Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

Hayward Holdings, Inc. (NYSE:HAYW), a global leader in pool equipment manufacturing, presented its second quarter 2025 earnings results on July 30, 2025, highlighting better-than-expected performance despite ongoing tariff challenges. The company, celebrating its 100th anniversary this year, demonstrated resilience in a market affected by economic uncertainty and supply chain disruptions.

The pool equipment manufacturer reported solid growth figures, though investor reaction was mixed, with the stock rising 2.76% during regular trading to $15.02 but falling 1.6% in aftermarket trading to $14.78, according to available market data.

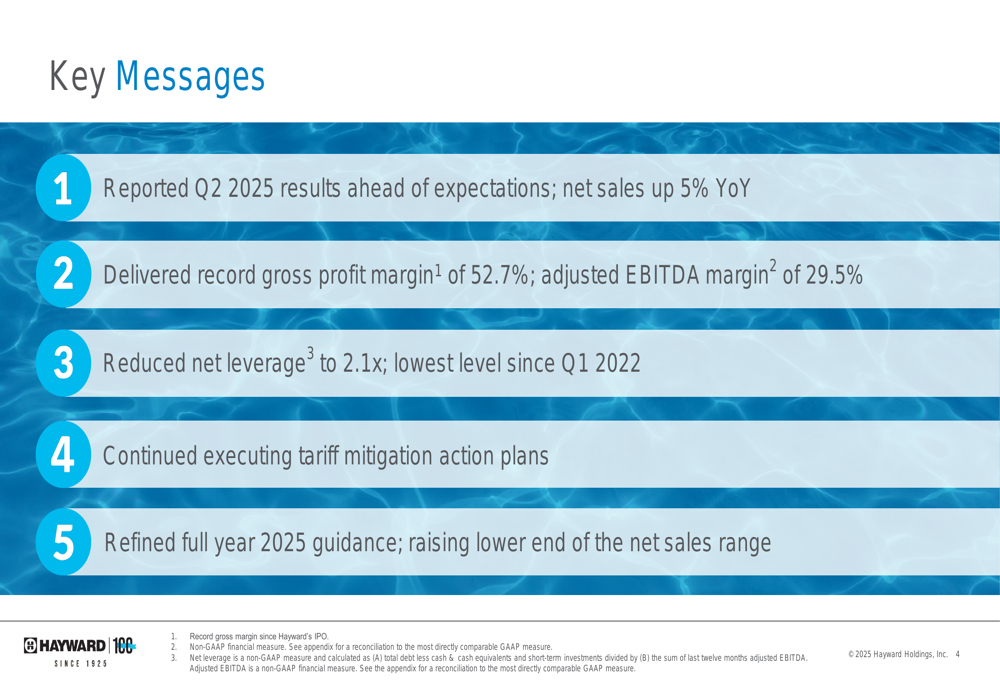

As shown in the following key messages from the presentation, Hayward exceeded expectations across multiple metrics:

Quarterly Performance Highlights

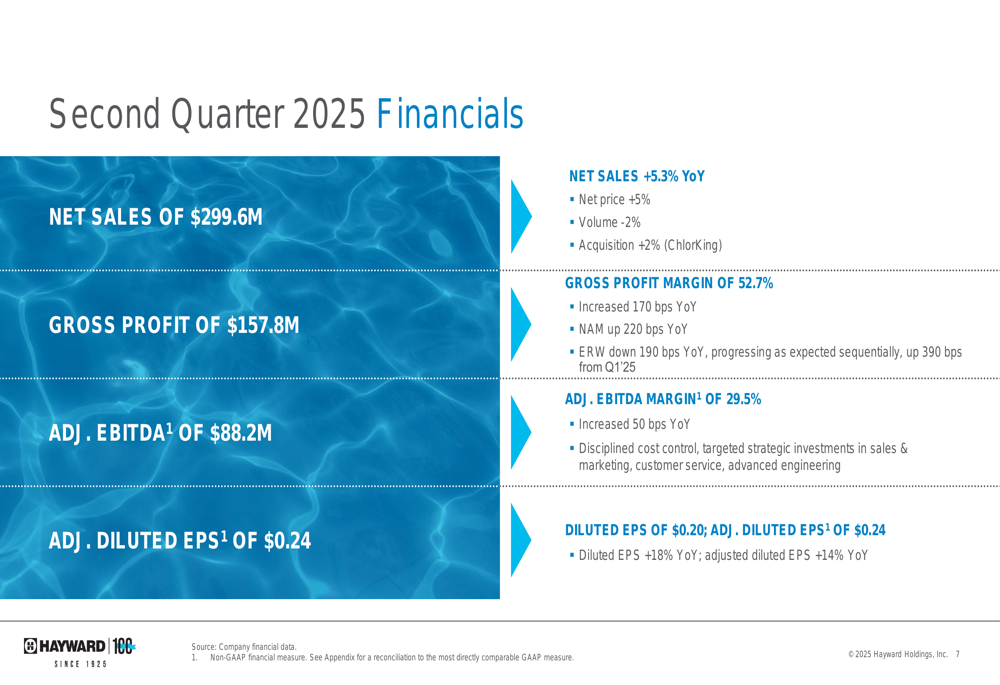

Hayward reported net sales of $299.6 million for Q2 2025, representing a 5.3% increase compared to the same period last year. This growth was primarily driven by a 5% contribution from net price increases and a 2% boost from the ChlorKing acquisition, partially offset by a 2% volume decline.

The company achieved a record gross profit margin of 52.7%, an improvement of 170 basis points year-over-year. Adjusted EBITDA grew to $88.2 million, up 7% from the previous year, with adjusted EBITDA margin expanding by 50 basis points to 29.5%. Adjusted diluted earnings per share increased by 14% to $0.24.

The detailed financial overview demonstrates the company’s solid execution and margin expansion:

A deeper analysis of the quarter’s financial performance reveals strong pricing power and strategic growth investments:

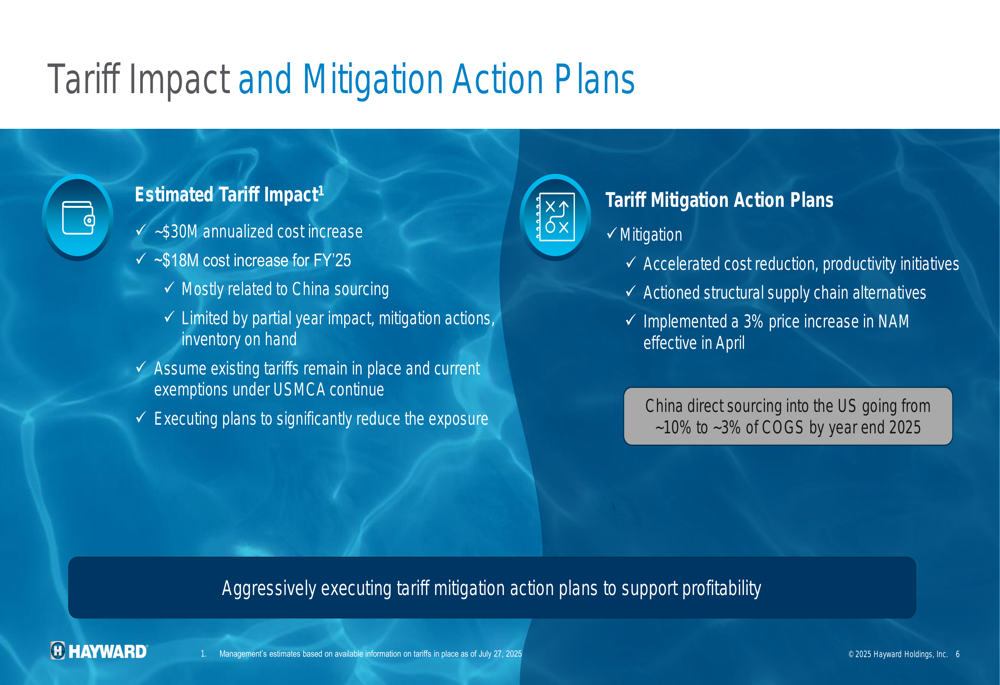

Tariff Impact and Mitigation Strategy

A significant challenge facing Hayward is the impact of tariffs, particularly on goods sourced from China. The company estimates an annualized cost increase of approximately $30 million, with about $18 million affecting fiscal year 2025. In response, Hayward has implemented a comprehensive mitigation strategy, including a 3% price increase in North America effective April 2025 and plans to dramatically reduce direct sourcing from China.

As illustrated in the following slide, the company is taking decisive action to restructure its supply chain:

This proactive approach aims to reduce China direct sourcing into the US from approximately 10% to just 3% of cost of goods sold by year-end 2025, significantly minimizing the company’s exposure to potential future tariff increases.

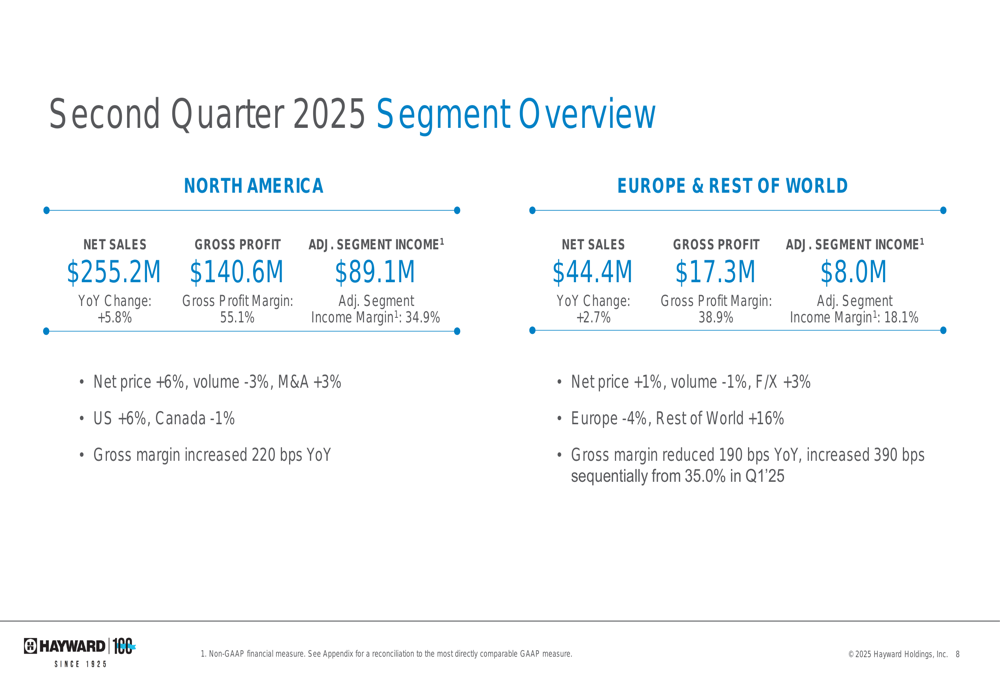

Segment Performance Analysis

Hayward’s business performance varied by geographic segment. North America, which represents about 85% of total sales, delivered net sales of $255.2 million, up 5.8% year-over-year. The segment achieved a gross profit margin of 55.1%, an increase of 220 basis points, and adjusted segment income margin of 34.9%.

In contrast, the Europe & Rest of World segment reported more modest growth of 2.7%, reaching $44.4 million in net sales. While Europe itself saw a 4% decline, the Rest of World markets grew by an impressive 16%. The segment’s gross margin decreased by 190 basis points year-over-year to 38.9%, though it improved sequentially by 390 basis points from Q1 2025.

The segment breakdown provides insight into regional performance dynamics:

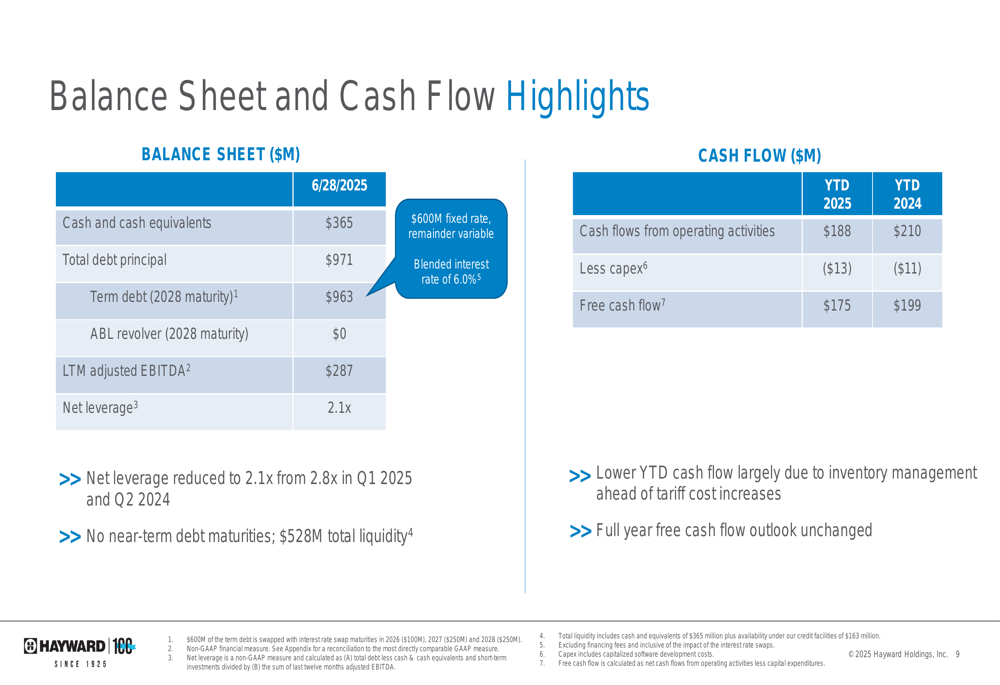

Balance Sheet Strength and Capital Allocation

Hayward has significantly strengthened its financial position, reducing net leverage to 2.1x, its lowest level since Q1 2022. As of Q2 2025, the company reported $365 million in cash and cash equivalents against total debt principal of $971 million.

Year-to-date free cash flow reached $175 million, slightly lower than the $199 million generated in the same period of 2024, primarily due to inventory management decisions ahead of tariff cost increases. However, the company maintained its full-year free cash flow outlook of approximately $150 million.

The following slide details Hayward’s balance sheet and cash flow highlights:

Regarding capital allocation, Hayward has established clear priorities focused on balancing growth investments with shareholder returns:

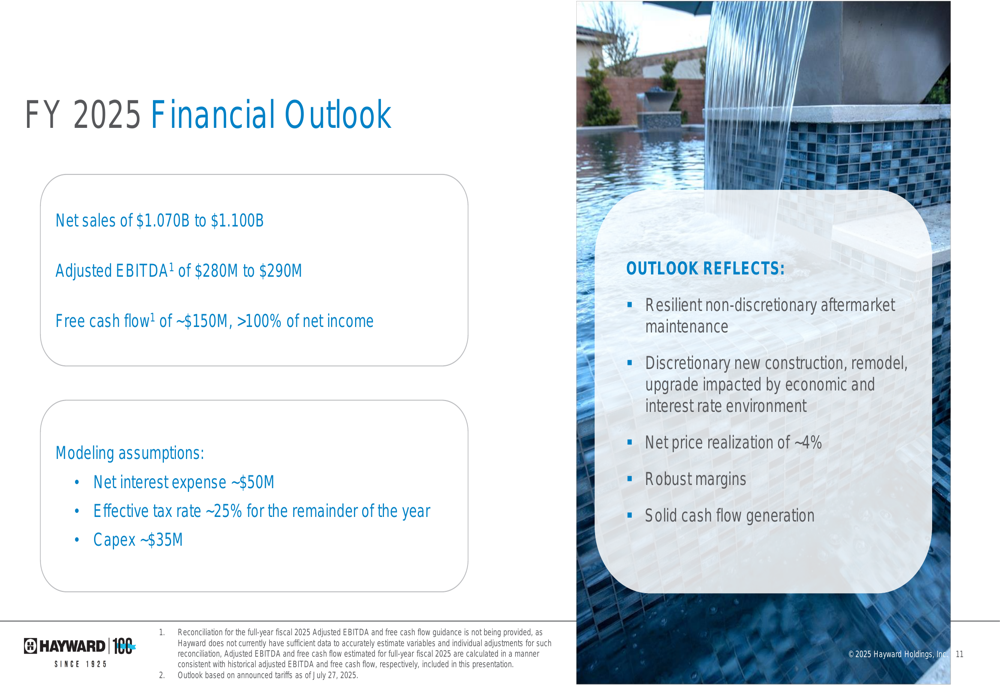

Forward Guidance and Outlook

Based on its strong first-half performance, Hayward refined its full-year 2025 guidance, raising the lower end of its net sales range. The company now expects net sales between $1.070 billion and $1.100 billion, with adjusted EBITDA projected between $280 million and $290 million.

The guidance reflects Hayward’s confidence in its resilient aftermarket business model, which accounts for approximately 85% of sales and is largely non-discretionary in nature. While the company acknowledges that discretionary spending on new construction and remodeling remains impacted by the current economic and interest rate environment, it expects to achieve net price realization of approximately 4% for the full year.

The detailed financial outlook is presented below:

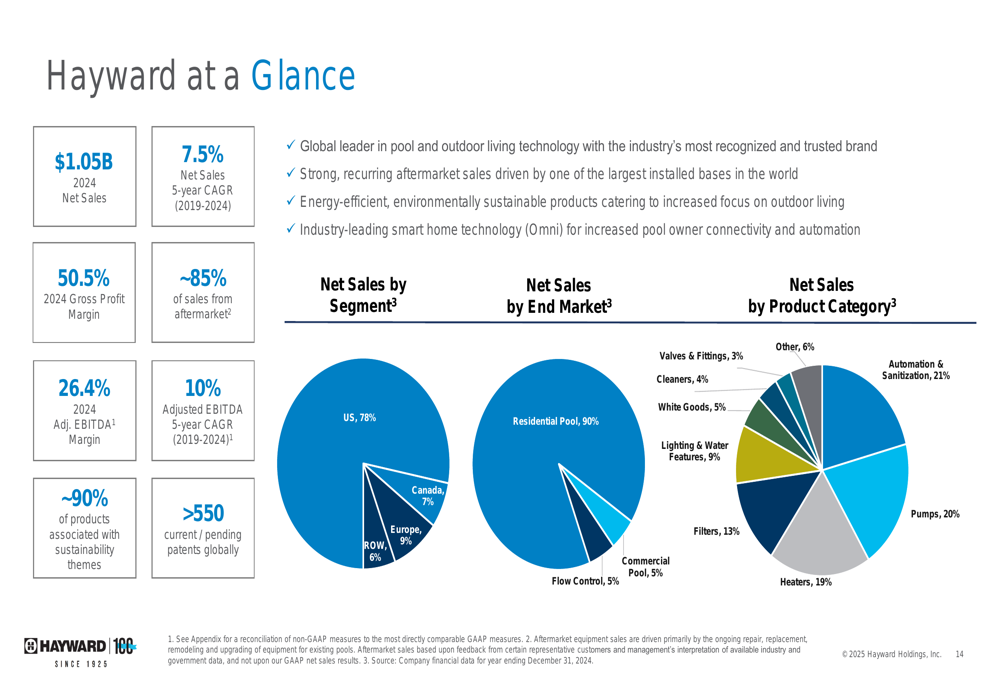

Hayward’s long-term investment thesis remains compelling, supported by its strong brand, technological leadership, and focus on sustainability. The company’s products cater to growing trends in outdoor living and smart home technology, with approximately 90% of its offerings associated with sustainability themes.

As shown in this comprehensive overview, Hayward combines a strong financial profile with attractive industry positioning:

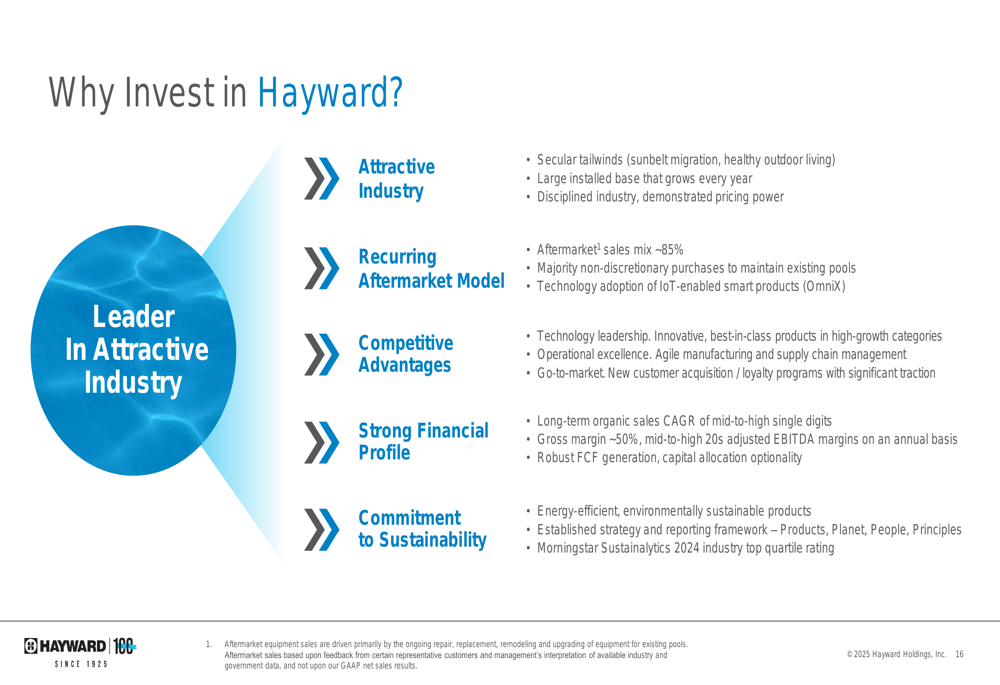

The company’s investment case is further strengthened by its recurring aftermarket revenue model, competitive advantages, and commitment to sustainability:

Despite near-term challenges from tariffs and economic uncertainty, Hayward’s Q2 2025 results demonstrate the company’s ability to execute effectively while positioning itself for long-term growth through strategic investments, operational excellence, and disciplined capital allocation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.