Novo Nordisk, Eli Lilly slide after Trump comments on weight loss drug pricing

Introduction & Market Context

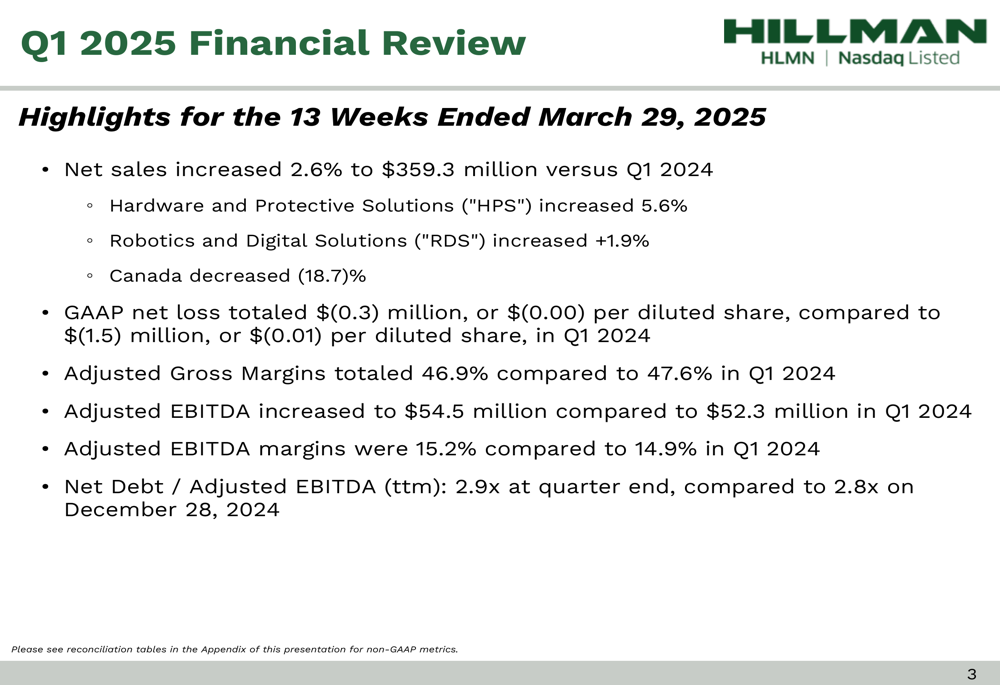

Hillman Solutions Corp (NASDAQ:HLMN) reported its first quarter 2025 financial results on April 29, 2025, showing modest revenue growth and improved profitability despite continued challenges in its Canadian segment. The hardware and home improvement solutions provider continues to execute on its strategic initiatives, particularly in diversifying its supply chain to reduce reliance on Chinese manufacturing.

The company’s shares responded positively to the earnings release, with premarket trading showing an 8.06% increase to $8.18, suggesting investors were encouraged by the results and outlook.

Quarterly Performance Highlights

Hillman reported Q1 2025 net sales of $359.3 million, representing a 2.6% increase compared to the same period in 2024. The company narrowed its GAAP net loss to $(0.3) million, or $(0.00) per diluted share, an improvement from the $(1.5) million, or $(0.01) per share, reported in Q1 2024.

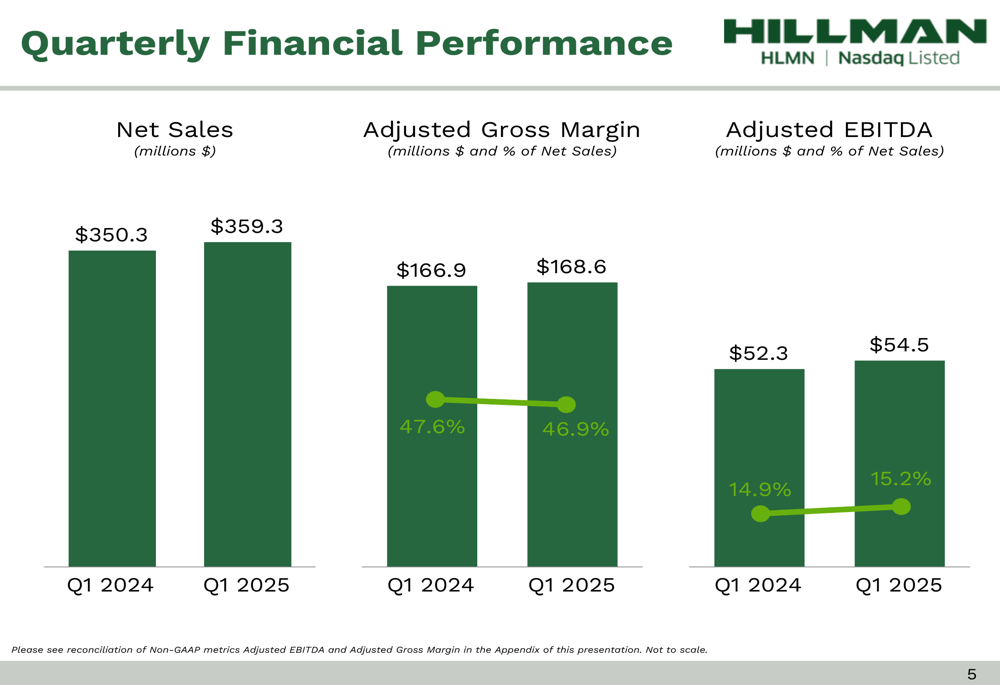

As shown in the following financial summary, Hillman’s adjusted EBITDA increased to $54.5 million from $52.3 million in the prior year, with adjusted EBITDA margins improving to 15.2% from 14.9%:

The company’s quarterly financial performance demonstrates continued growth in both revenue and profitability metrics, though adjusted gross margins experienced a slight decline to 46.9% from 47.6% in the prior year period:

Hillman maintained strong operational performance with year-to-date fill rates averaging 96%, reflecting the company’s commitment to customer service. This focus on customer relationships was further validated when Hillman Canada won the 2024 "Vendor of the Year" award from Kent Building Supplies during the quarter.

Segment Analysis

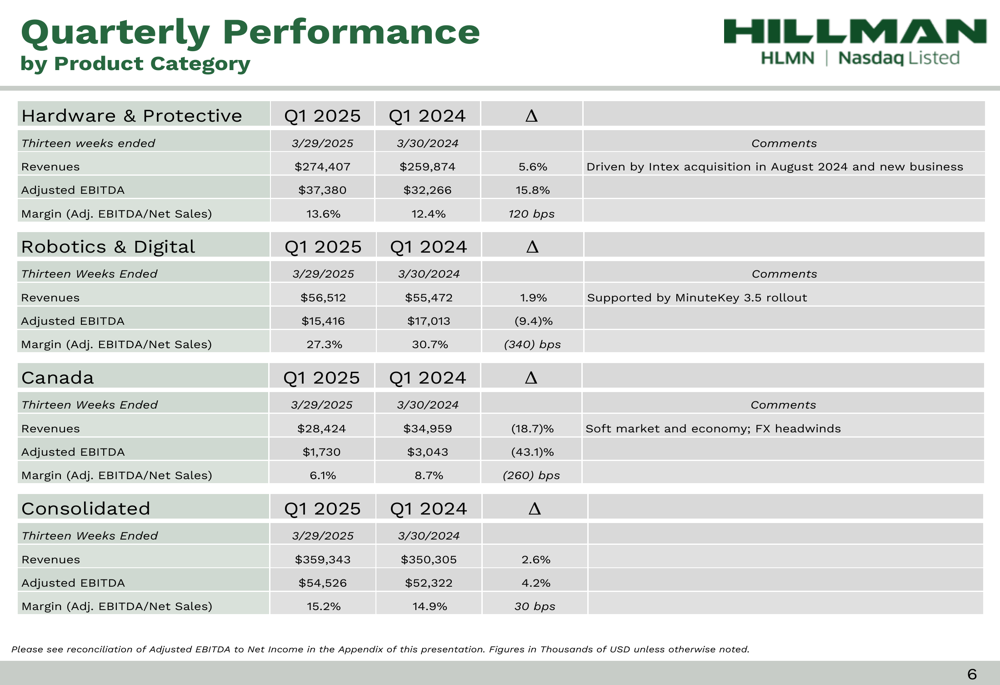

Hillman’s performance varied significantly across its three business segments. The Hardware and Protective Solutions (HPS) segment led growth with a 5.6% revenue increase to $274.4 million, driven in part by the Intex acquisition. Robotics and Digital Solutions (RDS) grew modestly at 1.9% to $56.5 million, while the Canadian segment experienced a significant 18.7% decline to $28.4 million.

The following breakdown illustrates the performance by product category:

The HPS segment showed particularly strong adjusted EBITDA growth of 15.8% to $37.4 million, while RDS experienced a decline of 9.4% to $15.4 million. Canada’s adjusted EBITDA fell by 43.1% to $1.7 million, reflecting challenging market conditions and foreign exchange headwinds.

Strategic Initiatives

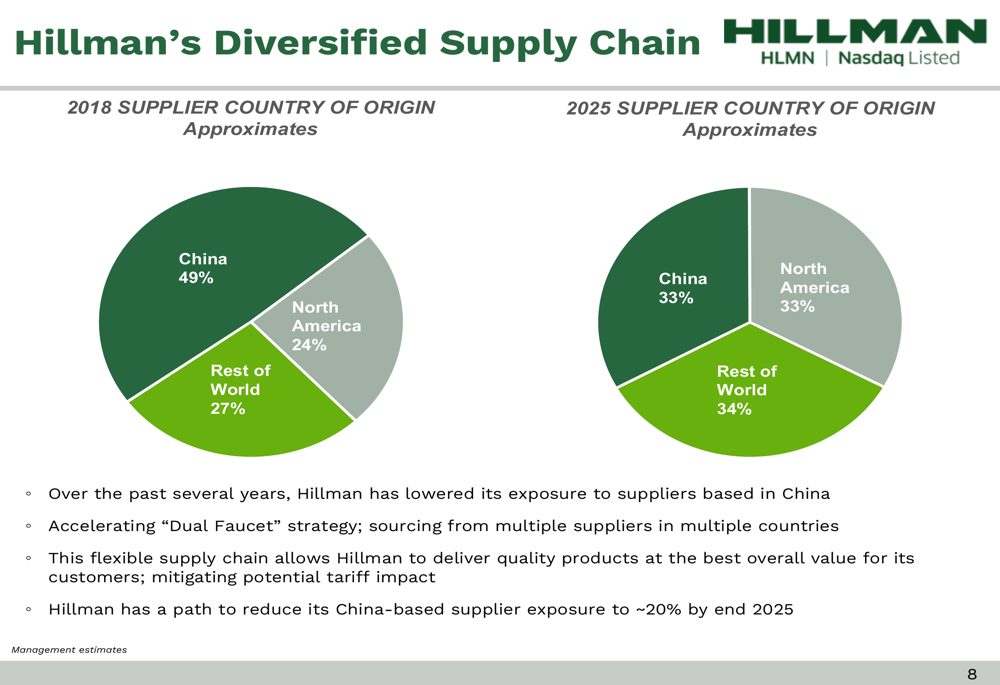

A key focus of Hillman’s strategic initiatives is the diversification of its supply chain. The company has made significant progress in reducing its reliance on Chinese suppliers, shifting from 49% China-based sourcing in 2018 to 33% in 2025. Hillman has indicated it has the ability to further reduce its China exposure to approximately 20% by year-end 2025.

The following chart illustrates Hillman’s supply chain diversification strategy:

This "Dual Faucet" strategy involves sourcing from multiple suppliers in multiple countries, creating a more flexible supply chain that can mitigate potential tariff impacts while delivering quality products at competitive values for customers.

Capital Structure & Guidance

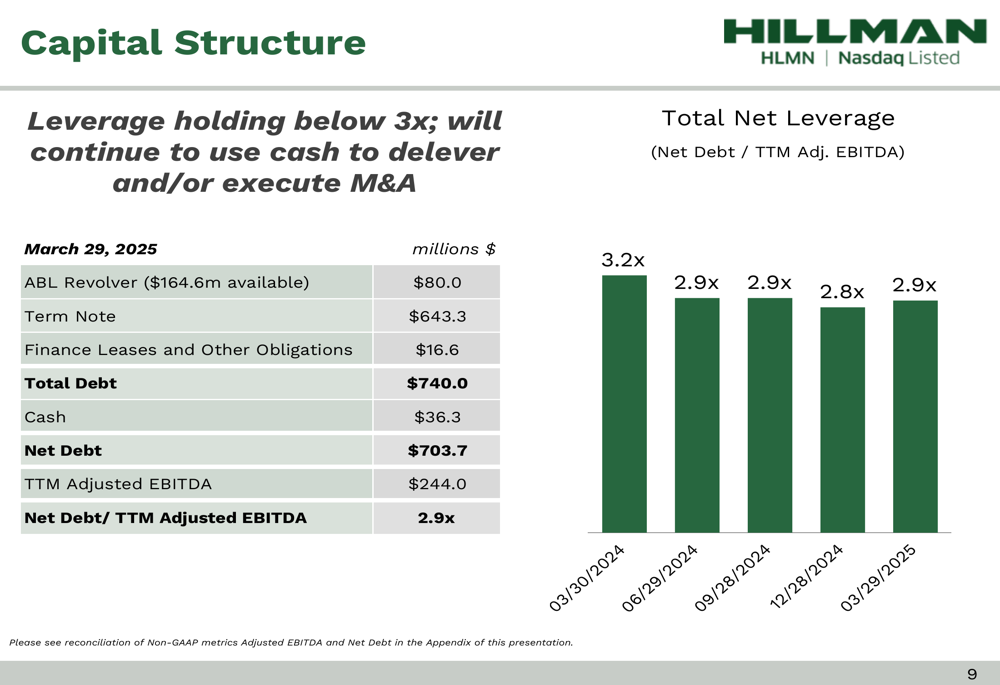

Hillman’s capital structure remains relatively stable, with net leverage at 2.9x adjusted EBITDA as of March 29, 2025, slightly up from 2.8x at the end of 2024 but down from 3.2x a year earlier. The company continues to focus on deleveraging while maintaining flexibility for strategic acquisitions.

The following slide details Hillman’s current capital structure:

For the full year 2025, Hillman reiterated its guidance for revenues of $1.495 to $1.575 billion and adjusted EBITDA of $255 to $275 million. The company has withdrawn its previous free cash flow guidance and is now targeting a year-end leverage ratio of 2.5x.

Forward-Looking Statements

Hillman emphasized its resilience through multiple economic cycles and its focus on products utilized for repair, maintenance, and remodel projects, which tend to be less cyclical than new construction. The company’s direct-to-store fulfillment model, supported by a 1,200-member distribution team, continues to be a competitive advantage.

The company highlighted its value proposition as an indispensable partner to winning retailers, with market leadership across multiple categories:

Hillman’s product portfolio spans three primary categories where it maintains a #1 market position: Hardware Solutions, Protective Solutions, and Robotics & Digital Solutions. The company serves major retailers including ACE Hardware, The Home Depot (NYSE:HD), Lowe’s (NYSE:LOW), Tractor Supply (NASDAQ:TSCO) Co., and Walmart (NYSE:WMT).

Looking ahead, Hillman continues to pursue accretive, tuck-in M&A opportunities that leverage the company’s competitive advantages. Management maintains historical long-term annual growth targets of 6% for organic revenue growth and 10% for organic adjusted EBITDA growth, with acquisitions potentially adding another 4-5% to both metrics.

The company’s Q1 2025 results represent a solid start to the year, with continued execution on strategic initiatives despite challenges in certain segments. Hillman’s focus on supply chain diversification, customer relationships, and strategic acquisitions positions it well for sustainable growth in the hardware and home improvement solutions market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.