One & One Green Technologies stock soars 100% after IPO debut

Introduction & Market Context

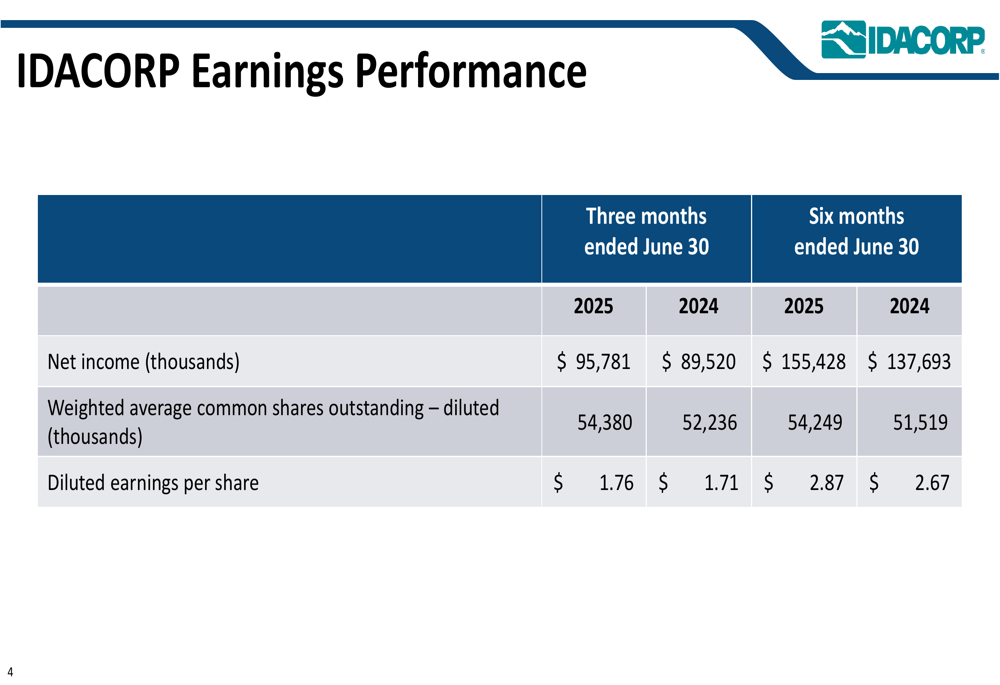

IDACORP, Inc. (NYSE:IDA) reported second-quarter 2025 earnings on July 31, posting solid results with diluted earnings per share of $1.76, up from $1.71 in the same period last year. The utility company’s stock closed up 2.28% at $122.54 during regular trading but slipped 1.13% to $121.15 in after-hours trading following the earnings release.

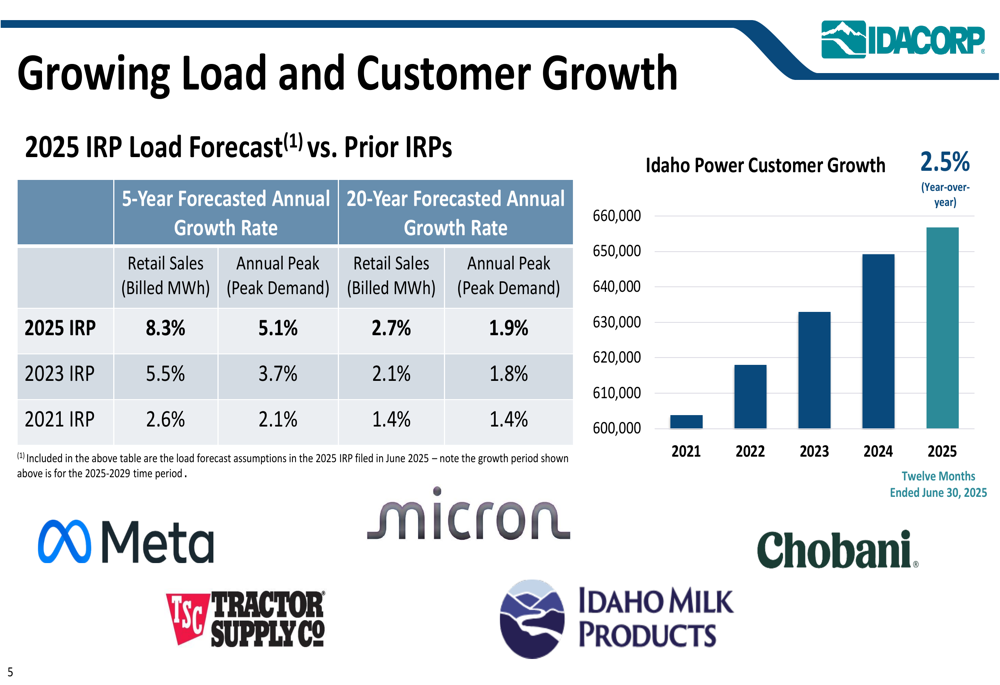

The company’s performance reflects continued strong customer growth in its Idaho Power service territory, with the customer base expanding 2.5% year-over-year to 659,000. This growth, coupled with strategic investments in transmission and generation capacity, positions IDACORP to meet accelerating demand forecasts in its service area.

Quarterly Performance Highlights

IDACORP reported net income of $95.8 million for the second quarter of 2025, compared to $89.5 million for the same period in 2024, representing a 7% increase. For the first six months of 2025, net income reached $155.4 million, up 12.9% from $137.7 million in the first half of 2024.

As shown in the following earnings performance table:

The company’s diluted earnings per share for the first half of 2025 reached $2.87, a 7.5% increase from $2.67 in the same period last year. This growth came despite a 4.1% increase in outstanding shares, reflecting strong underlying performance.

A key driver of IDACORP’s performance has been its expanding customer base. The company’s customer growth chart illustrates the consistent upward trend:

Customer growth has been supported by continued investment from major commercial and industrial customers, including Meta (NASDAQ:META), Micron (NASDAQ:MU), and Chobani. This growth has contributed to a significant upward revision in IDACORP’s load forecasts, with the 2025 Integrated Resource Plan (IRP) now projecting 8.3% annual retail sales growth over the next five years, up from 5.5% in the 2023 IRP.

Strategic Initiatives

IDACORP highlighted several strategic initiatives aimed at meeting growing demand while transitioning to cleaner energy sources. A centerpiece of these efforts is the Boardman-to-Hemingway (B2H) transmission line project, which broke ground in June 2025 and is expected to enter service in late 2027. Idaho Power holds approximately 45% interest in this project, which has received regulatory approvals from Oregon, Idaho, and Wyoming utility commissions.

The B2H project represents a critical infrastructure investment:

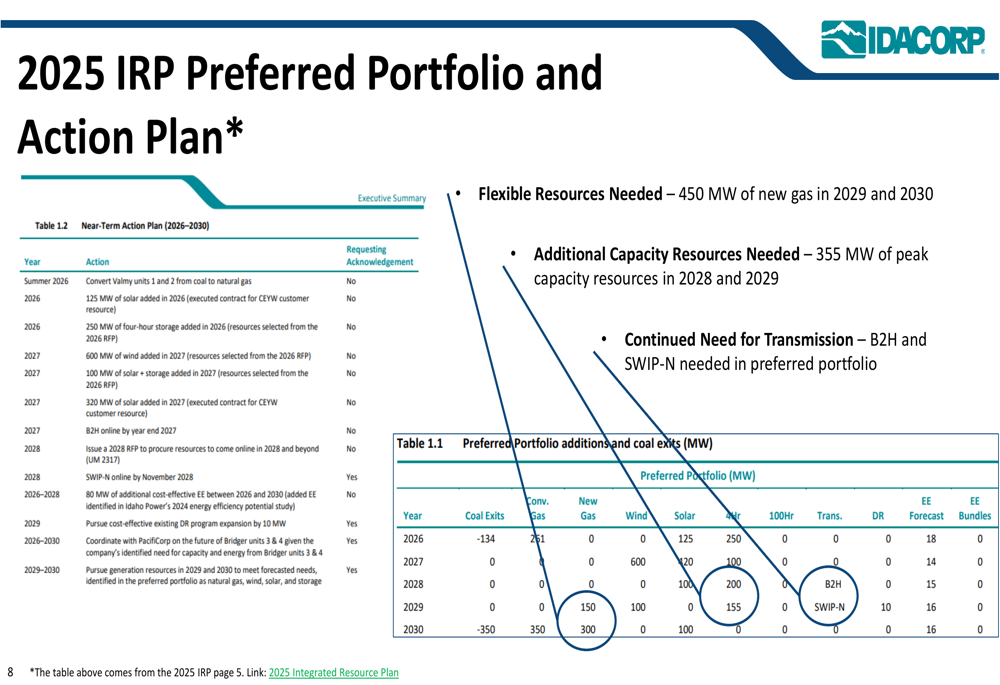

The company’s 2025 Integrated Resource Plan outlines a comprehensive approach to meeting future energy needs, including a mix of natural gas, wind, solar, and battery storage resources. The plan calls for adding 600 MW of wind capacity in 2027, along with other significant resource additions:

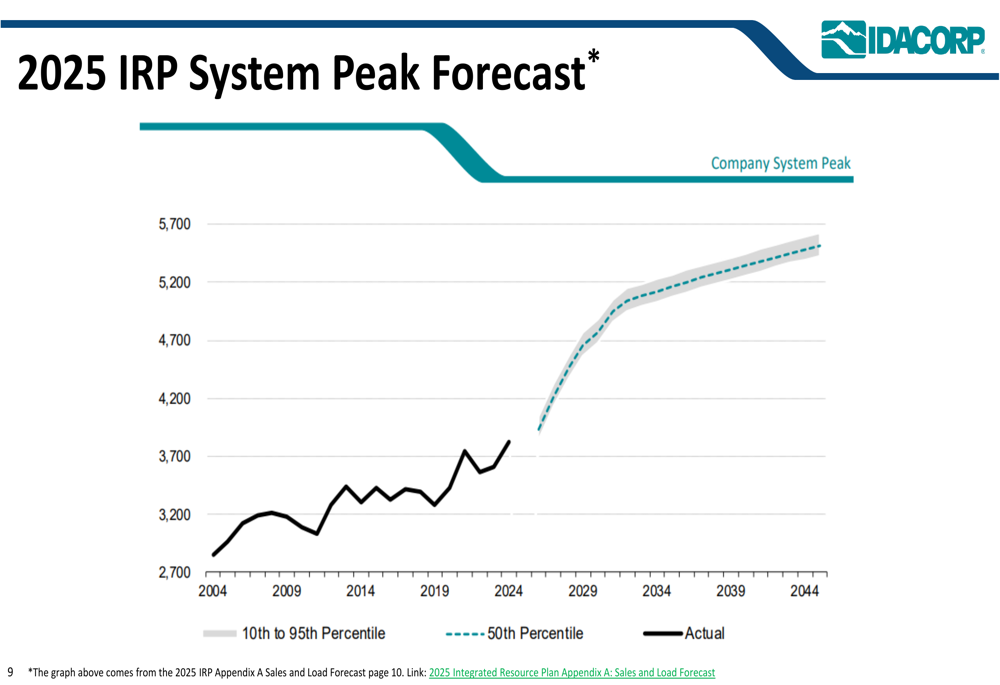

IDACORP’s system peak forecast shows the expected growth in demand that necessitates these investments:

To support this growth, the company has issued multiple Requests for Proposals (RFPs) for new generation resources. The 2028 RFP final shortlist includes 300 MW of solar through asset purchase, 80 MW of solar through power purchase agreements (PPAs), and various other solar, wind, and battery storage projects. The 2029+ RFP final shortlist includes additional solar, wind, battery storage, and 167 MW of natural gas generation.

Forward-Looking Statements

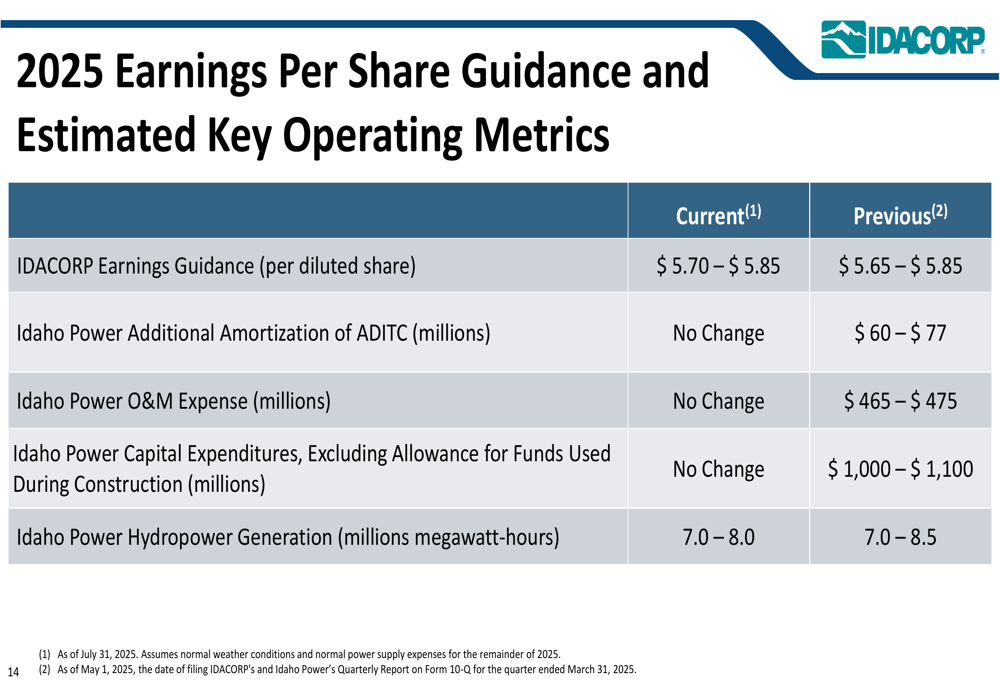

IDACORP has narrowed and slightly raised its 2025 earnings guidance to $5.70-$5.85 per diluted share, compared to the previous range of $5.65-$5.85. The company maintained its capital expenditure forecast of $1.0-$1.1 billion for 2025 and expects hydropower generation of 7.0-8.0 million megawatt-hours.

The updated guidance reflects management’s confidence in continued growth:

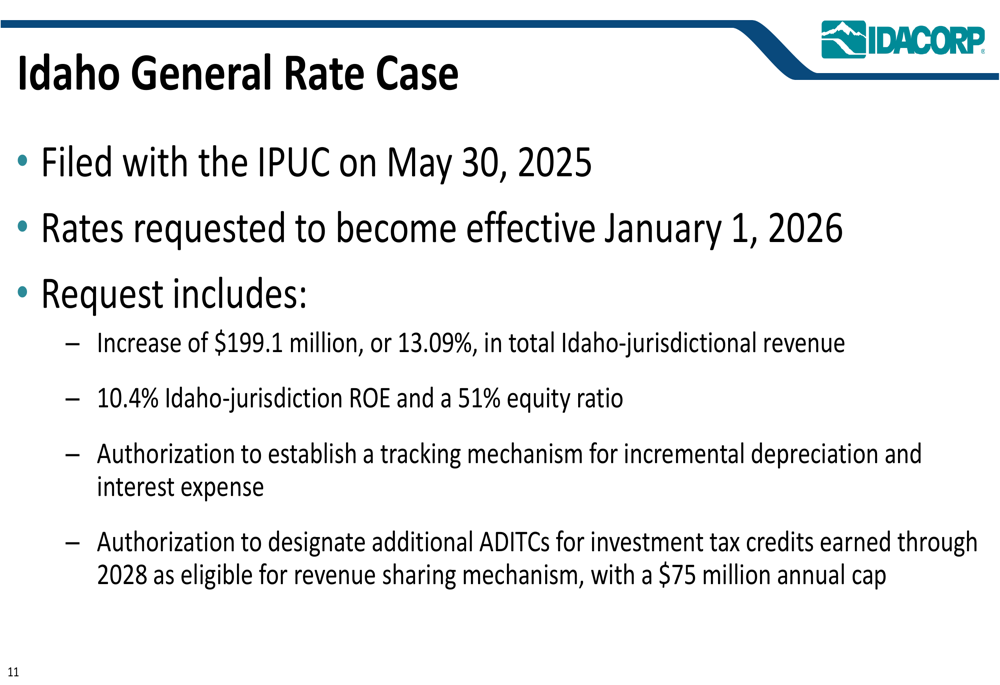

A significant development for future earnings is the Idaho General Rate Case filed on May 30, 2025. The company is requesting a $199.1 million (13.09%) increase in Idaho-jurisdictional revenue, with rates to become effective January 1, 2026. The filing includes a requested 10.4% return on equity and a 51% equity ratio.

Detailed Financial Analysis

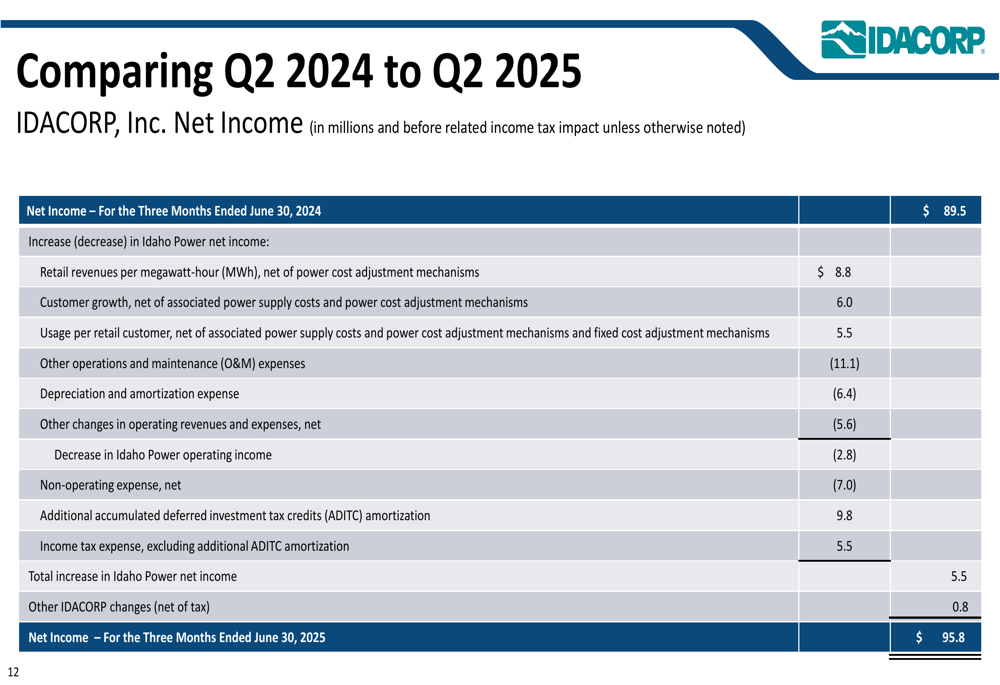

IDACORP provided a detailed breakdown of the factors contributing to its Q2 2025 performance compared to Q2 2024. The $6.3 million increase in net income was driven by several factors, including higher retail revenues per megawatt-hour ($8.8 million), customer growth ($6.0 million), and increased usage per customer ($5.5 million).

These positive factors were partially offset by higher operations and maintenance expenses ($11.1 million), increased depreciation and amortization ($6.4 million), and other operating expenses ($5.6 million). The company also benefited from $9.8 million in additional accumulated deferred investment tax credits (ADITC) amortization and a $5.5 million reduction in income tax expense.

The following breakdown illustrates these changes:

IDACORP maintains a strong liquidity profile with $100 million available at the holding company level and $400 million at Idaho Power. The company also has $143.5 million available through its at-the-market offering program and $560.4 million in potential proceeds from forward sale agreements.

This financial position supports IDACORP’s ambitious capital expenditure plans, which are necessary to meet the accelerating growth in its service territory. The company’s investment strategy aligns with its updated load forecasts, which show significantly higher expected growth compared to previous projections.

Analyst Perspectives

While IDACORP’s Q2 results showed solid growth, the slight decline in after-hours trading suggests investors may have had higher expectations or concerns about the company’s ability to execute its ambitious growth plans. The stock is currently trading near the middle of its 52-week range of $98.19 to $125.97.

Following the company’s Q1 2025 results, analysts had set price targets ranging from $121 to $135, according to the previous earnings report. IDACORP’s P/E ratio was 21.2x after Q1 results, reflecting premium valuation compared to some utility peers.

The company’s request for a significant rate increase in Idaho represents both an opportunity and a risk, as regulatory approval is not guaranteed. However, the strong customer growth and increasing load forecasts provide a solid foundation for the requested increase.

IDACORP’s consistent dividend history—having raised dividends for 13 consecutive years—continues to make it attractive to income-focused investors. The company’s strategic investments in transmission and renewable energy position it well for long-term growth, though execution risks remain given the scale of planned projects and the rapidly evolving energy landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.