US stock futures inch higher with Q3 earnings on tap

Introduction & Market Context

Home Bancorp Inc (NASDAQ:HBCP) released its second quarter 2025 earnings presentation on July 22, showcasing continued financial strength and operational momentum. The Lafayette, Louisiana-based regional bank reported significant improvements in profitability metrics, driven by expanding net interest margin and disciplined expense management.

The company’s stock has performed well in 2025, with shares trading at $56.08 as of July 21, 2025, representing a 46.4% increase from Q1 2024 levels. This performance reflects investor confidence in the bank’s strategic direction and financial health.

Home Bancorp operates 43 locations across Southern Louisiana, Western Mississippi, and Houston, with a market capitalization of $438 million as of mid-July 2025. The company has built on its Q1 momentum, when it beat earnings expectations with an EPS of $1.37 compared to the forecasted $1.15.

Quarterly Performance Highlights

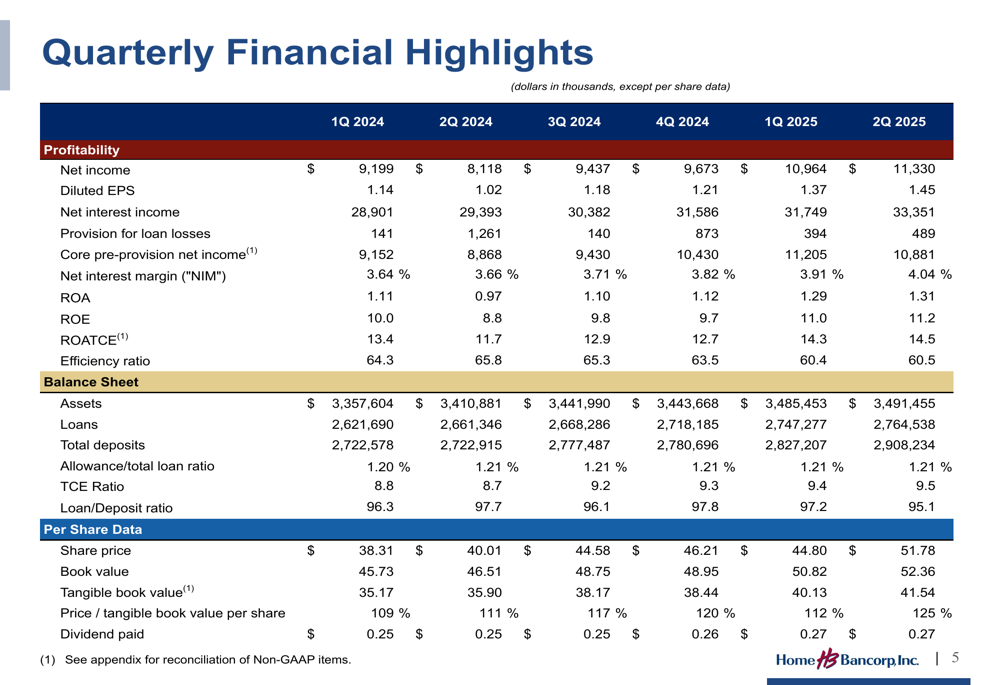

Home Bancorp reported impressive financial results for Q2 2025, with net income reaching $11.33 million, up from $9.20 million in Q1 2024, representing a 23.2% increase. Diluted earnings per share rose to $1.45, compared to $1.14 in the same period last year.

The company’s net interest margin expanded to 4.04% in Q2 2025, a significant improvement from 3.64% in Q1 2024, continuing the positive trend observed in the first quarter. This expansion has been a key driver of the bank’s improved profitability.

As shown in the following comprehensive financial highlights table, Home Bancorp demonstrated improvement across virtually all key performance metrics:

Return on average assets (ROA) increased to 1.31% in Q2 2025 from 1.11% in Q1 2024, while return on average equity (ROE) improved to 11.2% from 10.0% over the same period. The efficiency ratio, a measure of operating expenses as a percentage of revenue, improved to 60.5% from 64.3%, indicating better operational efficiency.

Total (EPA:TTEF) assets grew to $3.49 billion as of June 30, 2025, up from $3.36 billion in Q1 2024. Loans increased to $2.76 billion from $2.62 billion, while deposits rose to $2.91 billion from $2.72 billion over the same period.

Loan Portfolio and Market Diversification

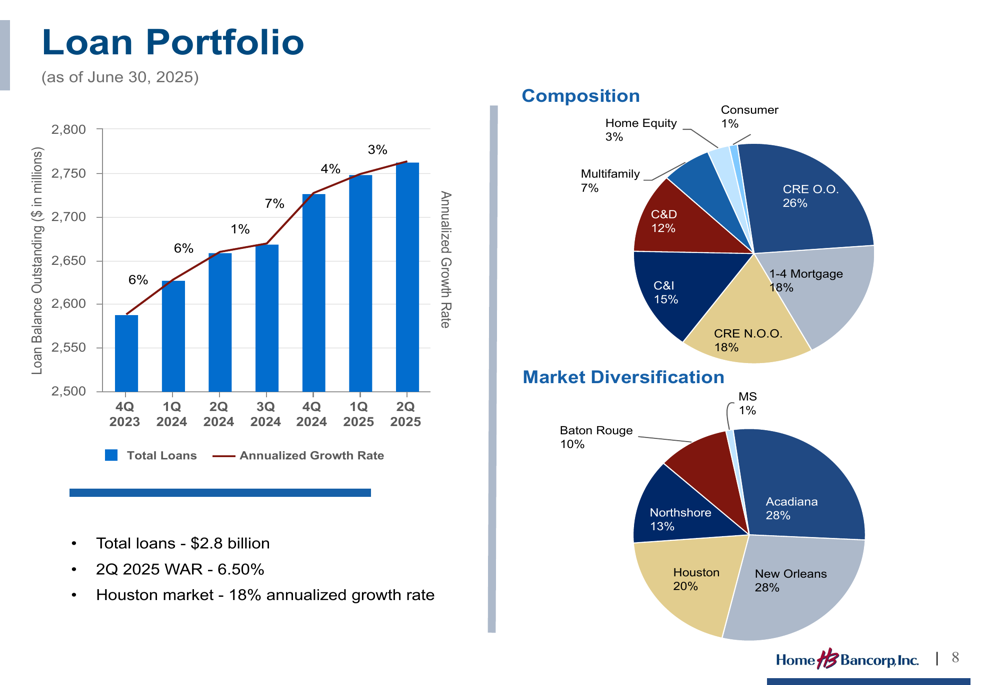

Home Bancorp maintains a well-diversified loan portfolio across various sectors and geographic markets, which has contributed to its resilience and growth. The loan portfolio composition shows a balanced mix of commercial real estate (CRE), residential mortgages, and commercial and industrial (C&I) loans.

The following chart illustrates the company’s loan portfolio composition and market diversification as of June 30, 2025:

Owner-occupied commercial real estate represents the largest segment at 26% of the total loan portfolio, followed by 1-4 family mortgages (18%) and non-owner-occupied commercial real estate (18%). Commercial and industrial loans make up 15% of the portfolio, while construction and development loans account for 12%.

Geographically, the loan portfolio is well-distributed across the bank’s markets, with Acadiana (28%) and New Orleans (28%) representing the largest concentrations, followed by Houston (20%), Northshore (13%), and Baton Rouge (10%).

The Houston market has been particularly strong, showing an 18% annualized growth rate, highlighting the success of the bank’s expansion strategy in this market. The weighted average rate on the loan portfolio was 6.50% in Q2 2025, contributing to the bank’s strong net interest margin.

Asset Growth and Long-term Performance

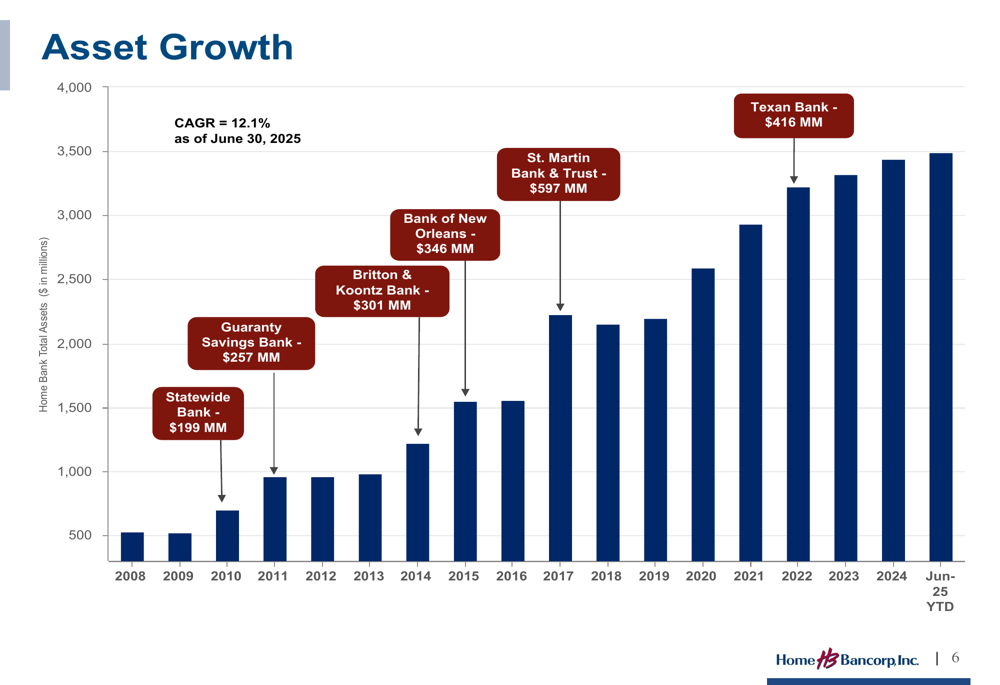

Home Bancorp has demonstrated consistent asset growth over the years, with a compound annual growth rate (CAGR) of 12.1% since 2008. This growth has been achieved through both organic expansion and strategic acquisitions.

The following chart illustrates the bank’s impressive asset growth trajectory:

Since 2010, Home Bancorp has completed six acquisitions, adding significant scale to its operations. These acquisitions include Statewide Bank ($199 million), Guaranty Savings Bank ($257 million), Britton & Koontz Bank ($301 million), Bank of New Orleans ($346 million), St. Martin Bank & Trust ($597 million), and Texan Bank ($416 million).

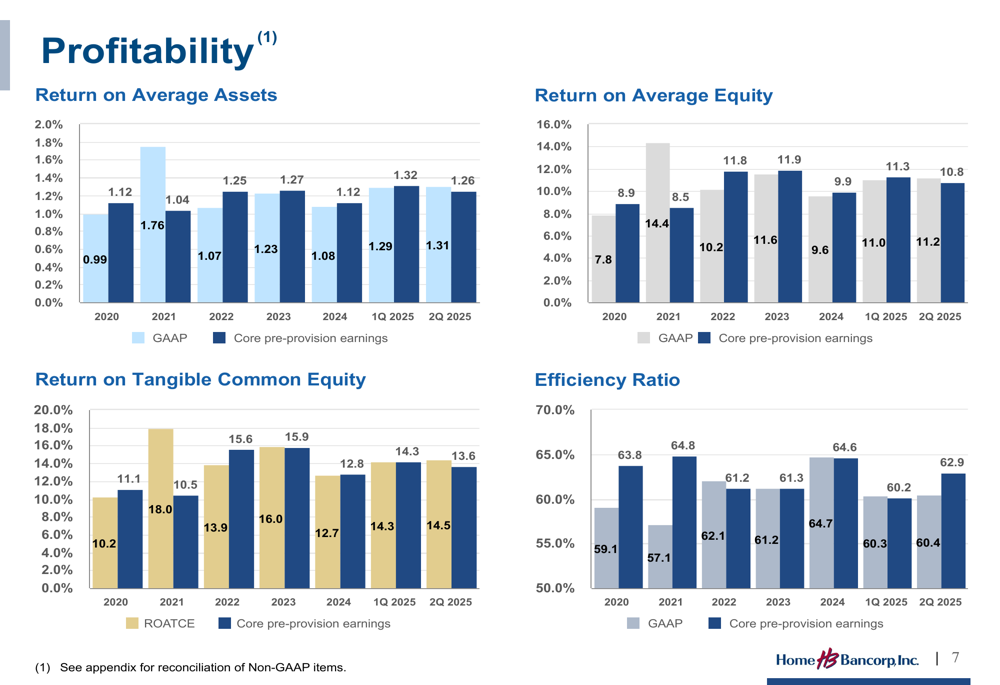

The bank’s profitability metrics have also shown positive trends over time, with improvements in ROA, ROE, and efficiency ratio:

Credit Quality and Risk Management

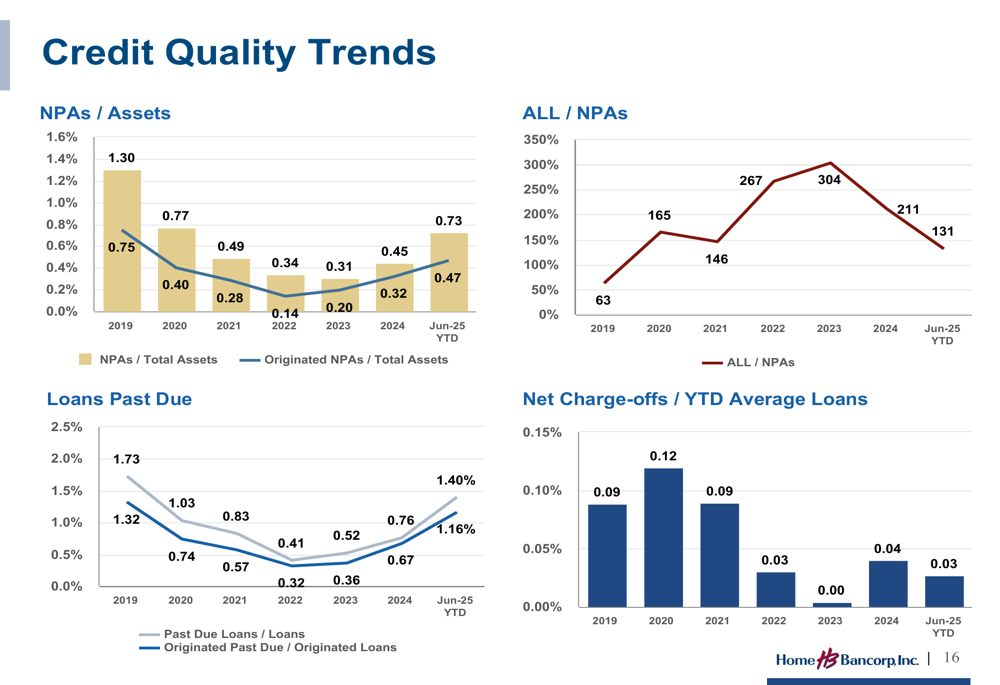

Home Bancorp maintains a conservative credit culture, which is reflected in its credit quality metrics. While nonperforming loans increased to $23.35 million as of June 30, 2025, from $16.82 million a year earlier, they remain well-covered by the bank’s allowance for loan losses.

The following chart illustrates the bank’s credit quality trends:

The allowance for loan losses stood at $33.4 million as of June 30, 2025, providing adequate coverage for potential credit losses. Net charge-offs have remained low, reflecting the bank’s disciplined underwriting standards and effective risk management practices.

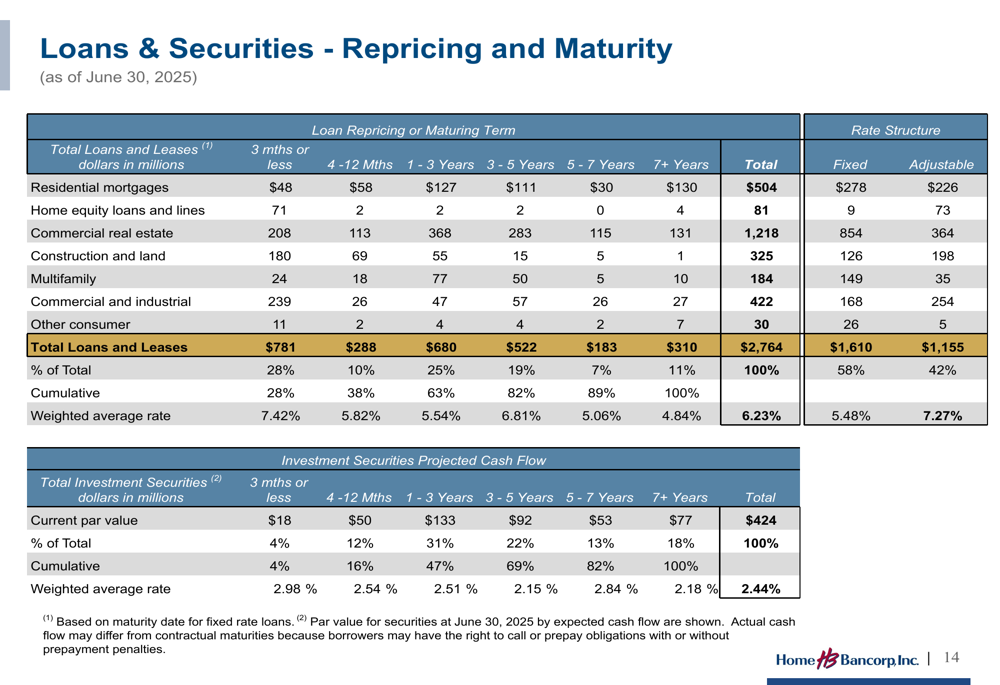

The bank’s loan portfolio is well-structured in terms of repricing and maturity, providing some protection against interest rate fluctuations:

Deposit Base and Liquidity

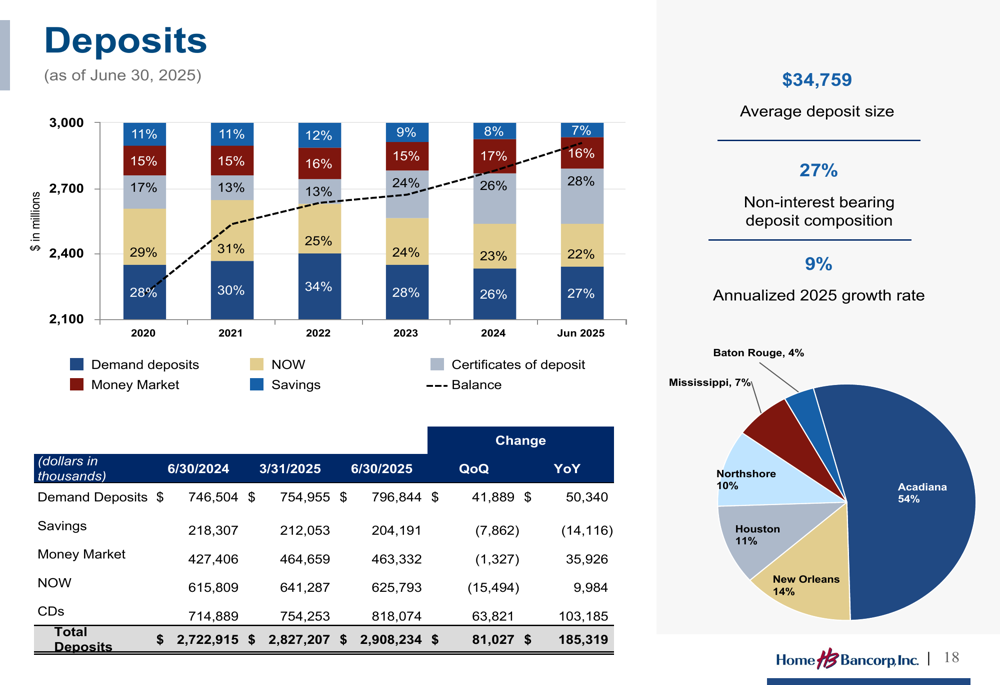

Home Bancorp’s deposit base has shown healthy growth, with total deposits reaching $2.91 billion as of June 30, 2025, representing an annualized growth rate of 9% in 2025. The deposit composition is diversified across the bank’s markets, with a solid base of core deposits.

The following chart provides an overview of the bank’s deposit composition:

Non-interest bearing deposits represent 27% of total deposits, contributing to the bank’s favorable funding costs. The average deposit size is $34,759, indicating a granular deposit base primarily composed of retail and small business customers.

The bank maintains a strong liquidity position, with total primary and secondary liquidity of $1.32 billion, providing 179% coverage of uninsured deposits. Approximately 62% of deposits are FDIC insured, with uninsured deposits representing 24% of the total.

Capital Position and Shareholder Returns

Home Bancorp maintains a strong capital position, with regulatory capital ratios well above regulatory requirements. As of June 30, 2025, the bank’s Tier 1 leverage ratio was 11.5%, common equity Tier 1 ratio was 13.4%, and total risk-based capital ratio was 14.7%.

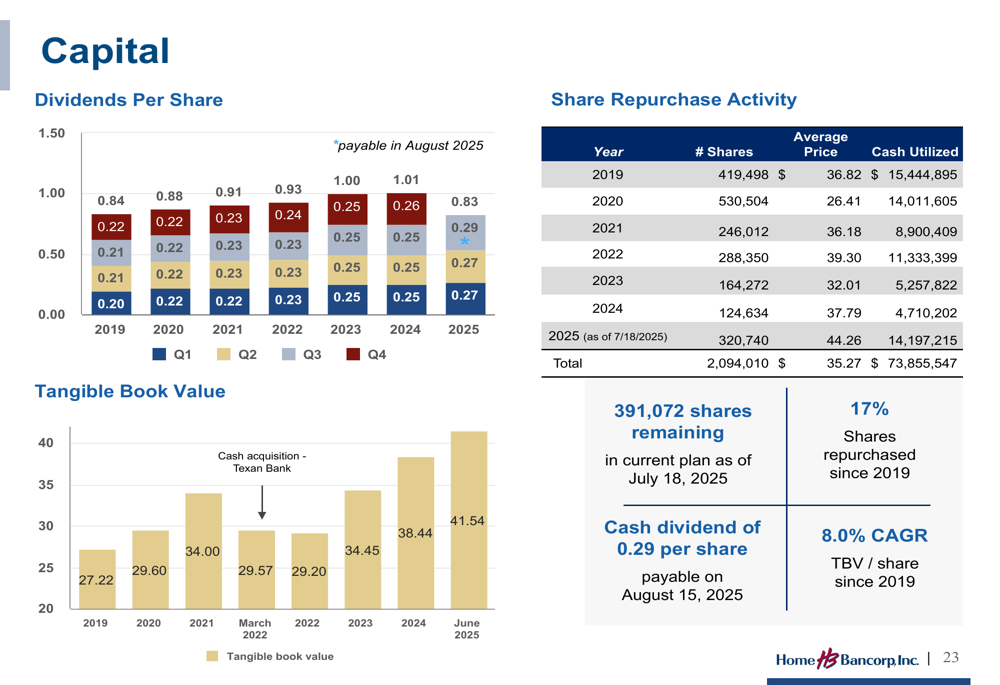

The bank has demonstrated a commitment to returning capital to shareholders through dividends and share repurchases. The following chart illustrates the growth in dividends per share and tangible book value:

Tangible book value per share has increased to $41.54 as of June 30, 2025, from $35.17 in Q1 2024, representing a compound annual growth rate of 8.0% since 2019. The bank has declared a cash dividend of $0.29 per share payable on August 15, 2025, up from $0.27 in the previous quarter and $0.25 in Q1 2024.

Since 2019, Home Bancorp has repurchased approximately 17% of its outstanding shares, with 391,072 shares remaining under the current repurchase authorization.

Forward-Looking Statements

Looking ahead, Home Bancorp is well-positioned for continued growth and profitability. The bank’s strong capital position provides capacity for organic growth and potential acquisitions. The diversified loan portfolio and market presence offer multiple avenues for expansion.

Management has highlighted several key strengths that support the bank’s investment perspective, including strong earnings and shareholder returns, a conservative and well-managed credit culture, and the ability to capitalize on market disruption to create new opportunities.

The bank’s performance in Q2 2025 builds on the positive momentum observed in Q1, when management expressed optimism about continued net interest margin expansion and loan growth of 4-6% annually. The Q2 results suggest that the bank is on track to meet or exceed these expectations.

With its strong financial performance, diversified business model, and commitment to shareholder returns, Home Bancorp appears well-positioned to navigate the current economic environment and deliver long-term value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.