Trump administration authorizes CIA for covert action in Venezuela - Bloomberg

Introduction & Market Context

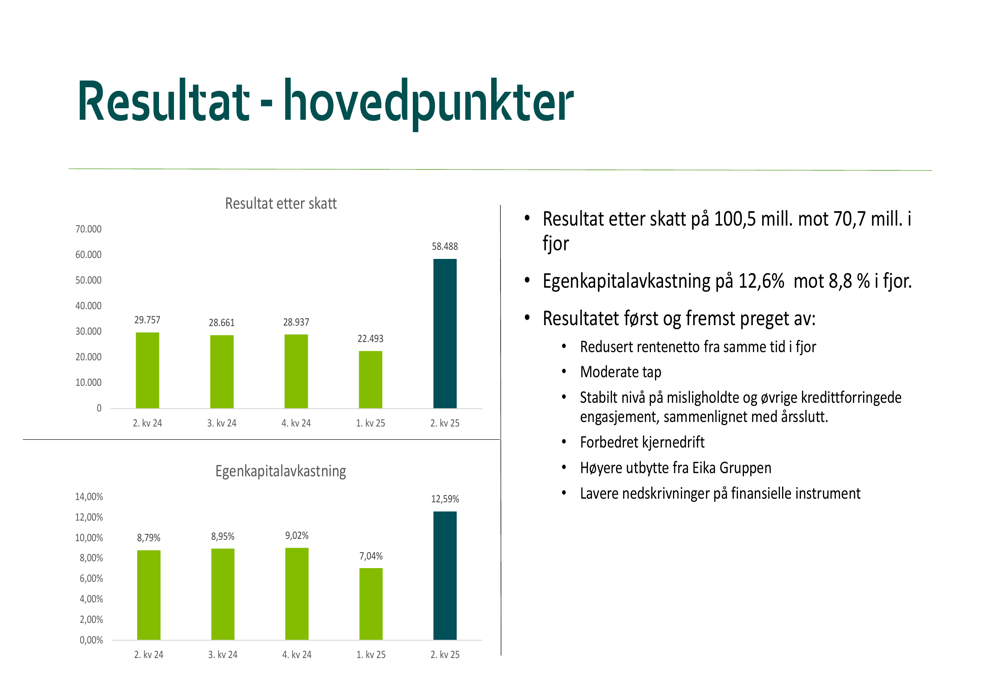

Grong Sparebank (Grong Sparebank) reported a significant improvement in profitability for the first half of 2025, with profit after tax reaching NOK 100.5 million, a 42% increase from NOK 70.7 million in the same period last year. The Norwegian regional bank presented these results on August 13, 2025, highlighting its ability to grow despite challenging market conditions characterized by low overall market growth and intense competition.

The bank’s shares have been trading at NOK 153, within a 52-week range of NOK 140-159, suggesting relatively stable investor sentiment over the past year.

Quarterly Performance Highlights

Grong Sparebank achieved a return on equity of 12.6% in the first half of 2025, significantly higher than the 8.8% reported for the same period in 2024 and well above the bank’s long-term target of at least 9%.

As shown in the following chart of quarterly profit and return on equity trends, the bank experienced a substantial improvement in Q2 2025:

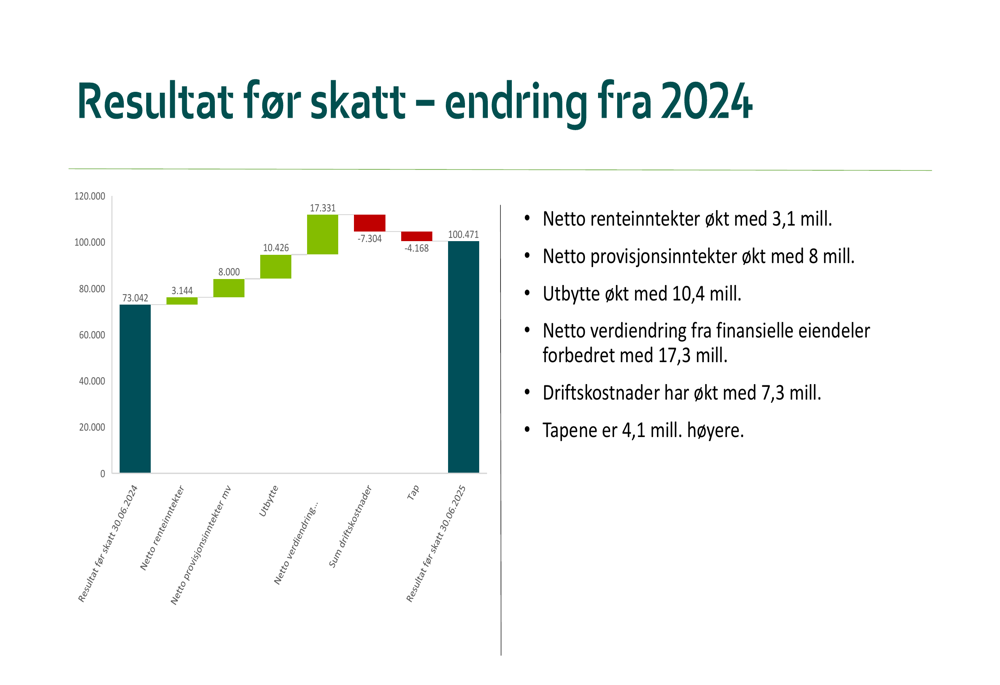

The bank’s profit growth was driven by multiple factors, including improved core operations, higher dividends from Eika Gruppen, and lower write-downs on financial instruments. This waterfall chart illustrates the key contributors to the profit increase:

Detailed Financial Analysis

Net Interest Income and Margins

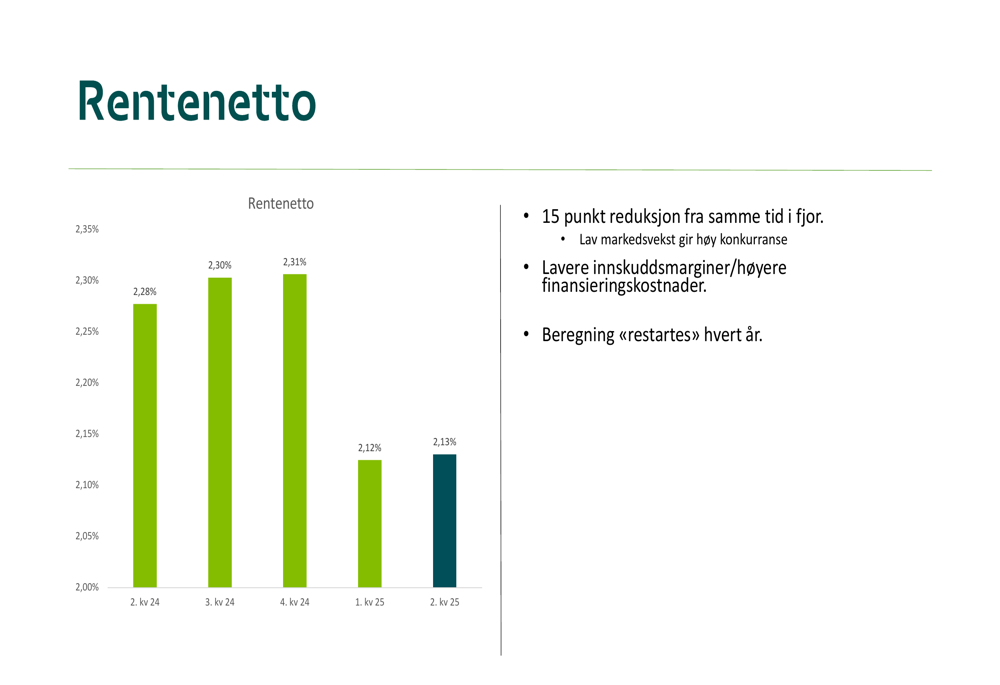

While the bank reported overall growth, its net interest margin declined to 2.12% in Q2 2025 from 2.28% in Q2 2024, representing a 15 basis point reduction. Management attributed this to high competition due to low market growth, along with lower deposit margins and higher financing costs.

Net interest income increased by NOK 3.1 million compared to the first half of 2024, despite margin pressure. The following chart shows the trend in net interest margin over recent quarters:

Commission Income and Fee-Based Revenue

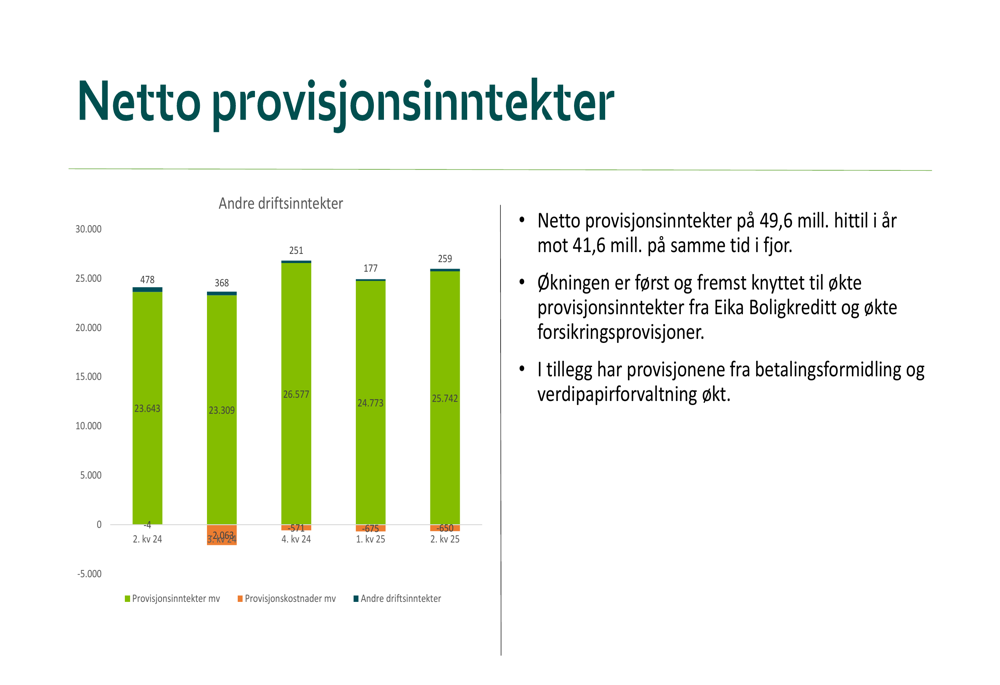

Net commission income showed strong growth, reaching NOK 49.6 million in the first half of 2025 compared to NOK 41.6 million in the same period last year. This increase was primarily driven by higher commission income from Eika Boligkreditt and increased insurance commissions, as well as growth in payment services and securities management fees.

The following chart breaks down the components of commission income across recent quarters:

Asset Quality and Loan Portfolio

Grong Sparebank reported loan growth of NOK 1.3 billion over the last 12 months, representing a 10.6% increase. Total (EPA:TTEF) lending volume, including loans transferred to Eika Boligkreditt, reached NOK 13.7 billion.

However, the bank also reported an increase in non-performing and loss-exposed engagements. Non-performing loans (over 90 days) rose to 0.69% of gross loans, while other loss-exposed engagements increased significantly to 1.17% from 0.14% in the same period last year. Combined, these risk exposures totaled 1.85% of the loan portfolio, a slight increase from 1.70% at year-end 2024.

Loan losses increased to NOK 8.4 million (0.18% of gross loans) from NOK 4.3 million (0.10%) in the same period last year, reflecting the challenging economic environment for some borrowers.

Deposits and Funding

Deposits grew by NOK 668 million over the last 12 months, representing an 8.8% increase, to reach NOK 8.3 billion. The deposit coverage ratio stood at 87.2%, slightly down from 88.6% last year, indicating that loan growth outpaced deposit growth.

Capital Position

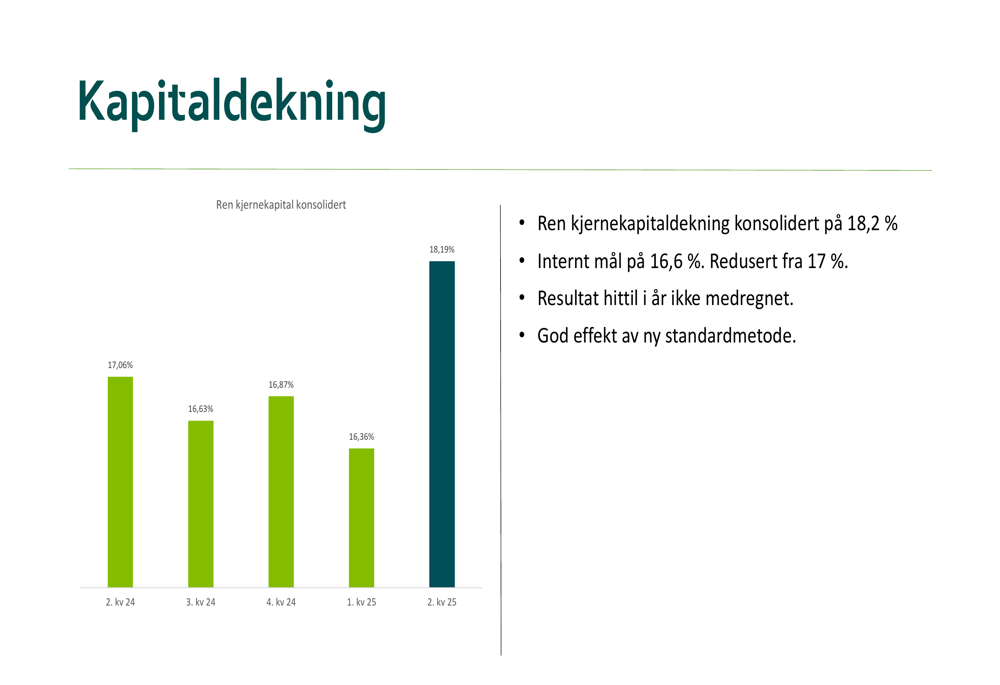

Grong Sparebank maintained a strong capital position with a consolidated core capital ratio of 18.2%, well above its internal target of 16.6% (which was reduced from 17% previously). The bank noted that the implementation of a new standard method had a positive effect on its capital position.

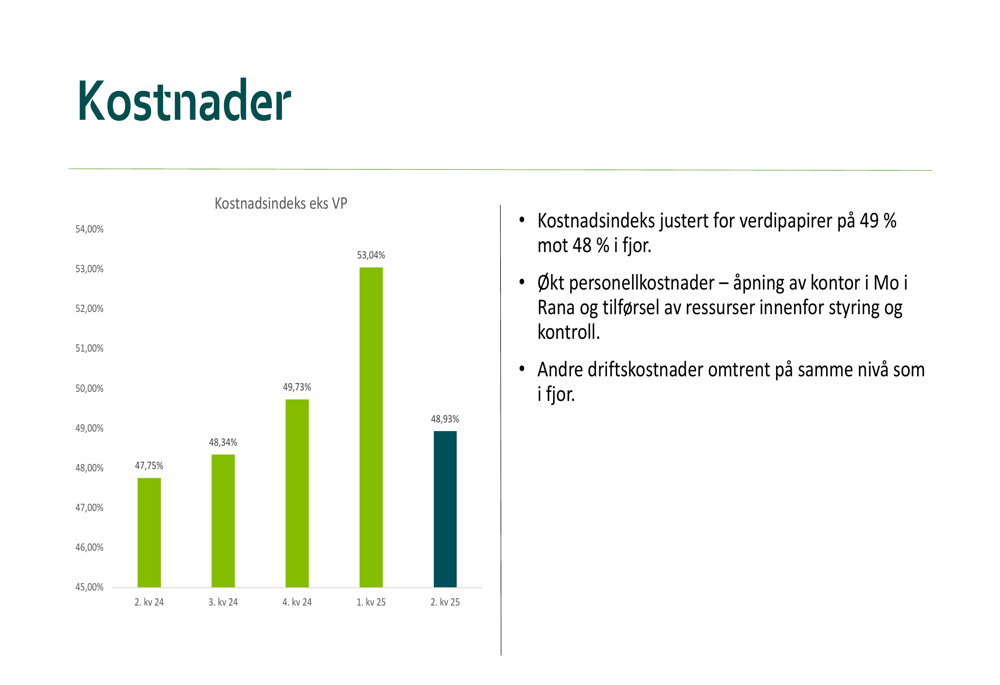

Cost Management

The bank’s cost index excluding securities stood at 48.93% in Q2 2025, slightly higher than the 47.75% reported in Q2 2024. For the first half of 2025, the cost index was 49% compared to 48% in the same period last year. The increase in costs was primarily attributed to higher personnel expenses related to the opening of a new office in Mo i Rana and additional resources allocated to management and control functions.

Strategic Initiatives

Grong Sparebank continues to execute its growth strategy with several key initiatives:

1. The bank opened a new office in Mo i Rana during the reporting period

2. A partnership with Helgeland Boligbyggerlag was established, with plans to present member benefits during Q3 2025

3. A new office in Sandnessjøen is scheduled to open in Q3 2025

These expansion efforts align with the bank’s strategy to grow its presence in the region while maintaining profitability and solid capital ratios.

Forward-Looking Statements

Looking ahead, Grong Sparebank expects an interest rate cut in the third quarter of 2025, which could impact margins but potentially stimulate loan demand. The bank emphasized that its improved capital situation following the introduction of the new standard method provides a foundation for continuing its existing growth strategy and competing in more areas.

Management expressed confidence in the bank’s ability to maintain its growth trajectory while managing the slight increase in non-performing loans. The strategic partnerships and new office openings are expected to contribute to continued customer acquisition and business volume growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.