Street Calls of the Week

Introduction & Market Context

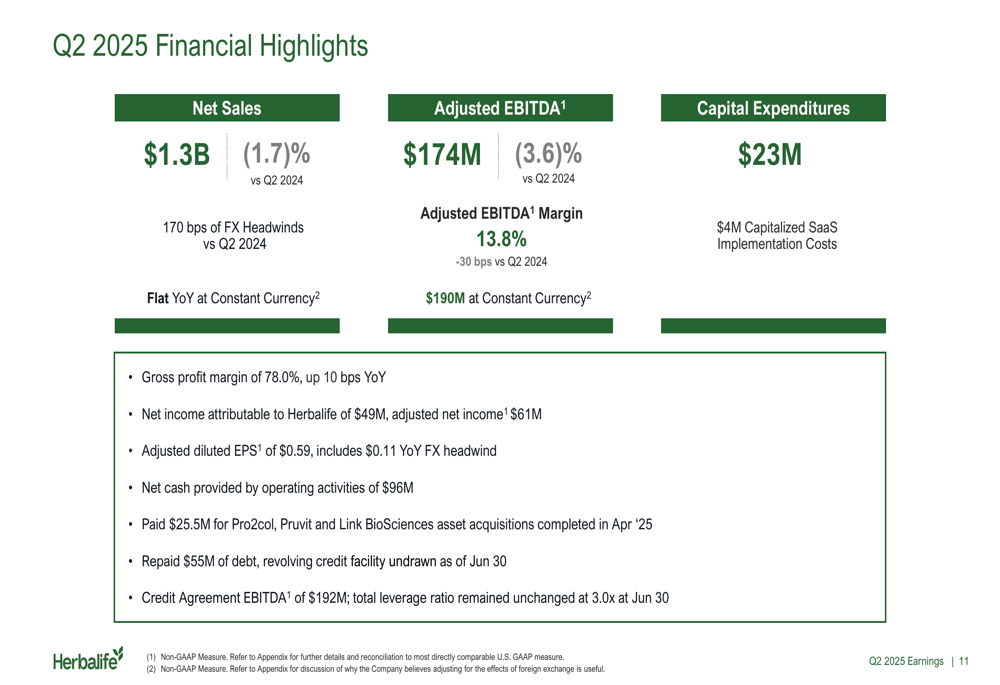

Herbalife Nutrition Ltd (NYSE:HLF) presented its Q2 2025 earnings results on August 6, 2025, reporting net sales of $1.3 billion, flat year-over-year on a constant currency basis but down 1.7% as reported. The nutritional supplement company’s shares closed at $9.25, down 2.22% on the day, suggesting mixed investor reaction despite the company raising its full-year adjusted EBITDA guidance.

The results come as Herbalife continues to navigate a challenging global economic environment while pushing forward with its digital transformation strategy and new product innovations. The company’s focus on debt reduction and operational efficiency appears to be gaining traction, even as sales volumes face pressure in certain markets.

Quarterly Performance Highlights

Herbalife’s Q2 2025 performance showed resilience in key financial metrics despite currency headwinds. The company reported adjusted EBITDA of $174 million, exceeding guidance, with a constant currency figure of $190 million. Gross profit margin improved slightly to 78.0%, up 10 basis points year-over-year.

As shown in the following comprehensive overview of Q2 results:

The company reported adjusted diluted EPS of $0.59, consistent with its Q1 2025 performance. Net income attributable to Herbalife was $49 million, with adjusted net income of $61 million. The company generated $96 million in cash from operating activities and continued its debt reduction strategy by repaying $55 million of debt, including $50 million of 2025 Notes.

A closer examination of Q2 financial metrics reveals the components affecting the company’s performance:

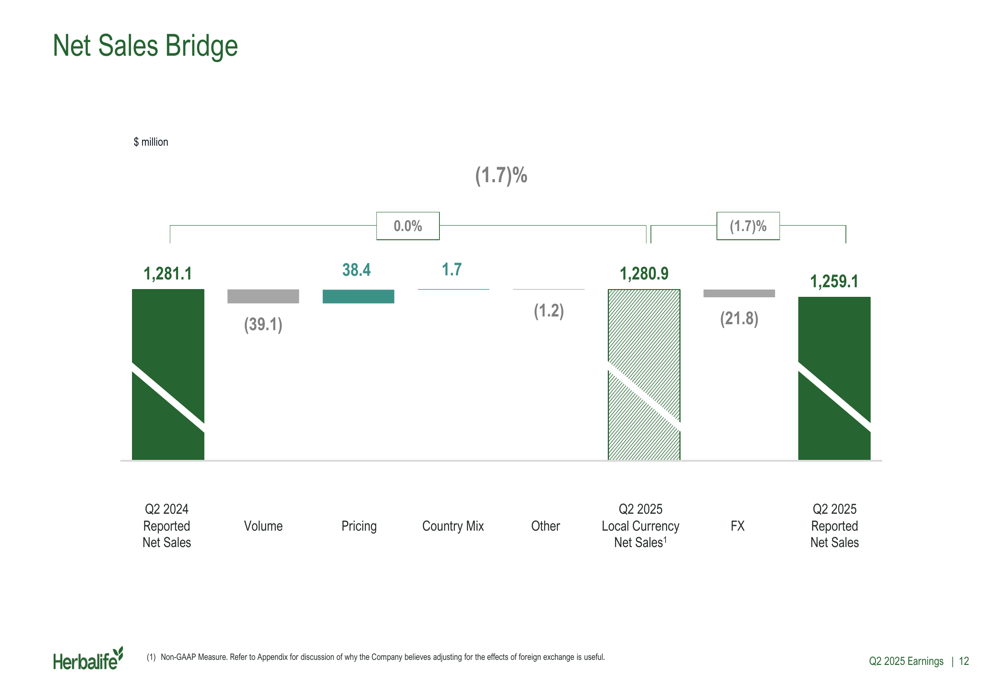

The sales bridge analysis illustrates how pricing increases nearly offset volume declines, resulting in flat constant currency sales:

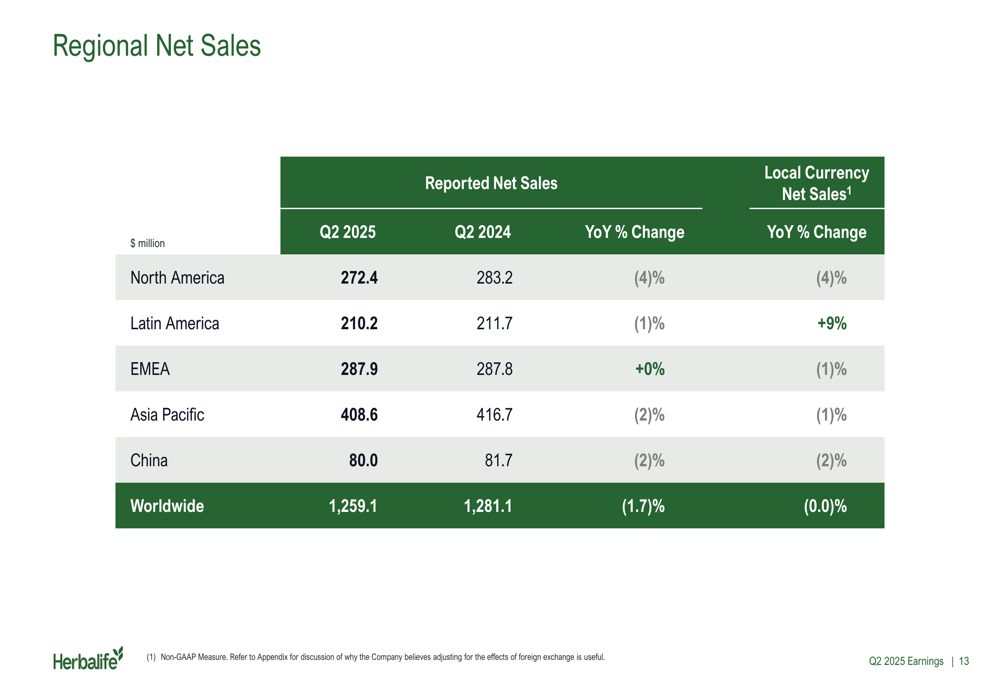

Regional performance varied significantly, with Latin America showing strength at 9% local currency growth despite a 1% decline in reported sales. North America faced the most significant challenges with a 4% decline in both reported and local currency sales. EMEA, Asia Pacific, and China showed modest declines between 1-2% in local currency terms.

Strategic Initiatives

Herbalife’s presentation highlighted several strategic initiatives aimed at driving future growth, with particular emphasis on its digital transformation. The company unveiled the beta version of its Pro2col digital platform, a personalized wellness system that has already engaged over 7,000 distributors, signaling strong initial demand.

The Pro2col platform combines personal data, biomarkers, targeted supplementation, lifestyle habits, coaching, and community elements:

In addition to digital innovation, Herbalife continues to expand its product portfolio with the launch of MultiBurn, a multifunctional weight-loss supplement containing clinically studied botanicals designed to support metabolic health:

The company also introduced market-specific products including Instant Coffee in Mexico, Nutri Muffin in Latin America, and Sleep Enhance in India, demonstrating its commitment to tailoring offerings to regional preferences.

Distributor engagement remains a key focus, with approximately 37,700 attendees at Extravaganza training events and the expanded global rollout of the Diamond Development Mastermind Program. New distributor growth was reported in four out of five regions, led by Latin America with a 16% increase.

Financial Analysis

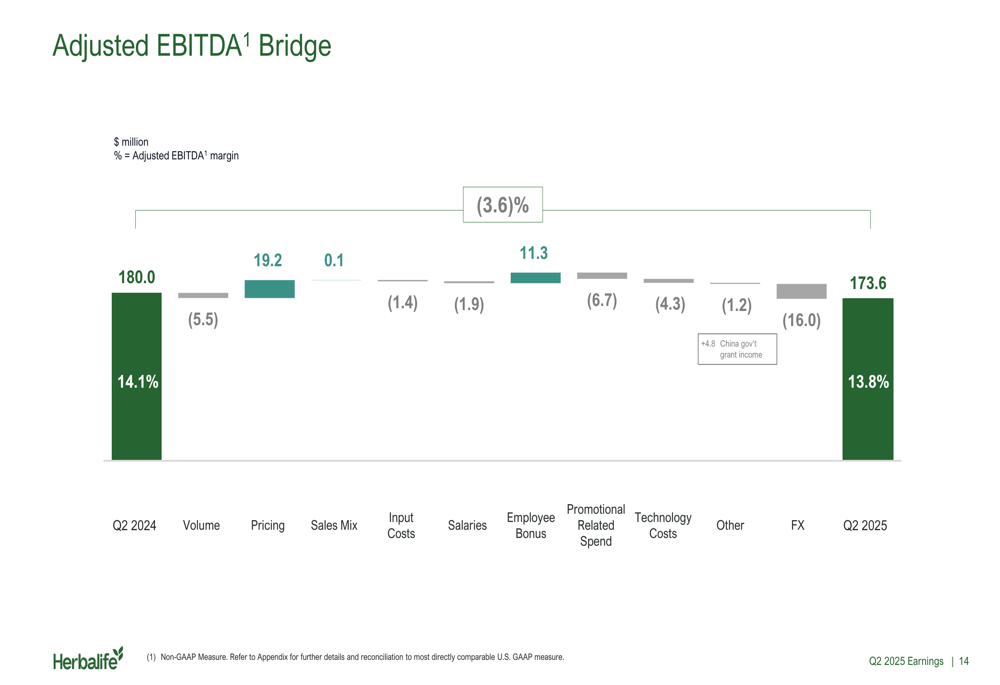

The adjusted EBITDA bridge provides insight into the factors affecting profitability. While volume decreases and foreign exchange negatively impacted EBITDA, these were partially offset by pricing increases and other factors including a China government grant:

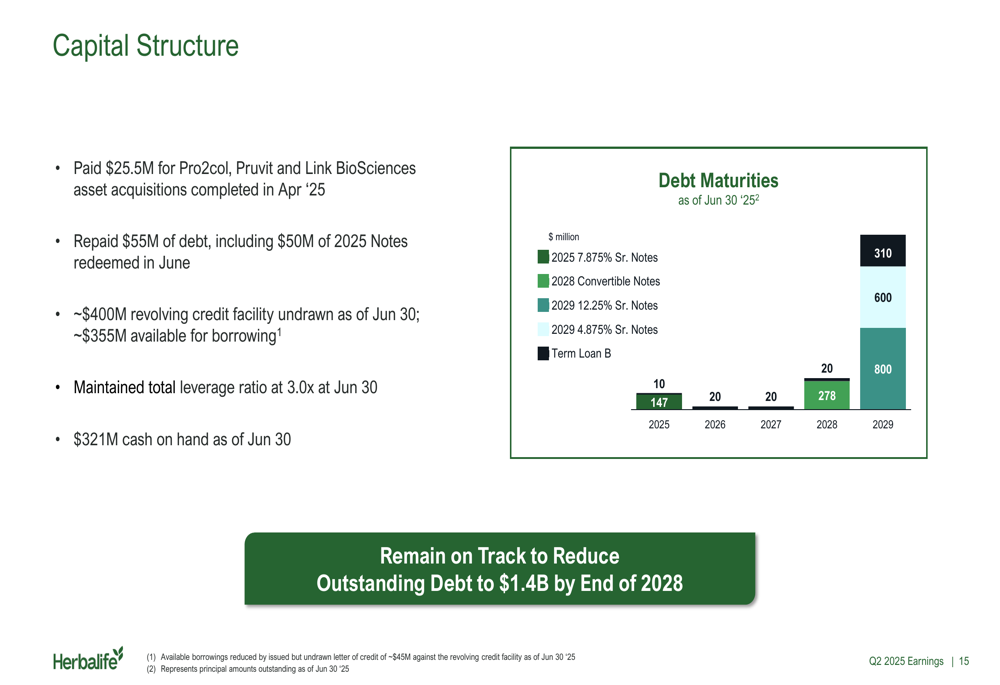

Herbalife’s capital structure shows continued focus on debt reduction, with $321 million in cash on hand as of June 30 and a total leverage ratio of 3.0x:

Forward-Looking Statements

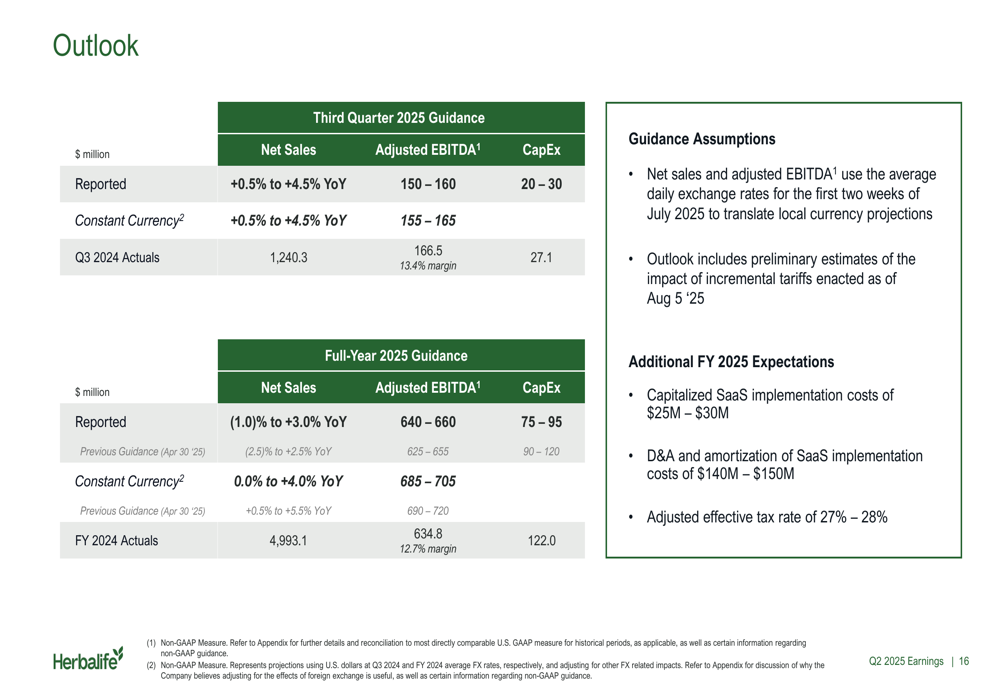

Herbalife raised its full-year 2025 adjusted EBITDA guidance to $640-660 million, up from the previous range of $625-655 million, suggesting confidence in its second-half performance. For Q3 2025, the company projects net sales growth of 0.5% to 4.5% year-over-year on both a reported and constant currency basis.

The detailed outlook for both Q3 and full-year 2025 shows expectations for improved performance in the second half:

The company’s capital expenditure guidance of $75-95 million for the full year, along with $25-30 million in capitalized SaaS implementation costs, indicates continued investment in technology infrastructure to support its digital transformation initiatives.

Conclusion

Herbalife’s Q2 2025 results reflect a company in transition, balancing financial discipline with strategic investments in digital platforms and product innovation. While sales remain flat on a constant currency basis, the raised EBITDA guidance suggests improving operational efficiency and cost management.

The Pro2col platform represents a significant bet on personalized wellness as a growth driver, while the company’s continued focus on debt reduction aims to strengthen its financial foundation. As Herbalife moves into the second half of 2025, investors will be watching closely to see if these strategic initiatives translate into accelerated growth and improved shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.