Bank of America, Morgan Stanley, Nvidia and Dollar Tree rise premarket

Introduction & Market Context

Humanica PCL (SET:HUMAN), Southeast Asia’s self-proclaimed leading HR solutions provider, presented its Q2 2025 financial results on August 22, 2025. The company’s stock closed at 6.85 baht, hovering closer to its 52-week low of 6.4 baht than its high of 11.9 baht, suggesting cautious investor sentiment despite the company’s strategic expansion efforts.

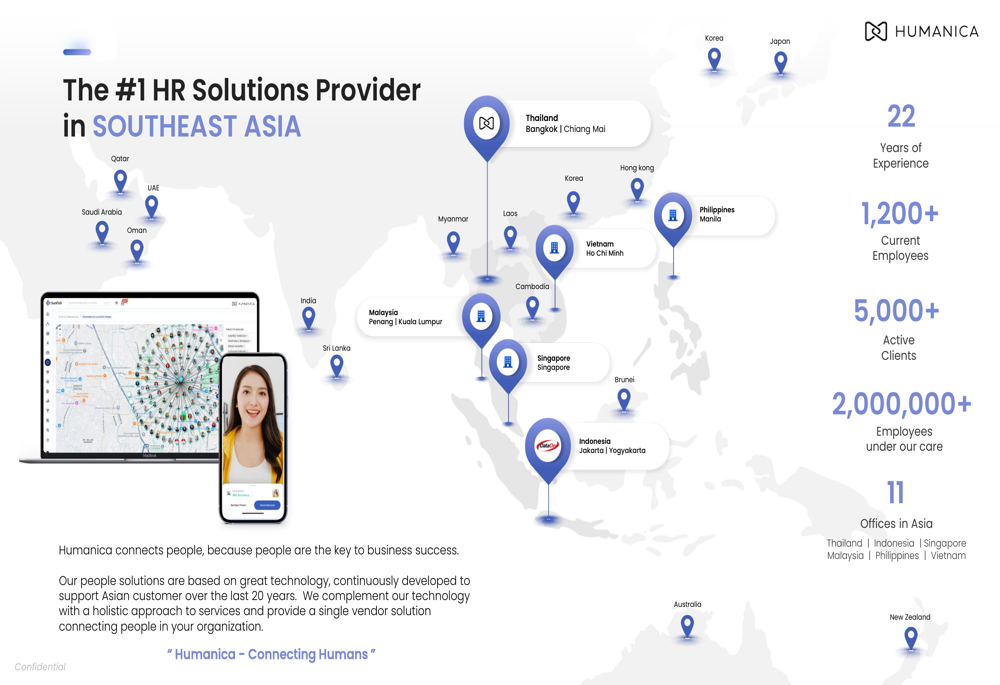

With 22 years of experience and a presence across six Southeast Asian countries through 11 offices, Humanica serves over 5,000 active clients and manages HR solutions for more than 2 million employees. The company’s presentation highlighted its continued focus on expanding recurring revenue streams and strengthening its regional footprint, particularly through its recent acquisition of Cadena in Vietnam.

Quarterly Performance Highlights

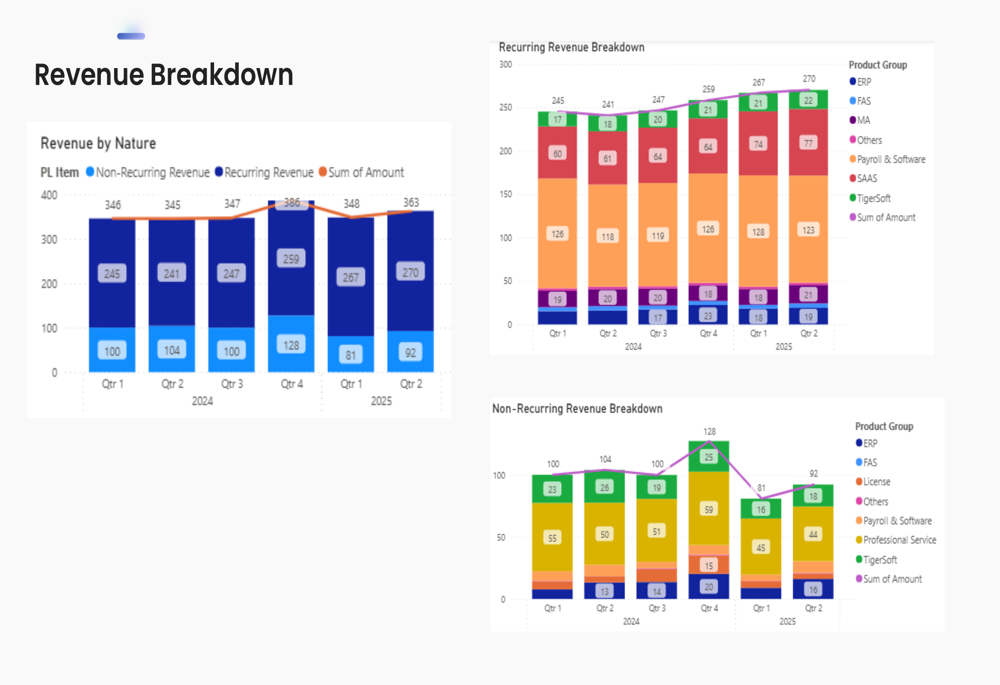

Humanica reported modest financial growth for Q2 2025, with revenue increasing by 3% year-to-date compared to 2024. The company’s gross profit also grew by 3% (+11 million baht), while operating profit and earnings before tax (EBT) both increased by 8% (+14 million baht and +15 million baht respectively). However, net profit decreased slightly by 0.6% (-1 million baht), suggesting increased operational costs or tax implications.

A key positive indicator was the company’s growing recurring revenue base, which increased from 70% in 2024 to 76% in 2025, demonstrating progress in the company’s strategy to build more predictable revenue streams.

The quarterly analysis shows similar trends, with the company maintaining its focus on building recurring revenue, which grew from 70% in Q2 2024 to 75% in Q2 2025.

Humanica’s revenue breakdown by product group reveals the company’s diversified portfolio approach, with enterprise resource planning (ERP) solutions generating significant recurring and non-recurring revenue streams.

Strategic Initiatives & Expansion

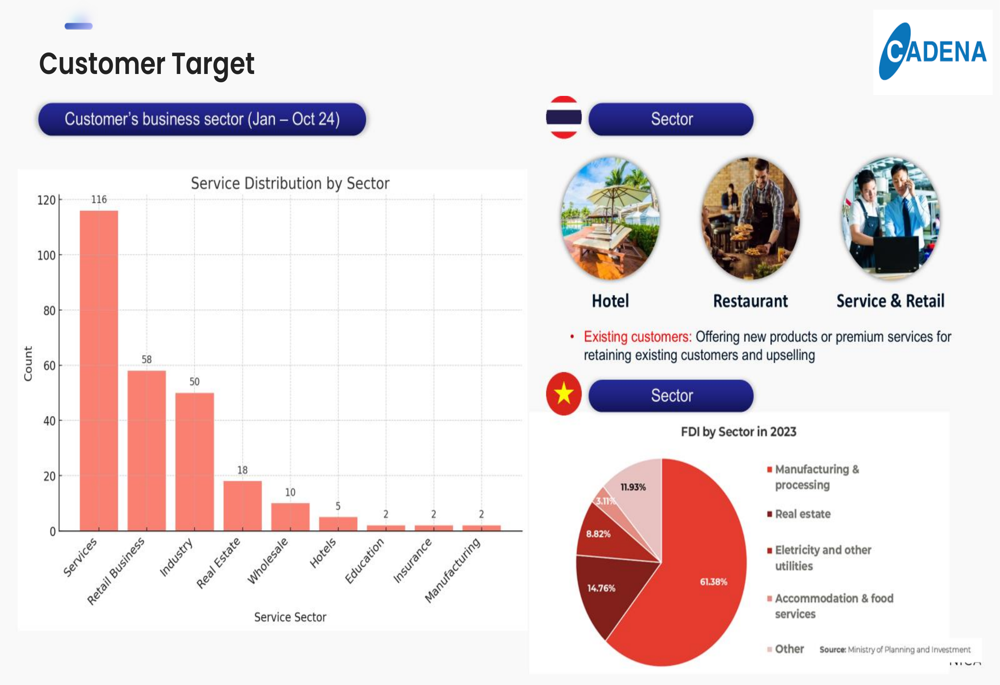

A significant highlight of Humanica’s presentation was its recent acquisition of Cadena, strengthening the company’s presence in Vietnam. Cadena brings 22+ years of experience, serves over 200,000 payslips, operates in 10 countries, and employs more than 100 people.

The acquisition positions Humanica more competitively in Vietnam’s HR information systems market, where it now competes with established players like FPT (operating since 2011) and VNResource. Cadena’s customer base spans multiple sectors, with particularly strong representation in services (116 clients), retail (58), and industrial businesses (50).

Humanica continues to diversify its solutions portfolio across four key areas: Enterprise HCM Solutions (including SunFish and Workplaze), Managed Payroll Services, SME HR Technology Solutions (Tigersoft and GreatDay HR), and Emerging Businesses. This comprehensive approach allows the company to serve various market segments while exploring growth opportunities in adjacent technology sectors.

Financial Position & Outlook

Despite the modest revenue growth, Humanica’s financial position showed some concerning trends. The company reported a 7.5% decrease in assets and a 7% decrease in equity (-54 million baht). These figures, coupled with the slight decline in net profit, suggest potential challenges in maintaining profitability while pursuing expansion.

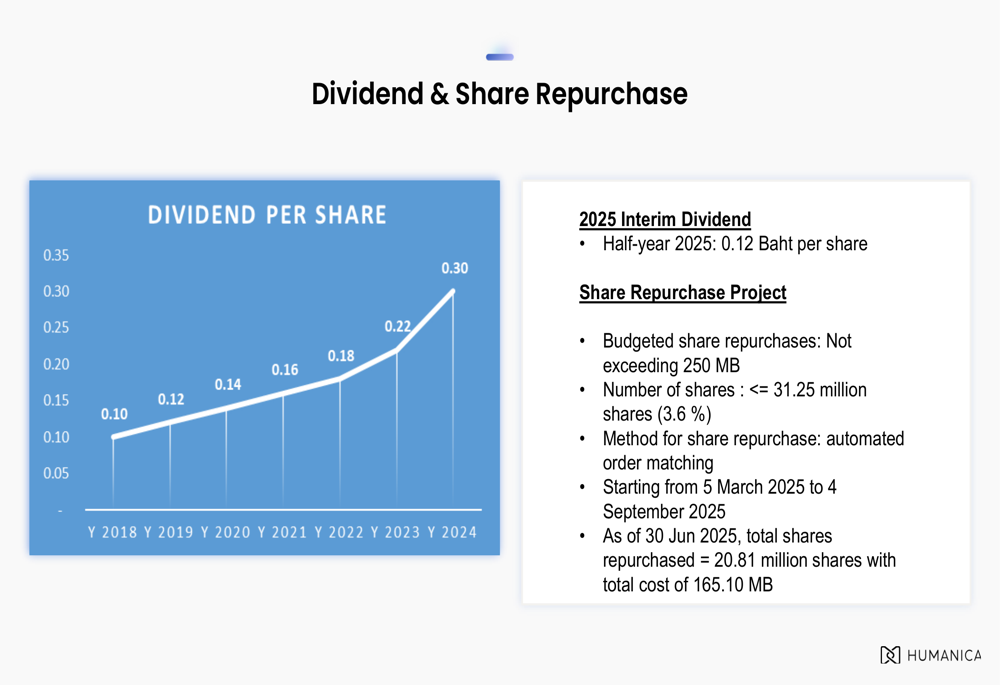

On a positive note, Humanica announced an interim dividend of 0.12 baht per share for 2025 and continued its share repurchase program with a budget of 250 million baht. As of the presentation date, the company had repurchased 20.81 million shares, demonstrating confidence in its long-term value proposition.

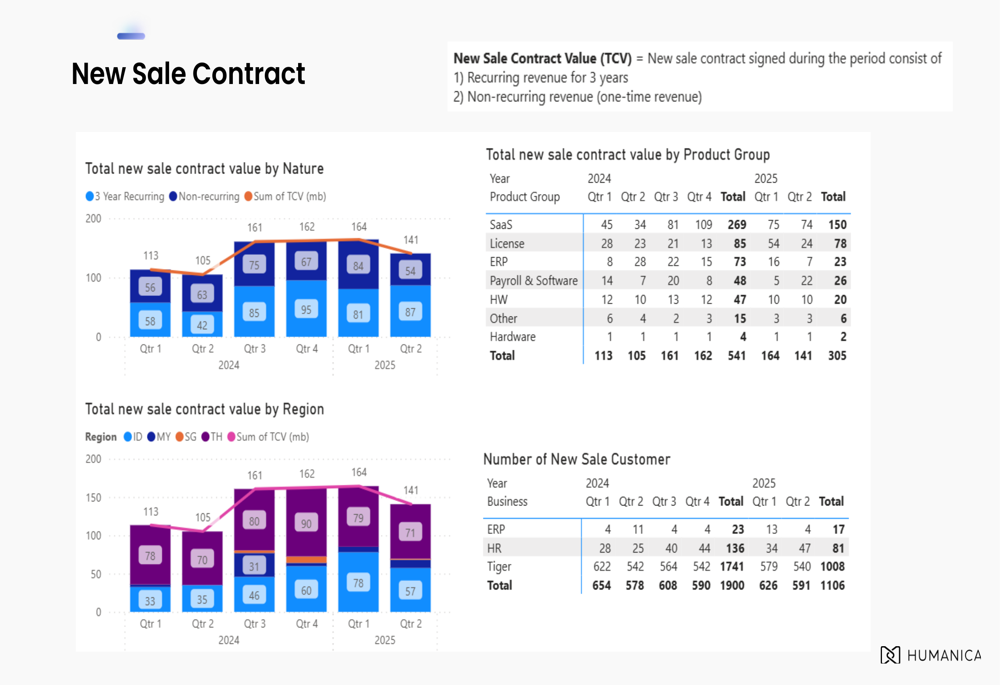

New sales contracts showed promising activity, particularly in the ERP segment with 1,741 new contracts signed. The company reported 1,106 new business closures, indicating continued market traction despite competitive pressures.

Competitive Industry Position

Humanica’s presentation emphasized its position as the "#1 HR Solutions Provider in Southeast Asia," though this claim wasn’t substantiated with market share data. The company’s acquisition strategy, particularly the Cadena purchase, appears designed to strengthen its competitive position in key markets like Vietnam.

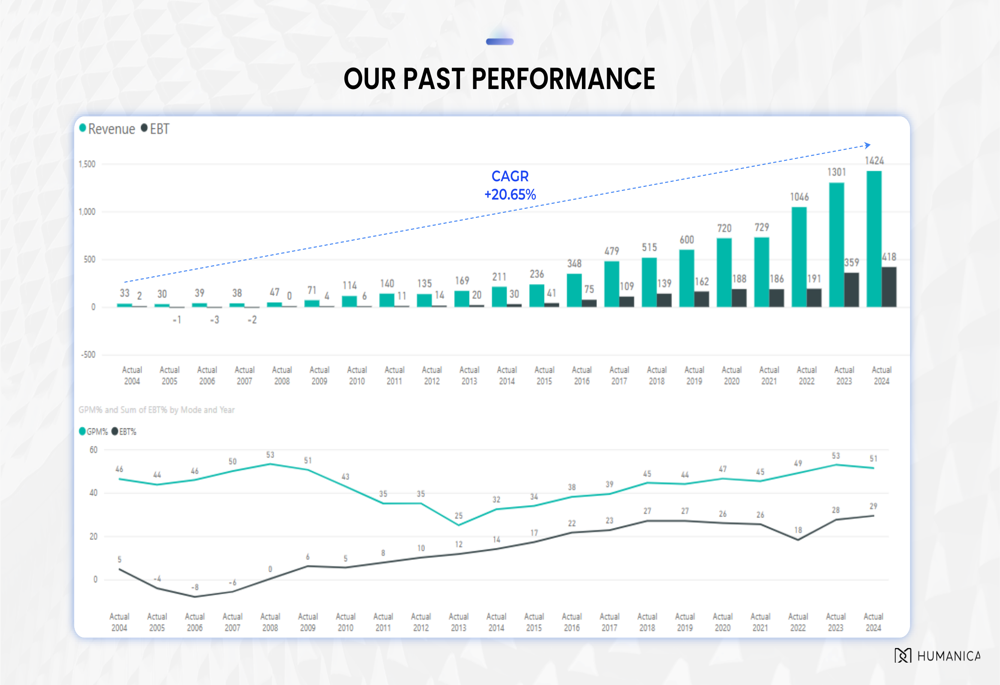

The company’s historical performance shows a compound annual growth rate (CAGR) of 20.65%, suggesting strong long-term momentum despite the more modest recent quarterly results.

Conclusion

Humanica’s Q2 2025 results present a mixed picture: modest revenue growth and improved operating profits are positive indicators, while the slight decline in net profit and reduced asset base suggest potential challenges. The company’s strategic focus on expanding recurring revenue streams appears to be yielding results, with recurring revenue now comprising 76% of total revenue.

The Cadena acquisition represents a significant strategic move to strengthen Humanica’s position in Vietnam and potentially accelerate growth in that market. However, investors may remain cautious until the company demonstrates that its expansion strategy can deliver more substantial bottom-line improvements.

With the stock trading closer to its 52-week low than high, market sentiment appears to reflect this cautious outlook, even as Humanica continues to position itself for long-term growth across Southeast Asia’s HR solutions market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.