Novo Nordisk, Eli Lilly fall after Trump comments on weight loss drug pricing

Introduction & Market Context

HORNBACH Holding AG & Co. KGaA presented its first quarter 2025/26 results on June 24, 2025, revealing strong performance driven by favorable weather conditions across Central Europe. The German home improvement retailer, which operates stores across multiple European countries, reported significant growth in both sales and profitability compared to the same period last year.

According to the presentation led by CEO & interim CFO Albrecht Hornbach, the company benefited from warm and mostly dry weather conditions in Central Europe during the quarter, which boosted customer frequency and encouraged larger purchase sizes in its home improvement stores. The company also noted that it had 1.2 additional business days compared to the prior-year period, further supporting sales growth.

Shares of HORNBACH (HBH) have been trading at €91.00 as of June 23, 2025, up 1.45% on the day, and have ranged between €69.80 and €106.80 over the past 52 weeks.

Quarterly Performance Highlights

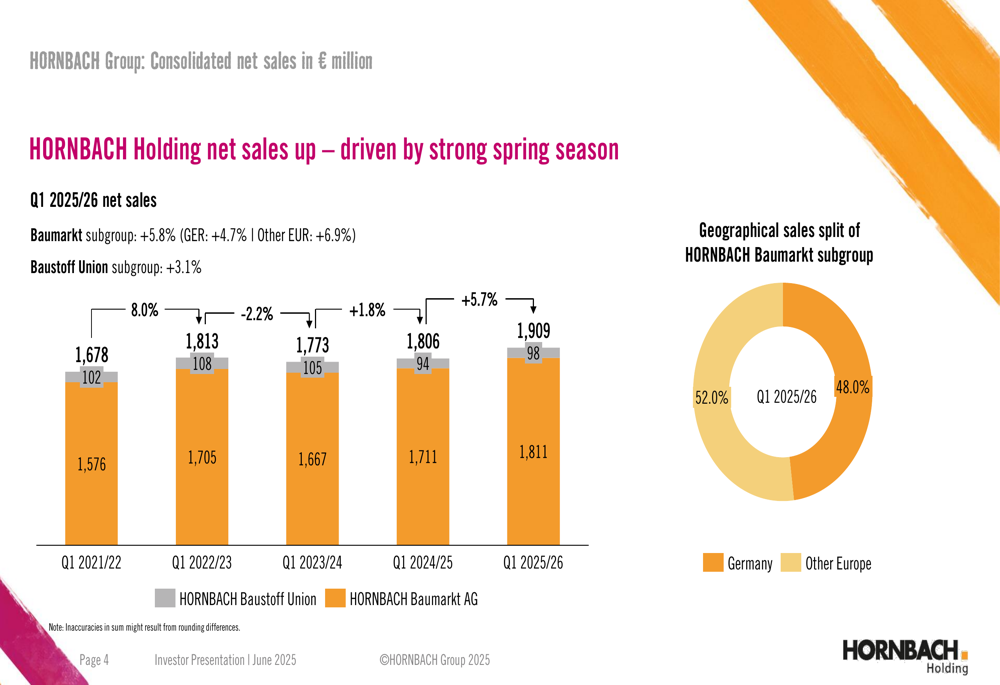

HORNBACH reported consolidated net sales of €1,909.2 million for Q1 2025/26, representing a 5.7% increase compared to the same period last year. Like-for-like sales in the DIY segment grew by 4.7%, with the HORNBACH Baumarkt subgroup showing a 5.8% increase and the HORNBACH Baustoff Union subgroup growing by 3.1%.

As shown in the following chart of quarterly consolidated net sales, the company has demonstrated consistent growth over recent years, with Q1 2025/26 marking the strongest first quarter performance to date:

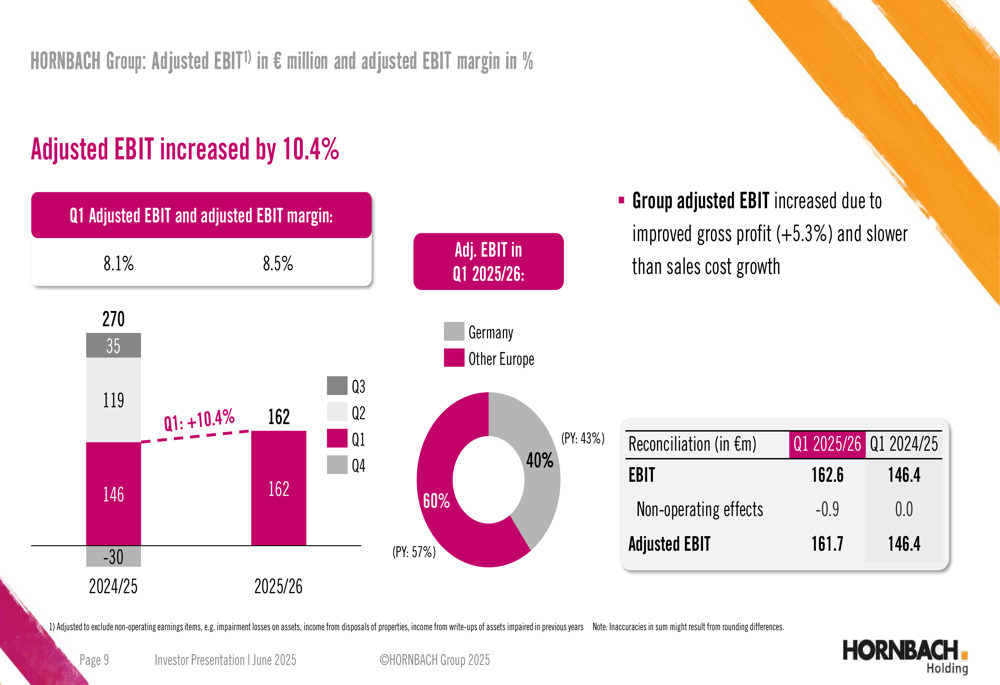

The company’s adjusted EBIT increased by 10.4% to €161.7 million, with the adjusted EBIT margin improving to 8.5% from 8.1% in the prior-year period. Earnings per share rose to €6.62 from €5.96 in Q1 2024/25.

The following chart illustrates HORNBACH’s adjusted EBIT performance, showing the significant improvement in the first quarter:

From a geographical perspective, Germany contributed 60% of the adjusted EBIT in Q1 2025/26 (up from 57% in the prior-year period), while Other European countries accounted for 40% (down from 43%). This shift reflects stronger performance in the company’s domestic market during the quarter.

Market Share and Competitive Position

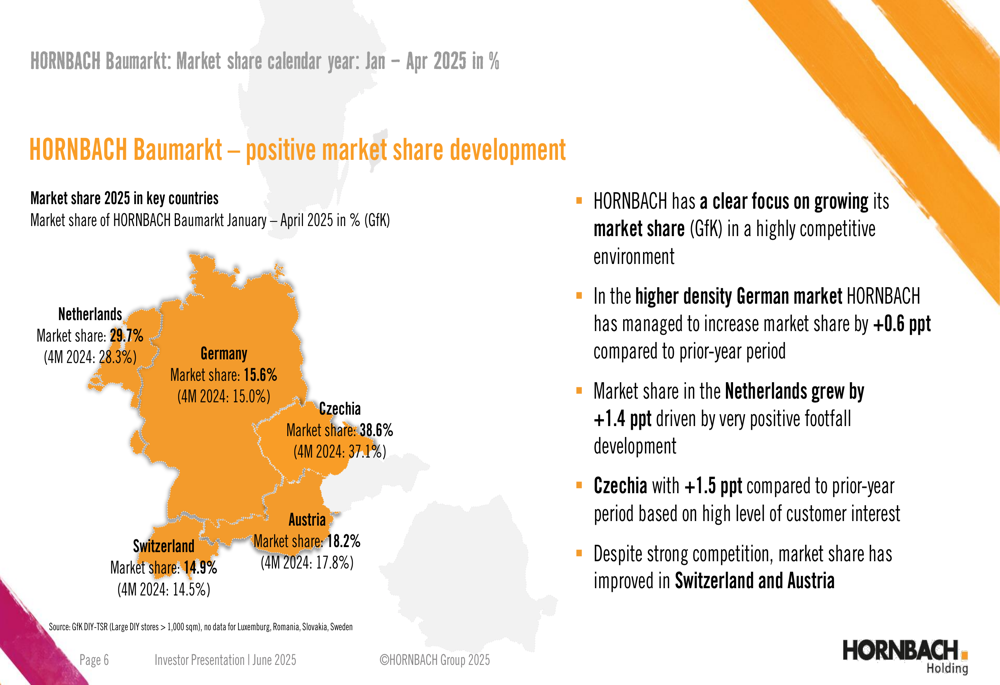

HORNBACH reported market share gains across all its key markets, demonstrating its competitive strength despite operating in a challenging retail environment. The company emphasized its "clear focus on growing market share in a highly competitive environment."

The market share developments from January to April 2025 compared to the same period in 2024 are illustrated in the following map:

Particularly notable were the gains in Czechia (+1.5 percentage points to 38.6%) and Germany (+0.6 percentage points to 15.6%). The Netherlands remains a strong market for HORNBACH with a 29.7% share (up from 28.3%), while Switzerland and Austria also showed improvements despite what the company described as "strong competition."

E-commerce and Digital Strategy

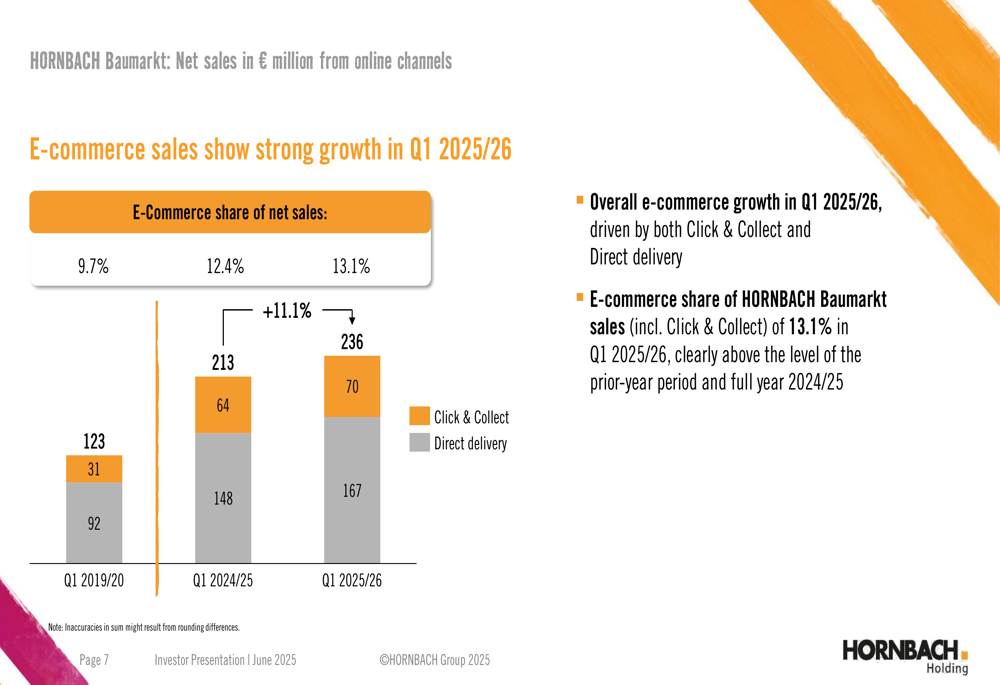

HORNBACH’s digital transformation continues to show strong results, with e-commerce sales growing to €236 million in Q1 2025/26, up from €213 million in the same period last year. The e-commerce share of total net sales increased to 13.1%, compared to 12.4% in Q1 2024/25.

The company’s omnichannel strategy is illustrated in the following chart showing the growth of both Click & Collect and Direct delivery sales channels:

Both Click & Collect sales (€70 million, up from €64 million) and Direct delivery (€167 million, up from €148 million) showed healthy growth, indicating customer adoption of both convenience options. The consistent growth in e-commerce sales since Q1 2019/20 demonstrates HORNBACH’s successful adaptation to changing consumer shopping preferences.

Financial Position and Cash Flow

HORNBACH reported a strong financial position with significant improvements in cash flow. Cash flow from operating activities increased substantially to €192.0 million in Q1 2025/26, compared to €58.3 million in the same period last year, primarily due to successful inventory management and the strong spring season.

Free cash flow after net CAPEX and dividends reached €147.4 million, more than triple the €43.0 million reported in Q1 2024/25. This improvement mainly reflects the positive change in working capital.

The company’s balance sheet remains robust, with an equity ratio of 45.5% as of May 31, 2025, up from 44.1% at the end of February 2025. Net leverage (measured as net debt to EBITDA) improved to 2.3x from 2.6x in February 2025.

Capital expenditures increased significantly to €47.7 million in Q1 2025/26, more than double the €23.4 million spent in the prior-year period. The CAPEX was allocated to land and new stores (58%), store conversions and equipment (32%), and software (10%), reflecting the company’s continued investment in growth and modernization.

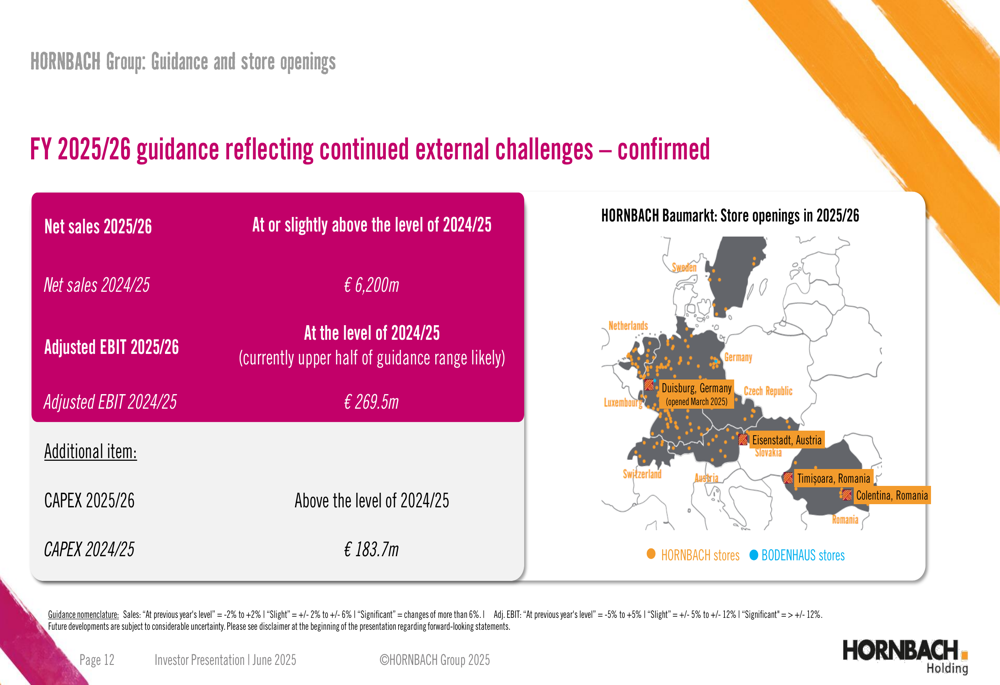

Guidance and Outlook

Despite the strong first-quarter performance, HORNBACH maintained its guidance for the full fiscal year 2025/26, citing "continued external challenges." The company expects:

- Net sales at or slightly above the level of 2024/25 (€6,200 million)

- Adjusted EBIT at the level of 2024/25 (€269.5 million), though the company noted that results in the "upper half of guidance range" are likely based on current performance

- Capital expenditures above the level of 2024/25 (€183.7 million)

The company’s expansion plans for fiscal year 2025/26 are illustrated in the following map showing planned store openings:

HORNBACH’s cautious guidance despite the strong Q1 results suggests management anticipates potential headwinds in the coming quarters, even as it continues to invest in growth opportunities across its European markets.

In summary, HORNBACH’s Q1 2025/26 presentation revealed a company performing well in a competitive environment, with strong sales growth, improved profitability, and solid financial position. The company’s market share gains and e-commerce growth highlight its successful strategic positioning, while its continued investment in store expansion demonstrates confidence in its long-term growth prospects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.