Stock market today: S&P 500 falls as government shutdown, trade jitters persist

GE HealthCare Technologies Inc (NASDAQ:GEHC) released its second quarter 2025 earnings presentation on July 30, showing modest organic growth and raising its full-year guidance despite margin pressure from tariffs. The healthcare equipment manufacturer reported solid order growth and record backlog, signaling continued demand strength in key markets.

Quarterly Performance Highlights

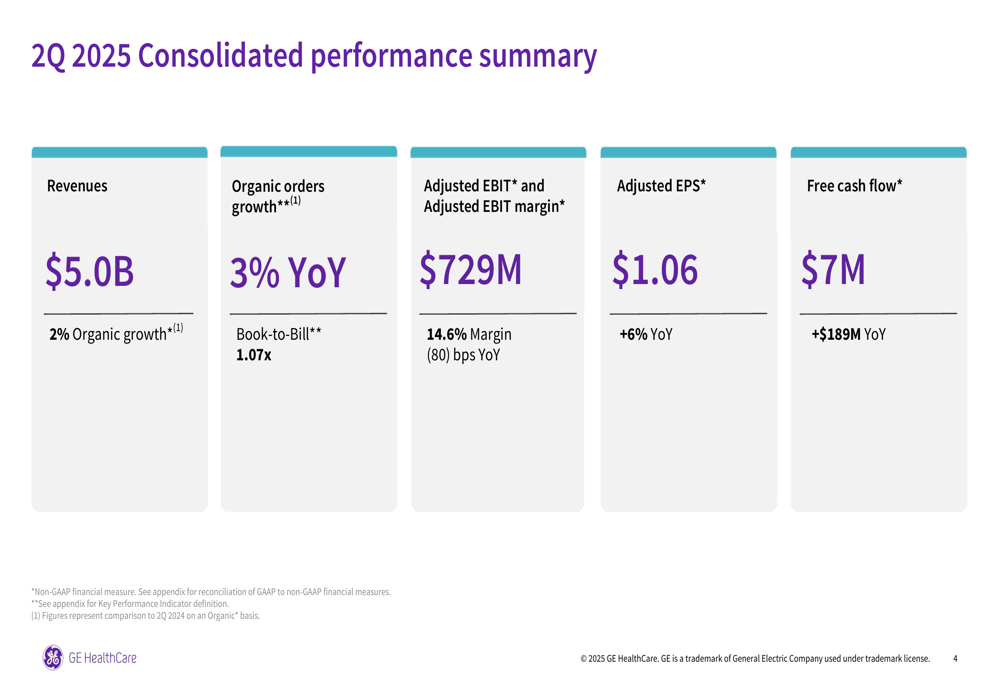

GE HealthCare delivered Q2 2025 revenue of $5.0 billion, representing 2% organic growth year-over-year. The company reported adjusted earnings per share of $1.06, up 6% compared to the same period last year, while adjusted EBIT reached $729 million with a margin of 14.6%, down 80 basis points year-over-year. Free cash flow improved significantly to $7 million, a $189 million increase from Q2 2024.

Orders grew 3% organically with a book-to-bill ratio of 1.07x, indicating healthy future revenue potential. The company highlighted strong performance in the U.S. and EMEA regions as key growth drivers.

As shown in the following consolidated performance summary:

Segment performance varied considerably across the company’s four business units. Advanced Visualization Solutions (AVS) emerged as the strongest performer, with 2% revenue growth and a 4% increase in segment EBIT, resulting in margin expansion of 20 basis points to 20.7%. Pharmaceutical (TADAWUL:2070) Diagnostics (PDx) saw the highest revenue growth at 5%, though margins declined 200 basis points to 29.3%.

The Imaging segment, GE HealthCare’s largest business unit, faced challenges with segment EBIT declining 10% despite 1% revenue growth, resulting in margin compression of 110 basis points to 8.5%. Patient Care Solutions (PCS) experienced the most significant pressure with flat revenue but a 23% decline in segment EBIT, driving margins down 240 basis points to 7.7%.

Tariff Impact & Mitigation Strategy

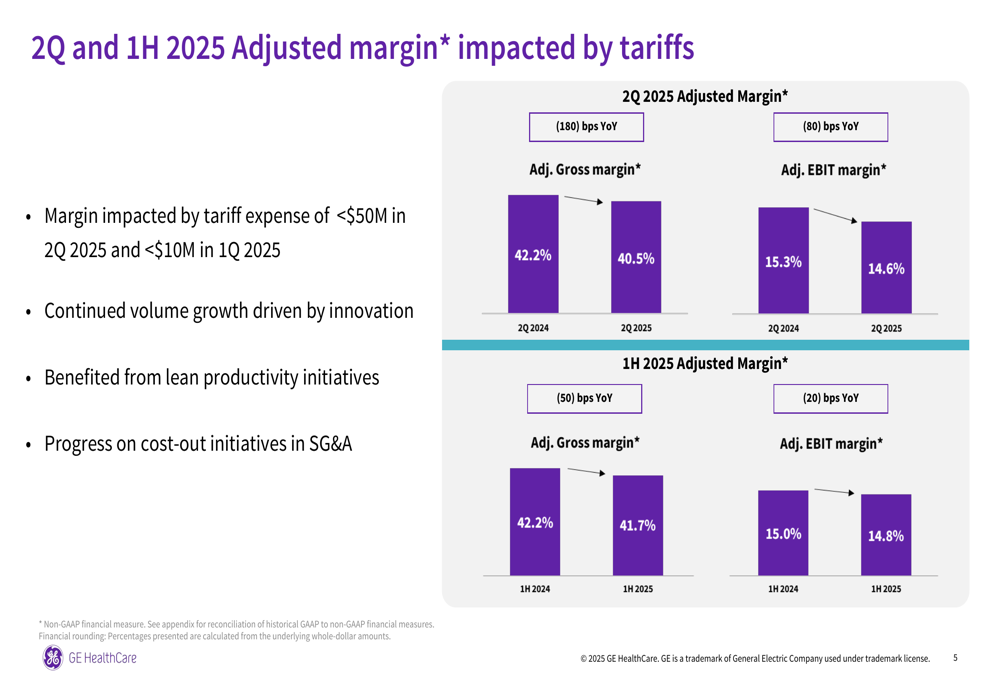

A key narrative throughout the presentation was the impact of tariffs on the company’s margins. GE HealthCare reported tariff expenses of less than $50 million in Q2 2025, compared to less than $10 million in Q1, demonstrating the escalating impact on profitability.

The following chart illustrates how tariffs affected the company’s margins:

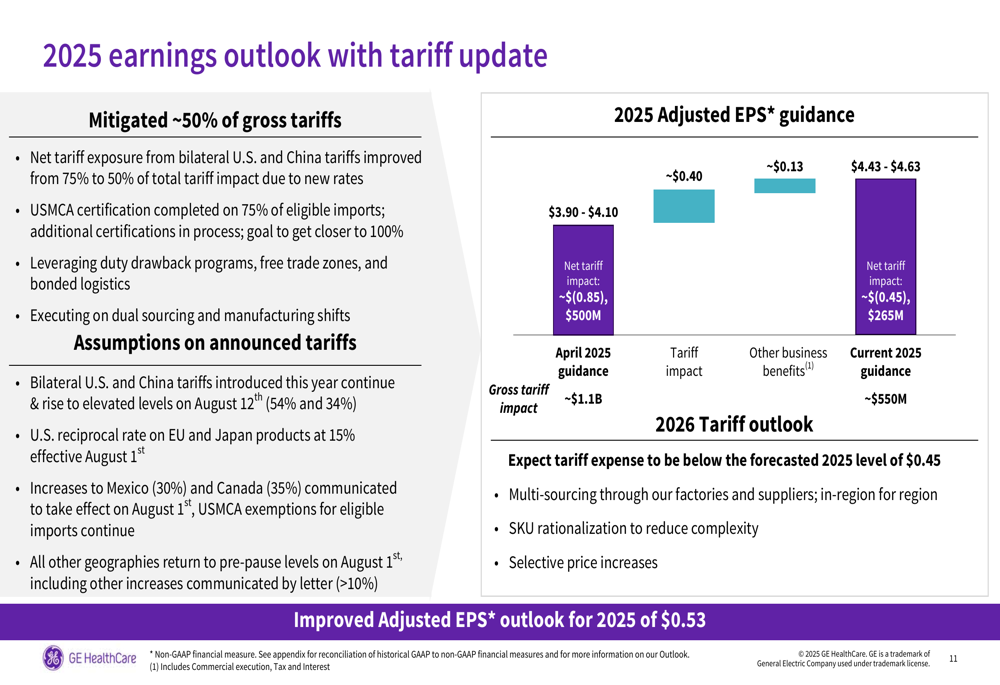

Despite these headwinds, GE HealthCare has implemented a comprehensive tariff mitigation strategy. The company reported it has successfully mitigated approximately 50% of gross tariffs through various initiatives including duty drawback programs, free trade zones, bonded logistics, dual sourcing, and manufacturing shifts.

The company’s tariff mitigation efforts are detailed in this slide:

"We’ve made significant progress in mitigating tariff impacts through our multi-faceted approach," the company noted in its presentation. "Our expectation is for tariff expense to be below the 2025 level of $0.45 by multi-sourcing through factories, rationalizing SKUs, and selective price increases."

Strategic Growth Initiatives

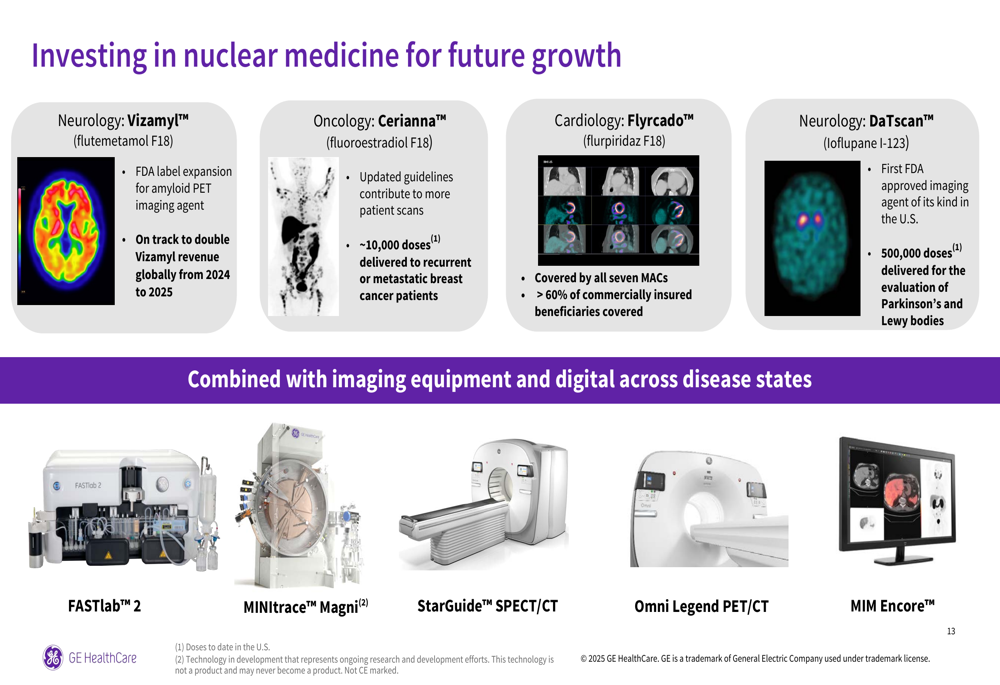

GE HealthCare highlighted its strategic focus on nuclear medicine as a key growth driver. The company is investing across multiple therapeutic areas including neurology, oncology, and cardiology with products like Vizamyl, Cerianna, Flyrcado, and DaTscan.

The following slide showcases the company’s nuclear medicine portfolio:

Innovation remains central to the company’s strategy, with the presentation featuring several new product launches. The Omni Legend PET/CT was highlighted as the company’s "fastest ever selling PET/CT," designed to meet growing market demands with scalable and performance-focused features.

The company also mentioned a unique collaboration with Egypt’s Ministry of Health to localize ultrasound production, advancing its strategy to win in emerging markets.

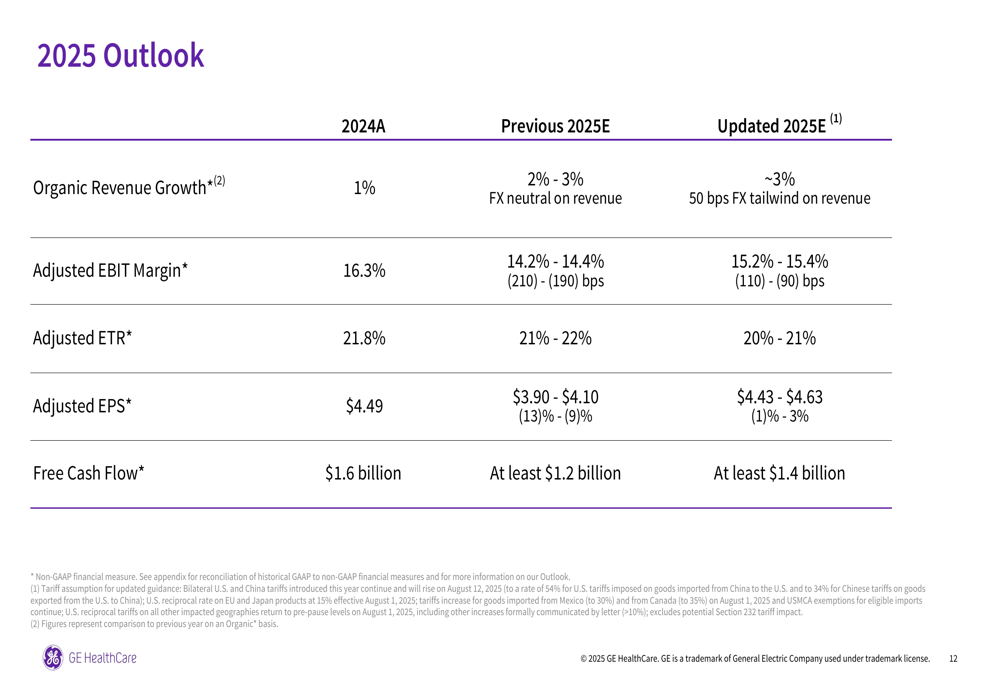

Revised 2025 Outlook

In a significant development, GE HealthCare raised its full-year 2025 guidance across all key metrics. Organic revenue growth is now expected to reach approximately 3%, up from the previous guidance of 2-3%. Adjusted EBIT margin guidance was raised substantially from 14.2-14.4% to 15.2-15.4%, while adjusted EPS guidance increased from $3.90-$4.10 to $4.43-$4.63.

The company also raised its free cash flow guidance from at least $1.2 billion to at least $1.4 billion, reflecting confidence in its operational execution and cash generation capabilities.

The updated outlook is presented in the following slide:

This revised guidance represents a significant improvement from the outlook provided after Q1 2025, when the company projected organic revenue growth between 2% and 3% and adjusted EPS in the range of $3.90 to $4.10.

Market Context

GE HealthCare’s stock was trading slightly lower in premarket activity, down 0.28% to $77.50, according to available market data. This modest decline comes despite the raised guidance, potentially reflecting investor concerns about margin pressure from tariffs.

The Q2 results show a slowdown from Q1 2025, when the company reported 4% organic revenue growth compared to Q2’s 2%. However, the sequential improvement in adjusted EPS from $1.01 in Q1 to $1.06 in Q2 demonstrates the company’s ability to drive bottom-line growth despite headwinds.

In its summary, GE HealthCare emphasized "solid orders and revenue performance supported by strong customer demand," "driving value through innovation," and "raising guidance with healthy end markets" as key takeaways for investors, positioning the company for continued growth despite the challenging trade environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.