Novo Nordisk, Eli Lilly fall after Trump comments on weight loss drug pricing

Introduction & Market Context

Green Brick Partners Inc (NASDAQ:GRBK) released its Q2 2025 earnings presentation on July 31, 2025, revealing a mixed performance characterized by operational strength but financial challenges. The homebuilder reported record closings and new orders, though earnings fell short of market expectations, leading to a 2.7% stock decline in after-hours trading to $62.99.

The company’s results reflect broader housing market challenges, including high interest rates and increased competition. Despite these headwinds, Green Brick maintained its industry-leading position in several key metrics while continuing to execute its land-focused strategy in supply-constrained markets.

Quarterly Performance Highlights

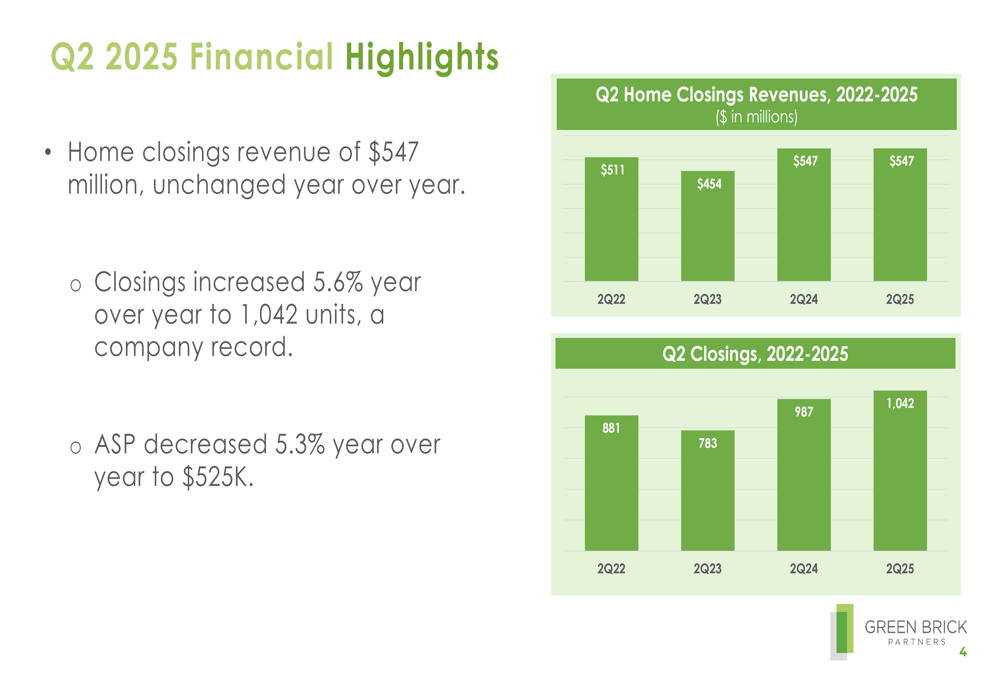

Green Brick delivered 1,042 homes in Q2 2025, a 5.6% increase year-over-year and a company record. However, home closings revenue remained flat at $547 million as the average sales price decreased 5.3% to $525,000, indicating price pressure in the current market environment.

As shown in the following chart of quarterly home closings and revenue:

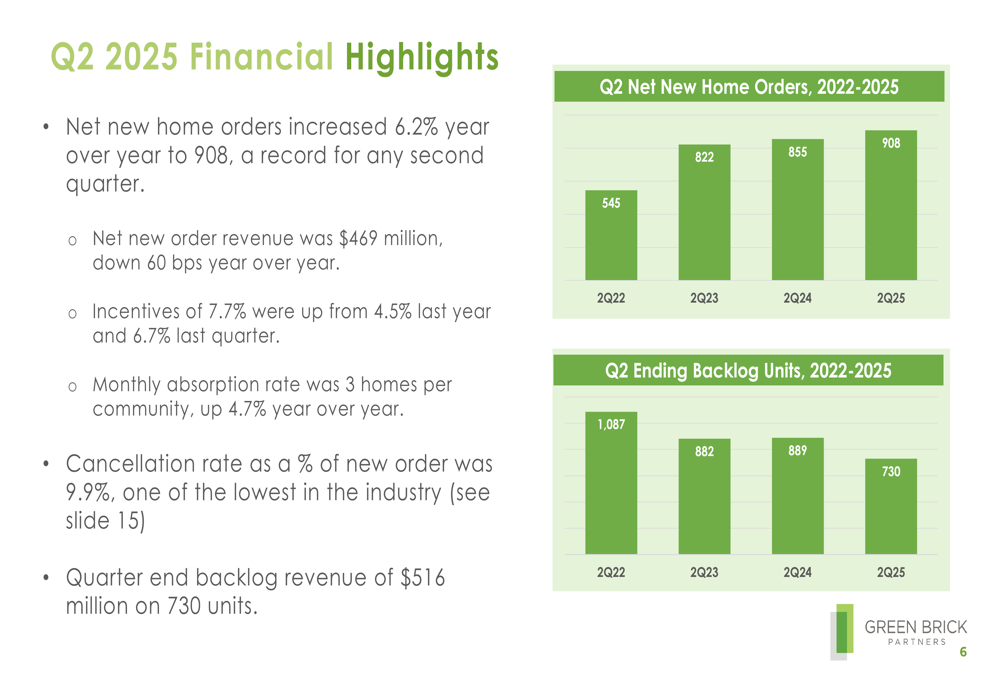

The company also achieved record second-quarter net new home orders, which increased 6.2% year-over-year to 908 units. This growth came despite a challenging market, though the company increased incentives to 7.7% from 4.5% last year to stimulate demand.

The order growth and backlog position are illustrated in this chart:

Detailed Financial Analysis

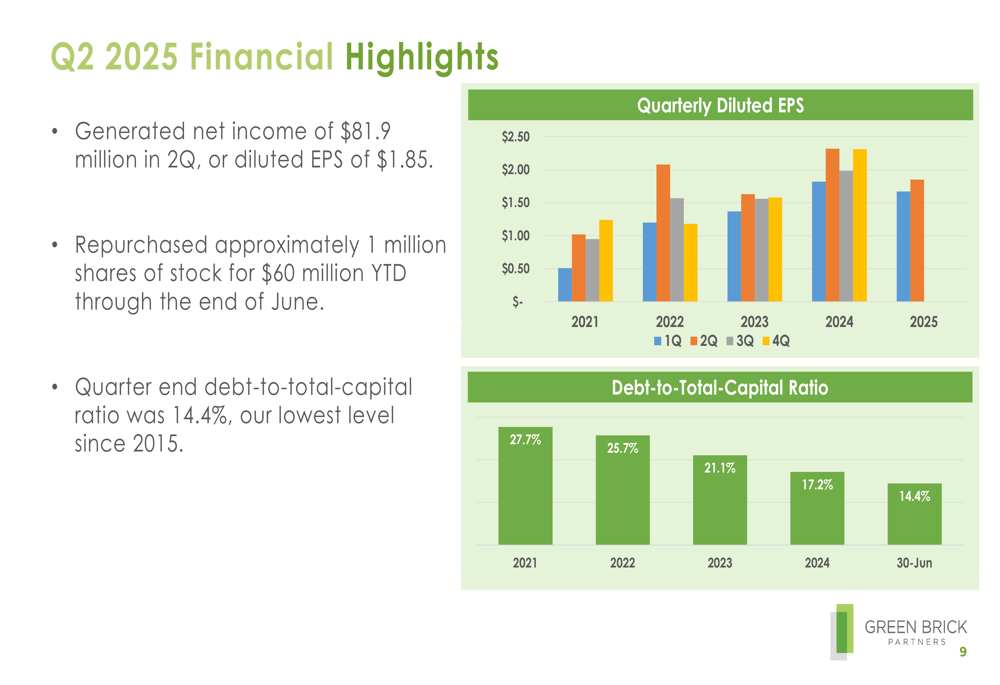

Despite operational achievements, Green Brick’s financial metrics showed some deterioration. Net income decreased 22.2% year-over-year to $81.9 million, with diluted earnings per share of $1.85, down 20.3% from $2.32 in Q2 2024. This EPS figure fell short of market expectations of $2.08, representing an 11.06% negative surprise according to the earnings report.

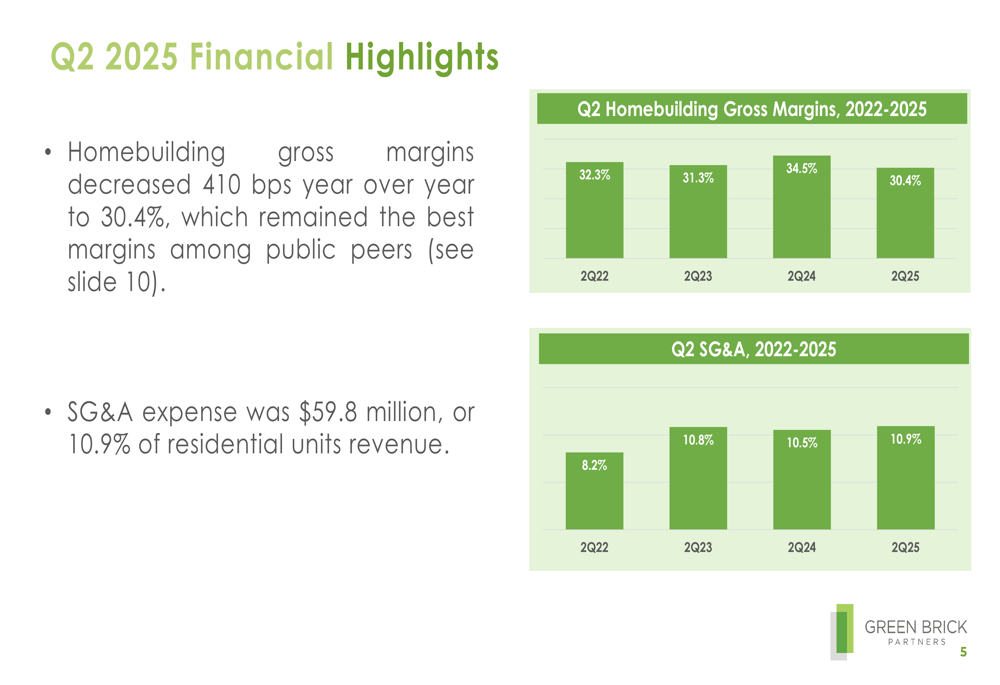

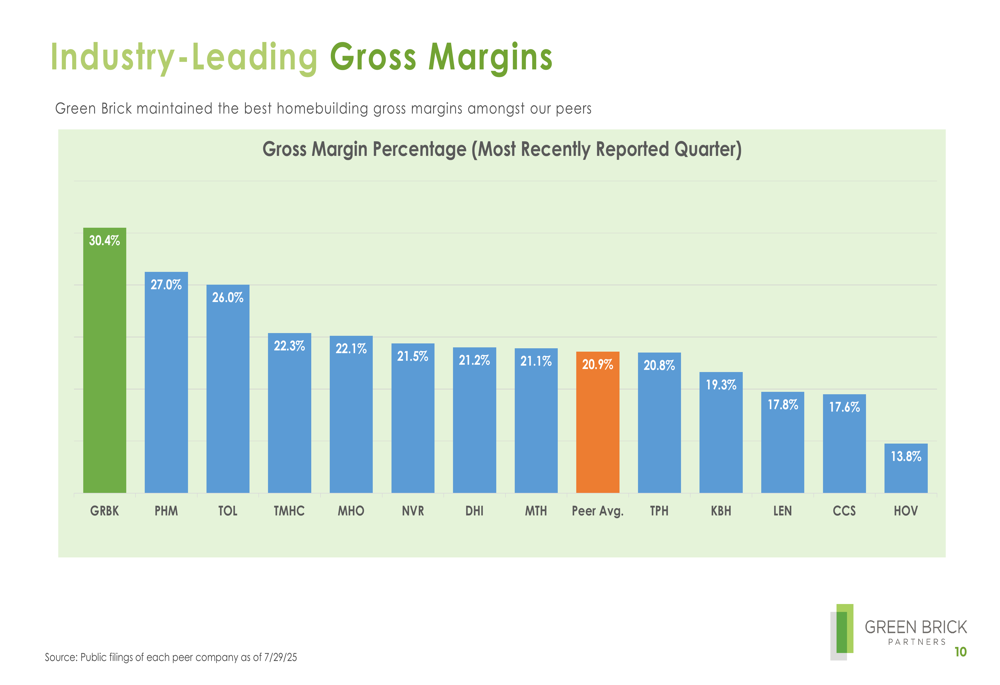

Homebuilding gross margins decreased 410 basis points year-over-year to 30.4%, while SG&A as a percentage of residential units revenue increased 40 basis points to 10.9%. However, the company emphasized that its margins remain the highest among public homebuilder peers.

The following chart illustrates the company’s gross margin performance:

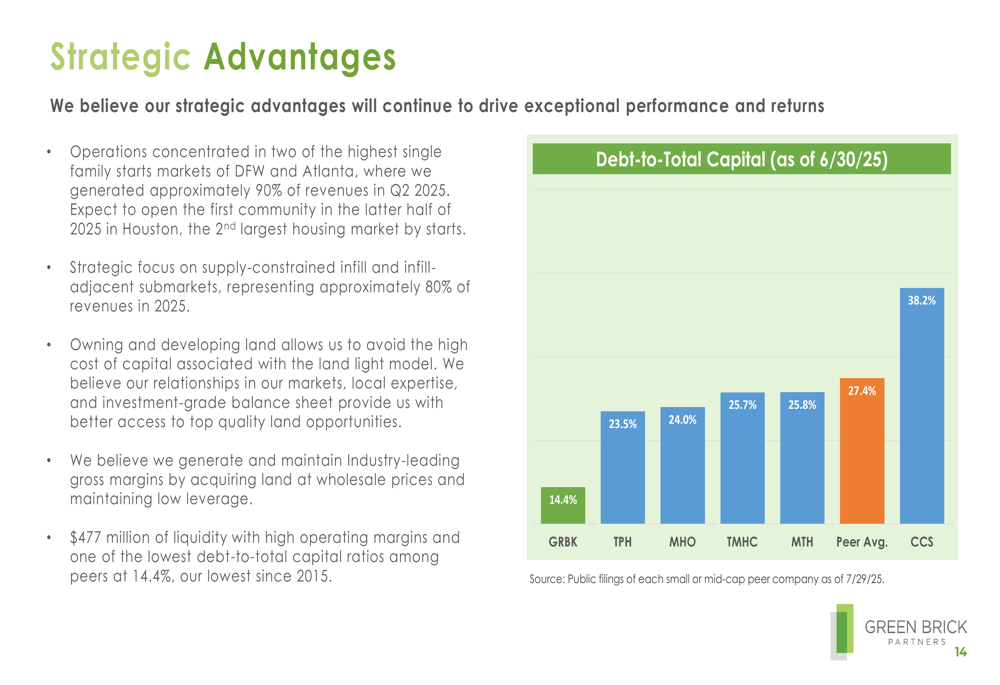

Green Brick maintained a strong balance sheet with $112 million in cash and $365 million in undrawn credit facilities. The company’s debt-to-total-capital ratio improved to 14.4%, its lowest level since 2015, providing financial flexibility in the current uncertain market.

The company’s EPS and debt trends are shown in this chart:

Competitive Industry Position

Despite margin pressure, Green Brick continues to lead the industry in gross margins at 30.4%, significantly outperforming the peer average of 20.9%. This competitive advantage is clearly illustrated in the following comparison:

The company also maintained one of the industry’s lowest cancellation rates at 9.9%, compared to a peer average of 14%. This metric suggests stronger buyer commitment and operational efficiency in Green Brick’s sales process.

Green Brick’s financial leverage remains among the lowest in the industry, with a debt-to-total-capital ratio of 14.4% compared to the peer average of 27.4%. This conservative financial position provides both stability and flexibility for future growth opportunities.

As shown in the following debt comparison:

Strategic Initiatives

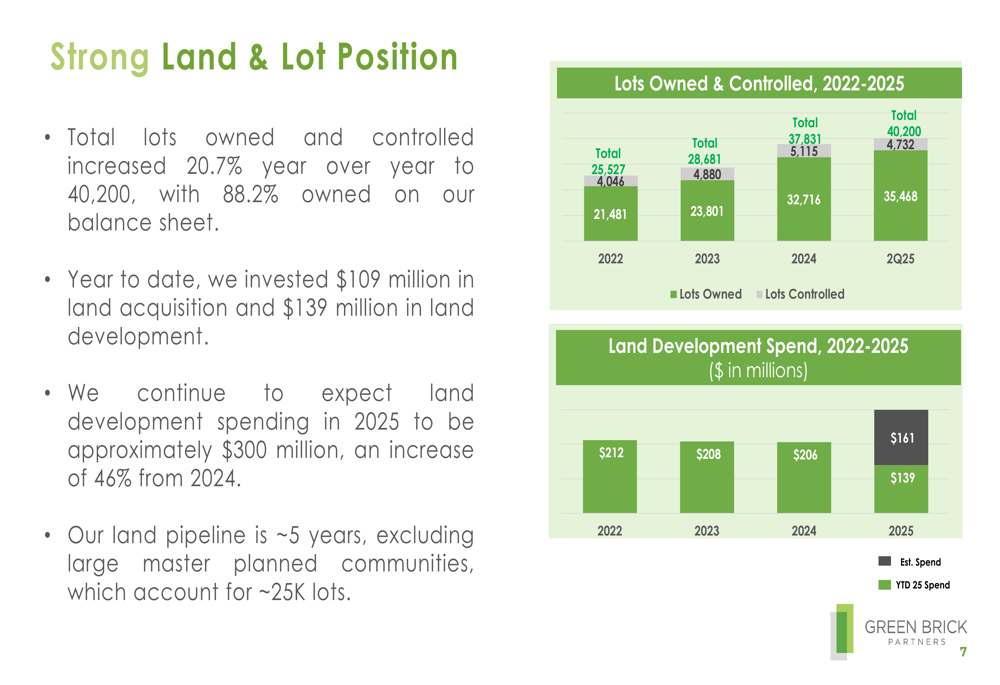

Green Brick’s strategic focus remains on land acquisition and development in supply-constrained markets. The company increased its total lots owned and controlled by 20.7% year-over-year to 40,200, with 88.2% owned on the balance sheet. This land-heavy strategy differs from many peers’ "land-light" approaches and has contributed to the company’s superior gross margins.

The following chart illustrates the company’s growing land position:

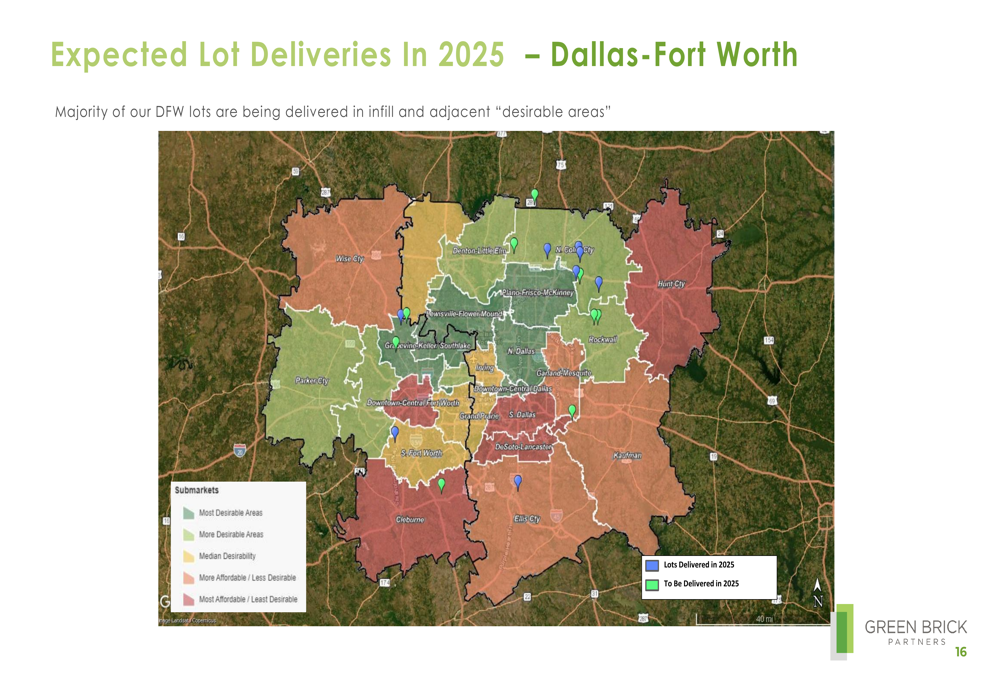

Geographically, Green Brick continues to concentrate on the Dallas-Fort Worth and Atlanta markets, which generated approximately 90% of revenues in Q2 2025. The company strategically focuses on infill and infill-adjacent submarkets, representing approximately 80% of revenues.

The company’s geographic strategy in Dallas-Fort Worth is illustrated in this map of expected lot deliveries:

Green Brick is also expanding its Trophy Signature Homes brand, which currently represents 37% of Q2 2025 revenues. The company plans to grow Trophy’s presence in Austin and Houston, with its first Houston community expected to open later in 2025.

Forward-Looking Statements

Looking ahead, Green Brick expects land development spending in 2025 to be approximately $300 million, an increase of 46% from 2024. This significant investment underscores the company’s commitment to its land-focused strategy despite current market challenges.

The company’s business priorities include balancing price and pace community by community to maximize returns, incrementally improving operations and cost efficiencies, and maintaining financial flexibility. Green Brick also plans to expand its wholly owned mortgage and insurance businesses throughout its markets.

While the presentation maintains an optimistic tone about the company’s strategic positioning, the earnings miss and stock price decline suggest investors remain cautious. According to the earnings report, future EPS forecasts range from $1.46 to $1.82 for upcoming quarters, with annual projections of $6.89 for 2025 and $7.16 for 2026.

Jim Brickman, CEO, expressed confidence in the company’s ability to navigate current market dynamics, stating, "We believe we are well positioned to navigate these market dynamics more effectively than our peers." However, challenges remain, including high interest rates impacting consumer demand, increased housing inventory leading to competitive pressures, and potential macroeconomic headwinds affecting the housing market.

Despite these challenges, Green Brick’s strong balance sheet, industry-leading margins, and strategic land position provide a solid foundation for weathering current market conditions and potentially capitalizing on future opportunities as the housing market evolves.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.