Walmart halts H-1B visa offers amid Trump’s $100,000 fee increase - Bloomberg

Introduction & Market Context

Genworth Financial (NYSE:GNW) released its second quarter 2025 investor presentation on July 30, 2025, revealing solid financial performance primarily driven by its Enact segment, while continuing to navigate challenges in its long-term care insurance business. The company’s stock closed at $8.68, up 1.61% in regular trading following the results, though it dipped slightly by 0.92% in aftermarket trading to $8.60.

The company, with a market capitalization of $3.62 billion, reported net income of $51 million and adjusted operating income of $68 million for the quarter, translating to $0.16 per diluted share. These results align with Genworth’s strategic focus on strengthening its capital position while investing in future growth initiatives.

Quarterly Performance Highlights

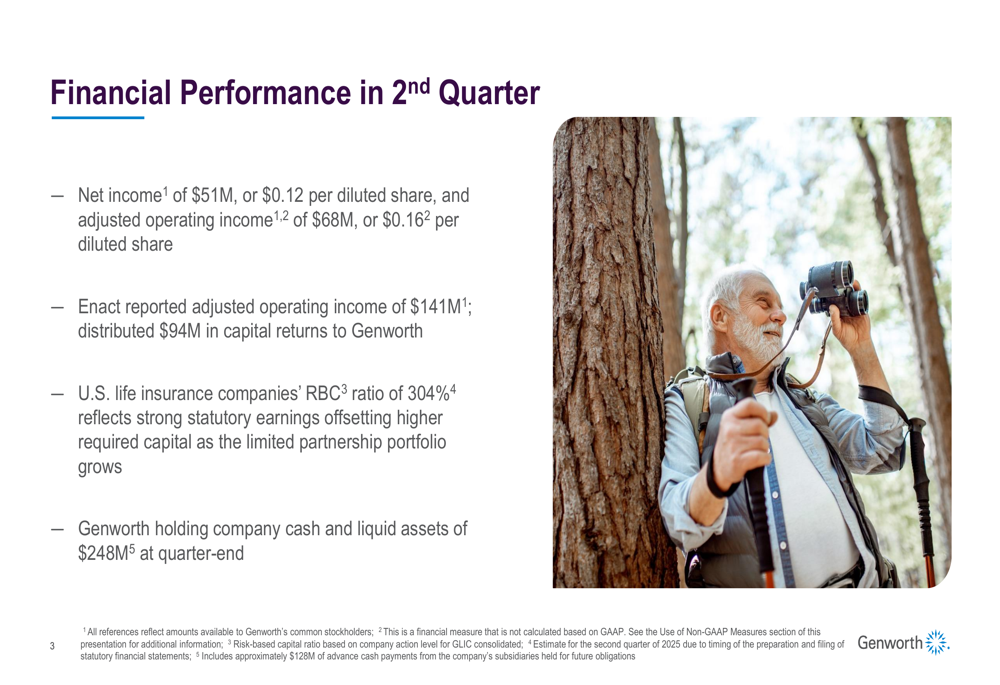

Genworth’s second quarter financial performance showed mixed results across its business segments, with Enact continuing to be the primary profit driver. The company reported net income of $51 million ($0.12 per diluted share) and adjusted operating income of $68 million ($0.16 per diluted share).

As shown in the following financial highlights slide:

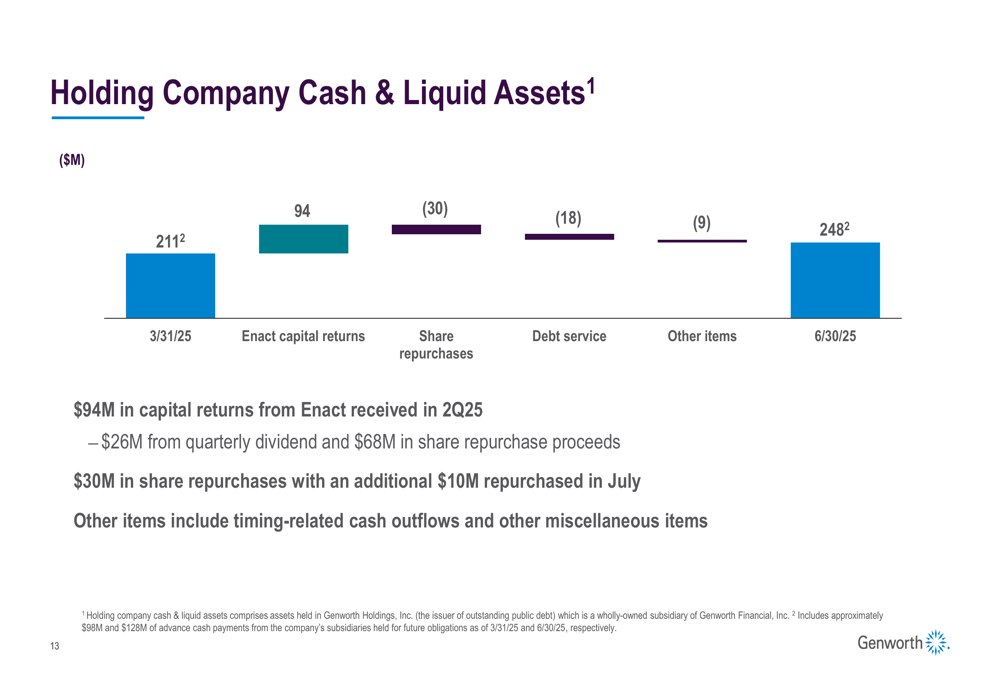

Enact, Genworth’s mortgage insurance business, reported adjusted operating income of $141 million and distributed $94 million in capital returns to Genworth during the quarter. The U.S. life insurance companies maintained a solid Risk-Based Capital (RBC) ratio of 304%, reflecting strong statutory earnings that offset higher required capital as the limited partnership portfolio grows. The holding company ended the quarter with $248 million in cash and liquid assets.

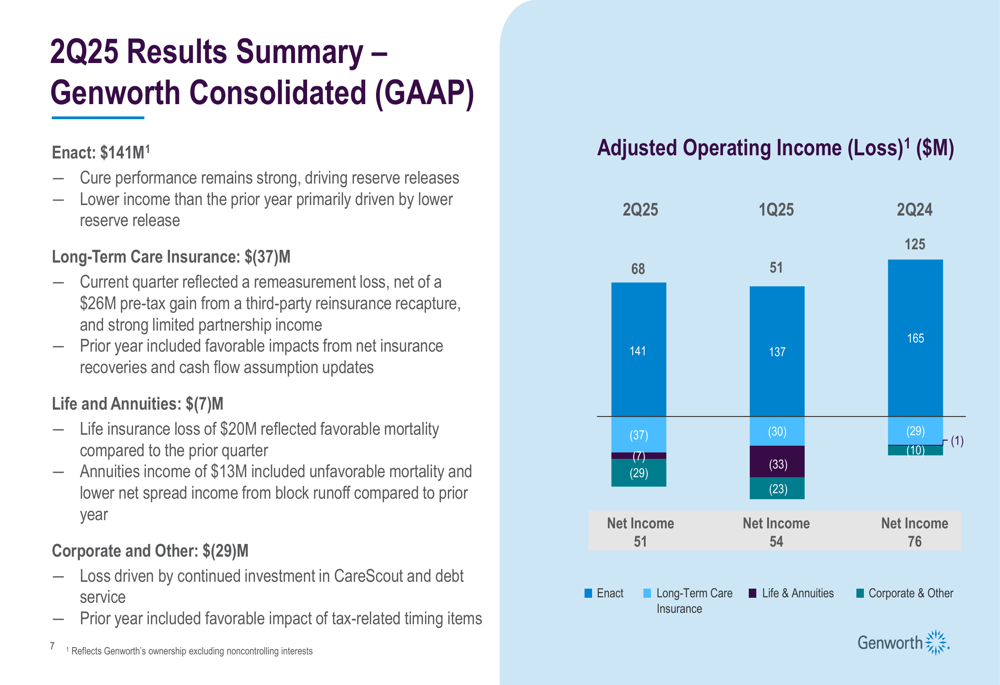

The segment breakdown reveals the contrasting performance across Genworth’s businesses:

While Enact delivered strong results, the Long-Term Care Insurance segment reported a loss of $37 million, which included a remeasurement loss partially offset by a $26 million pre-tax gain from a third-party reinsurance recapture and strong limited partnership income. The Life and Annuities segment showed improvement from the previous quarter but still posted a $7 million loss, with life insurance losses of $20 million offset by annuities income of $13 million. The Corporate and Other segment reported a $29 million loss, driven by continued investment in CareScout and debt service.

Strategic Initiatives

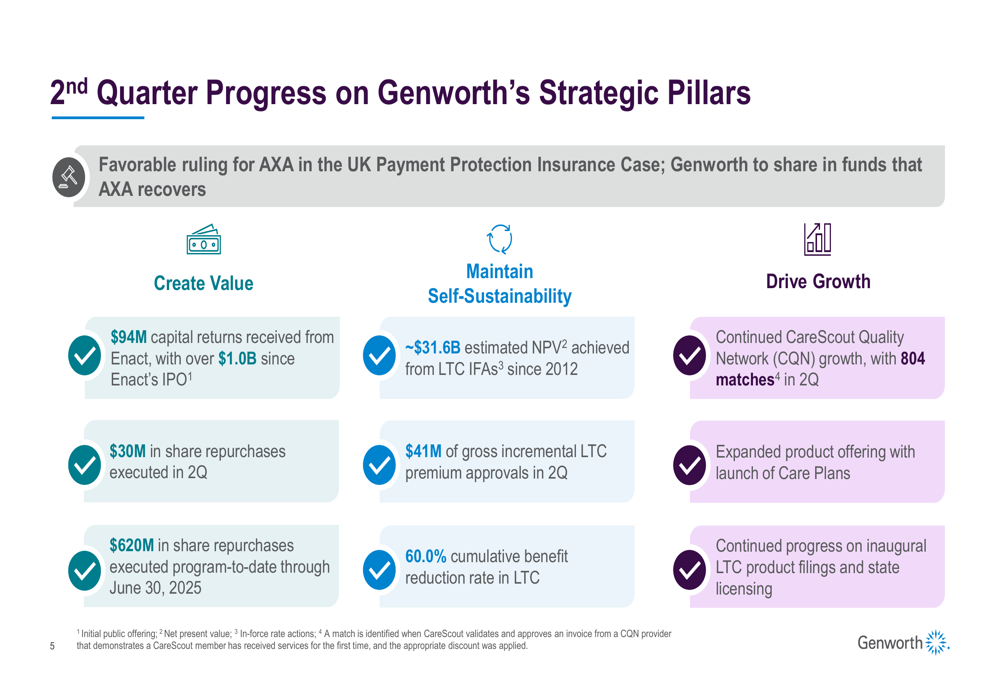

Genworth continues to execute on its three strategic pillars: creating value through Enact, maintaining self-sustainability in legacy insurance businesses, and driving future growth through CareScout. The company made notable progress across all three areas during the second quarter:

In terms of value creation, Genworth received $94 million in capital returns from Enact during the quarter, bringing the total to over $1.0 billion since Enact’s IPO. The company also executed $30 million in share repurchases in Q2, with program-to-date repurchases reaching $620 million through June 30, 2025.

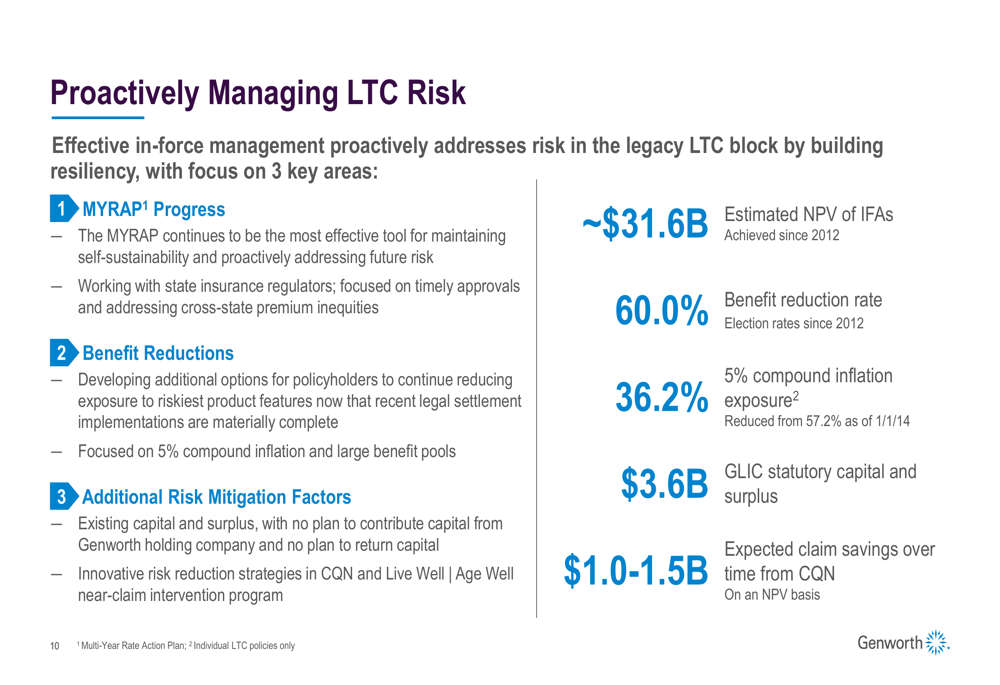

For its legacy long-term care business, Genworth continues to focus on maintaining self-sustainability through in-force rate actions (IFAs) and benefit reductions. The company has achieved an estimated net present value of $31.6 billion from LTC IFAs since 2012 and secured $41 million of gross incremental LTC premium approvals in Q2. The cumulative benefit reduction rate in LTC has reached 60.0%.

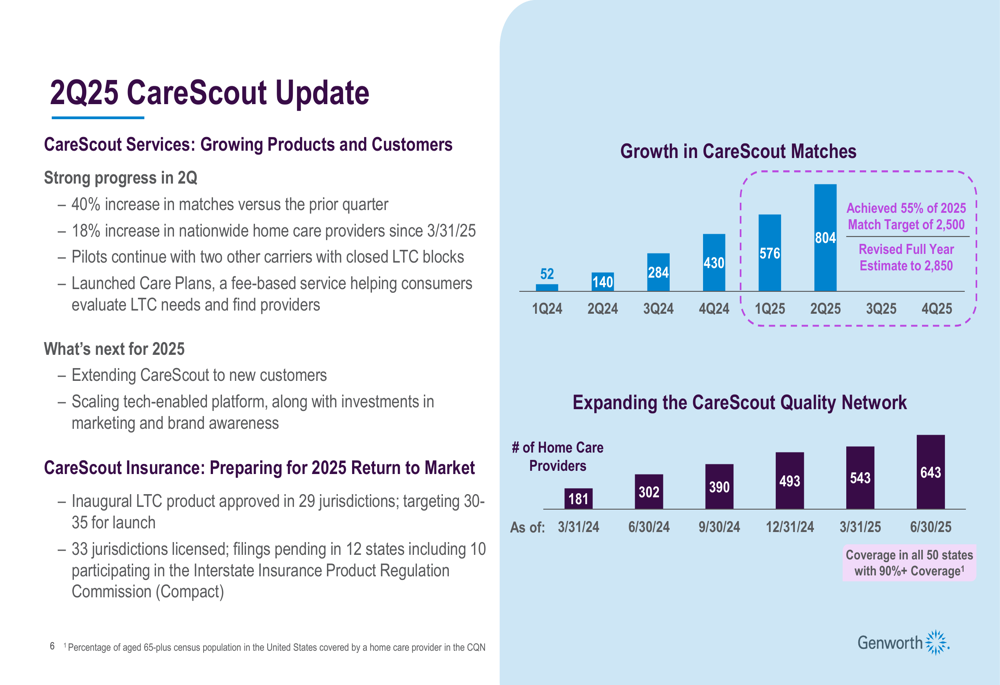

The CareScout business, Genworth’s growth initiative focused on aging care services, showed promising momentum:

CareScout achieved a 40% increase in matches versus the prior quarter and an 18% increase in nationwide home care providers since March 31, 2025. The company also launched Care Plans, a fee-based service helping consumers evaluate long-term care needs and find providers. On the insurance front, CareScout’s inaugural LTC product has been approved in 29 jurisdictions, with the company targeting 30-35 jurisdictions for launch.

Detailed Financial Analysis

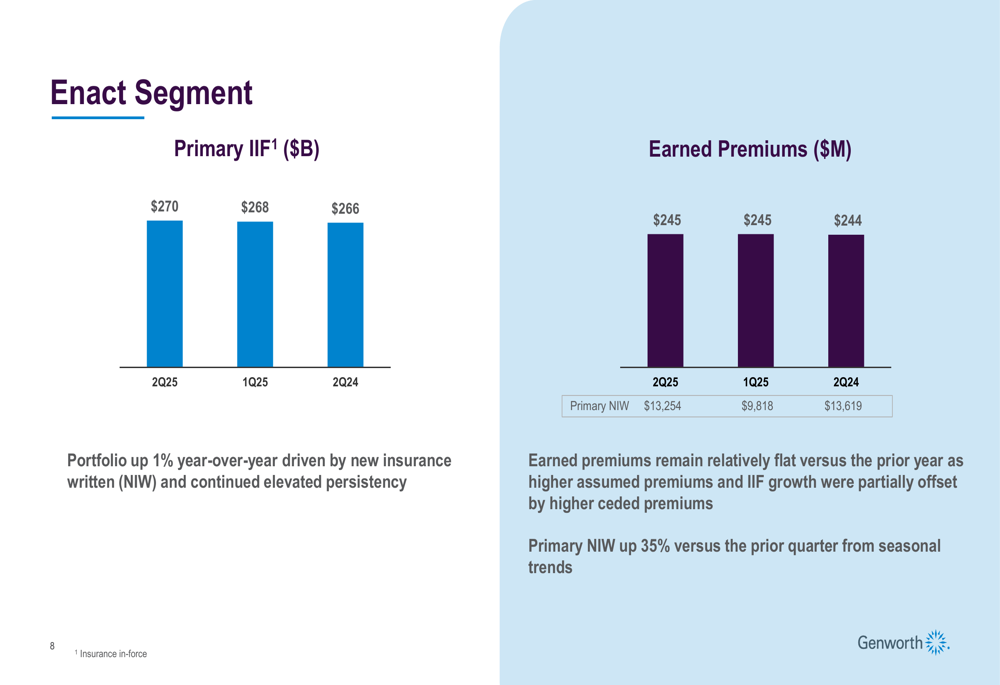

Enact continues to be Genworth’s strongest performing segment, with stable earned premiums and growth in its insurance in force:

Enact’s primary insurance in force (IIF) grew to $270 billion, up 1% year-over-year, driven by new insurance written (NIW) and continued elevated persistency. Earned premiums remained relatively flat at $245 million compared to the prior year, as higher assumed premiums and IIF growth were offset by higher ceded premiums. Primary NIW increased 35% versus the prior quarter to $13.25 billion, reflecting seasonal trends.

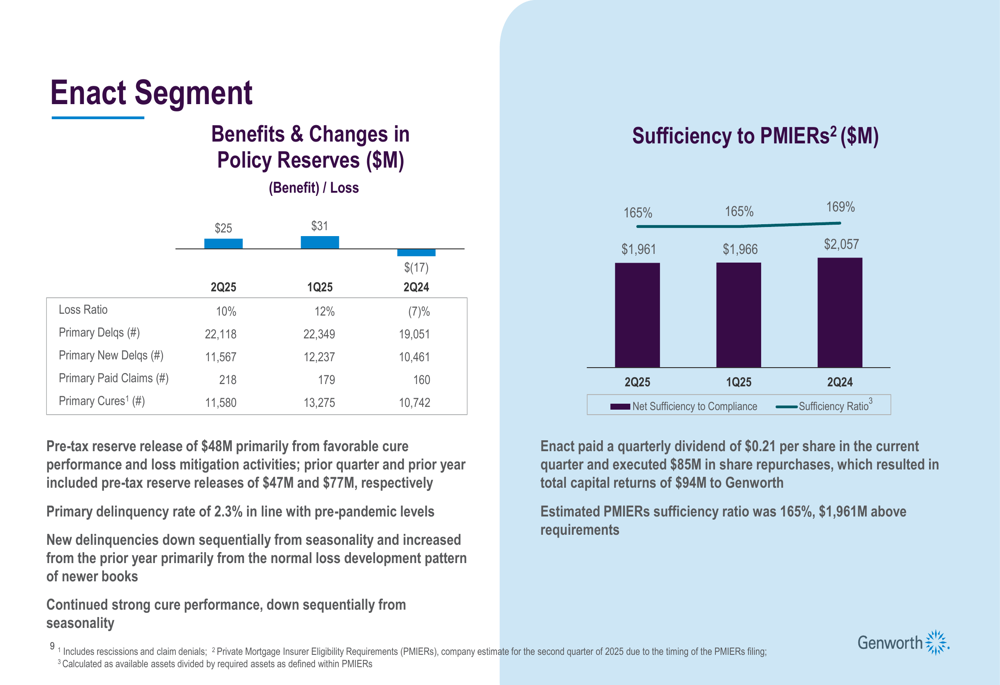

The segment also demonstrated strong credit performance:

Enact reported a pre-tax reserve release of $48 million, primarily from favorable cure performance and loss mitigation activities. The primary delinquency rate stood at 2.3%, in line with pre-pandemic levels. Enact maintained a strong capital position with a PMIERs sufficiency ratio of 165%, representing $1.96 billion above requirements.

For the Long-Term Care Insurance segment, Genworth continues to proactively manage risk:

The company’s Multi-Year Rate Action Plan (MYRAP) remains the most effective tool for maintaining self-sustainability and proactively addressing future risk. Genworth is also developing additional options for policyholders to reduce exposure to the riskiest product features, focusing on 5% compound inflation and large benefit pools. The company has reduced its 5% compound inflation exposure to 36.2% from 57.2% as of January 1, 2014.

Forward-Looking Statements

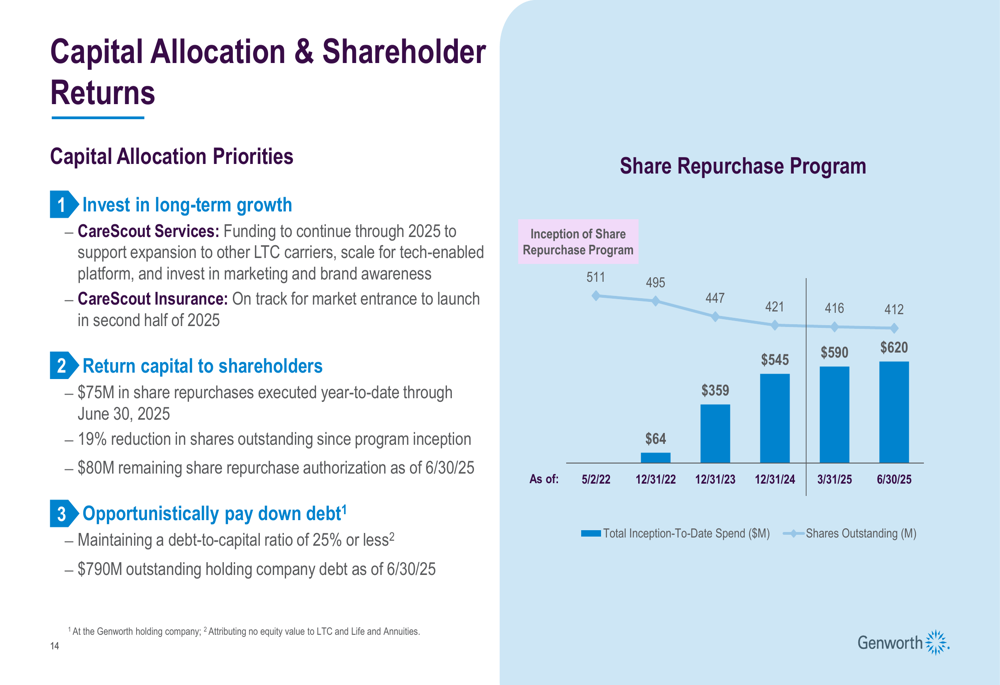

Genworth’s capital allocation priorities focus on investing in long-term growth, returning capital to shareholders, and managing debt:

The company plans to continue funding CareScout Services through 2025 to support expansion to other LTC carriers, scale its tech-enabled platform, and invest in marketing and brand awareness. CareScout Insurance remains on track for market entrance in the second half of 2025.

In terms of shareholder returns, Genworth executed $75 million in share repurchases year-to-date through June 30, 2025, resulting in a 19% reduction in shares outstanding since the program’s inception. The company had $80 million remaining in its share repurchase authorization as of June 30, 2025.

Genworth is also maintaining a debt-to-capital ratio of 25% or less, with $790 million in outstanding holding company debt as of the end of the quarter. The company’s holding company cash position improved during the quarter:

Holding company cash and liquid assets increased from $211 million at March 31, 2025, to $248 million at June 30, 2025, primarily due to $94 million in capital returns from Enact, partially offset by $30 million in share repurchases, $18 million in debt service, and $9 million in other items.

According to the earnings call, CEO Tom McInerney expressed confidence in Genworth’s position, stating, "We are stronger today than we’ve ever been." He also addressed the ongoing AXA litigation, noting, "We feel very good about the prospects of prevailing," and highlighted the importance of private market solutions like those offered by CareScout.

As Genworth continues to execute its strategic plan, the company faces ongoing challenges in its legacy businesses while building momentum in its growth initiatives. Investors will be watching closely to see if CareScout can deliver on its promise as a future growth driver while Enact continues to provide strong capital returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.