Infosys, Wipro decline despite upbeat Q2 earnings; margin concerns weigh

Hayward Holdings Inc (NYSE:HAYW) reported second quarter 2025 earnings on July 30, showcasing solid financial performance with record gross margins despite tariff challenges. The pool equipment manufacturer’s stock rose 2.81% in premarket trading following the announcement, indicating positive investor reception.

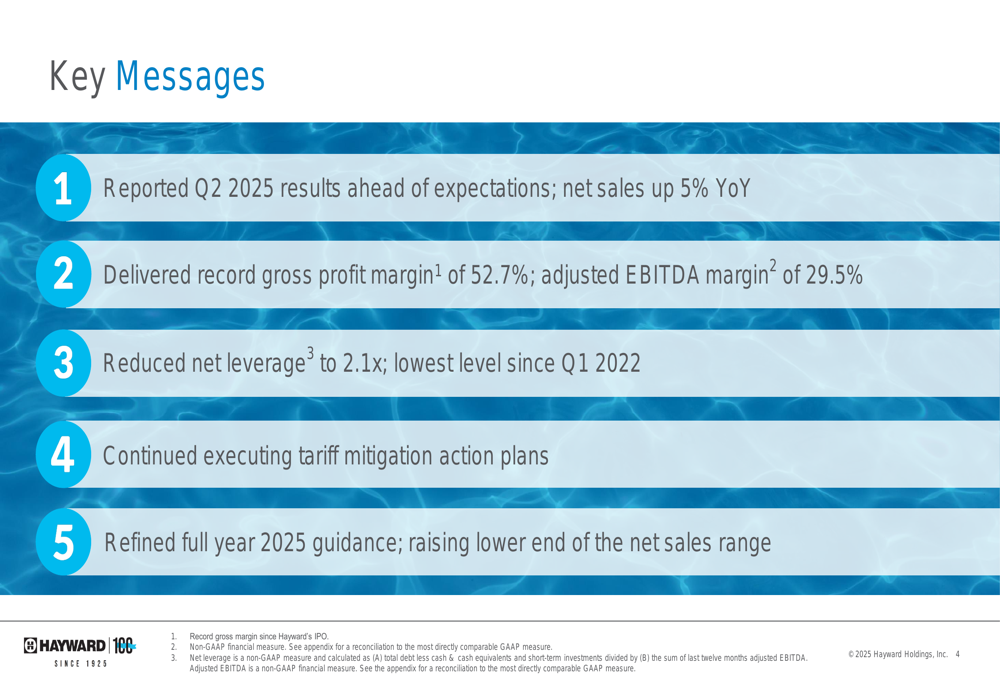

Executive Summary

Hayward delivered second quarter results that exceeded expectations, with net sales increasing 5% year-over-year to $299.6 million. The company achieved a record gross profit margin of 52.7% since its IPO, representing a 170 basis point improvement from the prior year. Adjusted EBITDA grew 7% to $88.2 million, with margins expanding to 29.5%.

As shown in the following key messages from the company’s presentation:

"We’re pleased with our second quarter performance, which demonstrates the resilience of our business model and our ability to execute effectively in a challenging environment," said Kevin Holleran, President and CEO of Hayward, according to the presentation materials.

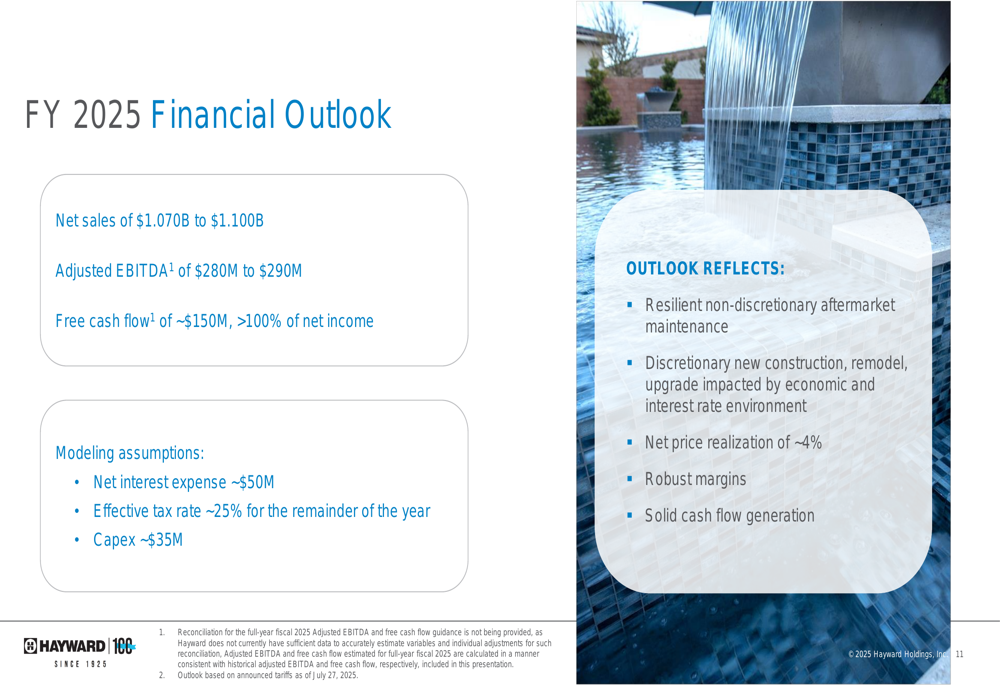

The company has refined its full-year 2025 guidance, raising the lower end of its net sales range to $1.070-$1.100 billion, while maintaining its adjusted EBITDA guidance of $280-$290 million.

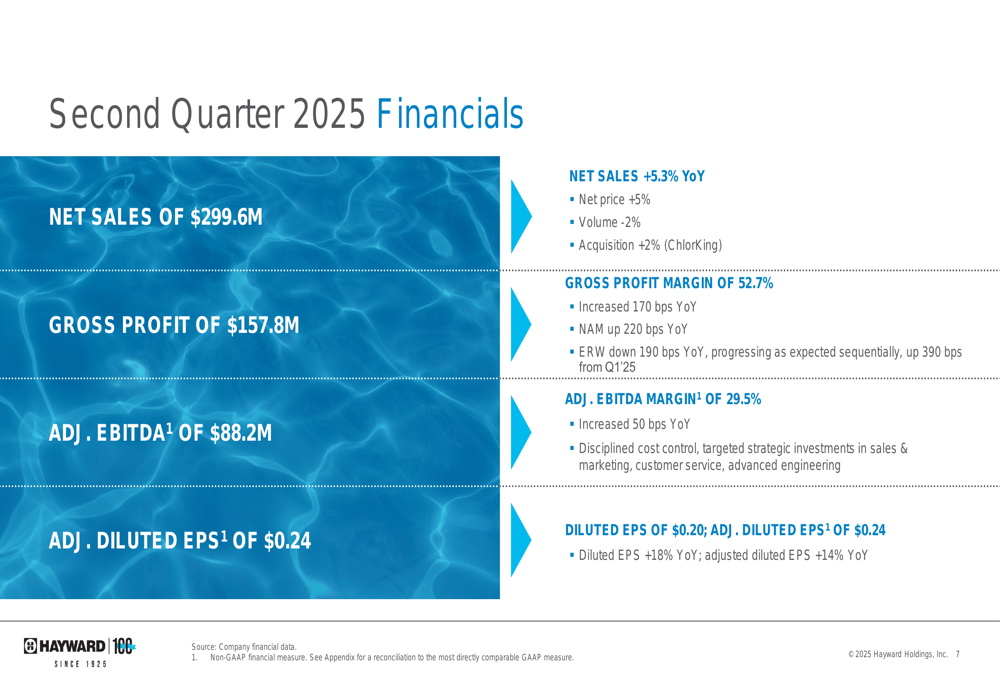

Quarterly Performance Highlights

Hayward’s second quarter showed meaningful improvement from its first quarter performance, when the company reported revenue of $229 million and EPS of $0.10. The Q2 results reflect both seasonal strength and continued execution of the company’s strategic initiatives.

The detailed financial breakdown reveals strong performance across key metrics:

The North America segment, which represents approximately 85% of total sales, grew 5.8% year-over-year to $255.2 million, with gross profit margin expanding 220 basis points to 55.1%. This growth was driven by a 6% increase in net price, partially offset by a 3% volume decline, with acquisition activity contributing 3% to growth.

Europe and Rest of World segment revenue increased 2.7% to $44.4 million. While gross margin in this segment declined 190 basis points year-over-year to 38.9%, it improved significantly from the first quarter, showing a 390 basis point sequential increase.

The following financial overview summarizes the company’s quarterly performance:

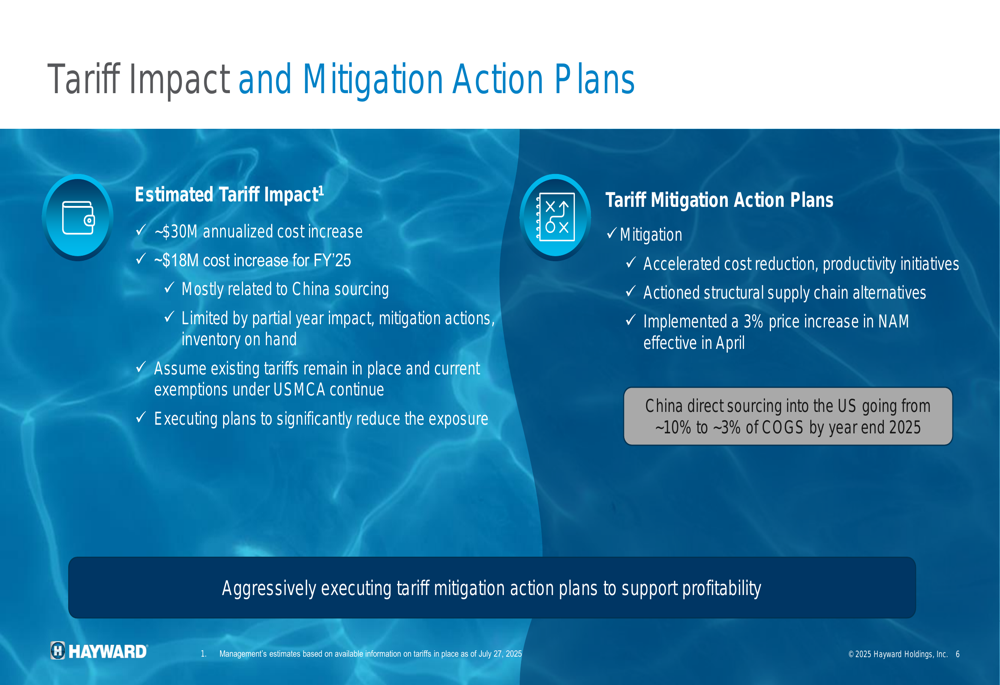

Tariff Impact and Mitigation Strategies

A significant focus of the presentation was Hayward’s response to tariff challenges. The company estimates an annualized cost increase of approximately $30 million due to tariffs, with about $18 million impacting fiscal year 2025. The majority of this impact relates to Chinese sourcing.

Hayward has implemented a comprehensive mitigation strategy that includes:

- A 3% price increase in North America effective April 2025

- Accelerated cost reduction and productivity initiatives

- Structural supply chain alternatives to reduce dependency on Chinese imports

As illustrated in the company’s tariff mitigation plan:

"We’re making significant progress in reducing our exposure to Chinese direct sourcing into the US, which we expect to decrease from approximately 10% to 3% of cost of goods sold by year-end 2025," noted Eifion Jones, Senior Vice President and CFO, according to presentation materials.

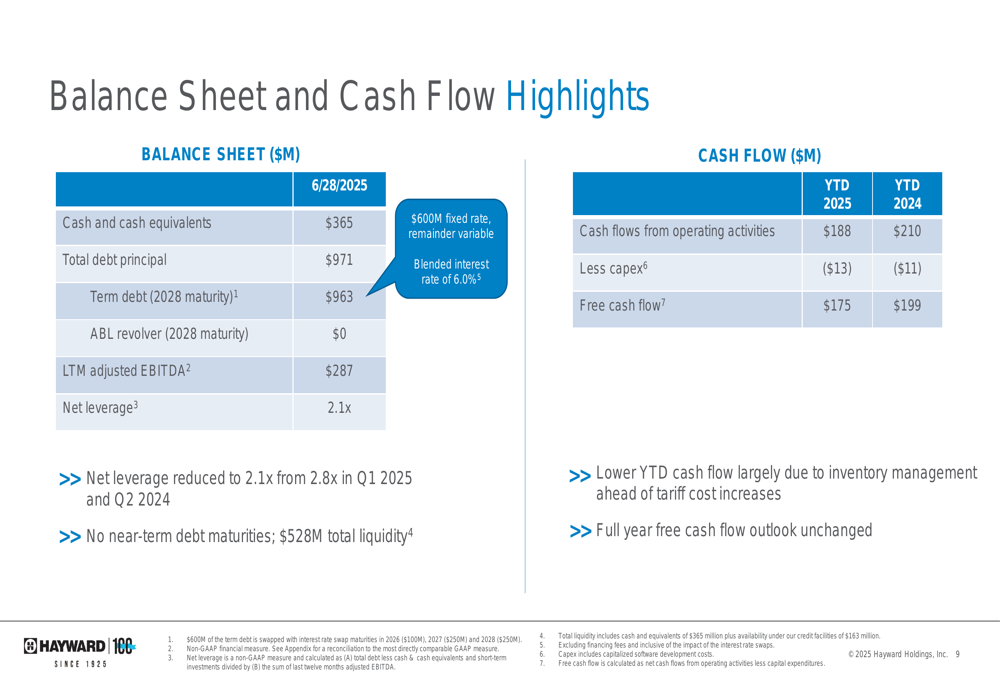

Balance Sheet Strength and Capital Allocation

Hayward has strengthened its financial position, reducing net leverage to 2.1x from 2.8x in both Q1 2025 and Q2 2024. This represents the lowest leverage level since Q1 2022, providing increased financial flexibility.

The company reported $365 million in cash and cash equivalents, with total debt principal of $971 million. Year-to-date free cash flow was $175 million, compared to $199 million in the same period last year, with the difference primarily attributed to inventory management ahead of tariff cost increases.

The balance sheet highlights demonstrate Hayward’s improved financial position:

Hayward’s capital allocation priorities remain focused on growth investments, strategic M&A, debt reduction, and shareholder returns, with a $450 million share repurchase authorization in place.

Forward-Looking Guidance

Looking ahead, Hayward refined its full-year 2025 financial outlook:

The guidance reflects the company’s confidence in its resilient aftermarket business model, with approximately 85% of sales coming from the existing installed base. Management expects net price realization of approximately 4% for the full year, helping to offset tariff impacts.

The outlook acknowledges that discretionary segments related to new construction, remodeling, and upgrades continue to be impacted by the economic and interest rate environment, while non-discretionary maintenance remains resilient.

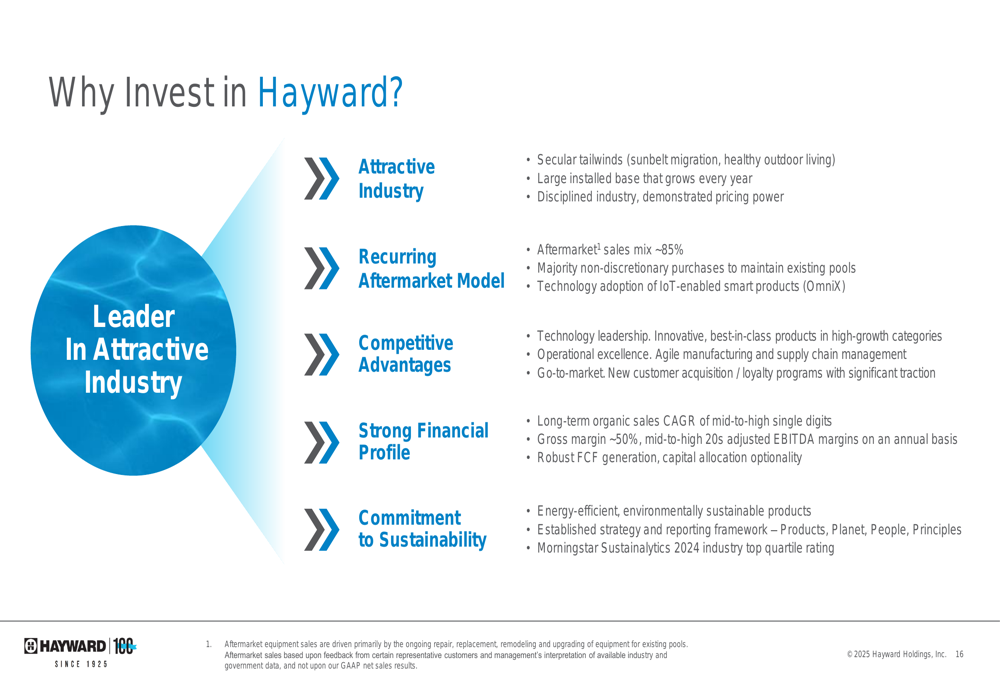

Competitive Industry Position

Hayward positions itself as a global leader in pool and outdoor living technology with a strong brand presence. The company has built its competitive advantage on technology leadership, operational excellence, and a multi-channel go-to-market strategy.

The company’s investment thesis highlights its attractive industry dynamics, recurring aftermarket revenue model, and strong financial profile:

With approximately 90% of products associated with sustainability themes and over 550 current or pending patents globally, Hayward continues to emphasize innovation as a key differentiator in the market.

The company’s presentation noted that it is celebrating its 100th anniversary in 2025, having evolved from its founding by Irving Hayward in 1925 to its current position as a public company following its 2021 IPO.

In conclusion, Hayward’s Q2 2025 presentation demonstrates solid execution in a challenging environment, with record gross margins and effective tariff mitigation strategies positioning the company for continued growth. The reduction in leverage and refined guidance suggest management confidence in the company’s strategic direction and financial outlook for the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.