US stock futures inch higher with Q3 earnings on tap

Introduction & Market Context

Graham Corporation (NYSE:GHM), a global leader in mission-critical fluid, power, vacuum, and heat transfer solutions, presented its first quarter fiscal 2026 financial results on August 5, 2025, showcasing strong performance across key metrics. Despite reporting double-digit growth in revenue and profitability, the company’s stock fell sharply, reflecting investor concerns about future growth prospects.

The company’s presentation highlighted an 11% year-over-year revenue increase and a record backlog, positioning Graham for continued growth in its core markets of defense, energy and process, and space. However, the stock dropped 17.5% in trading following the announcement, suggesting a disconnect between the company’s positive outlook and market expectations.

Quarterly Performance Highlights

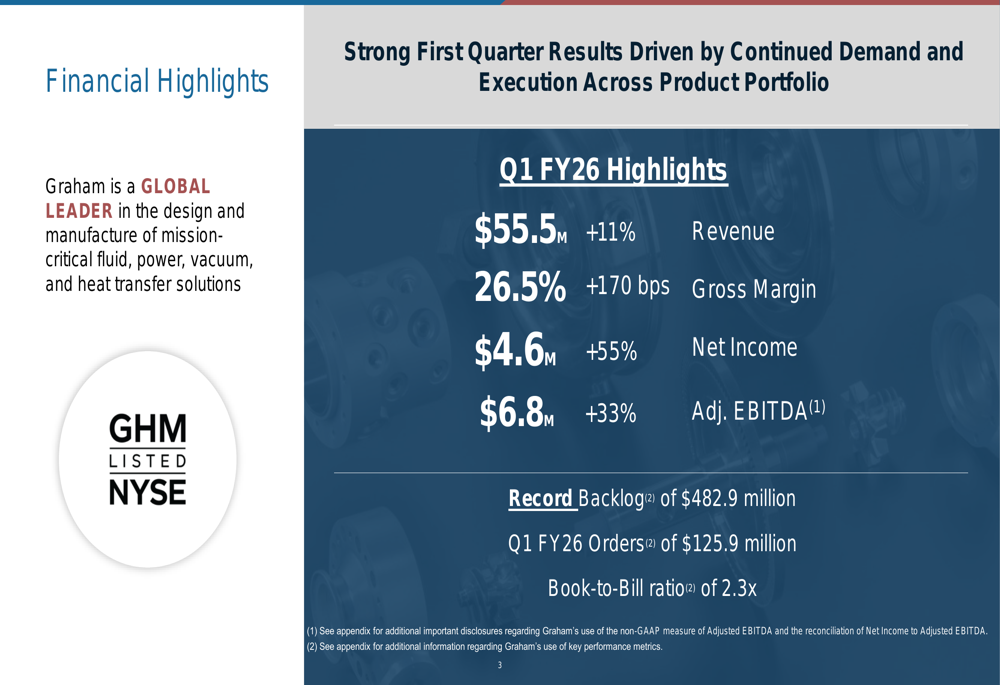

Graham reported solid financial results for Q1 FY26, with revenue reaching $55.5 million, up 11% compared to the same period last year. This growth was primarily driven by a 33% increase in both the Energy & Process segment and Aftermarket sales, while Defense grew by 2%. The Space segment experienced a 14% decline.

The company’s profitability metrics showed significant improvement, with gross margin expanding 170 basis points to 26.5%. Net income rose 55% to $4.6 million, or $0.42 per diluted share, while Adjusted EBITDA increased 33% to $6.8 million, representing a margin of 12.3%.

As shown in the following summary of Q1 FY26 financial highlights:

The company attributed these improvements to increased volume, better pricing and execution, and an improved mix of higher-margin sales. The quarterly performance continues a positive trend seen over the past year, with trailing twelve-month revenue reaching $215.4 million and Adjusted EBITDA margin expanding to 11.2%.

Strategic Investments and Growth Initiatives

Graham is making significant strategic investments across its business segments to fuel future growth, with all projects targeting returns on invested capital exceeding 20%. These investments span the company’s defense, energy and process, and space segments, with several key projects completed in Q1 FY26.

The following slide illustrates Graham’s organic investment strategy across its business segments:

In the Defense segment, Graham completed a new Navy facility in Q1 FY26, supported by a $13.5 million customer grant, and is on track to complete an X-Ray facility by the end of calendar year 2025. For the Energy & Process segment, the company completed a renovated Assembly & Test Facility in Arvada, Colorado, and is implementing an aftermarket acceleration initiative utilizing AI technology.

The Space segment is nearing completion of a P3 Cryogenic Test Facility in Jupiter, Florida, with Liquid Nitrogen Testing expected to be operational by August in Arvada. Corporate investments include IT infrastructure upgrades and an ERP system upgrade in Batavia scheduled for completion in Q3 FY26.

Backlog and Order Trends

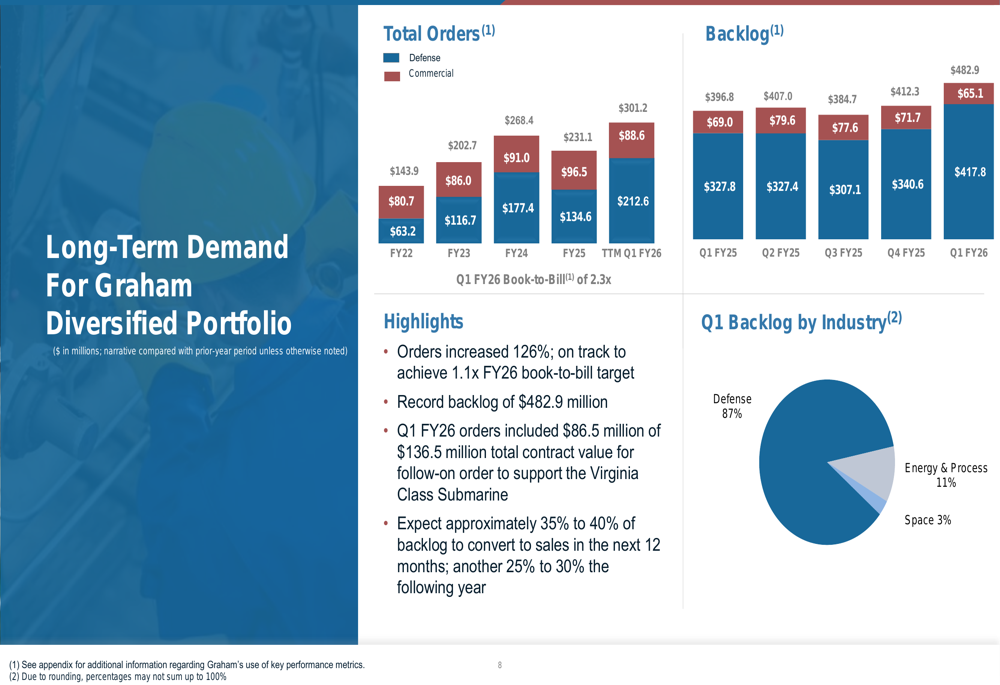

One of the most significant highlights from Graham’s presentation was the record backlog of $482.9 million at the end of Q1 FY26, representing a substantial increase from $412.3 million at the end of the previous quarter and $396.8 million a year ago. This growth was driven by strong order intake of $125.9 million during the quarter, resulting in a book-to-bill ratio of 2.3x.

The company’s order trends and backlog composition are illustrated in the following slide:

The backlog is heavily weighted toward the defense sector, which accounts for 87% of the total, while Energy & Process represents 11% and Space comprises 3%. Graham expects 35-40% of the current backlog to convert to sales within the next 12 months, providing solid visibility for future revenue growth.

The trailing twelve-month orders as of Q1 FY26 reached $212.6 million, significantly higher than the $134.6 million reported for fiscal 2025, indicating accelerating demand for Graham’s products and services.

Fiscal 2026 Guidance and Long-Term Goals

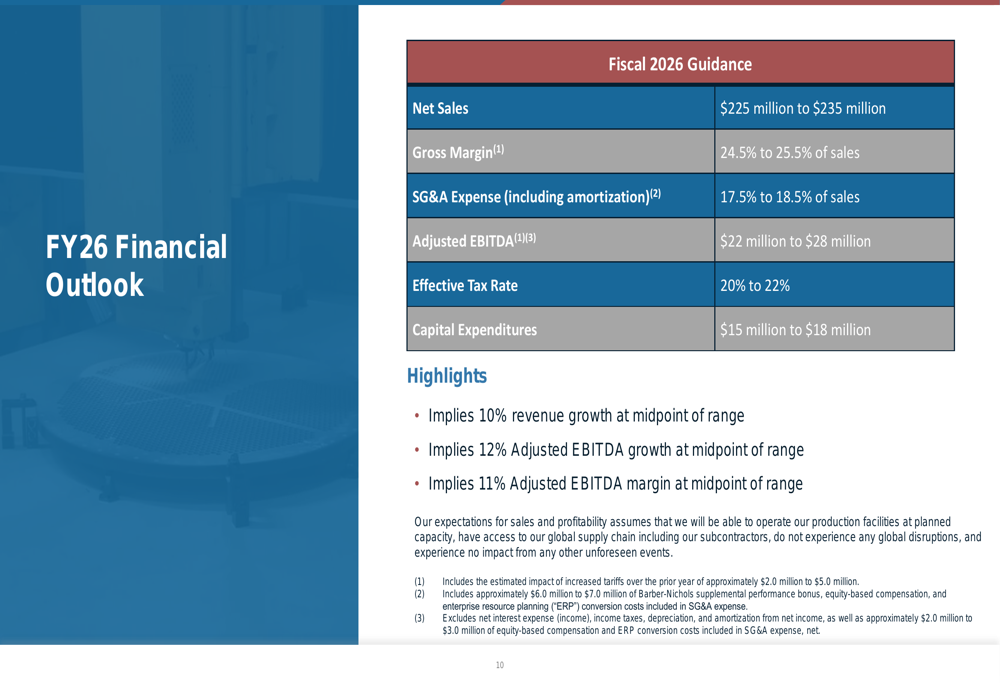

Graham provided guidance for fiscal 2026, projecting revenue between $225 million and $235 million, representing approximately 10% growth at the midpoint compared to fiscal 2025. The company expects gross margin to range from 24.5% to 25.5% of sales and Adjusted EBITDA between $22 million and $28 million, implying a margin of approximately 11% at the midpoint.

The detailed fiscal 2026 guidance is presented in the following slide:

Looking beyond fiscal 2026, Graham outlined its long-term financial goals, targeting revenue of $245-255 million by fiscal 2027. The company’s strategic actions to achieve these goals include engaging with customers to develop full life-cycle mission-critical product opportunities, pursuing operational excellence, expanding capital and R&D programs, and engaging with key stakeholders to broaden its global reach.

The company’s progress toward these long-term goals is illustrated in the following slide:

Graham’s capital allocation framework prioritizes maintaining a strong balance sheet, investing in organic growth with capital expenditures of 7-10% of sales and R&D spending of 1-2% of sales, and pursuing strategic acquisitions with leverage below 3.0x.

Market Reaction and Analyst Perspectives

Despite the positive results and outlook presented by Graham, the company’s stock fell 17.5% to $47.38 following the earnings release. This decline suggests that investors may have had higher expectations or concerns about specific aspects of the company’s performance or guidance.

According to the earnings article, Graham’s revenue of $55.5 million slightly missed analyst expectations of $56.8 million, which may have contributed to the negative market reaction. However, the company’s EPS of $0.45 significantly exceeded the forecast of $0.24, representing an 87.5% positive surprise.

The stock’s performance stands in contrast to its strong run over the past year, during which it had returned over 100% before the Q1 earnings release. At current levels, some analysts consider the stock overvalued, trading at an EV/EBITDA multiple of 31.3x and a P/E ratio of 43.1x.

Looking ahead, analyst consensus remains cautiously optimistic, with price targets ranging from $52 to $65, suggesting potential upside from current levels. CEO Matt Moore expressed confidence in the company’s trajectory, stating, "We are just getting started," and emphasizing that Graham’s foundation is enabling consistent results.

As Graham continues to execute its strategic initiatives and capitalize on its record backlog, investors will be closely monitoring the company’s ability to convert these opportunities into sustainable revenue and profit growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.