Oklo stock tumbles as Financial Times scrutinizes valuation

Introduction & Market Context

Gujarat Pipavav Port Ltd (BSE:GPPL) presented its Q1 2025-26 results on August 13, 2025, revealing modest revenue growth amid mixed performance across cargo segments. The port operator, part of the APM Terminals network, reported a 2% year-over-year increase in revenue despite facing headwinds in its container business.

The company’s stock has been under pressure recently, trading at INR 156.22, down 3.87% following the results presentation. The current share price sits significantly below its 52-week high of INR 236.9, reflecting investor concerns about the company’s profitability trajectory.

Quarterly Performance Highlights

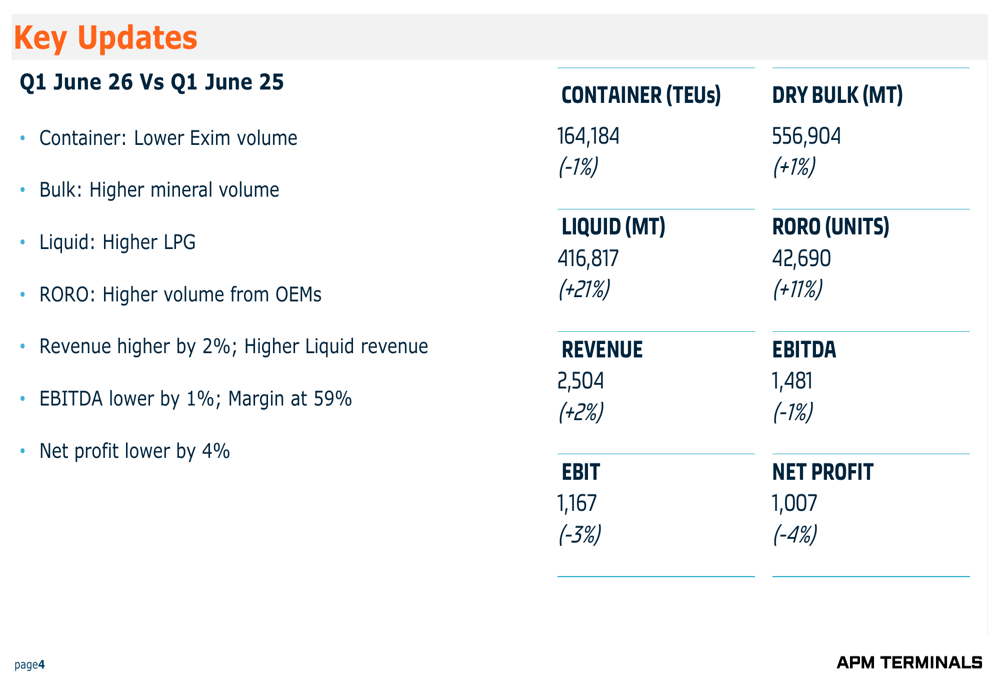

Gujarat Pipavav Port delivered mixed volume performance across its cargo segments in Q1 2025-26. While container volumes declined slightly by 1% year-over-year to 164,184 TEUs, the company saw robust growth in liquid cargo and RORO (Roll-on/Roll-off) segments, which increased by 21% and 11% respectively.

The company’s revenue grew by 2% to INR 2,504 million compared to the same quarter last year, despite the slight decline in container volumes. However, this top-line growth did not translate to improved profitability, with EBITDA declining by 1% to INR 1,481 million and net profit falling by 4% to INR 1,007 million.

As shown in the following summary of key performance metrics comparing Q1 June 2026 with Q1 June 2025:

The port’s diversified cargo handling capabilities appear to be providing some resilience, with growth in liquid cargo volumes standing out as a particular bright spot. The 21% increase in liquid volumes to 416,817 metric tons represents a significant opportunity for the company as it seeks to offset weakness in its container business.

Detailed Financial Analysis

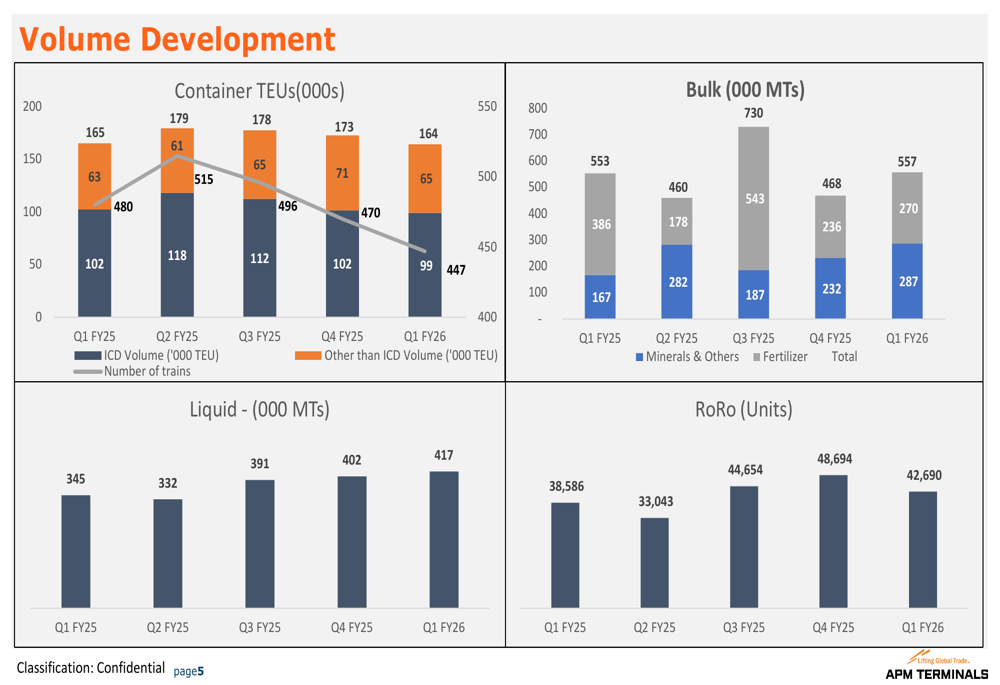

The quarterly volume development charts reveal important trends across Gujarat Pipavav’s business segments. Container volumes have remained relatively stable over the past five quarters, while bulk cargo shows some volatility. The most notable growth trend appears in the liquid cargo segment, which has shown consistent improvement.

As illustrated in these detailed volume development charts across all cargo segments:

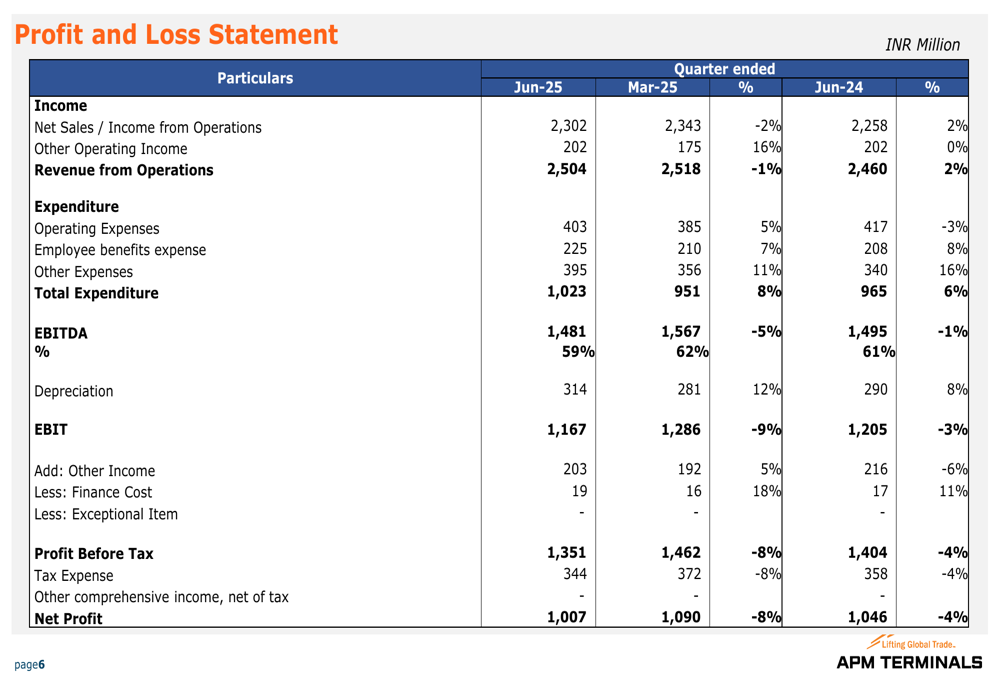

The company’s profit and loss statement reveals that while revenue increased slightly year-over-year, total expenditure rose more significantly from INR 965 million in June 2024 to INR 1,023 million in June 2025, representing a 6% increase. This expense growth outpaced revenue growth, putting pressure on margins and profitability.

The EBITDA margin remained healthy at 59%, but showed a slight decline from the previous year. The sequential comparison with the March 2025 quarter also indicates a downward trend in profitability, with net profit declining from INR 1,090 million to INR 1,007 million.

The complete profit and loss statement provides further details on the financial performance:

Forward-Looking Statements

While the presentation did not include explicit forward guidance, the company’s standard disclaimer acknowledged that actual results could differ materially from any forward-looking statements due to various factors including economic conditions, demand/supply dynamics, price conditions, and regulatory changes.

The mixed performance across cargo segments suggests that Gujarat Pipavav Port is navigating a challenging operating environment. The strong growth in liquid cargo and RORO segments demonstrates the value of the company’s diversified operations, but the pressure on profitability indicates that cost management will be crucial going forward.

Investors will likely focus on whether the company can maintain its revenue growth while addressing the rising expenditure that has impacted bottom-line performance. The stock’s current trading level, well below its 52-week high, suggests that the market remains cautious about the company’s near-term prospects despite the modest top-line growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.