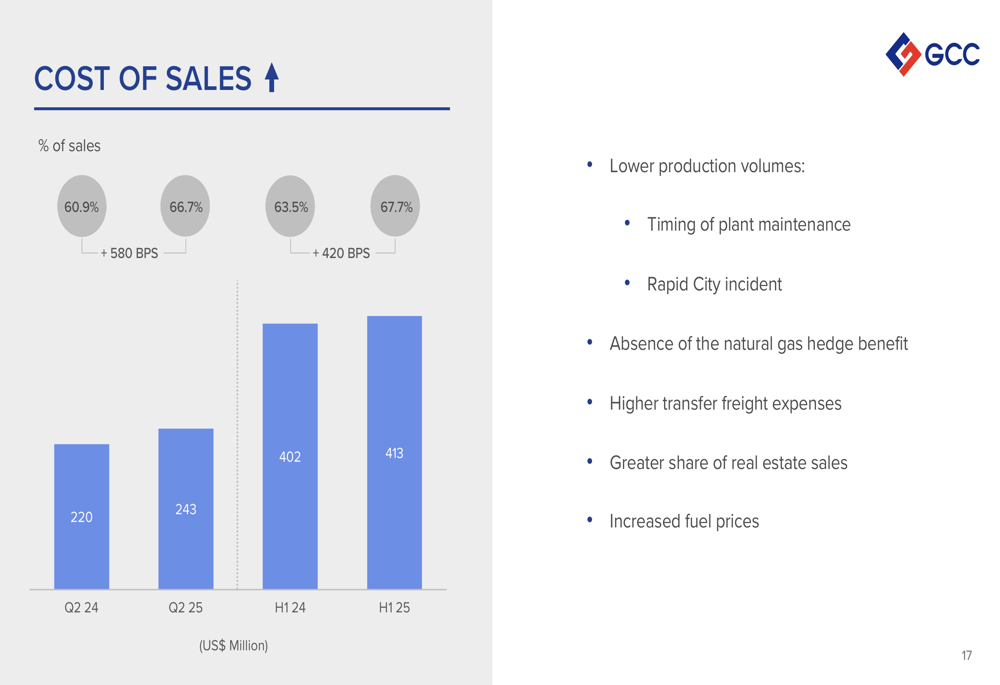

Cost pressures were evident in Q2 2025, with cost of sales increasing to 66.7% of sales compared to 60.9% in Q2 2024. This 580 basis point increase was attributed to lower production volumes from plant maintenance and the Rapid City incident, absence of natural gas hedge benefits, higher transfer freight expenses, and increased fuel prices.

The cost of sales trend is illustrated here:

On a positive note, SG&A expenses decreased to 8.3% of sales from 8.7% in Q2 2024, reflecting early benefits from the cost optimization program.

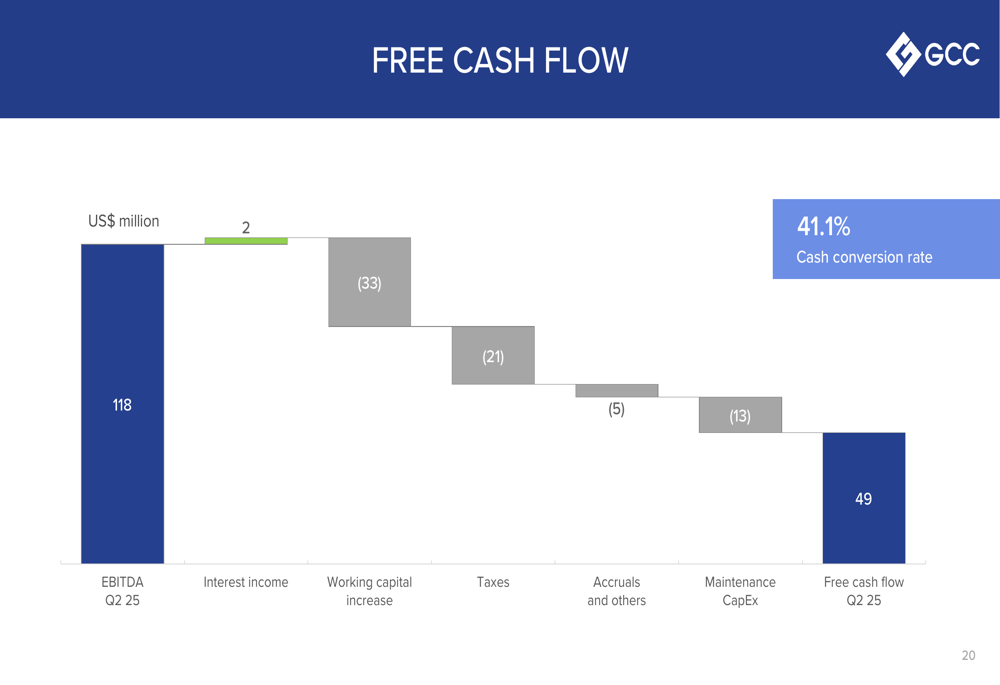

Free cash flow for Q2 2025 was US$48.6 million with a conversion rate of 41.1%, compared to US$29.0 million and 21.7% in Q2 2024. The improvement in free cash flow generation despite lower EBITDA demonstrates the company’s focus on cash management.

The free cash flow breakdown is shown in this chart:

2025 Outlook & Guidance

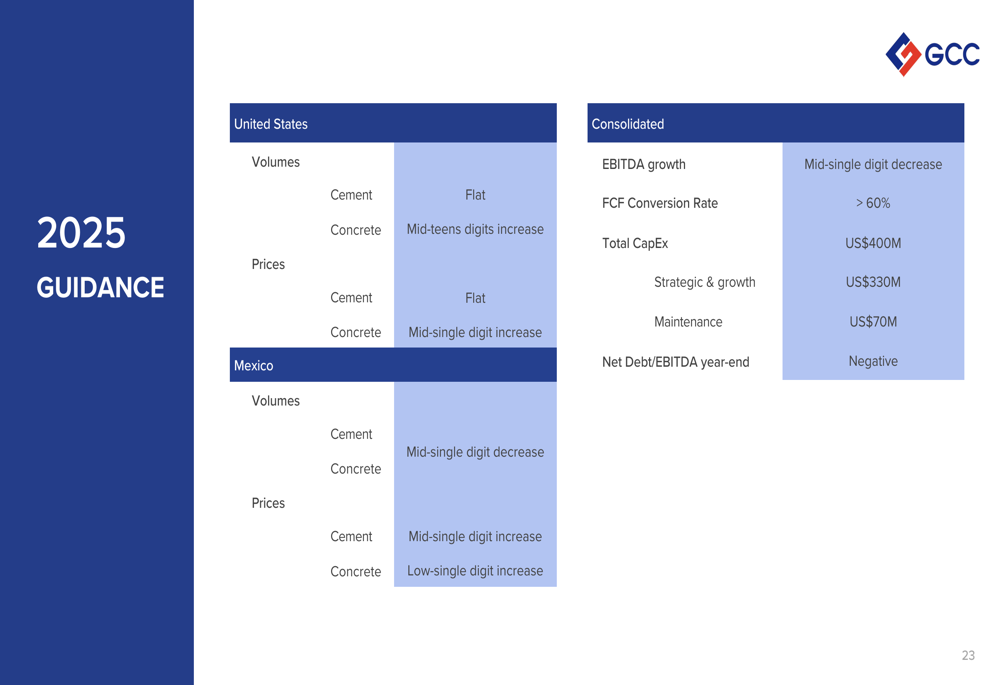

Looking ahead, GCC has maintained its 2025 guidance, projecting a mid-single-digit decrease in EBITDA growth for the full year. The company expects free cash flow conversion to exceed 60% and anticipates total capital expenditures of US$400 million, including US$330 million for strategic growth initiatives.

In the US market, GCC forecasts flat cement volumes and mid-teens growth in concrete volumes, with flat price increases for both products. For Mexico, the company projects a mid-single-digit decrease in cement volumes with mid-single-digit price increases.

The full 2025 guidance is detailed here:

This outlook represents a more cautious stance compared to earlier in the year, consistent with the company’s Q1 2025 messaging when CEO Enrique Escalante noted they were entering 2025 "with cautious optimism" amid market uncertainties.

Despite the challenging quarter, GCC maintains that its strategic fundamentals remain intact, with management emphasizing its focus on operational efficiencies, cost optimization, and disciplined capital deployment to navigate the current market environment while building long-term value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.