Joby Aviation closes $591 million stock offering with full underwriter option

Introduction & Market Context

GreenFirst Forest Products Inc. (TSX:GFP) presented its second quarter 2025 results on August 13, 2025, revealing a mixed performance characterized by increased revenue alongside widening losses. The company’s stock closed at $3.11, down 5.14% following the presentation, reflecting investor concerns about profitability challenges despite operational improvements.

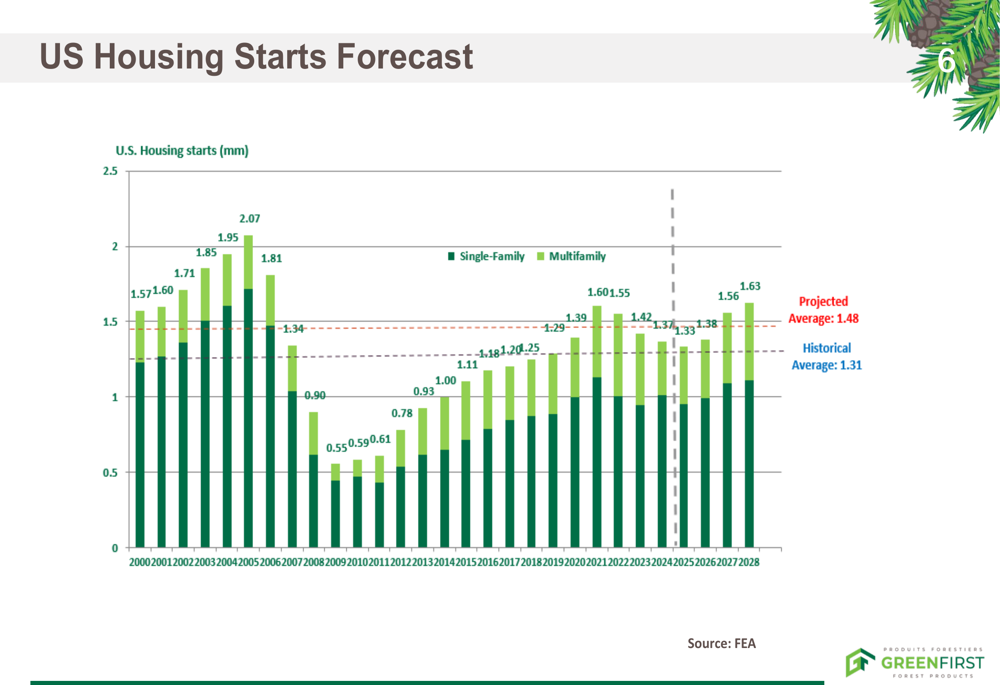

The presentation highlighted a positive outlook for the US housing market, which remains crucial for GreenFirst as it ships a majority of its lumber to American customers. According to Forest Economic Advisors (FEA) data shared in the presentation, US housing starts are projected to reach 1.38 million in 2025, increasing to 1.56 million in 2026 and 1.63 million in 2027, exceeding the historical average of 1.31 million.

As shown in the following chart of projected US housing starts:

However, this optimistic market outlook is tempered by significant trade challenges, including a new combined duty rate of 35.19% effective in early August, up from 14.4% previously. The company also noted the ongoing Section 232 investigation by the U.S. Department of Commerce, with findings expected in November 2025.

Quarterly Performance Highlights

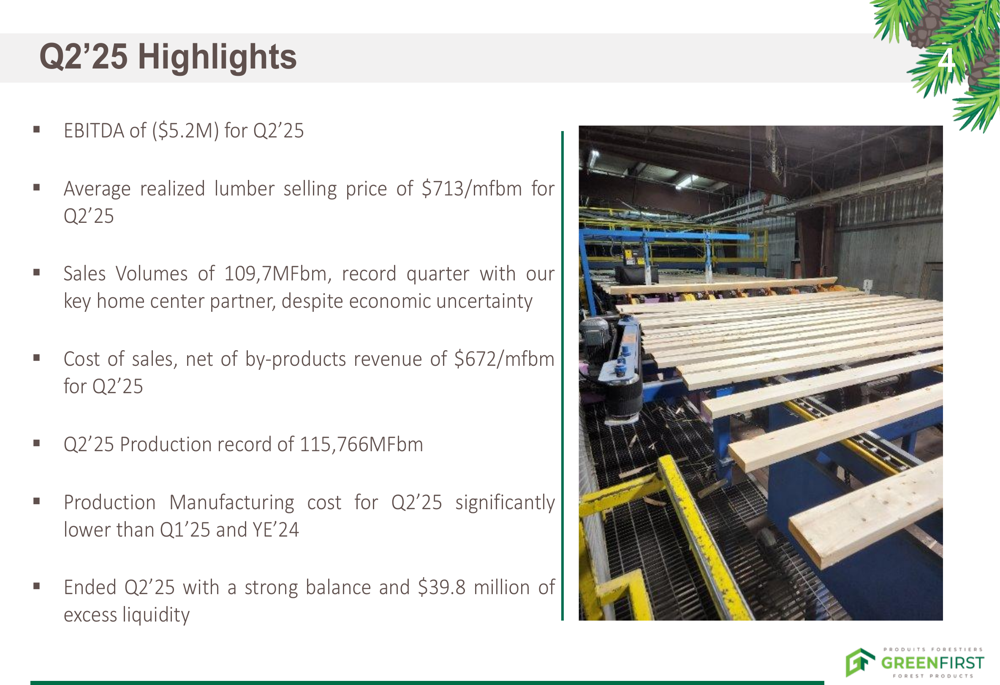

GreenFirst reported a substantial 18% quarter-over-quarter increase in revenue to $84.5 million for Q2 2025, up from $71.8 million in Q1 2025 and 21% higher than the $69.7 million reported in Q2 2024. This growth was driven by record production of 115,766 thousand board feet (MFbm) and sales volumes of 109,726 MFbm, which the company highlighted as a record quarter with its key home center partner.

The following slide details the company’s key performance metrics:

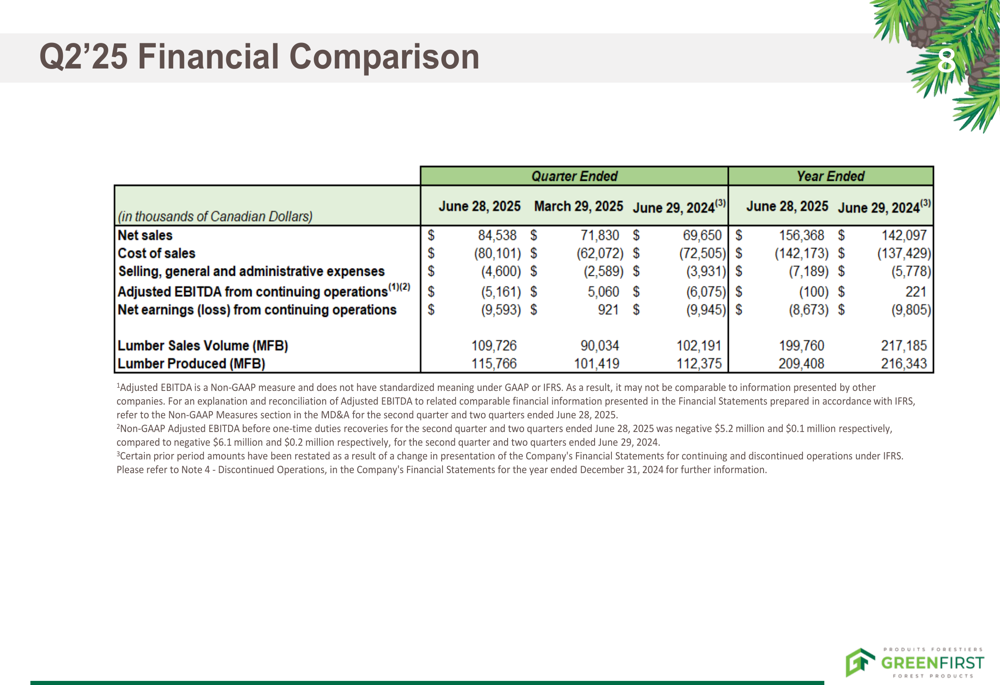

Despite the revenue growth, GreenFirst reported an adjusted EBITDA of negative $5.2 million for Q2 2025, a significant decline from the positive $5.1 million in Q1 2025. This resulted in a net loss from continuing operations of $9.6 million, compared to a profit of $0.9 million in the previous quarter and a loss of $9.9 million in the same quarter last year.

The company’s financial comparison across quarters reveals the extent of these challenges:

Detailed Financial Analysis

The deterioration in profitability can be attributed to several factors, most notably a substantial increase in cost of sales, which rose 29% quarter-over-quarter to $80.1 million. The average realized lumber selling price was $713 per thousand board feet, while the cost of sales (net of by-products revenue) was $672 per thousand board feet.

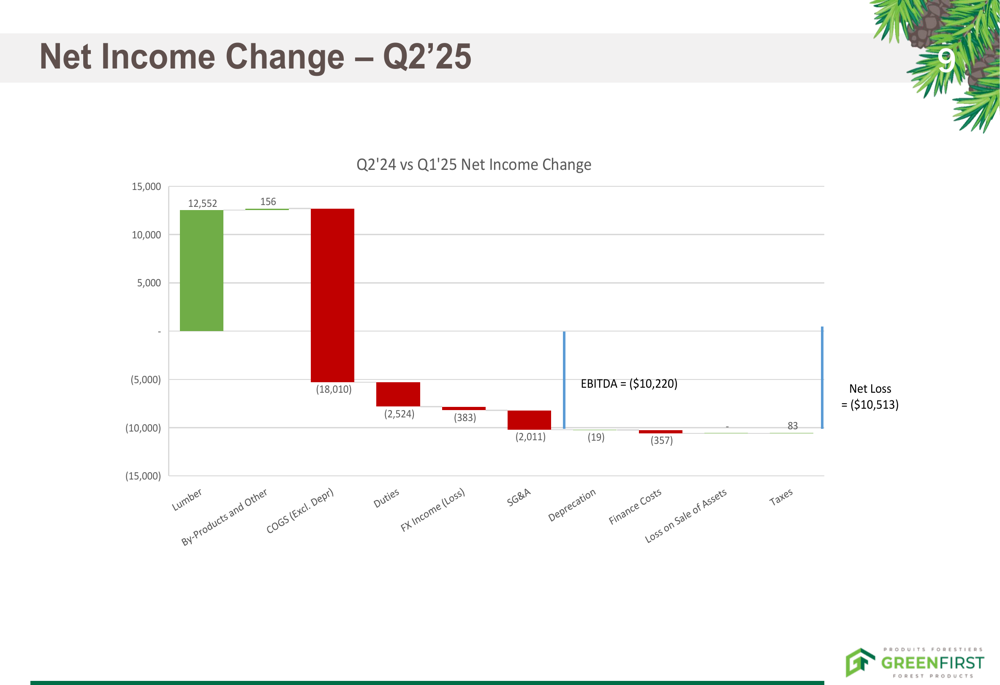

The presentation provided a detailed breakdown of the factors contributing to the net income change between Q1 and Q2 2025:

As illustrated above, while lumber sales contributed positively with a $12.6 million impact, this was more than offset by increased costs of goods sold (excluding depreciation) of $18 million and higher duties of $2.5 million. Selling, general, and administrative expenses also increased by $2 million quarter-over-quarter.

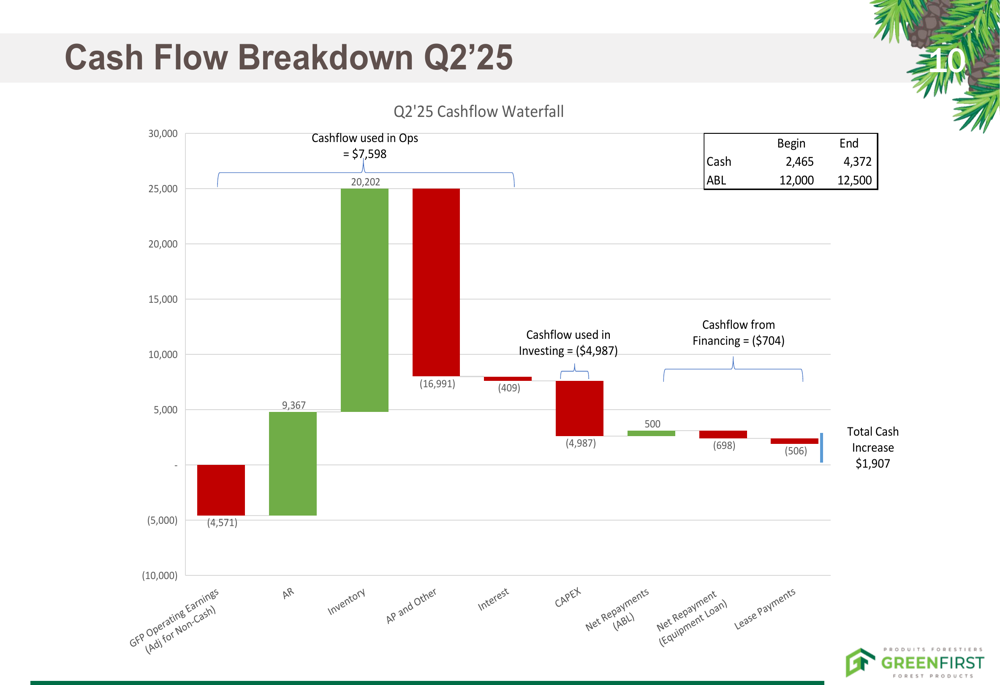

On the cash flow front, GreenFirst ended the quarter with a total cash increase of $1.9 million, despite operational challenges:

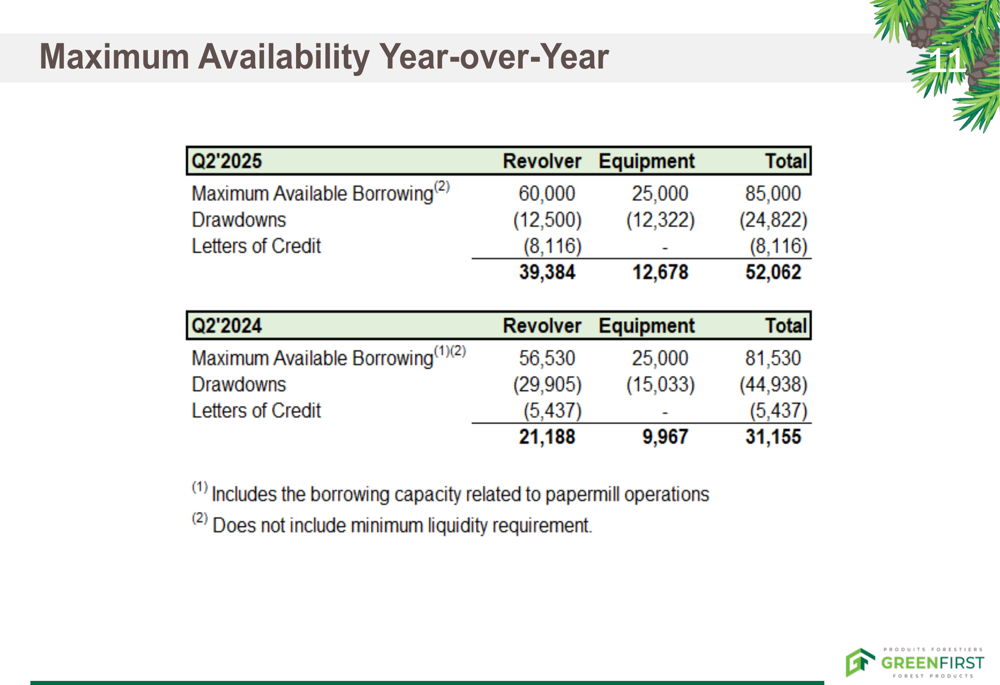

The company maintained a strong liquidity position with $39.8 million of excess liquidity at the end of Q2 2025. The maximum available borrowing improved year-over-year to $52.1 million compared to $31.2 million in Q2 2024:

Strategic Initiatives

GreenFirst outlined several strategic initiatives aimed at improving long-term performance. These include signing an agreement with a third party to explore building a torrefy pellet plant at Chapleau to enhance by-product consumption, and implementing a plan to reduce high inventory levels, particularly work-in-progress, by Q4 2025.

The company is also proceeding with capital investments, including the installation of a new sawline, planer mill, and co-generation plant at its Chapleau mill. According to the presentation, this project is expected to be completed on time and within budget.

The presentation also highlighted the announcement of new financial support from the Federal government amounting to $1.2 billion for the industry, although specific details about GreenFirst’s potential allocation were not provided.

Forward-Looking Statements

Looking ahead, GreenFirst articulated its vision to grow its business in the lumber sector and become one of the largest wood producers in Ontario. The company’s mission focuses on becoming a top quartile lumber producer in North America through continuous improvement, strategic capital investment, and pursuing mergers and acquisitions.

However, the company faces significant challenges, particularly from the increased duty rates on lumber exports to the United States. The presentation acknowledged economic uncertainty but emphasized operational improvements, including lower production manufacturing costs in Q2 2025 compared to both Q1 2025 and year-end 2024.

The disconnect between operational improvements and financial results suggests that external factors, particularly trade policies and market conditions, are currently outweighing internal efficiency gains. Investors will likely be watching closely to see if GreenFirst’s strategic initiatives can overcome these headwinds in the coming quarters, especially as the US housing market potentially strengthens according to the forecasts presented.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.