TSX lower as gold rally takes a breather

Introduction & Market Context

GSK plc (NYSE:GSK) presented its Q2 2025 financial results on July 30, 2025, showcasing continued momentum with 6% sales growth and 15% earnings per share growth at constant exchange rates (CER). The company’s performance was primarily driven by its Specialty Medicines segment, which now represents 40% of total sales. The results build on the strong trajectory seen in previous quarters, with GSK maintaining its position as a leader in key therapeutic areas including respiratory, HIV, and oncology.

Quarterly Performance Highlights

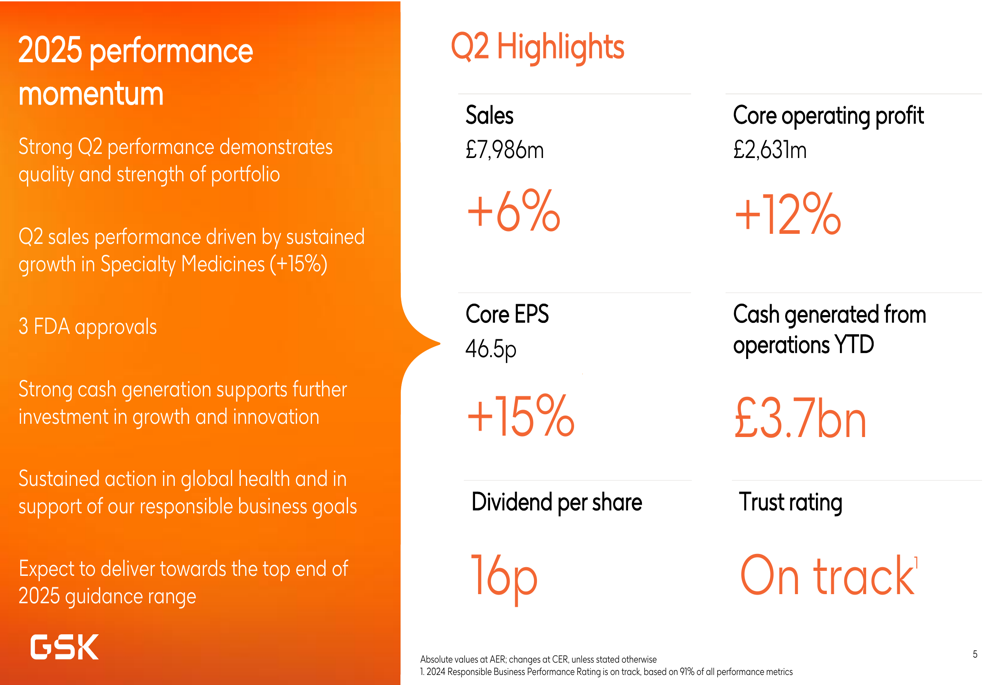

GSK reported Q2 2025 sales of £7,986 million, representing a 6% increase at CER compared to the same period last year. Core operating profit reached £2,631 million, up 12% at CER, while core earnings per share jumped 15% to 46.5p. The company also reported £3.7 billion in cash generated from operations year-to-date and declared a dividend of 16p per share.

As shown in the following quarterly highlights slide, GSK delivered strong performance across key financial metrics:

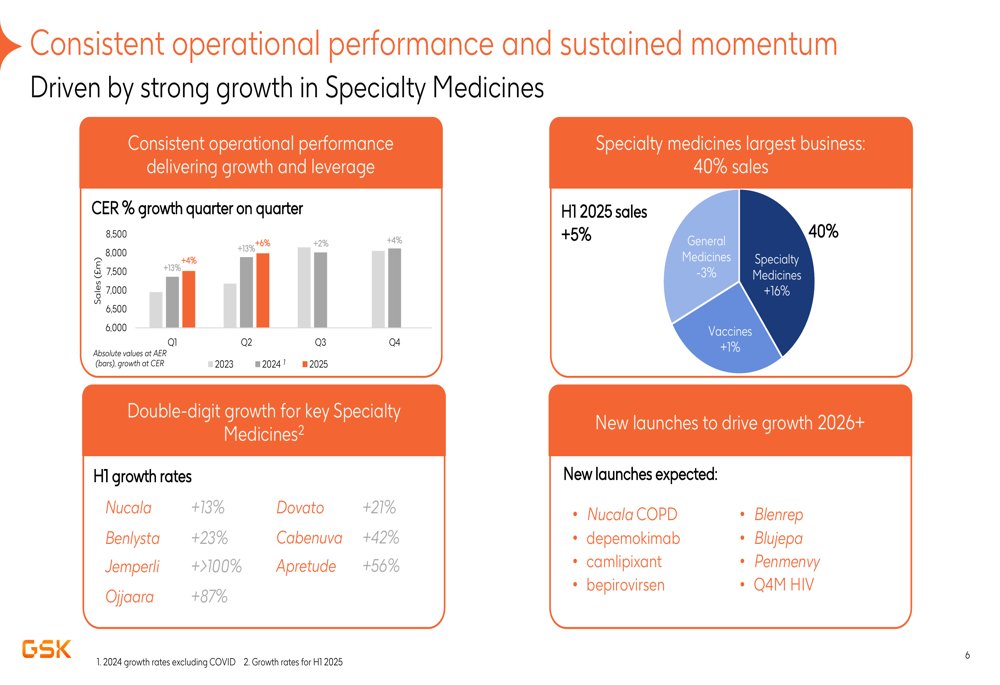

The company’s consistent operational performance is evident in the quarterly growth trends, with Specialty Medicines emerging as the largest business segment at 40% of total sales. Several key specialty medicines showed double-digit growth, including Nucala (+13%), Benlysta (+23%), and HIV treatments Dovato (+21%), Cabenuva (+42%), and Apretude (+56%).

Specialty Medicines Leading Growth

Specialty Medicines has become the growth engine for GSK, with sales increasing by 13% in Q2 2025. This segment now accounts for 40% of total sales, with particularly strong performance in HIV treatments, which grew 12% to £1,880 million. The following slide illustrates the momentum in Specialty Medicines:

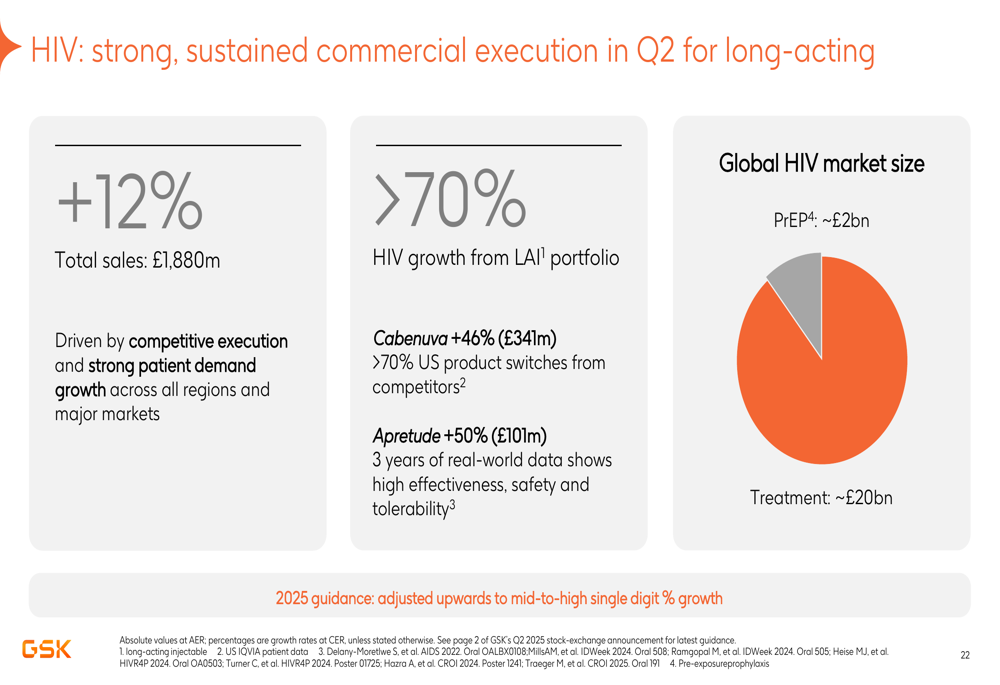

HIV treatments showed exceptional growth, driven by long-acting injectables (LAIs) which contributed more than 70% of HIV growth. Cabenuva sales increased 46% to £341 million, while Apretude grew 50% to £101 million. Based on this strong performance, GSK has adjusted its 2025 guidance for HIV upward to mid-to-high single-digit percentage growth.

The company’s HIV commercial execution has been particularly impressive, as shown in the following slide:

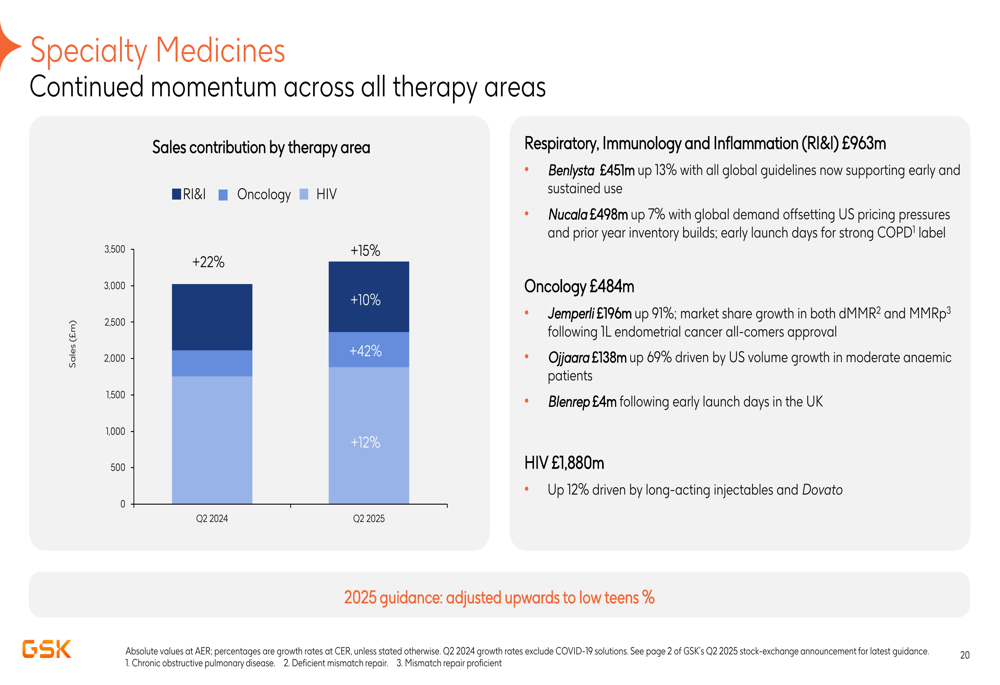

In oncology, Jemperli sales surged 91% to £196 million, while Ojjaara grew 69% to £138 million. GSK’s respiratory portfolio also showed strength, with Nucala receiving approval for COPD in May 2025, representing its fifth indication in the US.

Pipeline Progress and R&D Investment

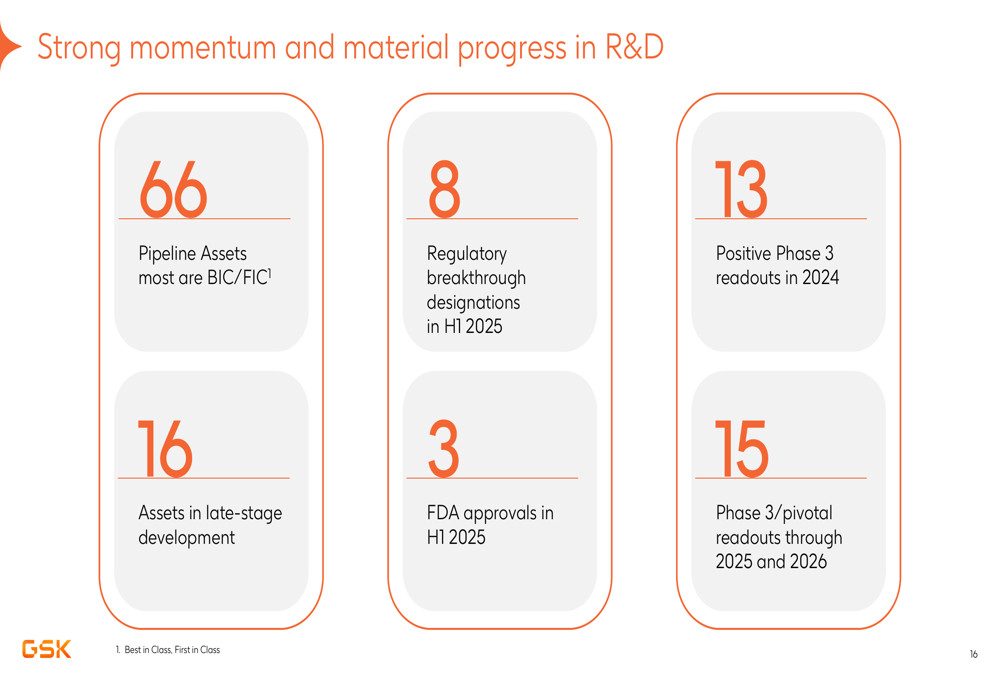

GSK continues to invest heavily in its pipeline, with R&D expenses increasing 11% in Q2 2025. The company highlighted 66 pipeline assets, with most being best-in-class or first-in-class. In the first half of 2025, GSK secured 8 regulatory breakthrough designations and 3 FDA approvals, with 15 Phase 3 or pivotal readouts expected through 2025 and 2026.

The following slide illustrates GSK’s momentum and progress in R&D:

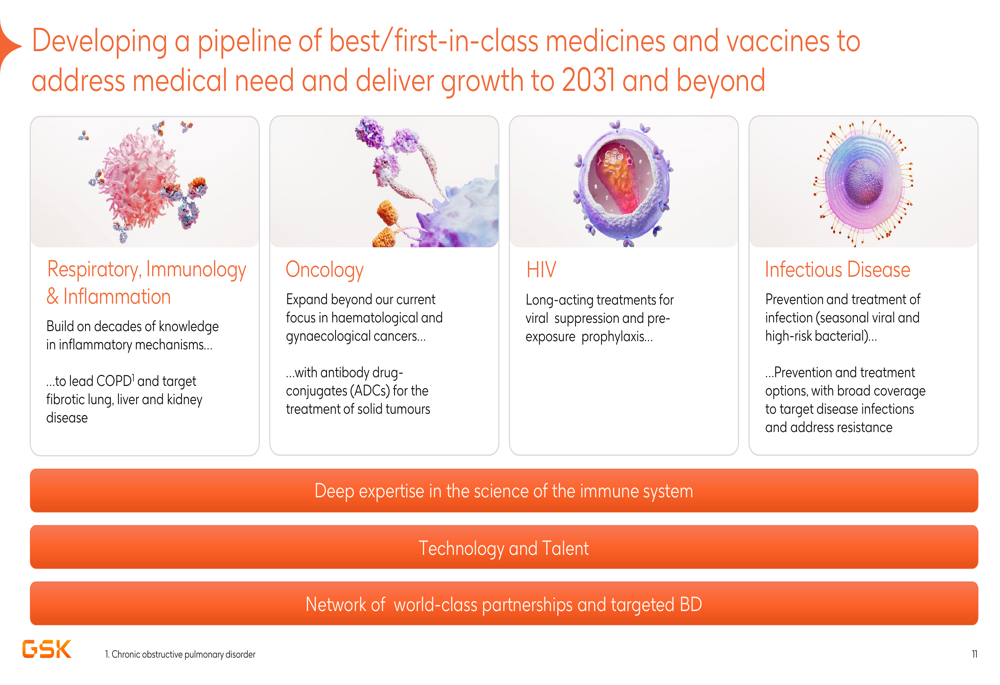

The company is developing a pipeline of innovative medicines across key therapeutic areas, focusing on respiratory, immunology and inflammation, oncology, HIV, and infectious diseases. This strategic approach is designed to address significant unmet medical needs:

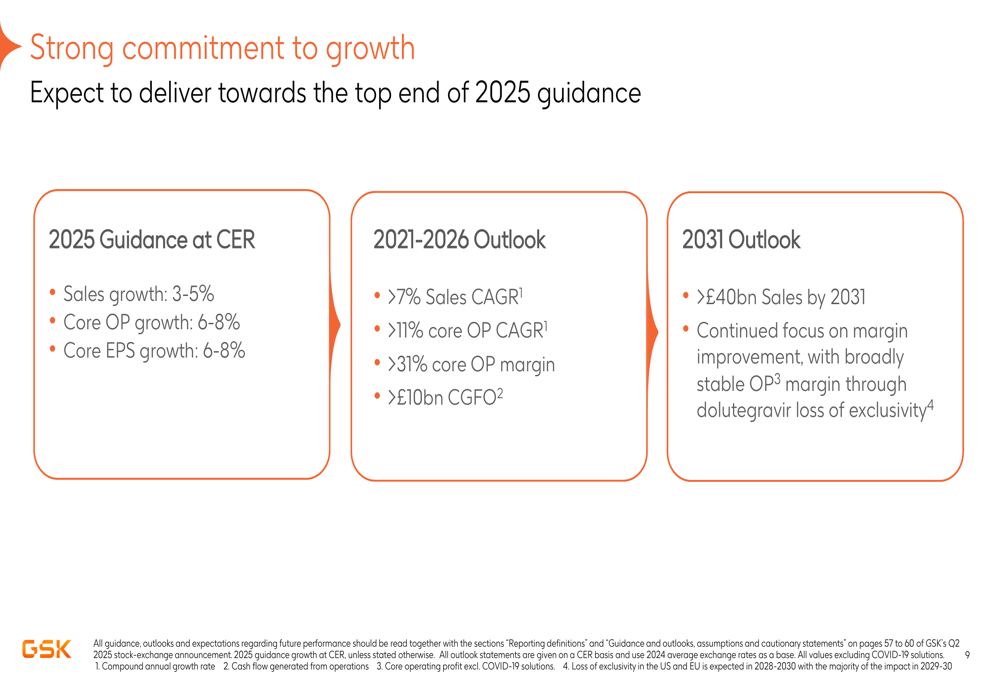

GSK expressed confidence in its long-term growth outlook, projecting sales of more than £40 billion by 2031. The company noted that approximately 90% of these projected sales would come from products that are already approved or planned for launch in the next three years.

Financial Analysis and Margin Improvement

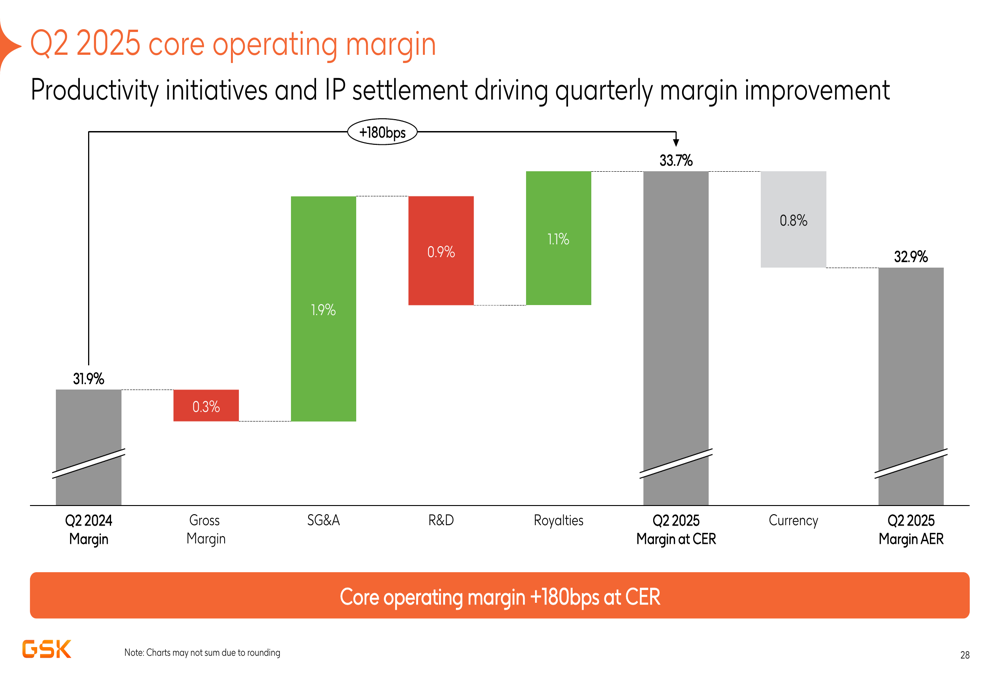

GSK’s core operating margin improved by 180 basis points at CER to 32.9% in Q2 2025. This improvement was driven by several factors, including SG&A efficiency, royalty income, and R&D investment, as illustrated in the following slide:

The company’s SG&A expenses decreased by 1% at CER, driven by phasing and acceleration of productivity initiatives. Meanwhile, royalty income benefited from an RSV IP settlement upfront payment. These factors, combined with strong sales growth, contributed to the 12% increase in core operating profit.

Forward-Looking Guidance

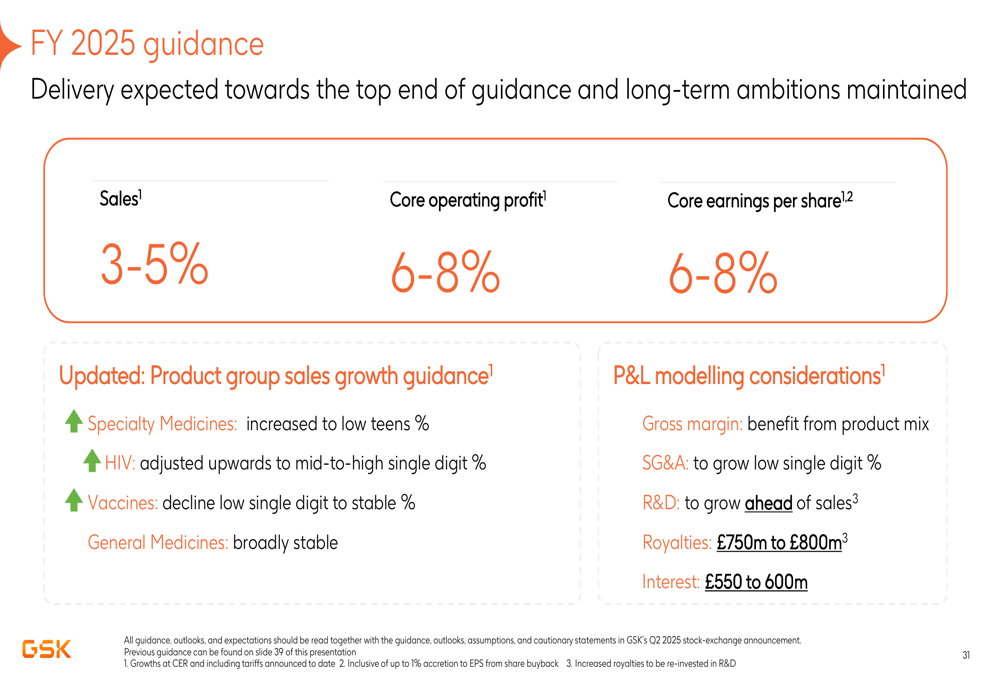

Based on the strong performance in Q2 2025, GSK confirmed its full-year guidance for 2025, projecting sales growth of 3-5%, core operating profit growth of 6-8%, and core EPS growth of 6-8% at CER. The company also provided updated guidance for specific product groups, raising the outlook for Specialty Medicines to low teens percentage growth and adjusting HIV growth to mid-to-high single-digit percentage.

Looking beyond 2025, GSK reaffirmed its 2021-2026 outlook of more than 7% sales CAGR and more than 11% core operating profit CAGR. The company also maintained its confidence in achieving sales of more than £40 billion by 2031, with continued focus on margin improvement.

Strategic Initiatives

GSK highlighted its capital allocation priorities, focusing on investing behind launch assets, prioritizing respiratory, immunology, inflammation, and oncology, pursuing targeted business development, and optimizing the supply chain. The company identified 14 scale opportunities with peak year sales potential exceeding £2 billion each.

In conclusion, GSK’s Q2 2025 results demonstrate continued momentum across its key business segments, particularly in Specialty Medicines. With strong financial performance, pipeline progress, and raised guidance for key segments, the company appears well-positioned to deliver on its long-term growth objectives. The focus on high-growth therapeutic areas and continued R&D investment supports GSK’s confidence in achieving its 2031 sales target of more than £40 billion.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.